Problem 5-20A (continued)

c. This problem illustrates the difficulty faced by some companies. When

variable labor costs increase, it is often difficult to pass these cost

Problem 5-21A (30 minutes)

1.

Product

White

Fragrant

Loonzain

Total

Sales …………………..

Variable expenses …..

Contribution margin ..

*

Fixed expenses ………

Net operating

Percentage of total

2. Break-even sales would be:

Problem 5-21A (continued)

3. Memo to the president:

Although the company met its sales budget of $750,000 for the month,

the mix of products changed substantially from that budgeted. This is

the reason the budgeted net operating income was not met, and the

Problem 5-22A (60 minutes)

1. The CM ratio is 30%:

Total

Per Unit

Percent of Sales

Sales (19,500 units) ………

$585,000

$30.00

100%

Variable expenses …………

Contribution margin ………

$175,500

$ 9.00

The break-even point is:

= ($30 − $21) × Q − $180,000

= ($9) × Q − $180,000

= $180,000

2.

Incremental contribution margin:

$80,000 increased sales × 0.30 CM ratio …………

$24,000

Problem 5-22A (continued)

3.

Sales (39,000 units @ $27.00 per unit*) ………

$1,053,000

819,000

Contribution margin …………………………………

Fixed expenses ($180,000 + $60,000) …………

Net operating loss …………………………………..

Variable expenses

4.

Profit

= Unit CM × Q − Fixed expenses

$9,750

= ($30.00 − $21.75*) × Q − $180,000

$9,750

= ($8.25) × Q − $180,000

$8.25Q

= $189,750

Q

= $189,750 ÷ $8.25

Q

= 23,000 units

*$21.00 + $0.75 = $21.75

Alternative solution:

5. a. The new CM ratio would be:

Per Unit

Percent of Sales

Sales ……………………….

$30.00

100%

Variable expenses ………

18.00

Contribution margin ……

$12.00

Problem 5-22A (continued)

The new break-even point would be:

b. Comparative income statements follow:

Not Automated

Automated

Total

Per

Unit

%

Total

Per

Unit

%

Contribution

Sales (26,000

Problem 5-22A (continued)

c. Whether or not the company should automate its operations depends

on how much risk the company is willing to take and on prospects for

future sales. The proposed changes would increase the company’s

fixed costs and its break-even point. However, the changes would

Note to the Instructor: Although it is not asked for in the problem,

if time permits you may want to compute the point of indifference

between the two alternatives in terms of units sold; i.e., the point

where profits will be the same under either alternative. At this point,

total revenue will be the same; hence, we include only costs in our

equation:

Problem 5-23A (60 minutes)

1. The CM ratio is 60%:

Sales price ………………….

$20.00

100%

Variable expenses ………..

3. $75,000 increased sales × 0.60 CM ratio = $45,000 increased

b. 4 × 20% = 80% increase in net operating income. In dollars, this

increase would be 80% × $60,000 = $48,000.

Problem 5-23A (continued)

5.

Last Year:

18,000 units

Proposed:

24,000 units*

Amount

Per Unit

Amount

Per Unit

Sales ………………………

Variable expenses ………

Net operating income …

6.

Expected total contribution margin:

18,000 units × 1.25 × $11.00 per unit* ……………………

$247,500

Present total contribution margin:

*$20.00 – ($8.00 + $1.00) = $11.00

Problem 5-24A (30 minutes)

1. The contribution margin per sweatshirt would be:

Selling price ………………………………………

$13.50

Variable expenses:

Purchase cost of the sweatshirts ………….

$8.00

Contribution margin …………………………….

$ 4.00

2. Since an order has been placed, there is now a “fixed” cost associated

with the purchase price of the sweatshirts (i.e., the sweatshirts can’t be

returned). For example, an order of 75 sweatshirts requires a “fixed”

Selling price …………………………………..

