7-141

86.

Dilbert Farm Supply is located in a small town in the rural west. Data regarding the store’s

operations follow:

o Sales are budgeted at $260,000 for November, $230,000 for December, and $210,000 for

January.

o Collections are expected to be 80% in the month of sale, 19% in the month following the

sale, and 1% uncollectible.

o The cost of goods sold is 65% of sales.

o The company desires to have an ending merchandise inventory at the end of each month

equal to 60% of the next month’s cost of goods sold. Payment for merchandise is made in the

month following the purchase.

o Other monthly expenses to be paid in cash are $20,300.

o Monthly depreciation is $20,000.

o Ignore taxes.

Balance Sheet

October 31

Assets

Cash

$27,000

Accounts receivable, net of allowance for uncollectible accounts

79,000

Merchandise inventory

101,400

Property, plant and equipment, net of $574,000 accumulated depreciation

1,082,000

Total assets

$1,289,400

Liabilities and Stockholders’ Equity

Accounts payable

$169,000

Common stock

740,000

Retained earnings

380,400

Total liabilities and stockholders’ equity

$1,289,400

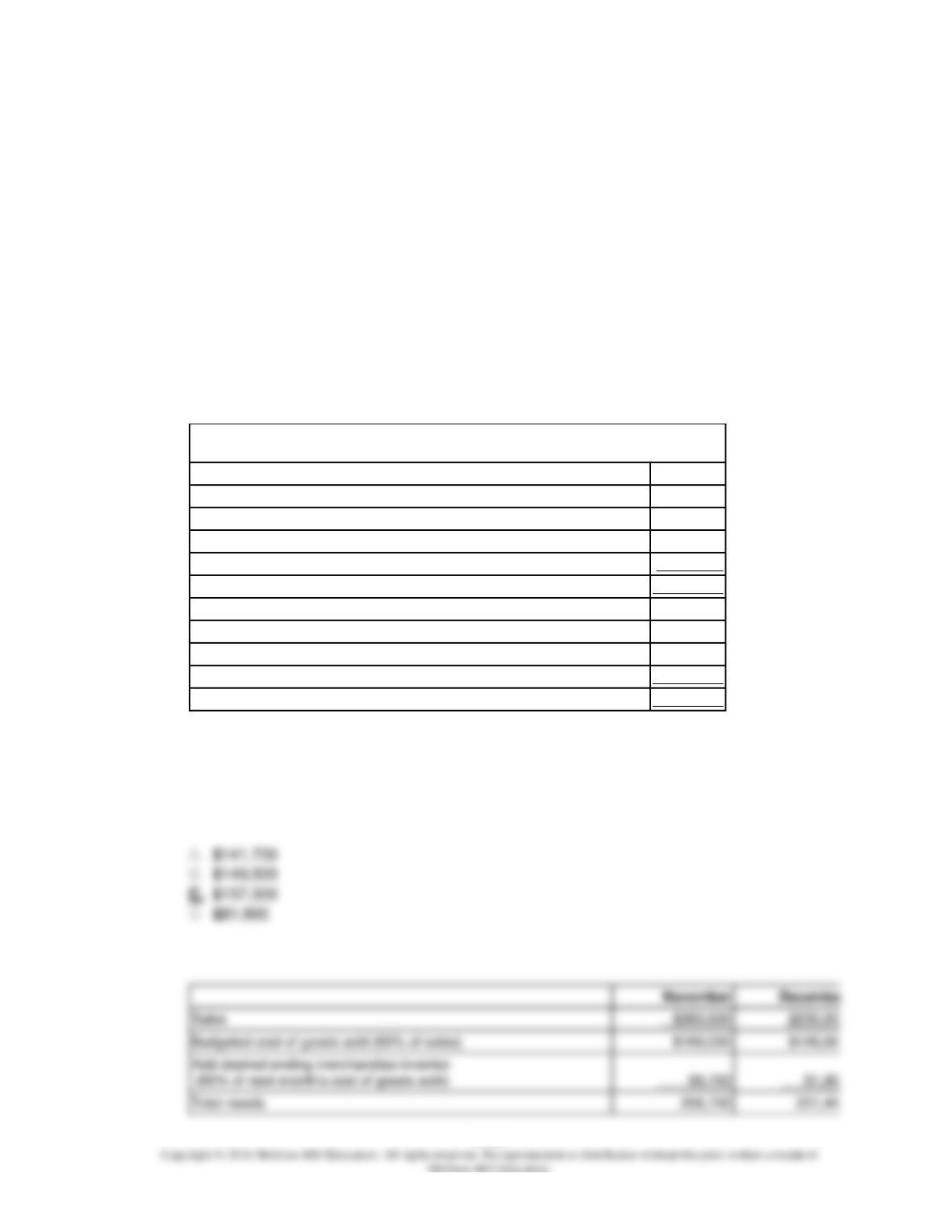

Sales

$210,000

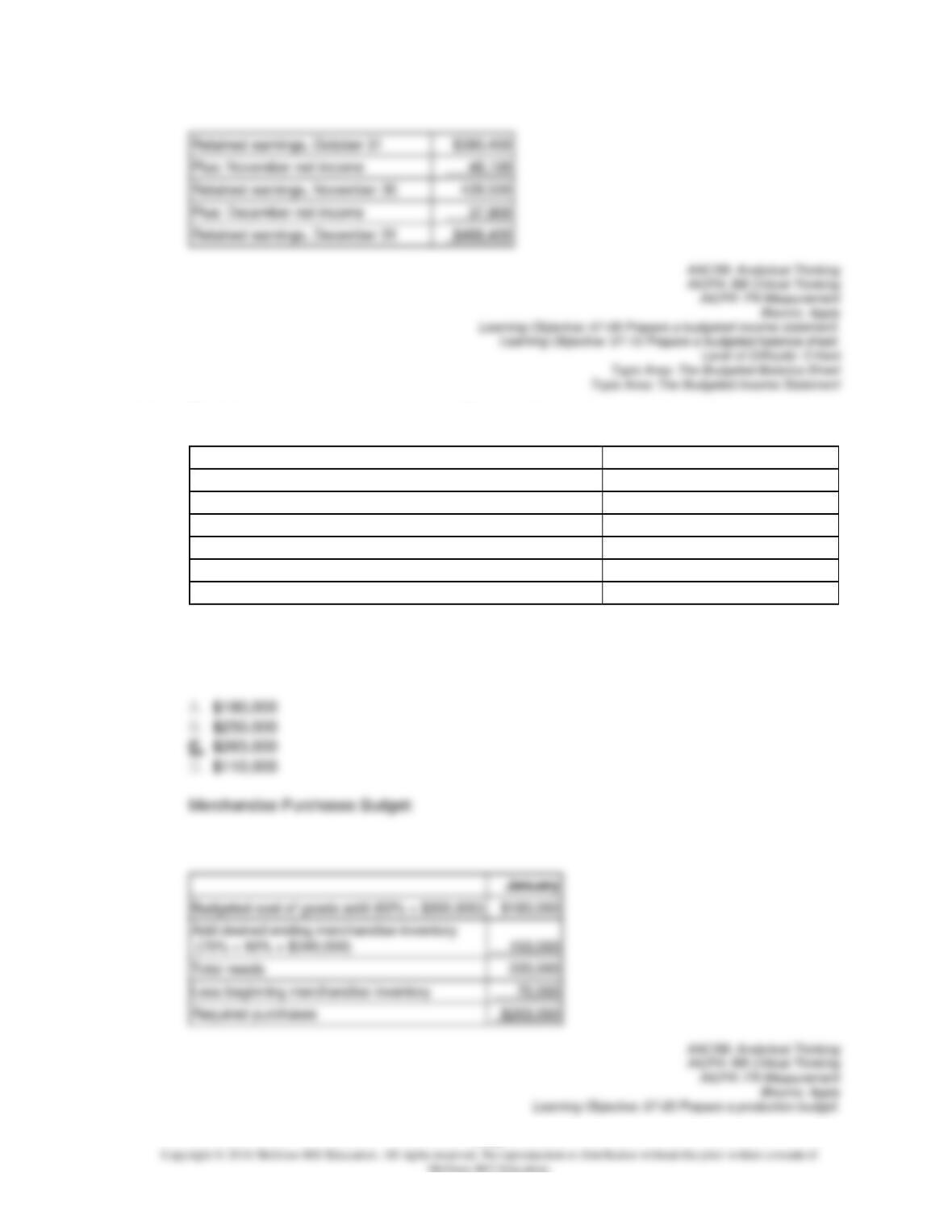

The cost of December merchandise purchases would be:

7-142

7-143

87.

Dilbert Farm Supply is located in a small town in the rural west. Data regarding the store’s

operations follow:

o Sales are budgeted at $260,000 for November, $230,000 for December, and $210,000 for

January.

o Collections are expected to be 80% in the month of sale, 19% in the month following the

sale, and 1% uncollectible.

o The cost of goods sold is 65% of sales.

o The company desires to have an ending merchandise inventory at the end of each month

equal to 60% of the next month’s cost of goods sold. Payment for merchandise is made in the

month following the purchase.

o Other monthly expenses to be paid in cash are $20,300.

o Monthly depreciation is $20,000.

o Ignore taxes.

Balance Sheet

October 31

Assets

Cash

$27,000

Accounts receivable, net of allowance for uncollectible accounts

79,000

Merchandise inventory

101,400

Property, plant and equipment, net of $574,000 accumulated depreciation

1,082,000

Total assets

$1,289,400

Liabilities and Stockholders’ Equity

Accounts payable

$169,000

Common stock

740,000

Retained earnings

380,400

Total liabilities and stockholders’ equity

$1,289,400

Sales

Budgeted cost of goods sold (65% of sales)

December cash disbursements for merchandise purchases would be:

7-144

7-145

88.

Dilbert Farm Supply is located in a small town in the rural west. Data regarding the store’s

operations follow:

o Sales are budgeted at $260,000 for November, $230,000 for December, and $210,000 for

January.

o Collections are expected to be 80% in the month of sale, 19% in the month following the

sale, and 1% uncollectible.

o The cost of goods sold is 65% of sales.

o The company desires to have an ending merchandise inventory at the end of each month

equal to 60% of the next month’s cost of goods sold. Payment for merchandise is made in the

month following the purchase.

o Other monthly expenses to be paid in cash are $20,300.

o Monthly depreciation is $20,000.

o Ignore taxes.

