Problem 1-22A (continued)

3. The high-low estimate of fixed costs is $170.90 lower than the estimate

provided by least-squares regression. The high-low estimate of the

Problem 1-23A (45 minutes)

1. High-low method:

Units

Sold

Shipping

Expense

High activity level …………..

20,000

$210,000

Fixed cost element …………………………….

Problem 1-23A (continued)

2.

Milden Company

Budgeted Contribution Format Income Statement

For the First Quarter, Year 3

Sales (12,000 units × $100 per unit) ………..

$1,200,000

Variable expenses:

Total variable expenses ………………………….

Contribution margin ………………………………

Fixed expenses:

Total fixed expenses ……………………………..

Net operating income …………………………...

Problem 1-24A (45 minutes)

1.

Cost Behavior

Selling or

Administrative

Product Cost

Cost Item

Variable

Fixed

Cost

Direct

Indirect

Direct labor ………………………….

$118,000

$118,000

Advertising …………………………..

$50,000

$50,000

Factory supervision ………………..

40,000

$40,000

Property taxes, factory building ..

Sales commissions …………………

Insurance, factory …………………

Lease cost, factory equipment ….

12,000

Indirect materials, factory ……….

6,000

Depreciation, factory building …..

Administrative office supplies …..

Administrative office salaries ……

Direct materials used ……………..

Utilities, factory …………………….

Total costs …………………………..

$321,000

$182,000

$212,000

Problem 1-24A (continued)

2. The average product cost for one patio set would be:

Direct ………………………………………….

$212,000

$306,000 ÷ 2,000 sets = $153 per set

3. The average product cost per set would increase if the production

4. a. Yes, the president may expect a minimum price of $153, which is the

average cost to manufacture one set. He might expect a price even

higher than this to cover a portion of the administrative costs as well.

Ethics Challenge (30 minutes)

1. A cost that is classified as a period cost will be recognized on the income

statement as an expense in the current period. A cost that is classified

as a product cost will be recognized on the income statement as an

2. The discussion below is divided into two parts—Gallant’s actions to

postpone expenditures and the actions to reclassify period costs as

product costs.

The decision to postpone expenditures is questionable. It is one thing to

postpone expenditures due to a cash bind; it is quite another to

Analytical Thinking (30 minutes)

