Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-1

Chapter 8

Lecture Notes

Chapter theme: This chapter explains how to prepare

flexible budgets and how to compare them to actual results

I. The variance analysis cycle

A. The steps of the cycle

i. The cycle begins with the preparation of

performance reports in the accounting

department.

ii. These reports highlight variances which are

iii. The variances raise questions such as:

1. Why did this variance occur?

2

5

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-2

II. Flexible budgets

A. Characteristics of a flexible budget

i. A planning budget is prepared before the period

begins and is valid for only the planned level of

activity.

1. If the actual level of activity differs from

ii. A flexible budget is an estimate of what revenues

and costs should have been, given the actual level

of activity for the period. Flexible budgets:

4

22

2

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

B. Larry’s Lawn Service: Illustrating the deficiencies

of the static planning budget

i. Assume the following facts with respect to Larry’s

ii. Assume that Larry prepared the planning budget

for June as shown. Notice that the budget includes:

1. Two variable costs—gasoline and supplies

iii. Assume that Larry’s actual results for the month

of June are as shown. Notice:

1. Larry actually mowed 550 lawns.

iv. If Larry wanted to, he could compare his actual

results to the planning budget as shown on this

slide. Notice:

1. A variance is computed for revenue and

8

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-4

3. A favorable (unfavorable) revenue variance

occurs when actual revenue is greater than

(less than) the planning budget.

6. At this point, we cannot answer this question

because the actual level of activity is

greater than the planned level of activity.

C. How a flexible budget works

i. Keys to understanding a flexible budget

1. Variable costs change in direct proportion to

14

11

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-5

ii. Larry’s Lawn Service: preparing a flexible

budget

1. Larry’s flexible budget for an activity level

of 550 lawns mowed is as shown on this

slide. Notice, the “Q” in all revenue and

2. The fixed costs in Larry’s flexible budget

are not sensitive to changes in the activity

level.

Learning Objective 8-2: Prepare a report showing

revenue and spending variances.

D. Computing revenue and spending variances

i. A revenue variance is the difference between what

15

19

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-6

E. Larry’s Lawn Service: Computing revenue and

spending variances

i. The revenue and spending variances for Larry’s

Lawn Service would be computed as shown on this

slide. Notice:

1. The apple icons on the slide indicate that the

actual results and flexible budget columns

III. Flexible budgets with multiple cost drivers

Learning Objective 8-3: Prepare a flexible budget with

more than one cost driver.

