Exercise 7-13 (30 minutes)

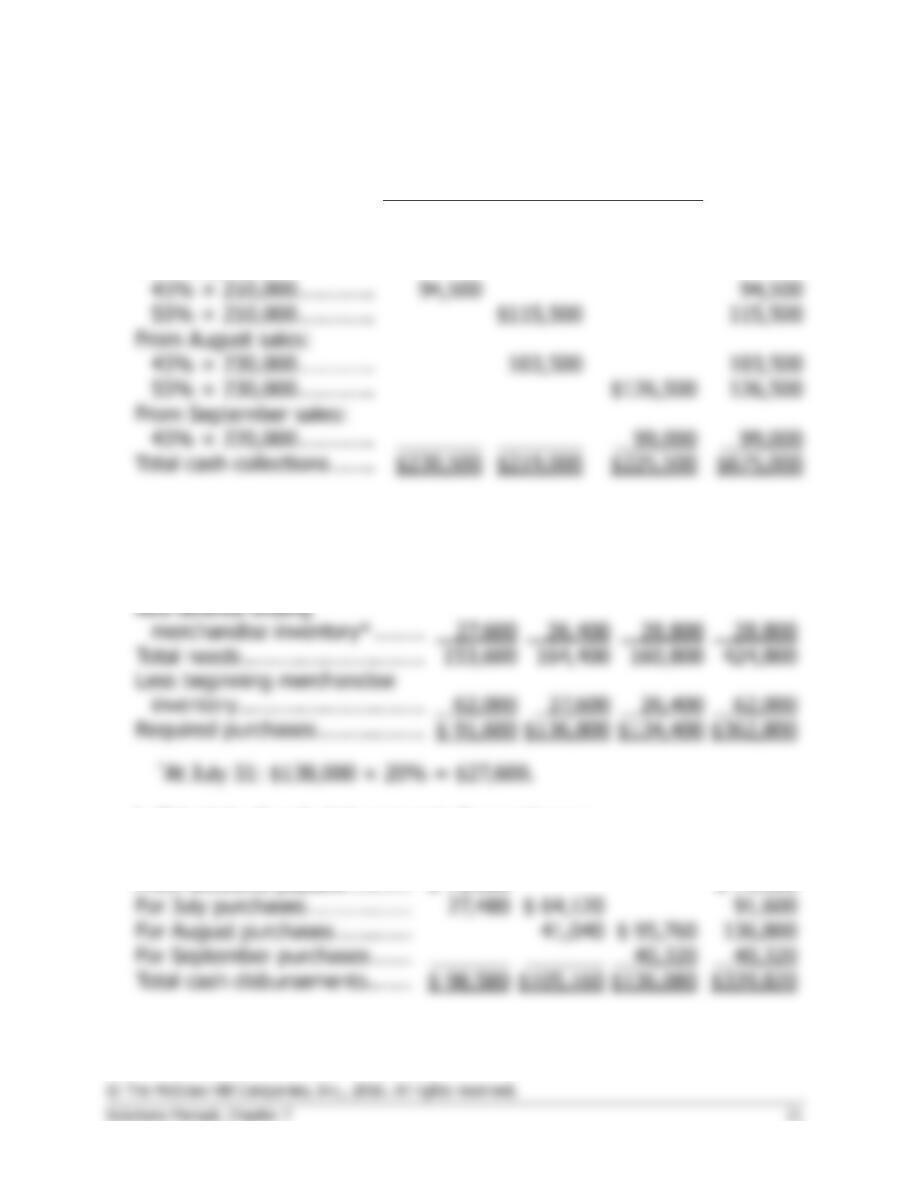

1. Schedule of expected cash collections:

Month

July

August

September

Quarter

From accounts receivable .

$136,000

$136,000

From July sales:

From August sales:

From September sales:

Total cash collections …….

2. a. Merchandise purchases budget:

July

August

Sept.

Total

Budgeted cost of goods sold ….

$126,000

$138,000

$132,000

$396,000

Total needs ………………………..

Required purchases ……………..

b. Schedule of cash disbursements for purchases:

July

August

Sept.

Total

From accounts payable ……….

$ 71,100

$ 71,100

For July purchases ……………..

$ 64,120

For August purchases …………

For September purchases ……

Total cash disbursements …….

$136,080

Exercise 7-13 (continued)

3.

Beech Corporation

Income Statement

For the Quarter Ended September 30

Sales ($210,000 + $230,000 + $220,000) ..

$660,000

Net operating income…………………………..

4.

Beech Corporation

Balance Sheet

September 30

Assets

Cash ($90,000 + $675,000 – $339,820 – ($55,000 ×

3)) ……………………………………………………….…..

$260,180

Accounts receivable ($220,000 × 55%) …………………

Inventory (Part 2a) ……………………………………………

Accounts payable ($134,400 × 70%) …………………….

Common stock (Given) ………………………………………

Retained earnings ($99,900 + $84,000) …………………

Exercise 7-14 (30 minutes)

1.

Jessi Corporation

Sales Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Budgeted unit sales ……………..

