8-721

208.

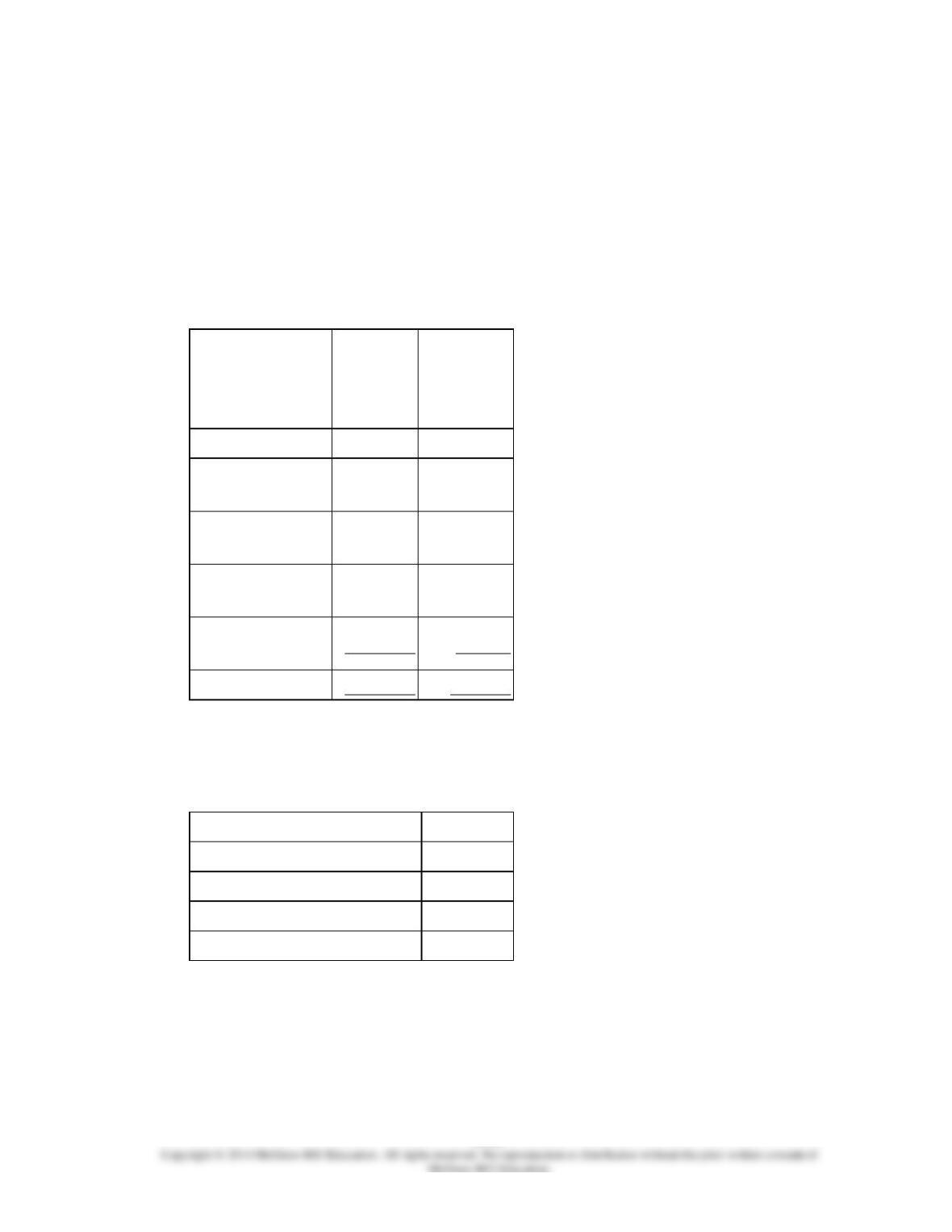

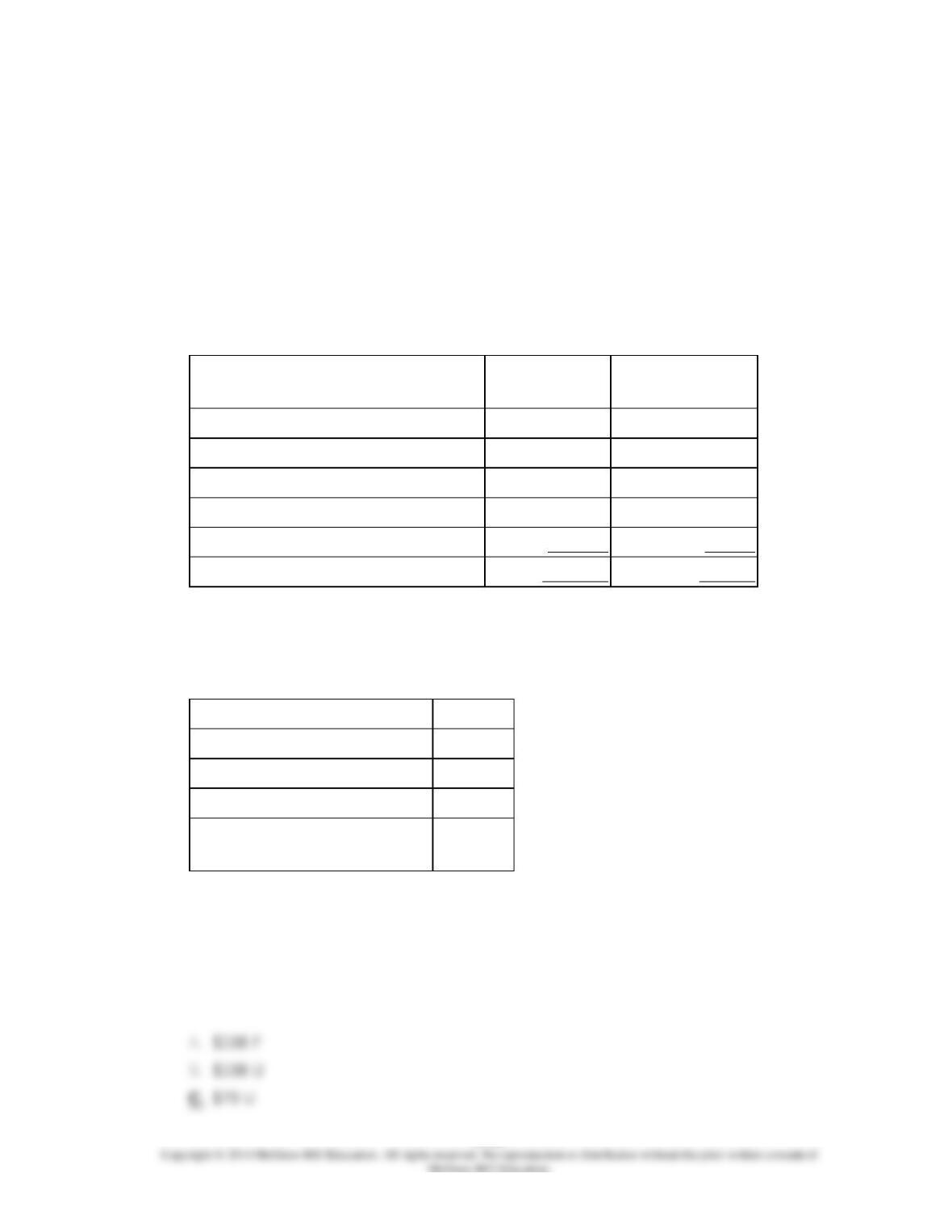

Wesolick Clinic uses client-visits as its measure of activity. During August, the clinic

budgeted for 2,900 client-visits, but its actual level of activity was 2,870 client-visits. The

clinic has provided the following data concerning the formulas used in its budgeting and

its actual results for August:

Data used in budgeting:

Fixed

element

per

month

Variable

element

per client-

visit

Revenue

−

$40.50

Personnel

expenses

$30,900

$12.80

Medical

supplies

1,400

5.60

Occupancy

expenses

7,500

2.00

Administrative

expenses

6,300

0.20

Total expenses

$46,100

$20.60

Actual results for August:

Revenue

$120,375

Personnel expenses

$65,916

Medical supplies

$16,872

Occupancy expenses

$13,200

Administrative expenses

$6,974

The spending variance for medical supplies in August would be closest to:

8-723

209.