Balance Sheet

October 31

Assets

Cash

$27,000

Accounts receivable, net of allowance for uncollectible accounts

79,000

Merchandise inventory

101,400

Property, plant and equipment, net of $574,000 accumulated depreciation

1,082,000

Total assets

$1,289,400

Liabilities and Stockholders’ Equity

Accounts payable

$169,000

Common stock

740,000

Retained earnings

380,400

Total liabilities and stockholders’ equity

$1,289,400

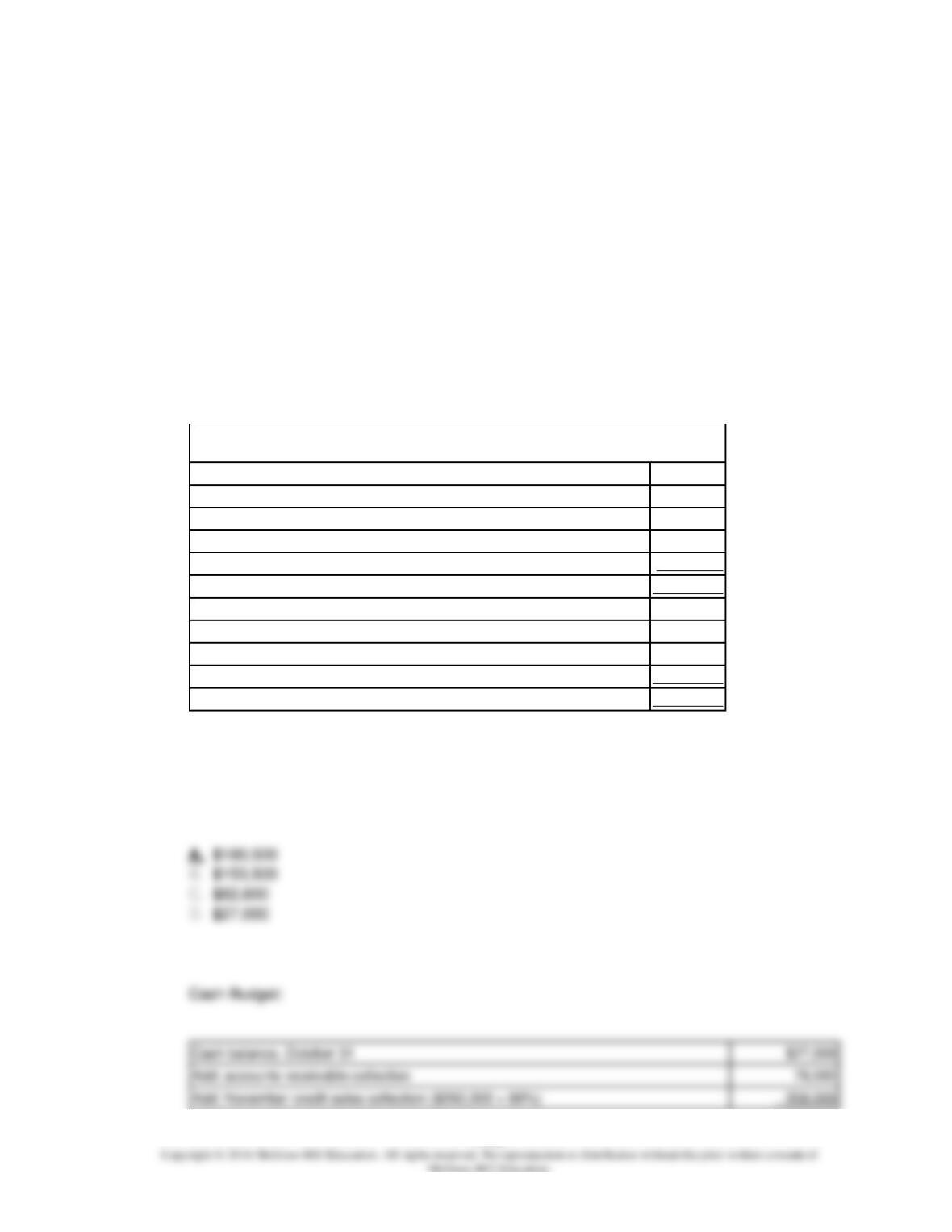

November credit sales collected in December ($260,000 × 19%)

December credit sales collected in December ($230,000 × 80%)

The difference between cash receipts and cash disbursements for December would be:

7-146

7-147

89.

Dilbert Farm Supply is located in a small town in the rural west. Data regarding the store’s

operations follow:

o Sales are budgeted at $260,000 for November, $230,000 for December, and $210,000 for

January.

o Collections are expected to be 80% in the month of sale, 19% in the month following the

sale, and 1% uncollectible.

o The cost of goods sold is 65% of sales.

o The company desires to have an ending merchandise inventory at the end of each month

equal to 60% of the next month’s cost of goods sold. Payment for merchandise is made in the

month following the purchase.

o Other monthly expenses to be paid in cash are $20,300.

o Monthly depreciation is $20,000.

o Ignore taxes.