11,000

12,000

14,000

13,000

50,000

Selling price per unit …………….

Total sales …………………………

Schedule of Expected Cash Collections

Beginning accounts receivable .

$ 70,200

$ 70,200

$ 59,400

188,100

205,200

239,400

Total cash collections ……………

Exercise 7-14 (continued)

2.

Jessi Corporation

Production Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Budgeted unit sales ……………..

11,000

12,000

14,000

13,000

50,000

Total needs ………………………..

Exercise 7-15 (20 minutes)

1.

Hruska Corporation

Direct Labor Budget

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Year

Required production in units ……..

12,000

10,000

13,000

14,000

49,000

Direct labor cost per hour …………

Total direct labor cost ………………

$24,000

$31,200

$33,600

2.

Hruska Corporation

Manufacturing Overhead Budget

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Year

Budgeted direct labor-hours ………

2,400

2,000

2,600

2,800

9,800

Fixed manufacturing overhead …..

Total manufacturing overhead …..

90,200

89,500

90,550

90,900

Less depreciation ……………………

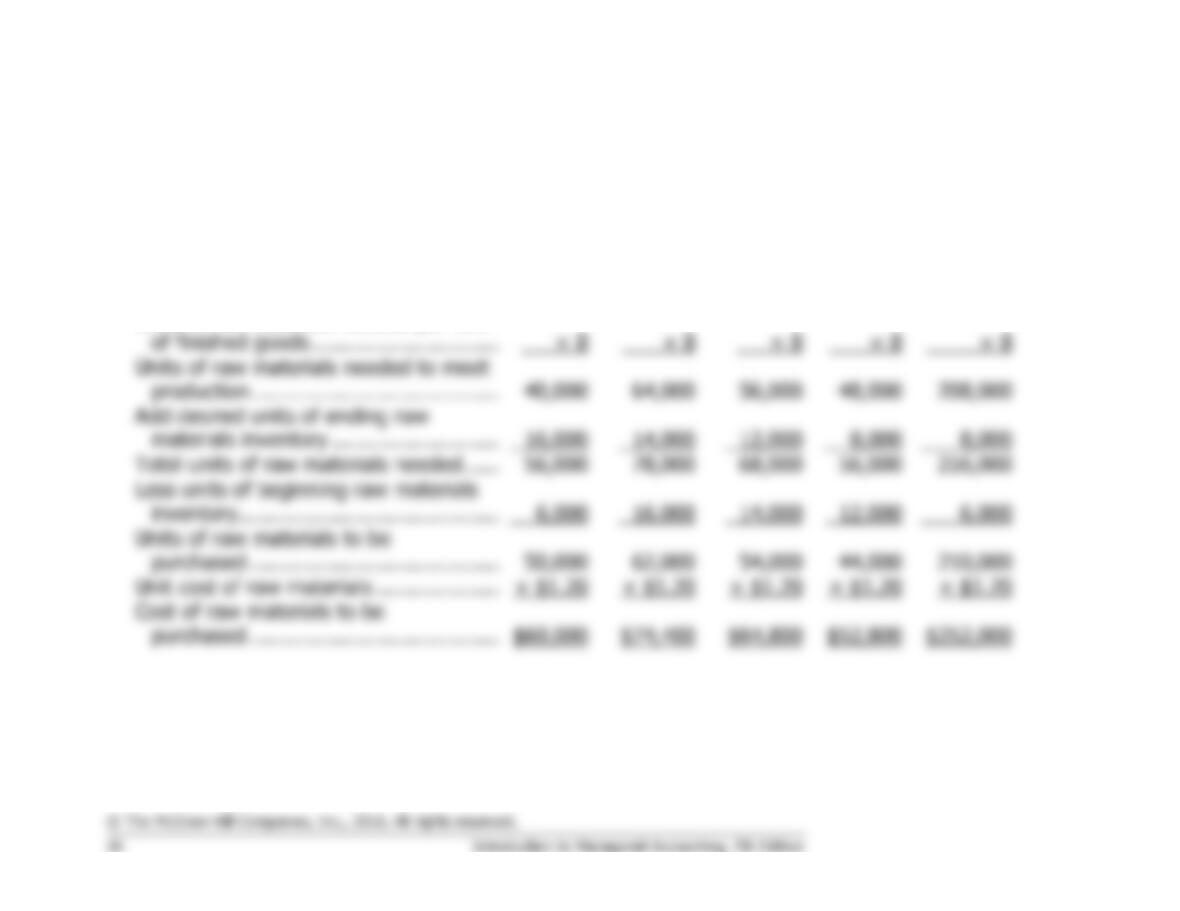

Exercise 7-16 (30 minutes)

1.

Zan Corporation

Direct Materials Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Required production in units of

finished goods …………………………….

5,000

8,000

7,000

6,000

26,000

Units of raw materials needed to meet

Add desired units of ending raw

inventory ……………………………………

Units of raw materials to be

Cost of raw materials to be

Units of raw materials needed per unit

Exercise 7-16 (continued)

Schedule of Expected Cash Disbursements for Materials

Beginning accounts payable ………

$ 2,880

$ 2,880

1st Quarter purchases ……………..