A. Key concepts

i. More than one cost driver may be needed to

21

22

24

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-7

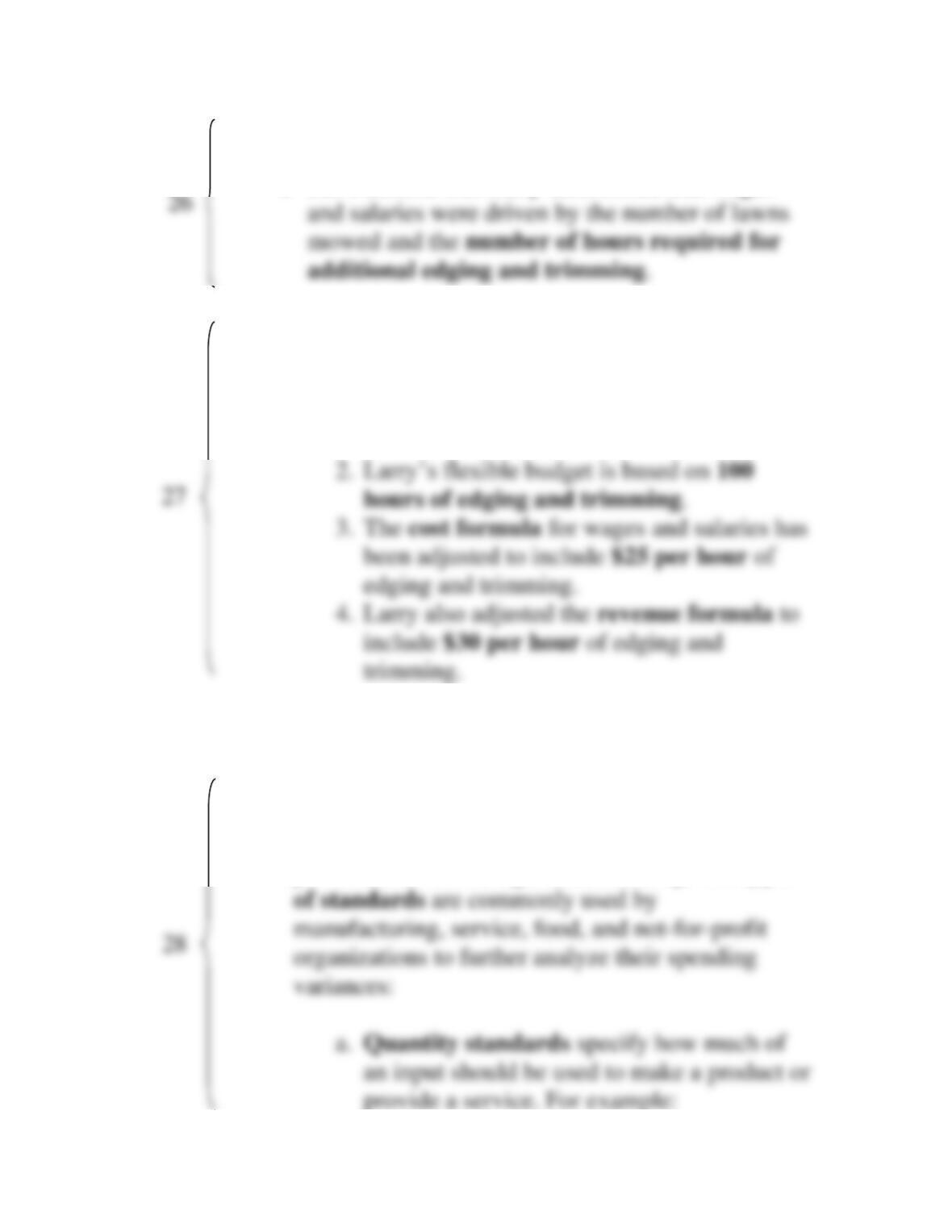

I. Larry’s Lawn Service: Multiple cost drivers

i. Let’s assume that Larry determined that wages

ii. Larry’s flexible budget could easily be adjusted to

accommodate the second cost driver. Notice:

1. The number of hours (H) is designated as

the second cost driver.

IV. Standard costs – setting the stage

A. Basic definitions/concepts

1. A standard is a benchmark for measuring

performance. In managerial accounting, two types

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-8

a. Auto service centers like Firestone

b. Price standards specify how much should

be paid for each unit of the input. For

example:

a. Hospitals have standard costs for

food, laundry, and other items.

b. Home construction companies have

B. Setting direct materials standards

i. The standard quantity per unit for direct

materials should reflect the amount of material

28

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-9

C. Setting direct labor standards

i. The standard hours per unit reflects the labor

hours required to complete one unit of product.

1. Standards can be determined by using

ii. The standard rate per hour for direct labor

includes not only wages earned but also fringe

benefits and other labor costs.

1. Many companies prepare a single rate for

all employees within a department that

reflects the “mix” of wage rates earned.

D. Setting variable manufacturing overhead standards

i. The quantity standard for variable manufacturing

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-10

E. The standard cost card

i. The standard cost card is a detailed listing of the

V. Using standards in flexible budgets

A. Breaking down spending variances

i. Standard costs per unit for direct materials, direct

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-11

VI. A general model for standard cost variance analysis

A. Price and quantity variances

i. A price variance is the difference between the

B. Price and quantity standards

i. Price and quantity standards are determined

separately because price and quantity variances

usually have different causes. In addition:

1. Different managers are usually

responsible for buying and for using

inputs. For example:

2. The buying and using activities occur at

different points in time. For example:

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-12

C. The general model—an overview

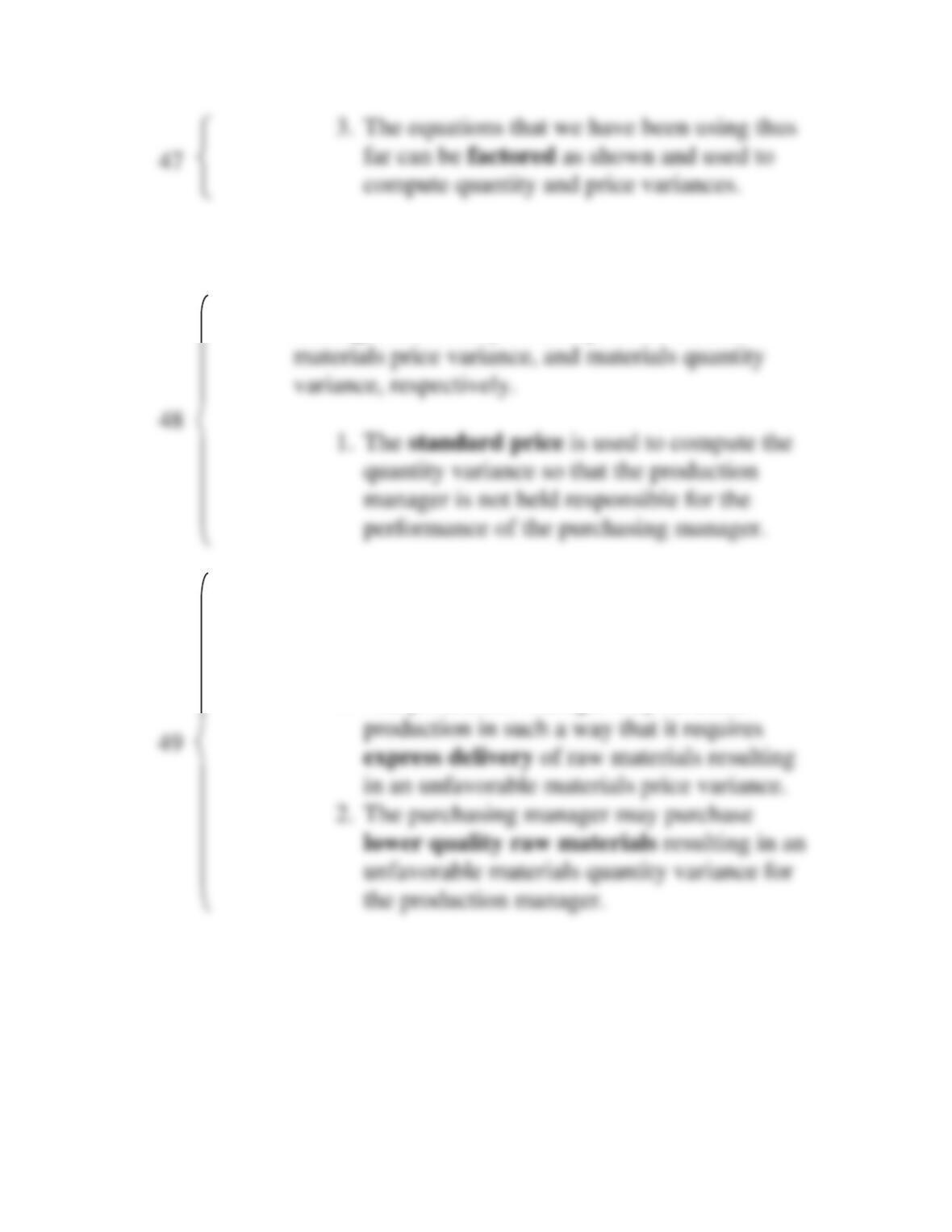

i. Price and quantity variances can be computed for

all three variable cost elements – direct materials,

1. The actual quantity represents the actual

amount of direct materials, direct labor, and

variable manufacturing overhead used.

Helpful Hint: Emphasize that the quantities in this

38

41

42

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-13

2. The standard quantity represents the

standard quantity allowed for the actual

output of the period.

Helpful Hint: Mention that the “SQ” portion of the

3. The actual price represents the actual

VII. Using standard costs—direct materials variances

Learning Objective 8-4: Compute the direct materials

39

46

45

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

A. Glacier Peak Outfitters – an example

i. The materials price variance, defined as the

difference between what is paid for a quantity of

ii. The materials quantity variance, defined as the

difference between the quantity of materials used in

production and the quantity that should have been

used according to the standard, is $50 unfavorable.

Helpful Hint: Remind students that a favorable price

variance might not always be a good thing. If it arose

iii. Supporting/additional computations

1. The standard quantity of 200 kilograms was

43

44

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-15

B. Direct materials variances—points of clarification:

i. The purchasing manager and production

manager are usually held responsible for the

ii. The materials variances are not always entirely

controllable by one person or department. For

example:

1. The production manager may schedule

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-16

VIII. Using standard costs—direct labor variances

Learning Objective 8-5: Compute the direct labor rate

and efficiency variances and explain their significance.

A. Glacier Peak Outfitters – continued (assume the

information as shown)

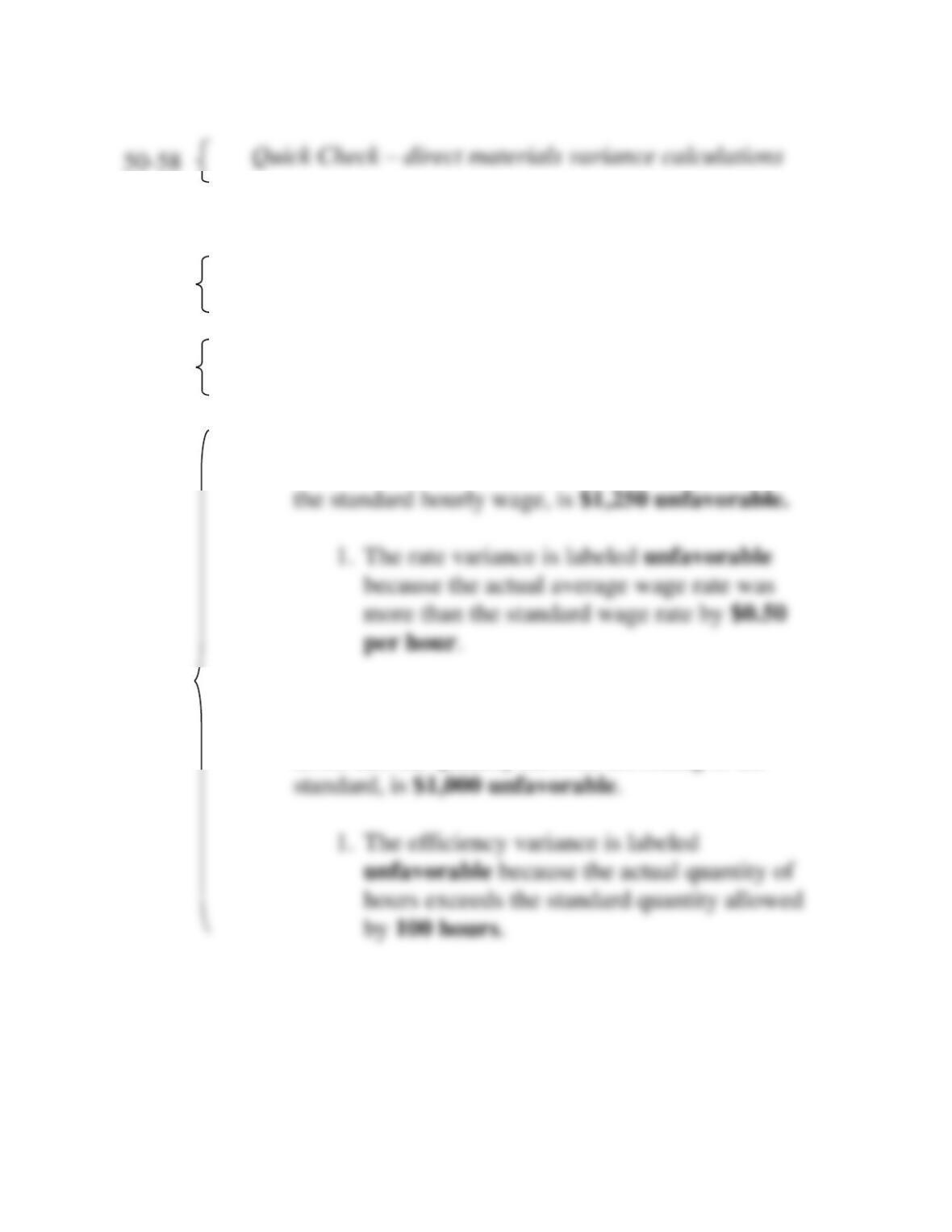

i. The labor rate variance, defined as the difference

between the actual average hourly wage paid and

ii. The labor efficiency variance, defined as the

difference between the actual quantity of labor

hours and the quantity allowed according to the

60

59

61

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-17

iii. Supporting/additional computations

1. The standard quantity of 2,400 hours was

B. Direct labor variances—points of clarification:

i. Labor variances are partially controllable by

employees within the Production Department. For

example, production managers/supervisors can

influence:

1. The deployment of highly skilled workers

ii. However, labor variances are not entirely

controllable by one person or department. For

example:

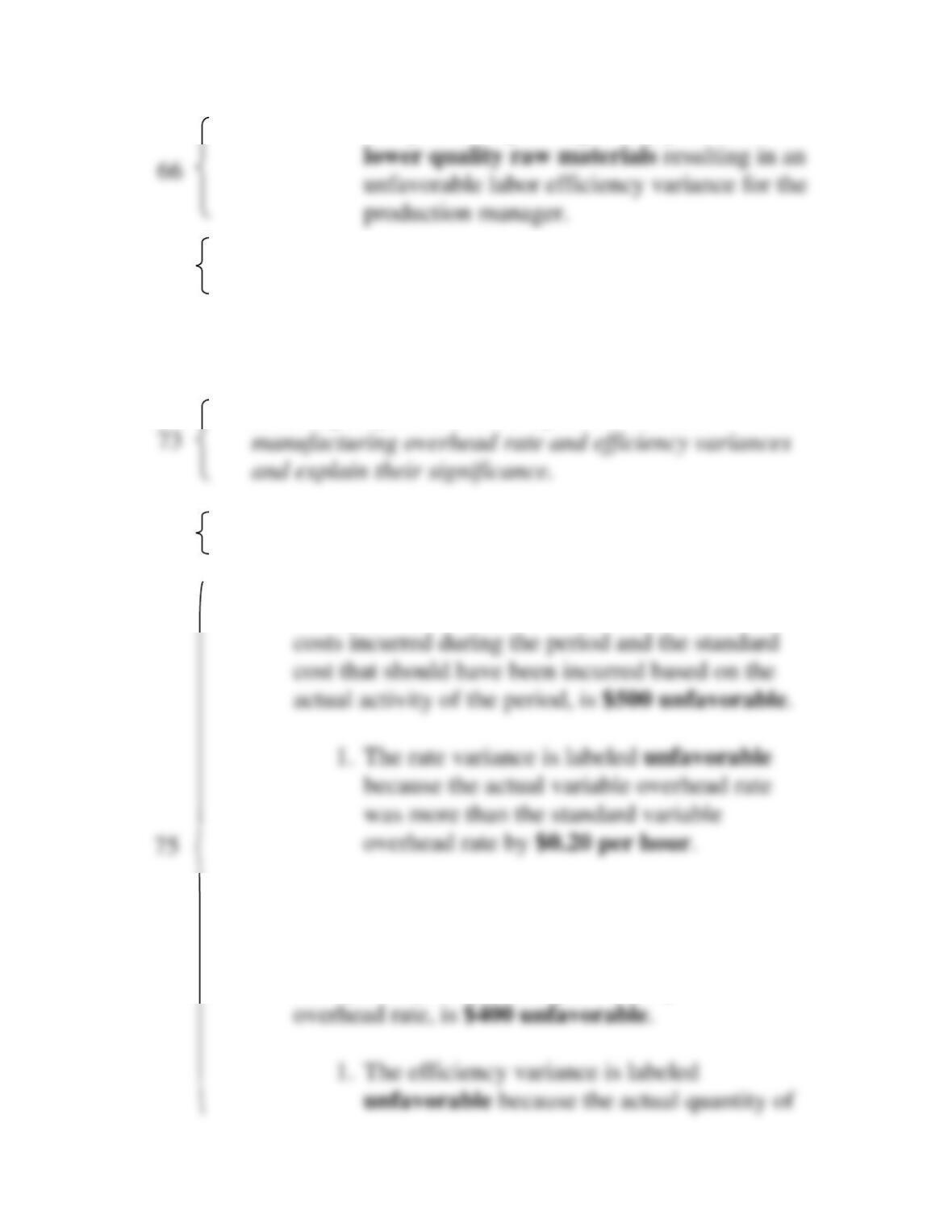

1. The Maintenance Department may do a

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-18

2. The purchasing manager may purchase

Quick Check – direct labor variance calculations

IX. Using standard costs—variable manufacturing

overhead variances

Learning Objective 8-6: Compute the variable

A. Glacier Peak Outfitters – continued

i. The variable overhead rate variance, defined as

the difference between the actual variable overhead

ii. The variable overhead efficiency variance,

defined as the difference between the actual activity

of a period and the standard activity allowed,

multiplied by the variable part of the predetermined

67–72

74

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis

8-19

iii. Supporting/additional computations

1. The standard quantity of 2,400 hours was

Quick Check – variable overhead variance calculations

X. Materials variances—an important subtlety

A. When the quantity of materials purchased differs

B. Glacier Peak Outfitters—revisited

i. The materials quantity variance is computed

79–84

86