Balance Sheet

October 31

Assets

Cash

$27,000

Accounts receivable, net of allowance for uncollectible accounts

79,000

Merchandise inventory

101,400

Property, plant and equipment, net of $574,000 accumulated depreciation

1,082,000

Total assets

$1,289,400

Liabilities and Stockholders’ Equity

Accounts payable

$169,000

Common stock

740,000

Retained earnings

380,400

Total liabilities and stockholders’ equity

$1,289,400

The net income for December would be:

7-148

7-149

90.

Dilbert Farm Supply is located in a small town in the rural west. Data regarding the store’s

operations follow:

o Sales are budgeted at $260,000 for November, $230,000 for December, and $210,000 for

January.

o Collections are expected to be 80% in the month of sale, 19% in the month following the

sale, and 1% uncollectible.

o The cost of goods sold is 65% of sales.

o The company desires to have an ending merchandise inventory at the end of each month

equal to 60% of the next month’s cost of goods sold. Payment for merchandise is made in the

month following the purchase.

o Other monthly expenses to be paid in cash are $20,300.

o Monthly depreciation is $20,000.

o Ignore taxes.

Balance Sheet

October 31

Assets

Cash

$27,000

Accounts receivable, net of allowance for uncollectible accounts

79,000

Merchandise inventory

101,400

Property, plant and equipment, net of $574,000 accumulated depreciation

1,082,000

Total assets

$1,289,400

Liabilities and Stockholders’ Equity

Accounts payable

$169,000

Common stock

740,000

Retained earnings

380,400

Total liabilities and stockholders’ equity

$1,289,400

Cash balance, October 31

The cash balance at the end of December would be:

7-150

7-151

91.

Dilbert Farm Supply is located in a small town in the rural west. Data regarding the store’s

operations follow:

o Sales are budgeted at $260,000 for November, $230,000 for December, and $210,000 for

January.

o Collections are expected to be 80% in the month of sale, 19% in the month following the

sale, and 1% uncollectible.

o The cost of goods sold is 65% of sales.

o The company desires to have an ending merchandise inventory at the end of each month

equal to 60% of the next month’s cost of goods sold. Payment for merchandise is made in the

month following the purchase.

o Other monthly expenses to be paid in cash are $20,300.

o Monthly depreciation is $20,000.

o Ignore taxes.