36,000

60,000

2nd Quarter purchases …………….

74,400

3rd Quarter purchases ……………..

4th Quarter purchases ……………..

31,680

31,680

2.

Zan Corporation

Direct Labor Budget

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Year

Required production in units ……..

5,000

8,000

7,000

6,000

26,000

Direct labor-hours per unit ………..

Total direct labor-hours needed….

Direct labor cost per hour …………

Total direct labor cost ………………

Problem 7-17A (45 minutes)

1. Schedule of cash receipts:

Cash sales—May …………………………………………

$ 60,000

Collections on account receivable:

70,000

Total cash receipts ………………………………………

$184,000

Schedule of cash payments for purchases:

April 30 accounts payable balance ………………….

$ 63,000

May purchases (40% × $120,000) …………………

48,000

Total cash payments ……………………………………

$111,000

Minden Company

Cash Budget

For the Month of May

Beginning cash balance ……………………………….

$ 9,000

Add collections from customers (above) …………..

184,000

Total cash available ……………………………………..

193,000

Less cash disbursements:

Purchase of inventory (above) …………………….

Total cash disbursements ……………………………..

189,500

Excess of cash available over disbursements …….

Financing:

Total financing ……………………………………………

Ending cash balance ……………………………………

Problem 7-17A (continued)

2.

Minden Company

Budgeted Income Statement

For the Month of May

Sales ……………………………………………….

$200,000

Cost of goods sold:

Cost of goods sold ………………………………

Gross margin ……………………………………..

Net operating income ………………………….

Interest expense …………………………..……

Net income ……………………………………….

3.

Minden Company

Budgeted Balance Sheet

May 31

Assets

Cash ……………………………………………………………….

$ 8,900

Accounts receivable (50% × $140,000) ………………….

70,000

Inventory …………………………..…………………………….

40,000

Total assets ………………………………………………………

Accounts payable (60% × 120,000) ……………………….

Note payable …………………………………………………….

Common stock ………………………………………………….

Retained earnings ($42,500 + $15,900) ………………….

Problem 7-18A (45 minutes)

1. Schedule of cash receipts:

Cash sales—May …………………………………………

$ 60,000

Collections on account receivable:

96,000

Total cash receipts ………………………………………

$210,000

Schedule of cash payments for purchases:

April 30 accounts payable balance ………………….

$ 63,000

May purchases (50% × $120,000) …………………

60,000

Total cash payments ……………………………………

$123,000

Minden Company

Cash Budget

For the Month of May

Beginning cash balance ……………………………….

$ 9,000

Add collections from customers (above) …………..

210,000

Total cash available ……………………………………..

219,000

Less cash disbursements:

Purchase of inventory (above) …………………….

Total cash disbursements ……………………………..

201,500

Excess of cash available over disbursements …….

Financing:

Total financing ……………………………………………

Ending cash balance ……………………………………

Problem 7-18A (continued)

2.

Minden Company

Budgeted Income Statement

For the Month of May

Sales ……………………………………………….

$220,000

Cost of goods sold:

Cost of goods sold ………………………………

Gross margin ……………………………………..

Net operating income ………………………….

Interest expense …………………………..……

Net income ……………………………………….

3.

Minden Company

Budgeted Balance Sheet

May 31

Assets

Cash ……………………………………………………………….

$ 22,900

Accounts receivable (40% × $160,000) ………………….

64,000

Inventory …………………………..…………………………….

Total assets ………………………………………………………

Accounts payable (50% × 120,000) ……………………….

Note payable …………………………………………………….

Capital stock …………………………………………………….

Retained earnings ($42,500 + $35,900) ………………….

Problem 7-19A (30 minutes)

1.

December cash sales …………………………….

$ 83,000

Collections on account:

October sales: $400,000 × 18% ……………

November sales: $525,000 × 60% …………

2.

Payments to suppliers:

December purchases: $280,000 × 30% ….

Total cash payments …………………………..

$245,000

3.

Ashton Company

Cash Budget

For the Month of December

Beginning cash balance ……………………………..

$ 40,000

Add collections from customers ……………………

590,000

Total cash available ……………………………………

630,000

Less cash disbursements:

Selling and administrative expenses* ………….

New web server ……………………………………..

Dividends paid ……………………………………….

9,000

Total cash disbursements …………………………...

Financing:

Borrowings ……………………………………………

100,000

Total financing ………………………………………….

100,000

Ending cash balance ………………………………….