Variable expenses (commissions only) …

Contribution margin …………………………

Problem 5-25A (45 minutes)

1. The contribution margin per unit on the first 16,000 units is:

Per Unit

Sales price ……………………..

$3.00

Variable expenses …………….

1.25

Contribution margin ………….

$1.75

Per Unit

Sales price ……………………..

Variable expenses …………….

Contribution margin ………….

Fixed costs on the first 16,000 units …………………..

Less contribution margin from the first 16,000 units

Remaining unrecovered fixed costs …………………….

Total fixed costs to be covered by remaining sales …

Problem 5-25A (continued)

The additional sales of units required to cover these fixed costs would

be:

3. If a bonus of $0.10 per unit is paid for each unit sold in excess of the

break-even point, then the contribution margin on these units would

drop from $1.60 to $1.50 per unit.

The desired monthly profit would be:

Problem 5-26A (60 minutes)

1.

Profit

= Unit CM × Q − Fixed expenses

$0

= ($30 − $18) × Q − $150,000

$0

= ($12) × Q − $150,000

$12Q

= $150,000

Q

= $150,000 ÷ $12

Q

= 12,500 pairs

12,500 pairs × $30 per pair = $375,000 in sales

Alternative solution:

2. See the graph on the following page.

3. The simplest approach is:

Break-even sales ……………………

12,500 pairs

Actual sales ………………………….

12,000 pairs

Sales short of break-even ………..

Sales (12,000 pairs × $30.00 per pair) ….

Contribution margin ………………………….

Fixed expenses ………………………………..

Net operating loss …………………………….

Problem 5-26A (continued)

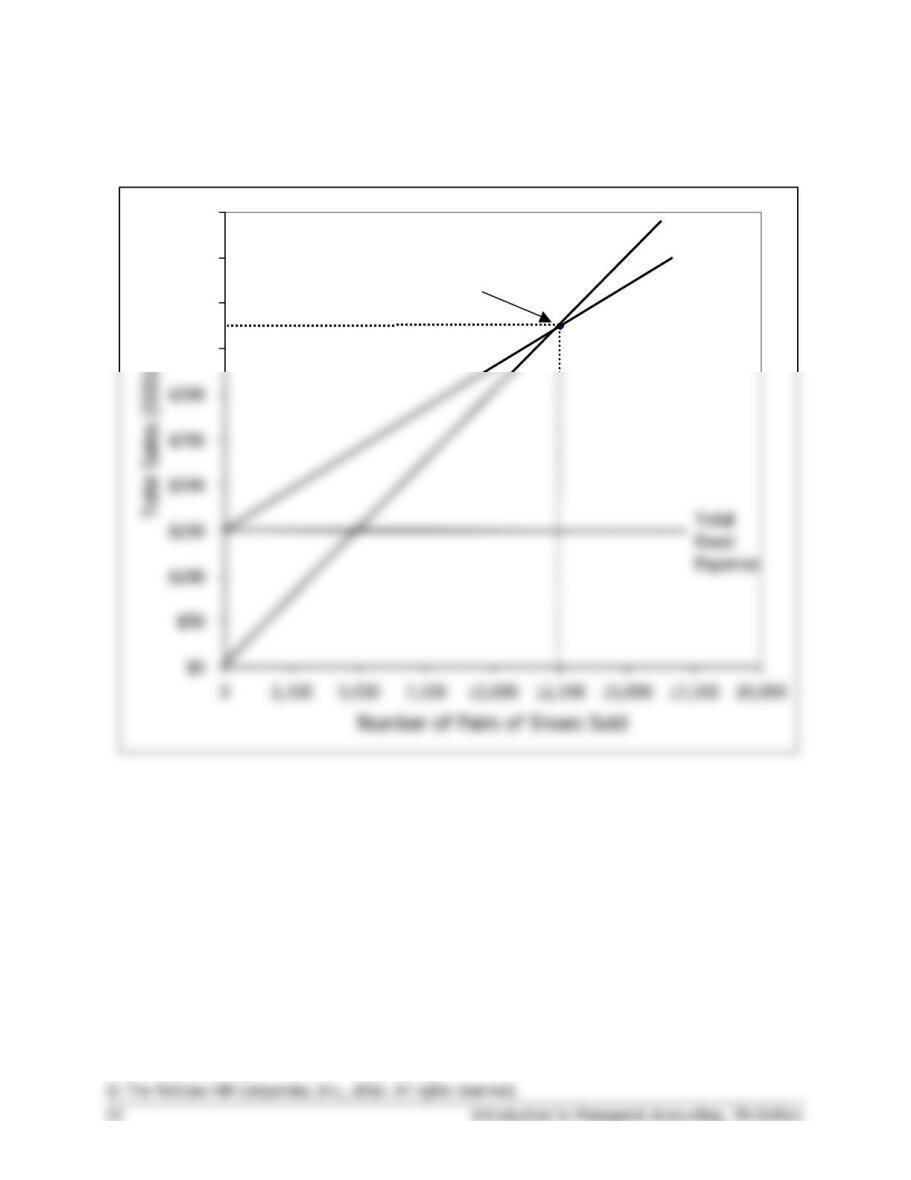

2. Cost-volume-profit graph:

$350

$400

$450

$500

Break-even point:

12,500 pairs of shoes or

$375,000 total sales

Total Sales

Total

Expense

Problem 5-26A (continued)

4. The variable expenses will now be $18.75 ($18.00 + $0.75) per pair,

and the contribution margin will be $11.25 ($30.00 – $18.75) per pair.

= Unit CM × Q − Fixed expenses

= ($30.00 − $18.75) × Q − $150,000

= ($11.25) × Q − $150,000

= $150,000

= $150,000 ÷ $11.25

= 13,333 pairs (rounded)

Alternative solution:

0.375

5. The simplest approach is:

Actual sales …………………………..

15,000 pairs

Break-even sales …………………….

12,500 pairs

Excess over break-even sales ……

2,500 pairs × $11.50 per pair* = $28,750 profit

*$12.00 present contribution margin – $0.50 commission = $11.50

Alternative solution:

Sales (15,000 pairs × $30.00 per pair) …………..

$450,000

Contribution margin …………………………………..

Problem 5-26A (continued)

6. The new variable expenses will be $13.50 per pair.

Although the change will lower the break-even point from 12,500 pairs

to 11,000 pairs, the company must consider whether this reduction in

the break-even point is more than offset by the possible loss in sales

arising from having the sales staff on a salaried basis. Under a salary

Problem 5-27A (45 minutes)

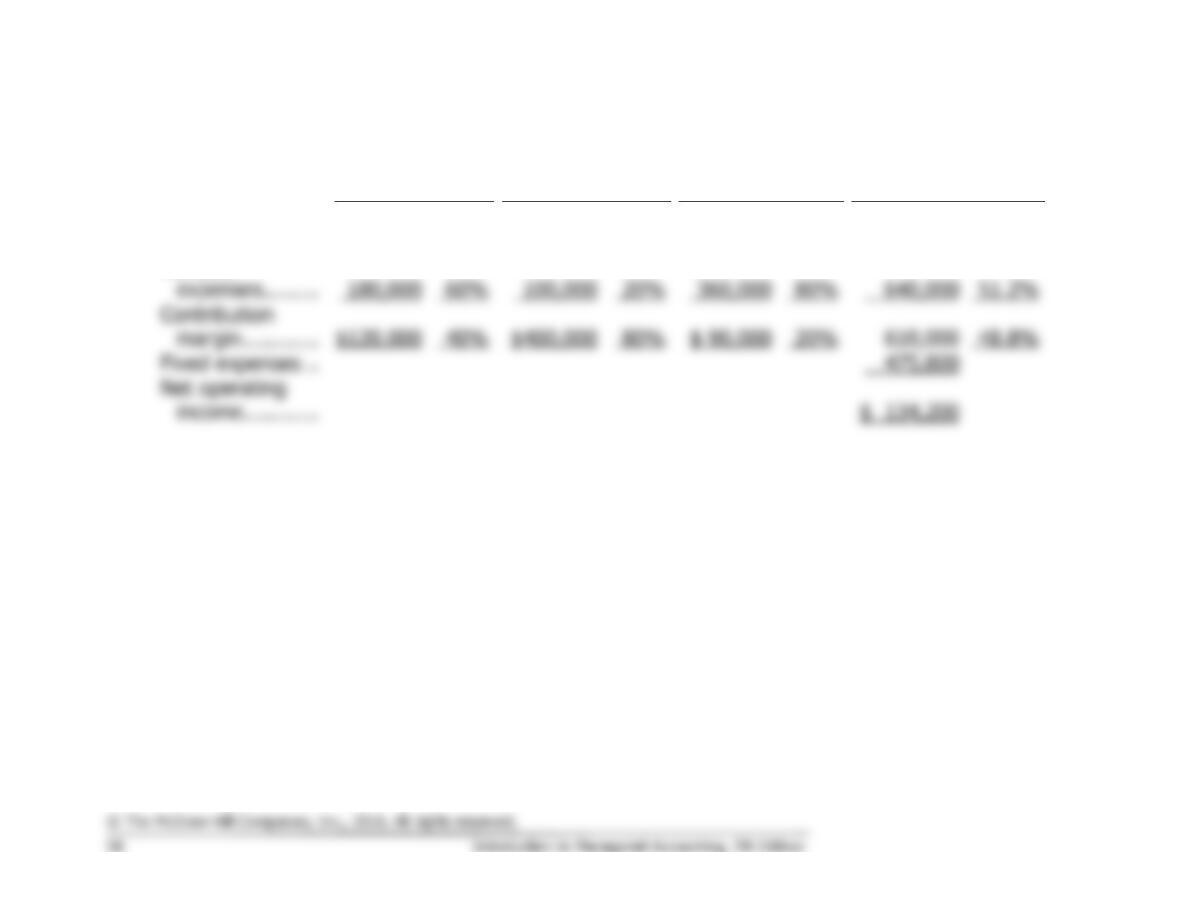

1.

a.

Hawaiian

Fantasy

Tahitian

Joy

Total

Amount

%

Amount

%

Amount

%

Sales ……………………..

$300,000

100%

$500,000

100%

$800,000

100%

Variable expenses …….

Net operating income ..

b.

Fixed expenses $475,800

Dollar sales to = = = $732,000

break even CM ratio 0.65

Problem 5-27A (continued)

2.

a.

Hawaiian

Fantasy

Tahitian

Joy

Samoan

Delight

Total

Amount

%

Amount

%

Amount

%

Amount

%

Sales ……………..

$300,000

100%

$500,000

100%

$450,000

100%

$1,250,000

100.0%

$120,000

$400,000

Fixed expenses ..

Variable

Problem 5-27A (continued)

b.

Fixed expenses $475,800

Dollar sales to = = = $975,000

break even CM ratio 0.488

3. The reason for the increase in the break-even point can be traced to the

decrease in the company’s overall contribution margin ratio when the

third product is added. Note from the income statements above that this

ratio drops from 65% to 48.8% with the addition of the third product.

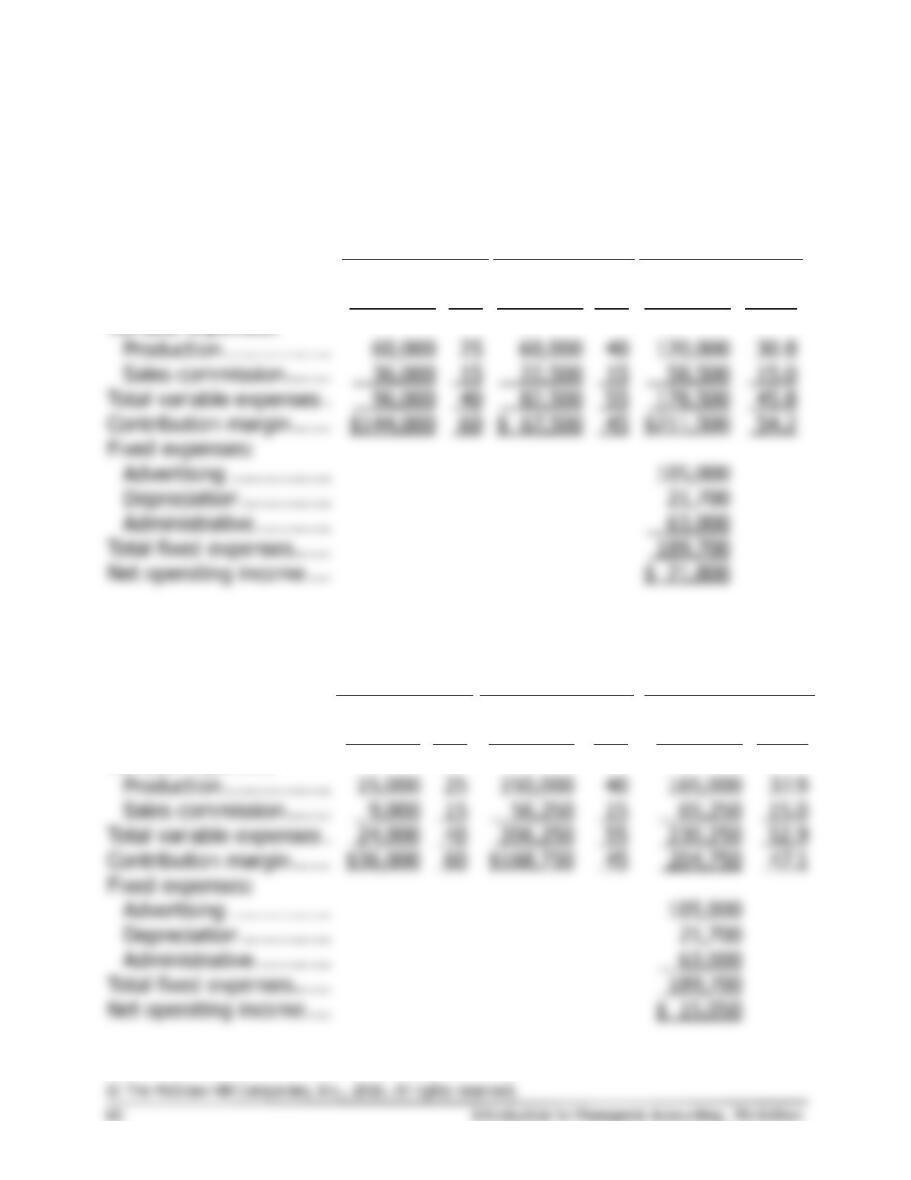

Problem 5-28A (60 minutes)

1.

Carbex, Inc.

Income Statement For April

Standard

Deluxe

Total

Amount

%

Amount

%

Amount

%

Sales ……………………….

$240,000

100

$150,000

100

$390,000

100.0

Variable expenses:

22,500

58,500

Total variable expenses .

96,000

178,500

45.8

Contribution margin ……

$ 67,500

54.2

Fixed expenses:

63,000

Total fixed expenses ……

189,700

Net operating income ….

Carbex, Inc.

Income Statement For May

Standard

Deluxe

Total

Amount

%

Amount

%

Amount

%

Sales ……………………….

$60,000

100

$375,000

100

$435,000

100.0

Variable expenses:

Total variable expenses .

Contribution margin ……

$36,000

$168,750

Fixed expenses:

Total fixed expenses ……

Net operating income ….

$ 15,050