Balance Sheet

October 31

Assets

Cash

$27,000

Accounts receivable, net of allowance for uncollectible accounts

79,000

Merchandise inventory

101,400

Property, plant and equipment, net of $574,000 accumulated depreciation

1,082,000

Total assets

$1,289,400

Liabilities and Stockholders’ Equity

Accounts payable

$169,000

Common stock

740,000

Retained earnings

380,400

Total liabilities and stockholders’ equity

$1,289,400

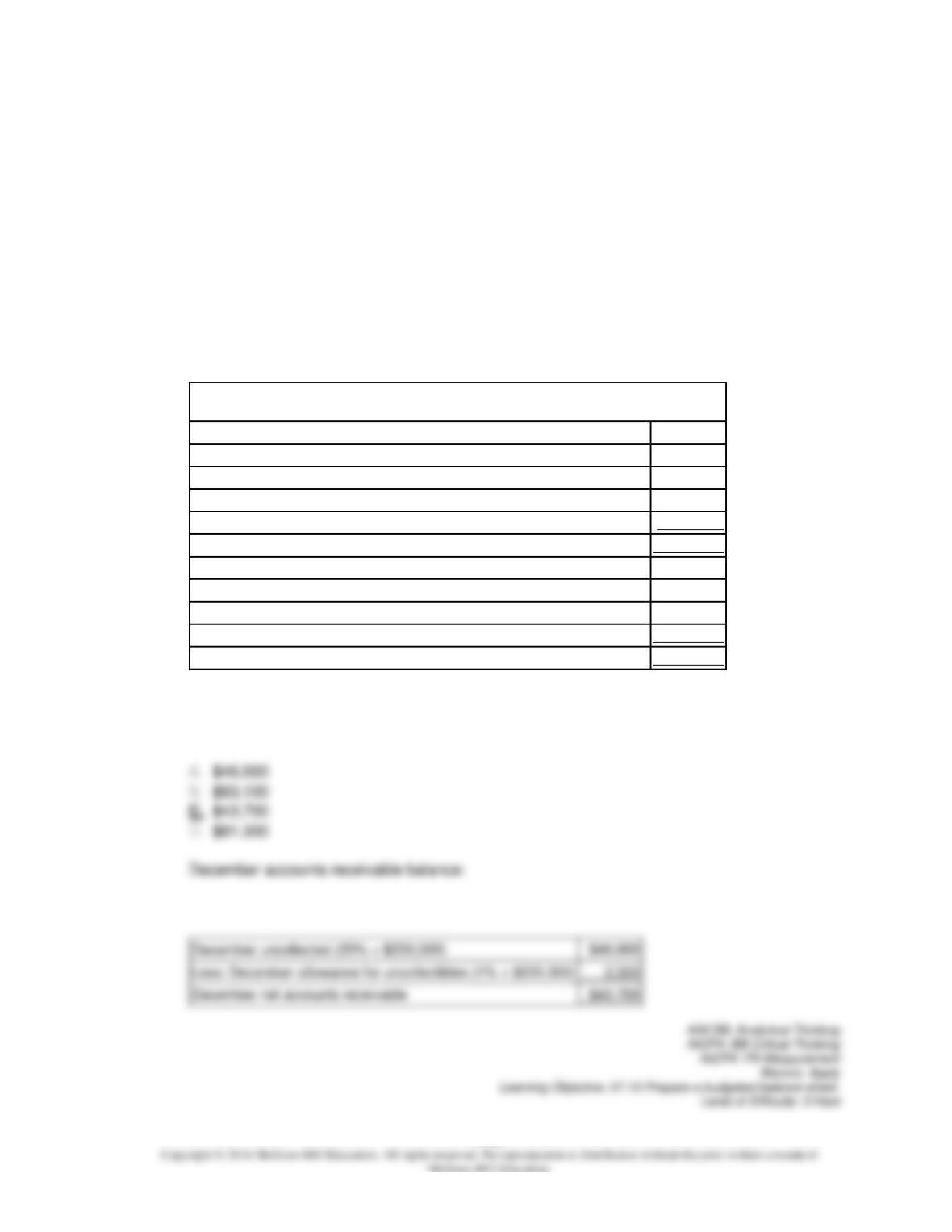

December uncollected (20% × $230,000)

Less: December allowance for uncollectibles (1% × $230,000)

2,300

December net accounts receivable

The accounts receivable balance, net of uncollectible accounts, at the end of December

would be:

7-152

92.

Dilbert Farm Supply is located in a small town in the rural west. Data regarding the store’s

operations follow:

o Sales are budgeted at $260,000 for November, $230,000 for December, and $210,000 for

January.

o Collections are expected to be 80% in the month of sale, 19% in the month following the

sale, and 1% uncollectible.

o The cost of goods sold is 65% of sales.

o The company desires to have an ending merchandise inventory at the end of each month

equal to 60% of the next month’s cost of goods sold. Payment for merchandise is made in the

month following the purchase.

o Other monthly expenses to be paid in cash are $20,300.

o Monthly depreciation is $20,000.

o Ignore taxes.

Balance Sheet

October 31

Assets

Cash

$27,000

Accounts receivable, net of allowance for uncollectible accounts

79,000

Merchandise inventory

101,400

Property, plant and equipment, net of $574,000 accumulated depreciation

1,082,000

Total assets

$1,289,400

Liabilities and Stockholders’ Equity

Accounts payable

$169,000

Common stock

740,000

Retained earnings

380,400

Total liabilities and stockholders’ equity

$1,289,400

Unpaid purchases for December sales ($230,000 × 65% × 40%)

Unpaid purchases for January sales ($210,000 × 65% × 60%)

December accounts payable

Accounts payable at the end of December would be:

7-153

7-154

93.