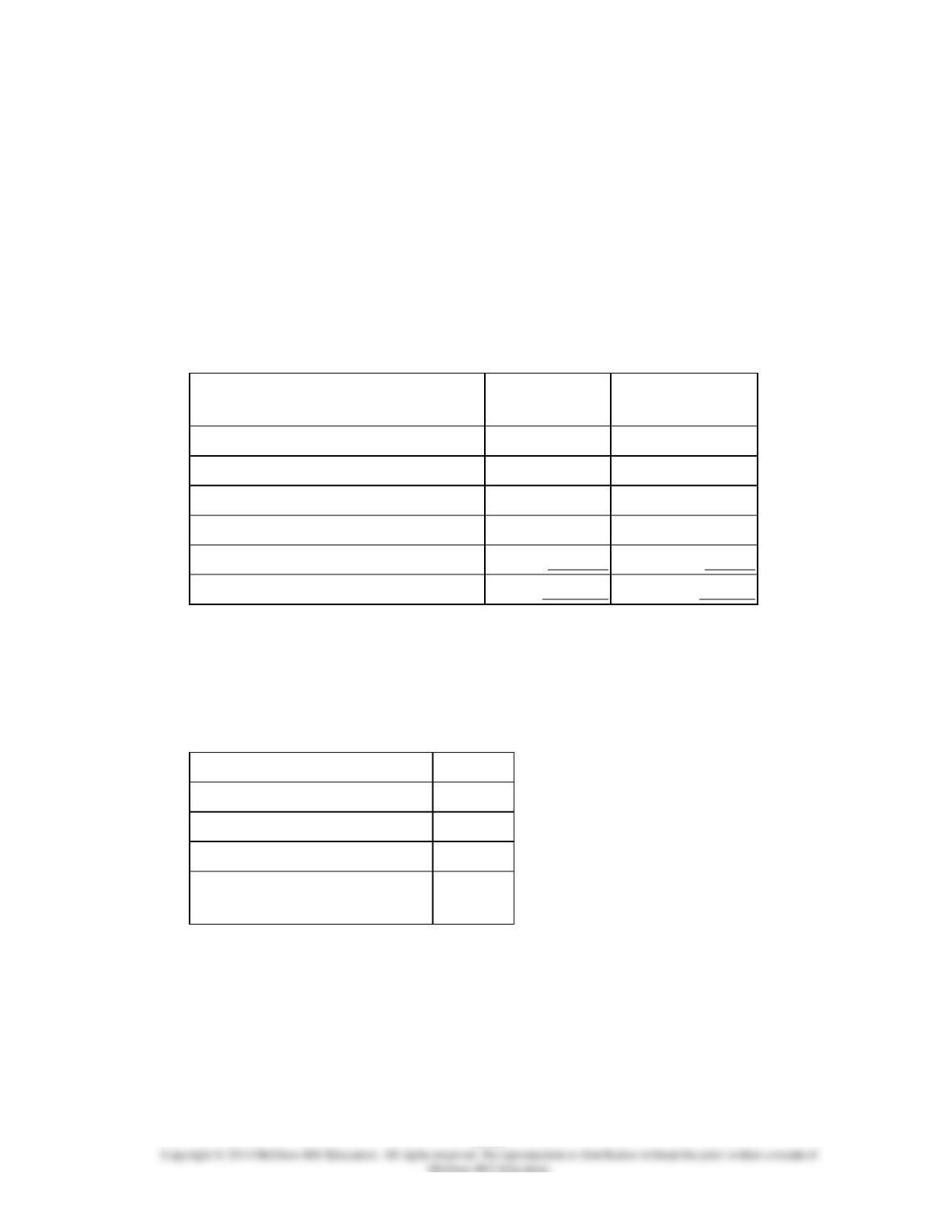

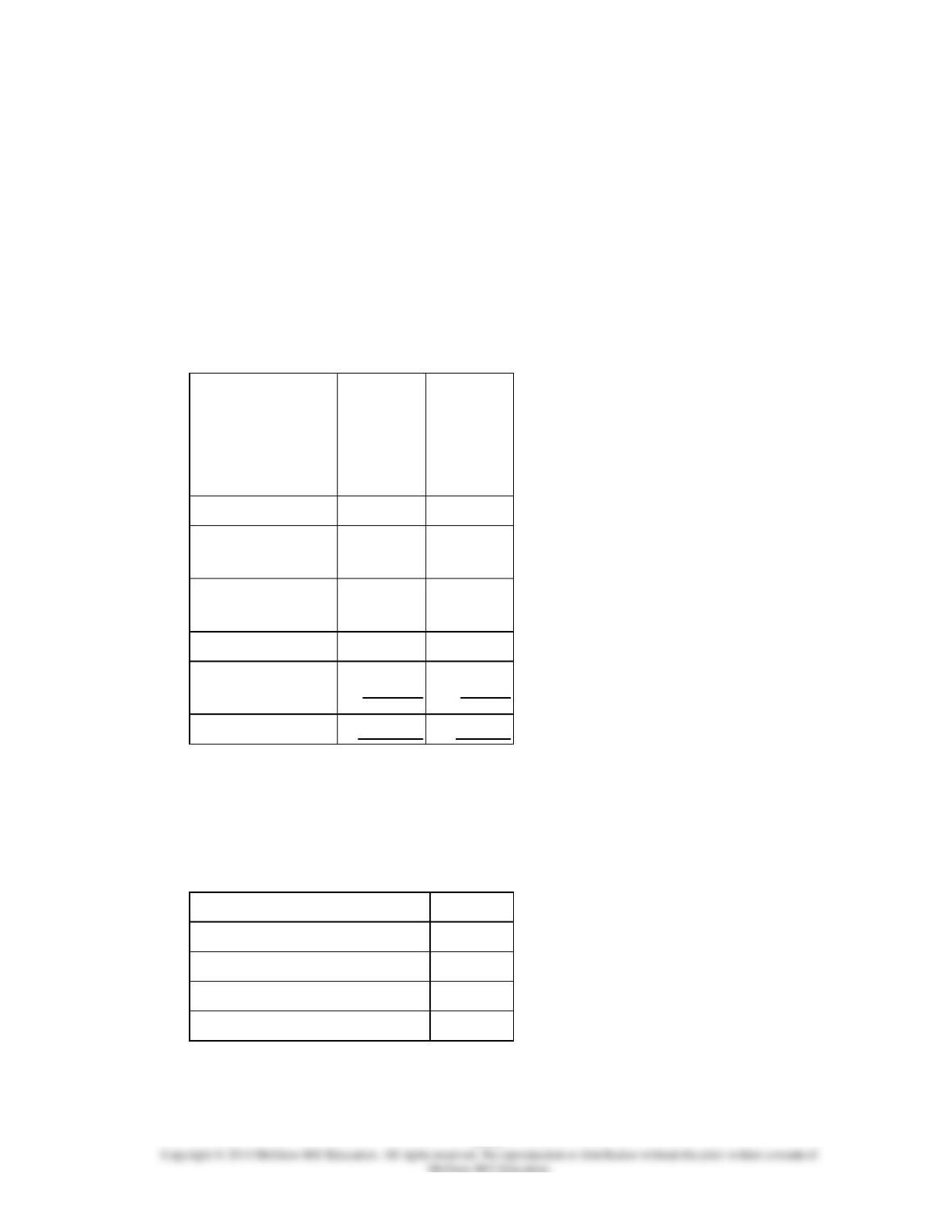

Coderre Corporation manufactures and sells a single product. The company uses units as

the measure of activity in its budgets and performance reports. During July, the company

budgeted for 7,800 units, but its actual level of activity was 7,780 units. The company has

provided the following data concerning the formulas used in its budgeting and its actual

results for July:

Data used in budgeting:

Fixed element

per month

Variable

element per unit

Revenue

−

$29.70

Direct labor

$0

$6.80

Direct materials

0

8.90

Manufacturing overhead

49,300

1.30

Selling and administrative expenses

26,300

0.10

Total expenses

$75,600

$17.10

Actual results for July:

Revenue

$224,996

Direct labor

$52,274

Direct materials

$69,312

Manufacturing overhead

$57,794

Selling and administrative

expenses

$27,588

The direct labor in the planning budget for July would be closest to:

8-724

8-725

210.