$ 20,000

Problem 7-20A (30 minutes)

1. The budget at Springfield is an imposed “top–down” budget that fails to

consider both the need for realistic data and the human interaction

essential to an effective budgeting/control process. The President has

not given any basis for his goals, so one cannot know whether they are

2. Springfield should consider adopting a “bottom–up” budget process. This

means that the people responsible for performance under the budget

would participate in the decisions by which the budget is established. In

addition, this approach requires initial and continuing involvement of

Problem 7-20A (continued)

3. The functional areas should not necessarily be expected to cut costs

when sales volume falls below budget. The time frame of the budget

(one year) is short enough so that many costs are relatively fixed. For

costs that are fixed, there is little hope for a reduction as a consequence

Problem 7-21A (45 minutes)

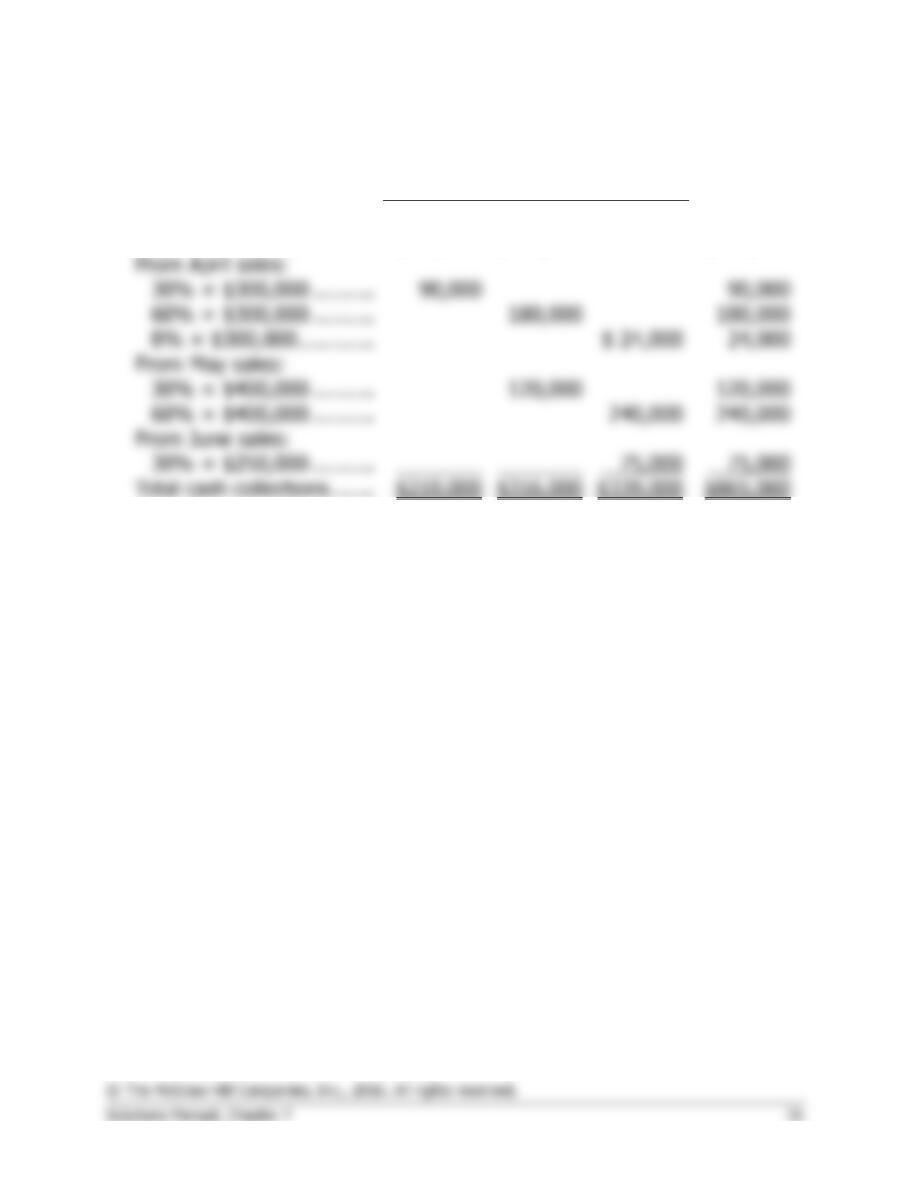

1. Schedule of expected cash collections:

Month

April

May

June

Quarter

From accounts receivable .

$120,000

$ 16,000

$136,000

From May sales:

Problem 7-21A (continued)

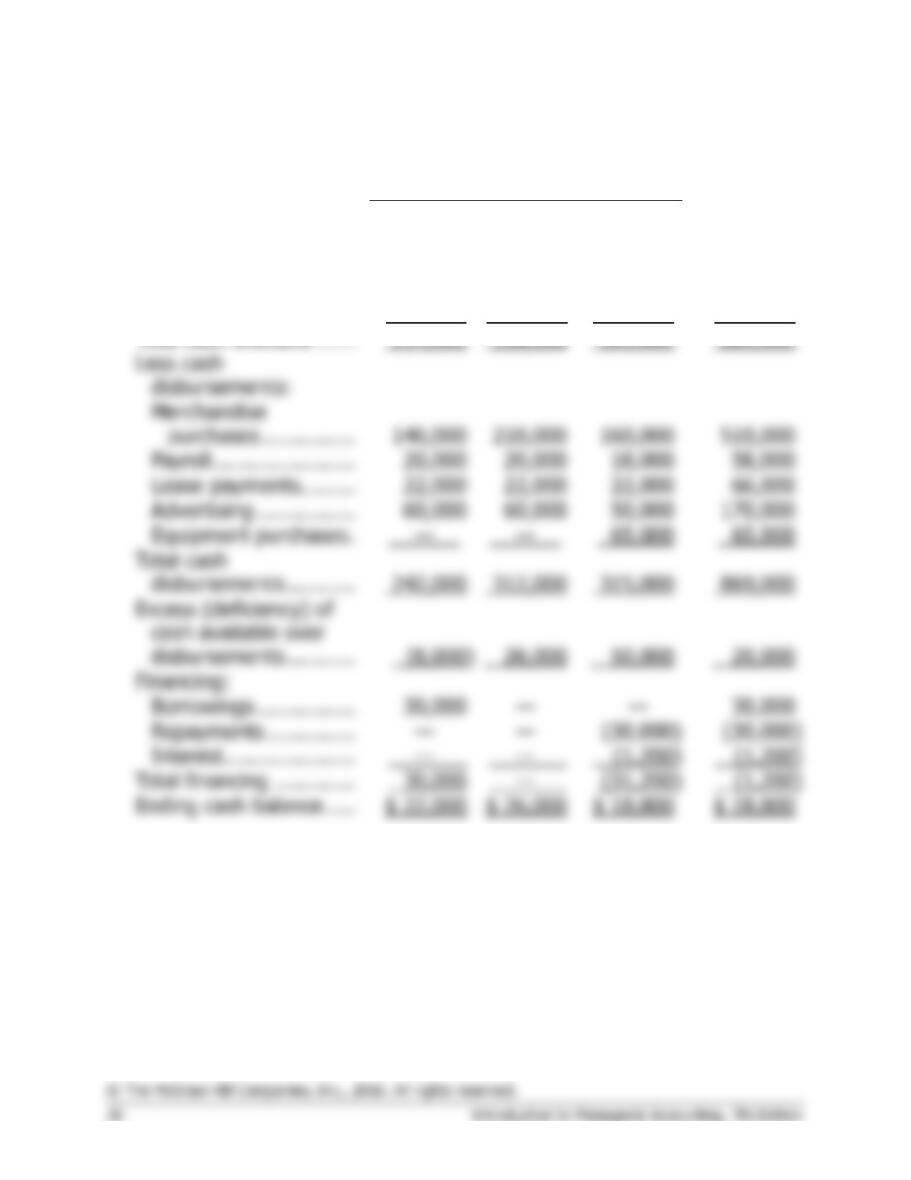

2. Cash budget:

Month

April

May

June

Quarter

Beginning cash balance

$ 24,000

$ 22,000

$ 26,000

$ 24,000

Add receipts:

Collections from

customers ……………

210,000

316,000

339,000

865,000

Total cash available ……

234,000

338,000

365,000

889,000

210,000

Payroll …………………..

Lease payments ………

Advertising …………….

Equipment purchases .

242,000

312,000

315,000

869,000

disbursements ………..

50,000

20,000

Financing:

Borrowings …………….

Repayments …………..

Interest …………………

(1,200)

(1,200)

Total financing ………….

(1,200)

Ending cash balance …..

$ 22,000

$ 26,000

$ 18,800

$ 18,800

3. If the company needs a minimum cash balance of $20,000 to start each

month, the loan cannot be repaid in full by June 30. Some portion of the

loan balance will have to be carried over to July.

Problem 7-22A (60 minutes)

1. Collections on sales:

April

May

June

Quarter

Cash sales …………………..

$120,000

$180,000

$100,000

$ 400,000

Sales on account:

Total cash collections …….

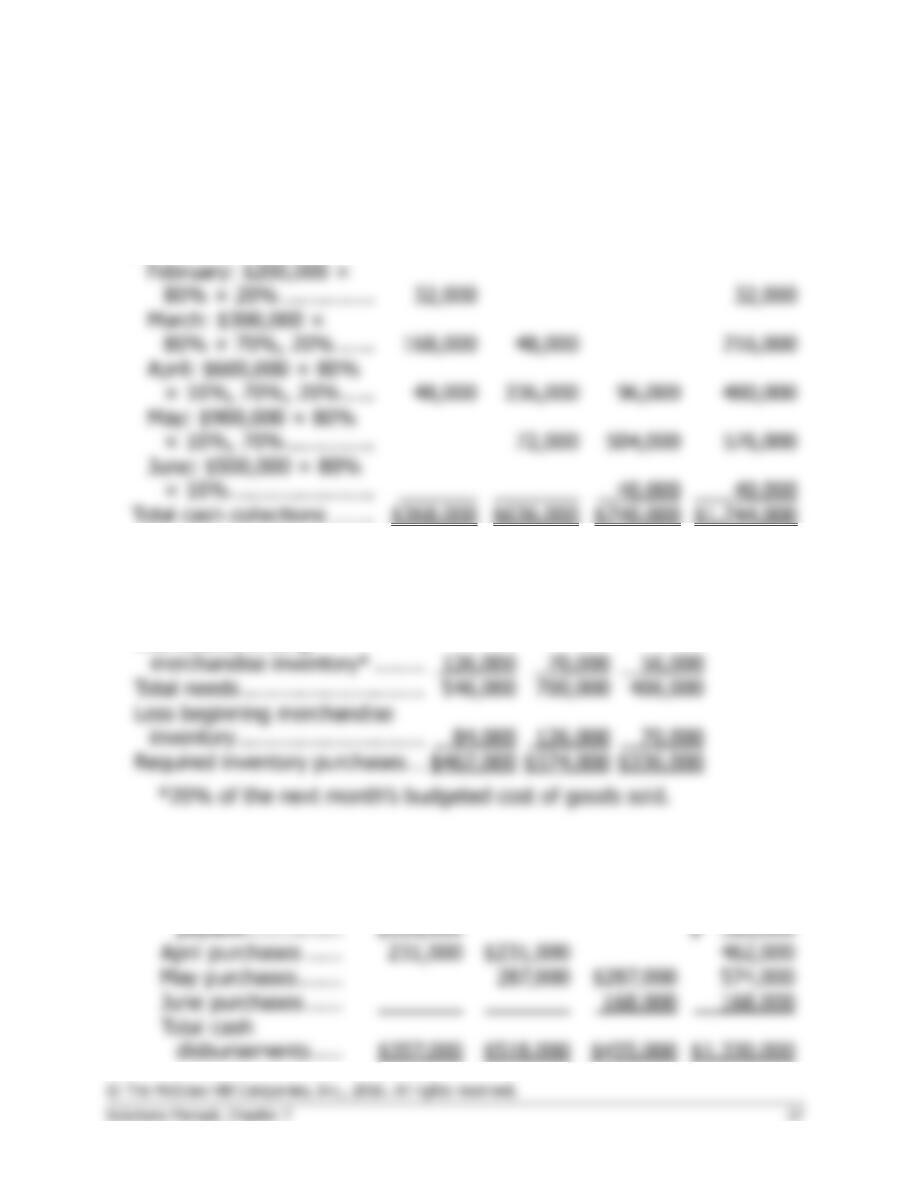

2. a. Merchandise purchases budget:

April

May

June

July

Budgeted cost of goods sold ….

$420,000

$630,000

$350,000

$280,000

Total needs ………………………..

Less beginning merchandise

84,000

70,000

Required inventory purchases…

$462,000

$574,000

$336,000

Add desired ending

b. Schedule of expected cash disbursements for merchandise purchases:

April

May

June

Quarter

April purchases ……

May purchases …….

June purchases ……

Total cash

Beginning accounts

Problem 7-22A (continued)

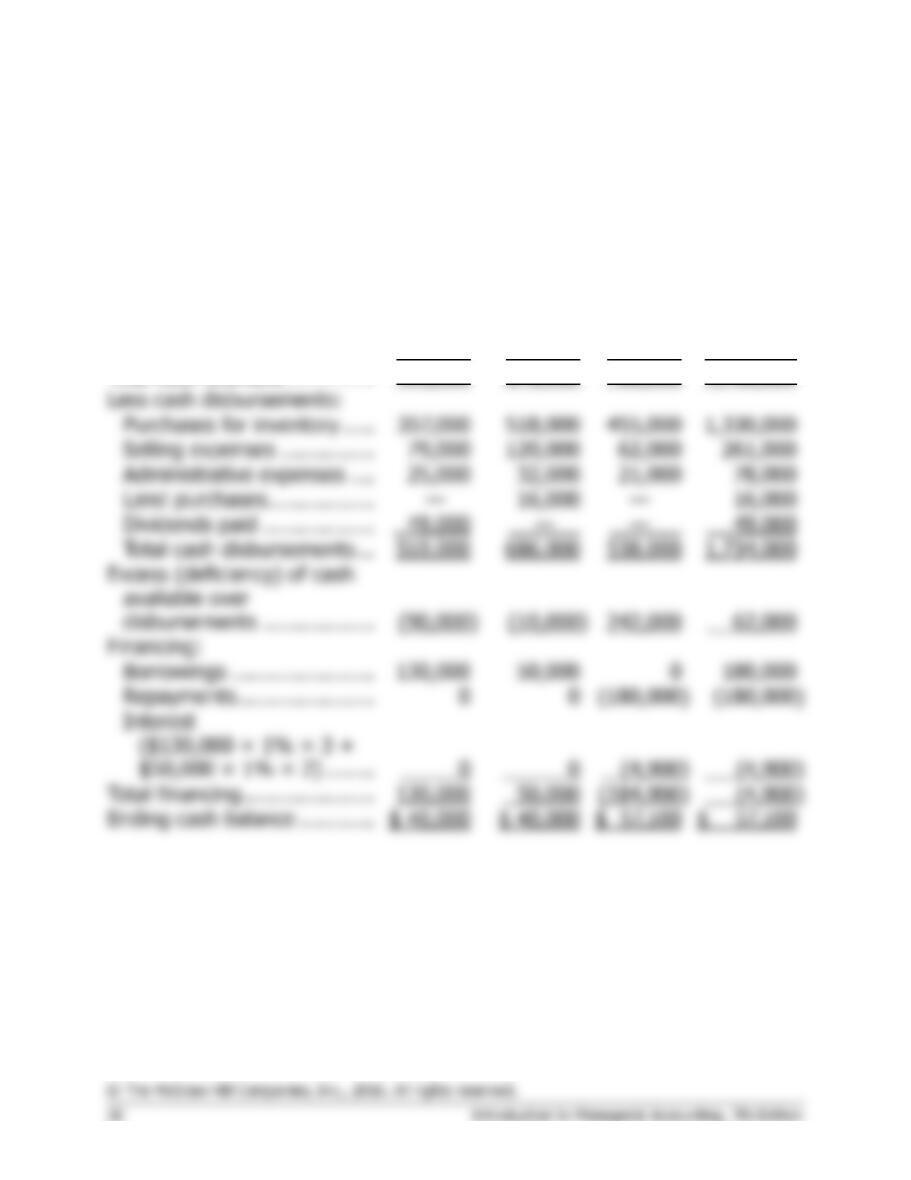

3.

Garden Sales, Inc.

Cash Budget

For the Quarter Ended June 30

April

May

June

Quarter

Beginning cash balance ……..

$ 52,000

$ 40,000

$ 40,000

$ 52,000

Add collections from

customers …………………….

368,000

636,000

740,000

1,744,000

Total cash available …………..

420,000

676,000

780,000

1,796,000

Less cash disbursements:

120,000

242,000

Financing:

Total financing …………………

130,000

Ending cash balance …………

$ 40,000

Problem 7-23A (60 minutes)

1. Collections on sales:

April

May

June

Quarter

Cash sales …………………..

$120,000

$180,000

$100,000

$ 400,000

Sales on account:

Total cash collections …….

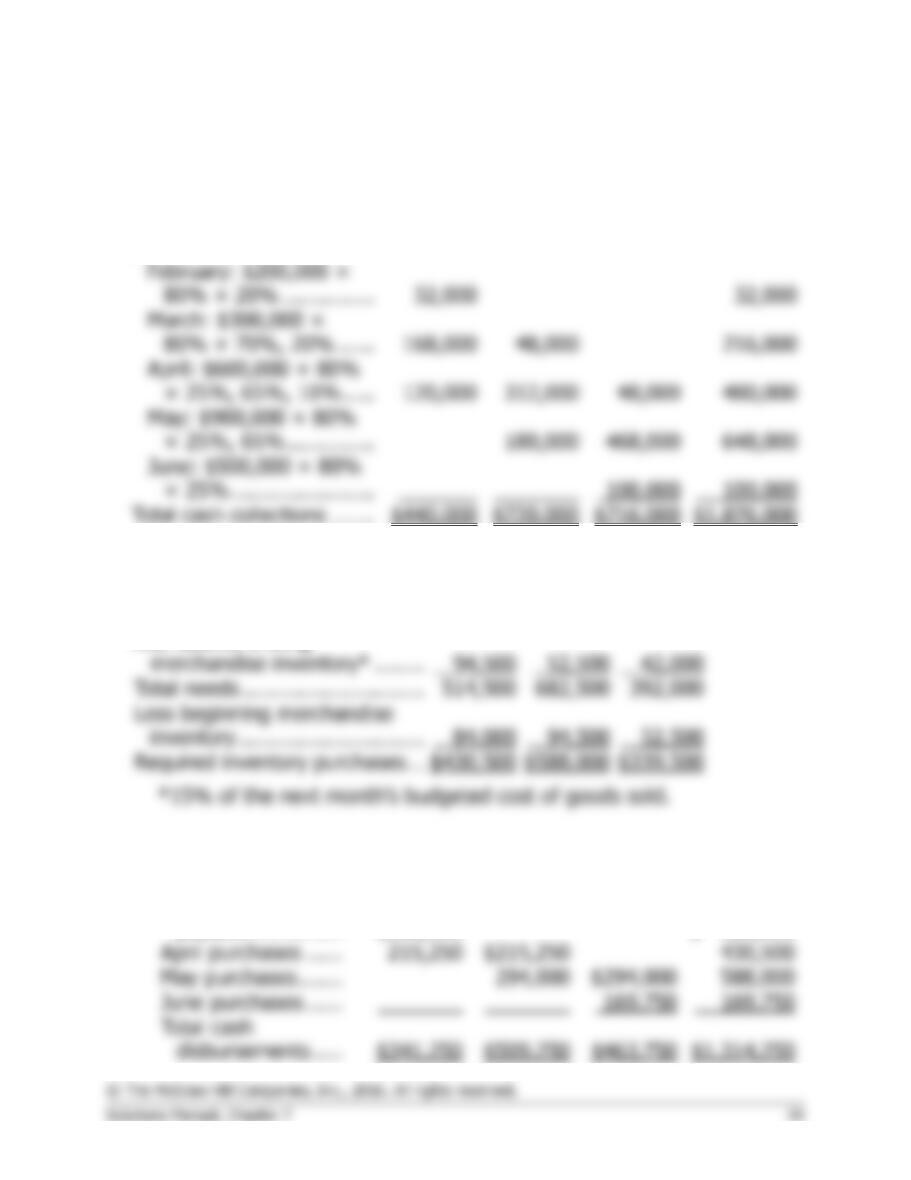

2. a. Merchandise purchases budget:

April

May

June

July

Budgeted cost of goods sold ….

$420,000

$630,000

$350,000

$280,000

Total needs ………………………..

Less beginning merchandise

84,000

52,500

Required inventory purchases…

Add desired ending

b. Schedule of expected cash disbursements for merchandise purchases:

April

May

June

Quarter

Beginning accounts

payable ……………

$126,000

$ 126,000

April purchases ……

May purchases …….

June purchases ……

Total cash

Problem 7-23A (continued)

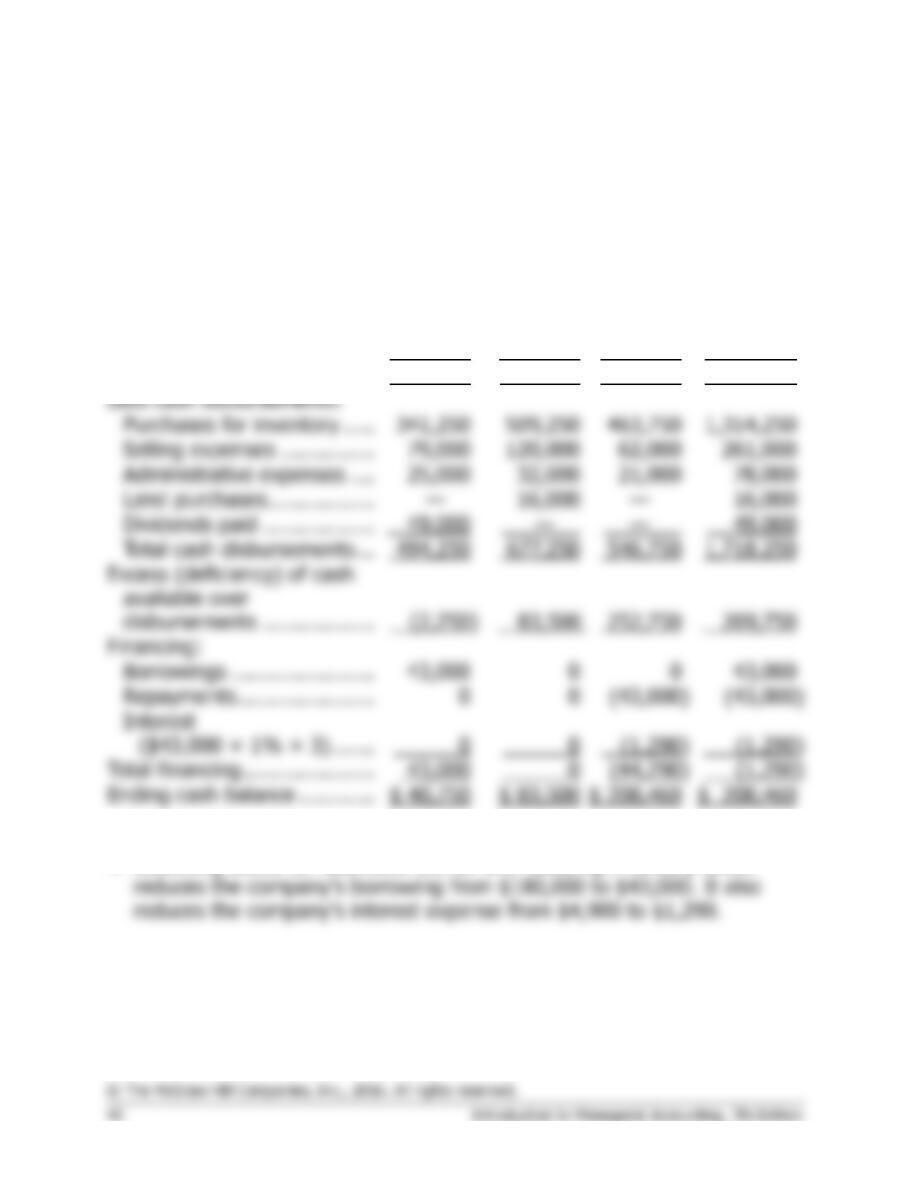

3.

Garden Sales, Inc.

Cash Budget

For the Quarter Ended June 30

April

May

June

Quarter

Beginning cash balance ……..

$ 52,000

$ 40,750

$ 83,500

$ 52,000

Add collections from

customers …………………….

440,000

720,000

716,000

1,876,000

Total cash available …………..

492,000

760,750

799,500

1,928,000

Less cash disbursements:

49,000

677,250

546,750

252,750

209,750

Financing:

Total financing …………………

Ending cash balance …………

$ 208,460

4. Collecting accounts receivable sooner and reducing inventory levels