Dilbert Farm Supply is located in a small town in the rural west. Data regarding the store’s

operations follow:

o Sales are budgeted at $260,000 for November, $230,000 for December, and $210,000 for

January.

o Collections are expected to be 80% in the month of sale, 19% in the month following the

sale, and 1% uncollectible.

o The cost of goods sold is 65% of sales.

o The company desires to have an ending merchandise inventory at the end of each month

equal to 60% of the next month’s cost of goods sold. Payment for merchandise is made in the

month following the purchase.

o Other monthly expenses to be paid in cash are $20,300.

o Monthly depreciation is $20,000.

o Ignore taxes.

Balance Sheet

October 31

Assets

Cash

$27,000

Accounts receivable, net of allowance for uncollectible accounts

79,000

Merchandise inventory

101,400

Property, plant and equipment, net of $574,000 accumulated depreciation

1,082,000

Total assets

$1,289,400

Liabilities and Stockholders’ Equity

Accounts payable

$169,000

Common stock

740,000

Retained earnings

380,400

Total liabilities and stockholders’ equity

$1,289,400

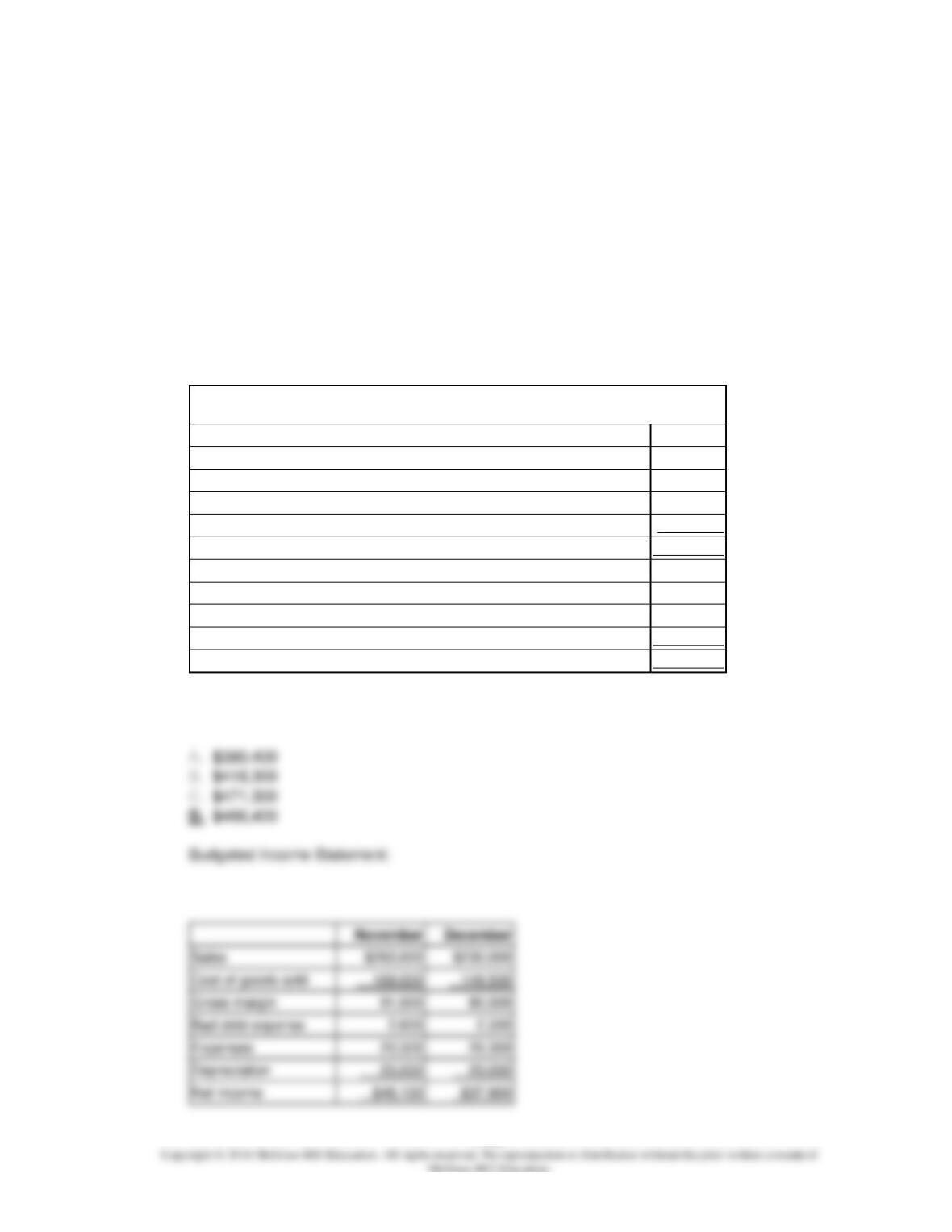

Sales

Cost of goods sold

Gross margin

Bad debt expense

Expenses

Retained earnings at the end of December would be:

7-155

Retained earnings, October 31

Plus: November net income

Retained earnings, November 30

Plus: December net income

Retained earnings, December 31

94.

The following are budgeted data for the Bingham Corporation, a merchandising company:

Budgeted Sales (at retail):

January

$300,000

February

$340,000

March

$400,000

April

$350,000

Cost of goods sold as a percentage of sales

60%

Desired ending inventory

75% of next month sales

Budgeted cost of goods sold (60% × $300,000)

Total needs

Less beginning merchandise inventory

Required purchases

Assuming that the Bingham Corporation had inventory on hand of $70,000 (at cost) on

January 1, the purchases for January (at cost) would be:

7-156

95.

The following are budgeted data for the Bingham Corporation, a merchandising company:

Budgeted Sales (at retail):

January

$300,000

February

$340,000

March

$400,000

April

$350,000