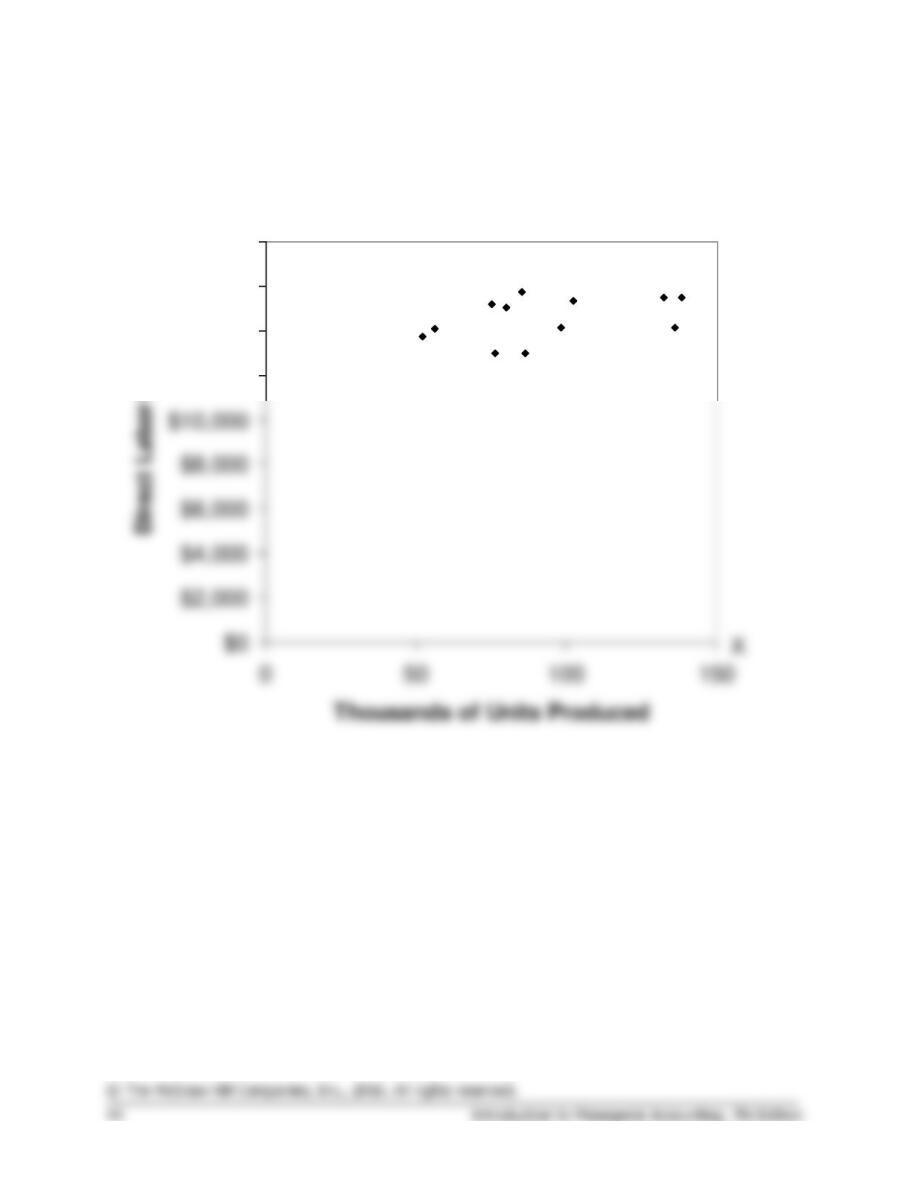

1. The scattergraph of direct labor cost versus the number of units

produced is presented below:

X

$12,000

$14,000

$16,000

$18,000

Y

Analytical Thinking (continued)

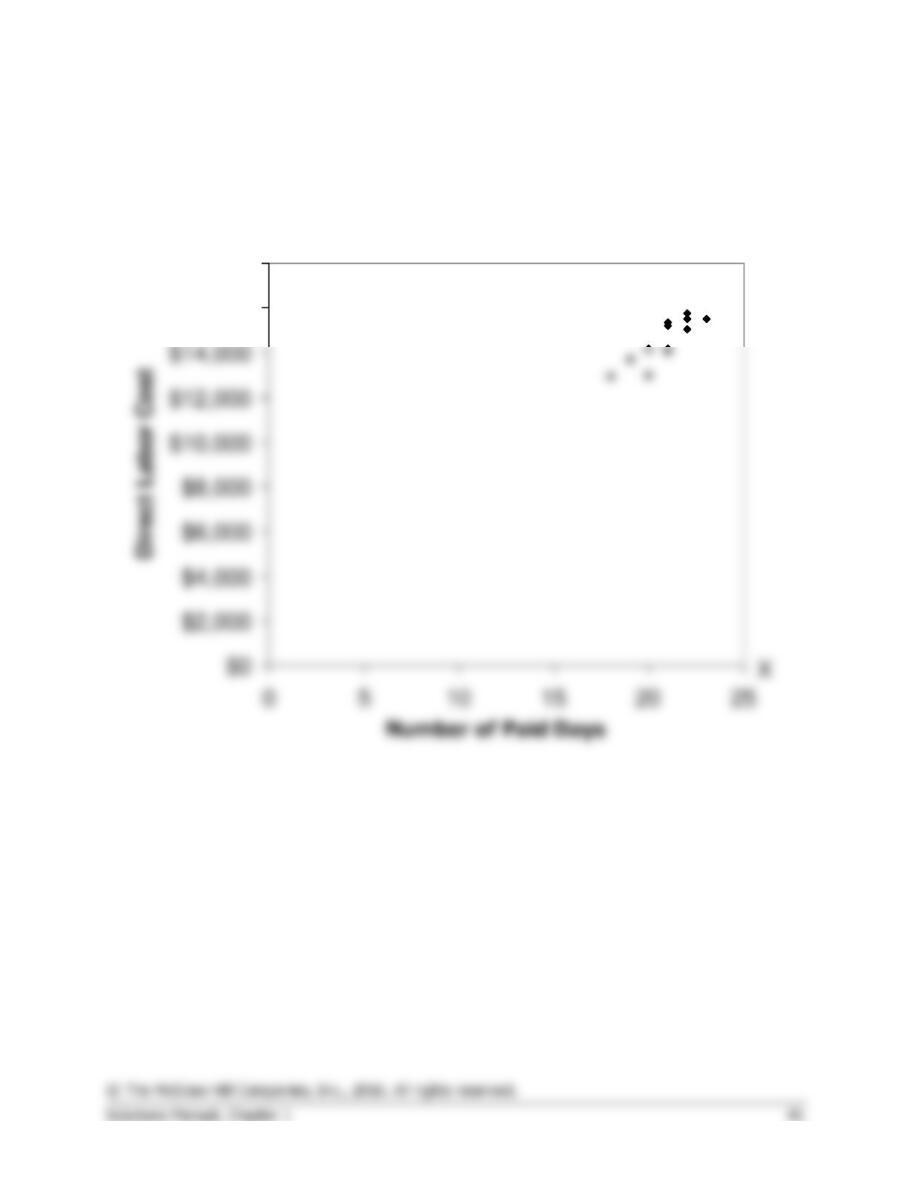

2. The scattergraph of the direct labor cost versus the number of paid days

is presented below:

$16,000

$18,000

Y

Analytical Thinking (continued)

3. The number of paid days should be used as the activity base rather than

the number of units produced. The scattergraphs reveal a much

stronger relation (i.e., higher correlation) between direct labor costs and

number of paid days than between direct labor costs and number of

Teamwork in Action

1. Student answers will vary concerning what is the best overall measure

of activity in each business. Some possibilities are:

a. Dental clinic: number of patient-visits; total patient revenues

Again, student answers will vary for examples of fixed and variable

costs, but some possibilities are:

Business

Measure

of Activity

Examples of

Fixed Costs

Examples of

Variable Costs

a.

Dental clinic

Number of

patient-visits

Receptionist’s

wages; office rent

Supplies such as

mouthwash,

Teamwork in Action (continued)

2. Within the relevant range, changes in activity have these effects:

Increases

in activity

Decreases

in activity

Total fixed cost ………………………………..

Constant

Constant

Total variable costs …………………………..

Variable cost per unit of activity ………….

Constant

Constant

Average total cost per unit of activity ……

Increase

3. The dental clinic probably has the lowest ratio of variable to fixed costs.

Very little of the costs of a dental clinic are variable with respect to the

number of patient-visits. Because of its high fixed costs and low variable

Chapter 1

Take Two Solutions

Exercise 1-4 (15 minutes)

1.

Cups of Coffee Served

in a Week

2,000

2,100

2,200

Fixed cost …………………………..

Total cost …………………………..

Average cost per cup served * ..

2. The average cost of a cup of coffee declines as the number of cups of

Exercise 1-5 (20 minutes)

1.

Occupancy-

Days

Electrical

Costs

High activity level (August) ..

2,406

$5,148

Total cost (August) …………………………………………….

Fixed cost element …………………………………………….

2. Electrical costs may reflect seasonal factors other than just the variation

in occupancy days. For example, common areas such as the reception

area must be lighted for longer periods during the winter than in the

Exercise 1-6 (15 minutes)

1. Traditional income statement

Cherokee Inc.

Traditional Income Statement

Sales ($30 per unit × 24,000 units) ………………..

$720,000

Gross margin …………………………..…………………

Selling and administrative expenses:

Administrative expenses

Net operating income ………………………………….

$314,000

2. Contribution format income statement

Cherokee Inc.

Contribution Format Income Statement

Sales …………………………..…………………………..

$720,000

Variable expenses:

Administrative expenses

Contribution margin …………………………………….

Fixed expenses:

Net operating income ………………………………….

Cost of goods sold

Exercise 1-8 (20 minutes)

1.

Kilometers

Driven

Total Annual

Cost*

High level of activity …………………….

105,000

$10,500

Low level of activity ……………………..

Change ……………………………………..

*

105,000 kilometers × $0.100 per kilometer = $10,500

70,000 kilometers × $0.134 per kilometer = $9,380

Total cost at 105,000 kilometers …………………

Fixed cost per year ………………………………….

2. Y = $7,140 + $0.032X

3.

Fixed cost …………………………………………………

$ 7,140

Total annual cost ………………………………………..

Exercise 1-13 (20 minutes)

1. Traditional income statement

The Alpine House, Inc.

Traditional Income Statement

Sales …………………………..…………………………..

$165,000

Gross margin …………………………..…………………

Net operating income (loss) ………………………….

Cost of goods sold

2. Contribution format income statement

The Alpine House, Inc.

Contribution Format Income Statement

Sales …………………………..…………………………..

$165,000

Variable expenses:

Contribution margin …………………………………….

Fixed expenses:

Net operating income (loss) ………………………….

Exercise 1-13 (continued)

2. Since 220 pairs of skis were sold and the contribution margin totaled