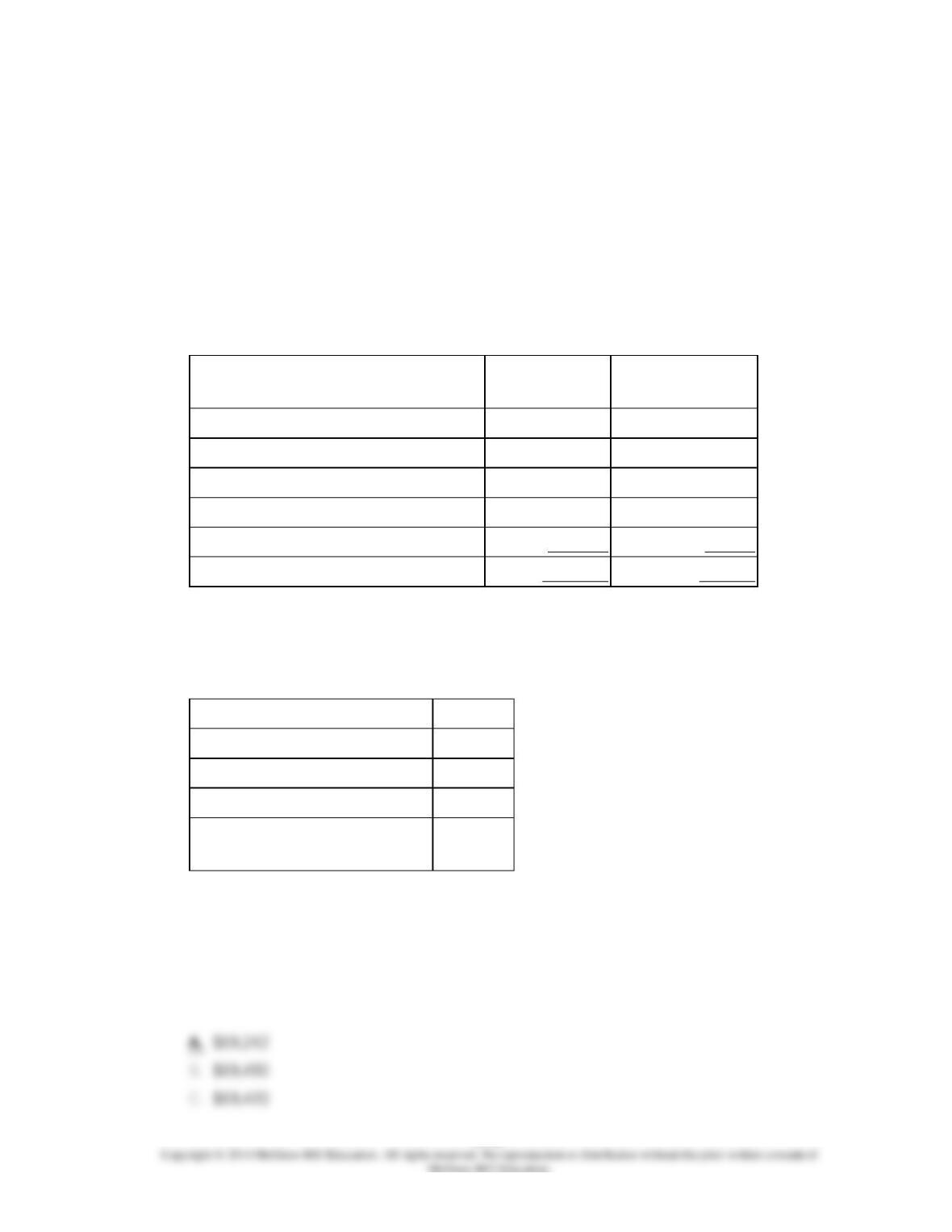

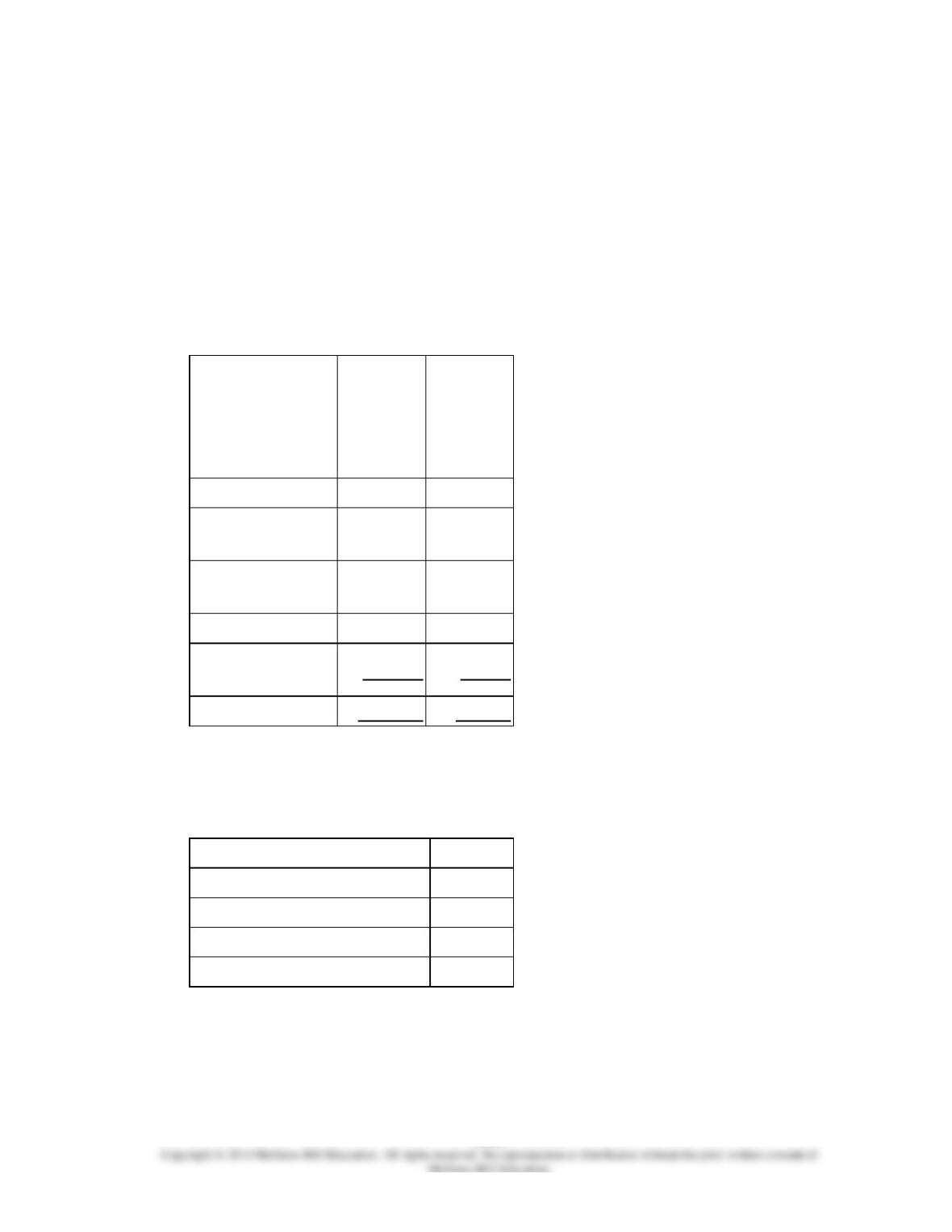

Coderre Corporation manufactures and sells a single product. The company uses units as

the measure of activity in its budgets and performance reports. During July, the company

budgeted for 7,800 units, but its actual level of activity was 7,780 units. The company has

provided the following data concerning the formulas used in its budgeting and its actual

results for July:

Data used in budgeting:

Fixed element

per month

Variable

element per unit

Revenue

−

$29.70

Direct labor

$0

$6.80

Direct materials

0

8.90

Manufacturing overhead

49,300

1.30

Selling and administrative expenses

26,300

0.10

Total expenses

$75,600

$17.10

Actual results for July:

Revenue

$224,996

Direct labor

$52,274

Direct materials

$69,312

Manufacturing overhead

$57,794

Selling and administrative

expenses

$27,588

The direct materials in the flexible budget for July would be closest to:

8-726

8-727

211.

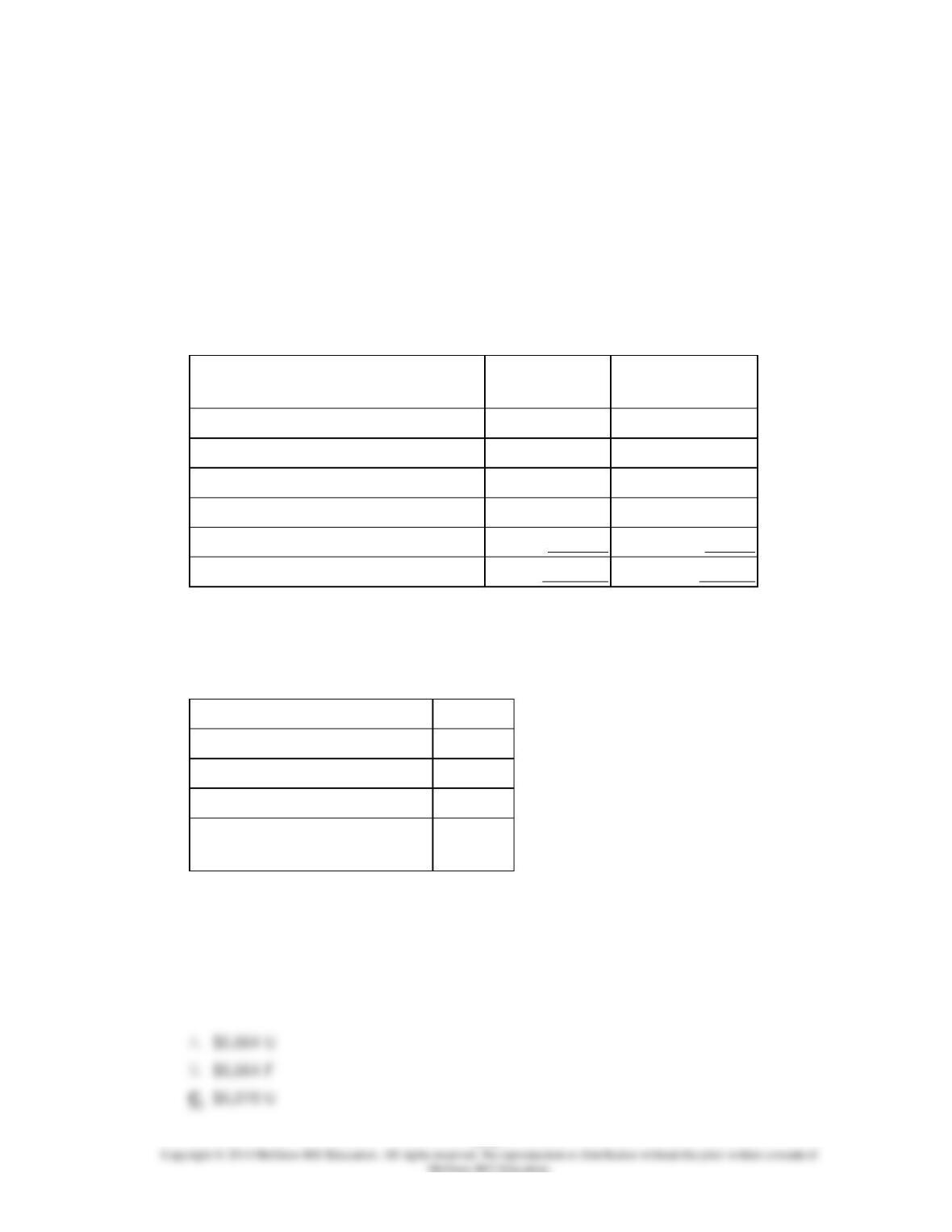

Coderre Corporation manufactures and sells a single product. The company uses units as

the measure of activity in its budgets and performance reports. During July, the company

budgeted for 7,800 units, but its actual level of activity was 7,780 units. The company has

provided the following data concerning the formulas used in its budgeting and its actual

results for July:

Data used in budgeting:

Fixed element

per month

Variable

element per unit

Revenue

−

$29.70

Direct labor

$0

$6.80

Direct materials

0

8.90

Manufacturing overhead

49,300

1.30

Selling and administrative expenses

26,300

0.10

Total expenses

$75,600

$17.10

Actual results for July:

Revenue

$224,996

Direct labor

$52,274

Direct materials

$69,312

Manufacturing overhead

$57,794

Selling and administrative

expenses

$27,588

The revenue variance for July would be closest to:

8-728

8-729

212.

Coderre Corporation manufactures and sells a single product. The company uses units as

the measure of activity in its budgets and performance reports. During July, the company

budgeted for 7,800 units, but its actual level of activity was 7,780 units. The company has

provided the following data concerning the formulas used in its budgeting and its actual

results for July:

Data used in budgeting:

Fixed element

per month

Variable

element per unit

Revenue

−

$29.70

Direct labor

$0

$6.80

Direct materials

0

8.90

Manufacturing overhead

49,300

1.30

Selling and administrative expenses

26,300

0.10

Total expenses

$75,600

$17.10

Actual results for July:

Revenue

$224,996

Direct labor

$52,274

Direct materials

$69,312

Manufacturing overhead

$57,794

Selling and administrative

expenses

$27,588

The spending variance for direct materials in July would be closest to:

8-730

8-731

213.

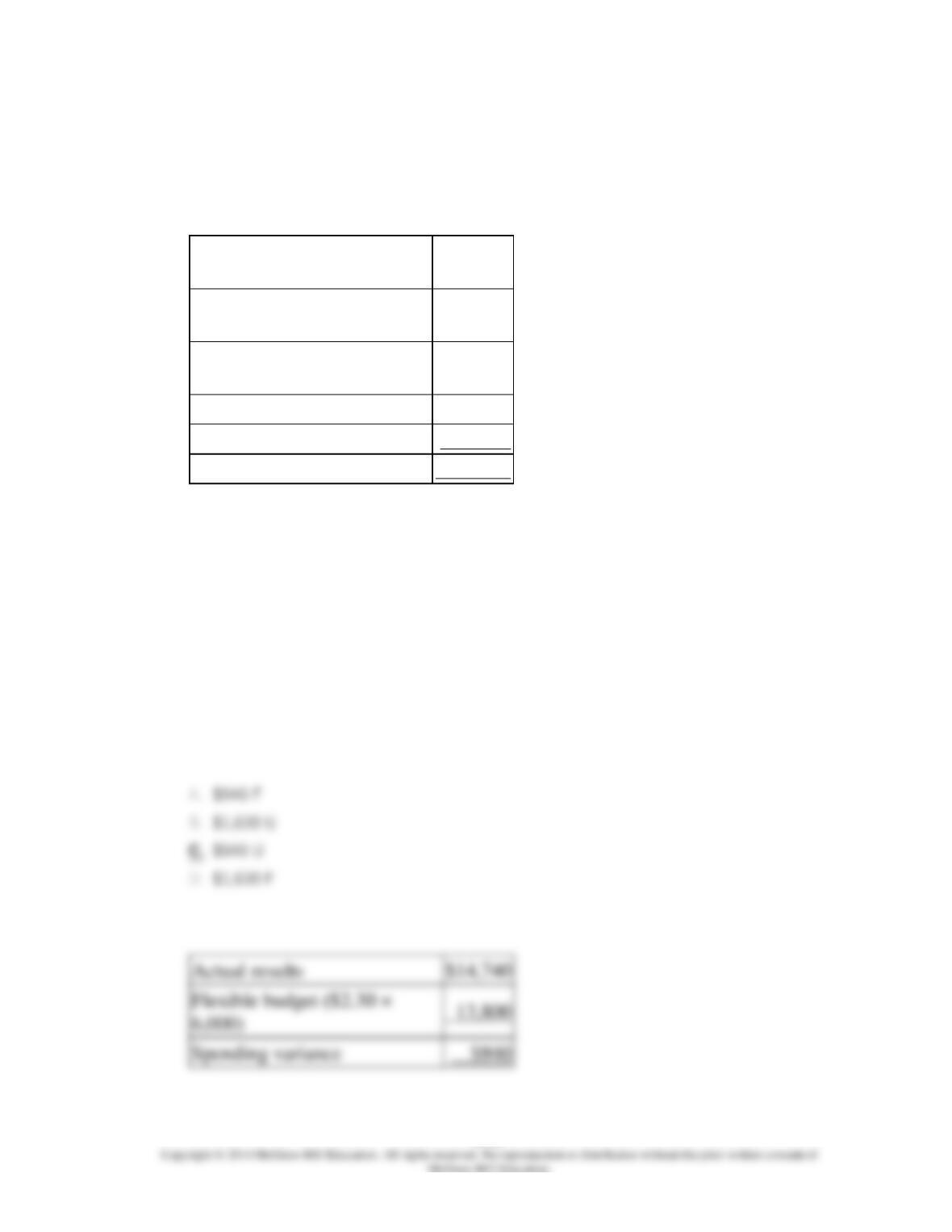

Zike Corporation’s static planning budget for October appears below. The company bases

its budgets on machine-hours.

Budgeted number of

machine-hours

5,700

Supplies (@ $2.30 per

machine-hour)

$13,110

Power (@ $8.00 per

machine-hour)

45,600

Salaries

15,390

Equipment depreciation

62,700

Total

$136,800

Actual results

$14,740

Flexible budget ($2.30 ×

6,000)

Spending variance

$940

In October, the actual number of machine-hours was 6,000, the actual supplies cost was

$14,740, the actual power cost was $49,170, the actual salaries cost was $15,390, and the

actual equipment depreciation was $63,670.

The spending variance for supplies cost in the performance report for the month should

be:

8-732

8-733

214.

Zike Corporation’s static planning budget for October appears below. The company bases

its budgets on machine-hours.

Budgeted number of

machine-hours

5,700

Supplies (@ $2.30 per

machine-hour)

$13,110

Power (@ $8.00 per

machine-hour)

45,600

Salaries

15,390

Equipment depreciation

62,700

Total

$136,800

Actual results

$49,170

Flexible budget ($8.00 ×

Spending variance

$1,170

In October, the actual number of machine-hours was 6,000, the actual supplies cost was

$14,740, the actual power cost was $49,170, the actual salaries cost was $15,390, and the

actual equipment depreciation was $63,670.

The spending variance for power cost in the performance report for the month should be:

8-734

8-735

215.

Zike Corporation’s static planning budget for October appears below. The company bases

its budgets on machine-hours.

Budgeted number of

machine-hours

5,700

Supplies (@ $2.30 per

machine-hour)

$13,110

Power (@ $8.00 per

machine-hour)

45,600

Salaries

15,390

Equipment depreciation

62,700

Total

$136,800

Actual results

Flexible budget

In October, the actual number of machine-hours was 6,000, the actual supplies cost was

$14,740, the actual power cost was $49,170, the actual salaries cost was $15,390, and the

actual equipment depreciation was $63,670.

The spending variance for equipment depreciation in the performance report for the

month should be:

8-736

8-737

216.

Smithj Kennel uses tenant-days as its measure of activity; an animal housed in the kennel

for one day is counted as one tenant-day. During February, the kennel budgeted for 3,500

tenant-days, but its actual level of activity was 3,490 tenant-days. The kennel has

provided the following data concerning the formulas used in its budgeting and its actual

results for February:

Data used in budgeting:

Fixed

element

per

month

Variable

element

per

tenant-

day

Revenue

−

$27.80

Wages and

salaries

$2,000

$5.10

Food and

supplies

1,100

9.10

Facility expenses

9,200

4.70

Administrative

expenses

7,600

0.40

Total expenses

$19,900

$19.30

Actual results for February:

Revenue

$96,382

Wages and salaries

$19,529

Food and supplies

$33,899

Facility expenses

$25,203

Administrative expenses

$8,956

8-738

The revenue variance for February would be closest to:

8-739

217.

Smithj Kennel uses tenant-days as its measure of activity; an animal housed in the kennel

for one day is counted as one tenant-day. During February, the kennel budgeted for 3,500

tenant-days, but its actual level of activity was 3,490 tenant-days. The kennel has

provided the following data concerning the formulas used in its budgeting and its actual

results for February:

Data used in budgeting:

Fixed

element

per

month

Variable

element

per

tenant-

day

Revenue

−

$27.80

Wages and

salaries

$2,000

$5.10

Food and

supplies

1,100

9.10

Facility expenses

9,200

4.70

Administrative

expenses

7,600

0.40

Total expenses

$19,900

$19.30

Actual results for February:

Revenue

$96,382

Wages and salaries

$19,529

Food and supplies

$33,899

Facility expenses

$25,203

Administrative expenses

$8,956

The spending variance for food and supplies in February would be closest to:

8-740