Cost of goods sold as a percentage of sales

60%

Desired ending inventory

75% of next month sales

The desired ending inventory (at cost) for February would be:

7-157

96.

The following are budgeted data for the Bingham Corporation, a merchandising company:

Budgeted Sales (at retail):

January

$300,000

February

$340,000

March

$400,000

April

$350,000

Cost of goods sold as a percentage of sales

60%

Desired ending inventory

75% of next month sales

(75% × 60% × $350,000)

Total needs

Assume that all purchases are paid for in the month following the month of purchase. The

cash disbursements for purchases that would appear in the April cash budget would be:

7-158

97.

Harris Inc., has budgeted sales in units for the next five months as follows:

June

9,400 units

July

7,800 units

August

7,300 units

September

5,400 units

October

4,100 units

Past experience has shown that the ending inventory for each month should be equal to 20%

of the next month’s sales in units. The inventory on May 31 contained 1,880 units. The

company needs to prepare a production budget for the next five months.

The beginning inventory for September should be:

7-159

98.

Harris Inc., has budgeted sales in units for the next five months as follows:

June

9,400 units

July

7,800 units

August

7,300 units

September

5,400 units

October

4,100 units

Past experience has shown that the ending inventory for each month should be equal to 20%

of the next month’s sales in units. The inventory on May 31 contained 1,880 units. The

company needs to prepare a production budget for the next five months.

The total number of units produced in July should be:

7-160

99.

May Corporation, a merchandising firm, has budgeted sales as follows for the third quarter of

the year:

July

$80,000

August

$90,000

September

$70,000

Cost of goods sold is equal to 65% of sales. The company wants to maintain a monthly

ending inventory equal to 130% of the Cost of Goods Sold for the following month. The

inventory on June 30 is less than this ideal since it is only $65,000. The company is now

preparing a Merchandise Purchases Budget.

The desired beginning inventory for September is: