3-543

136.

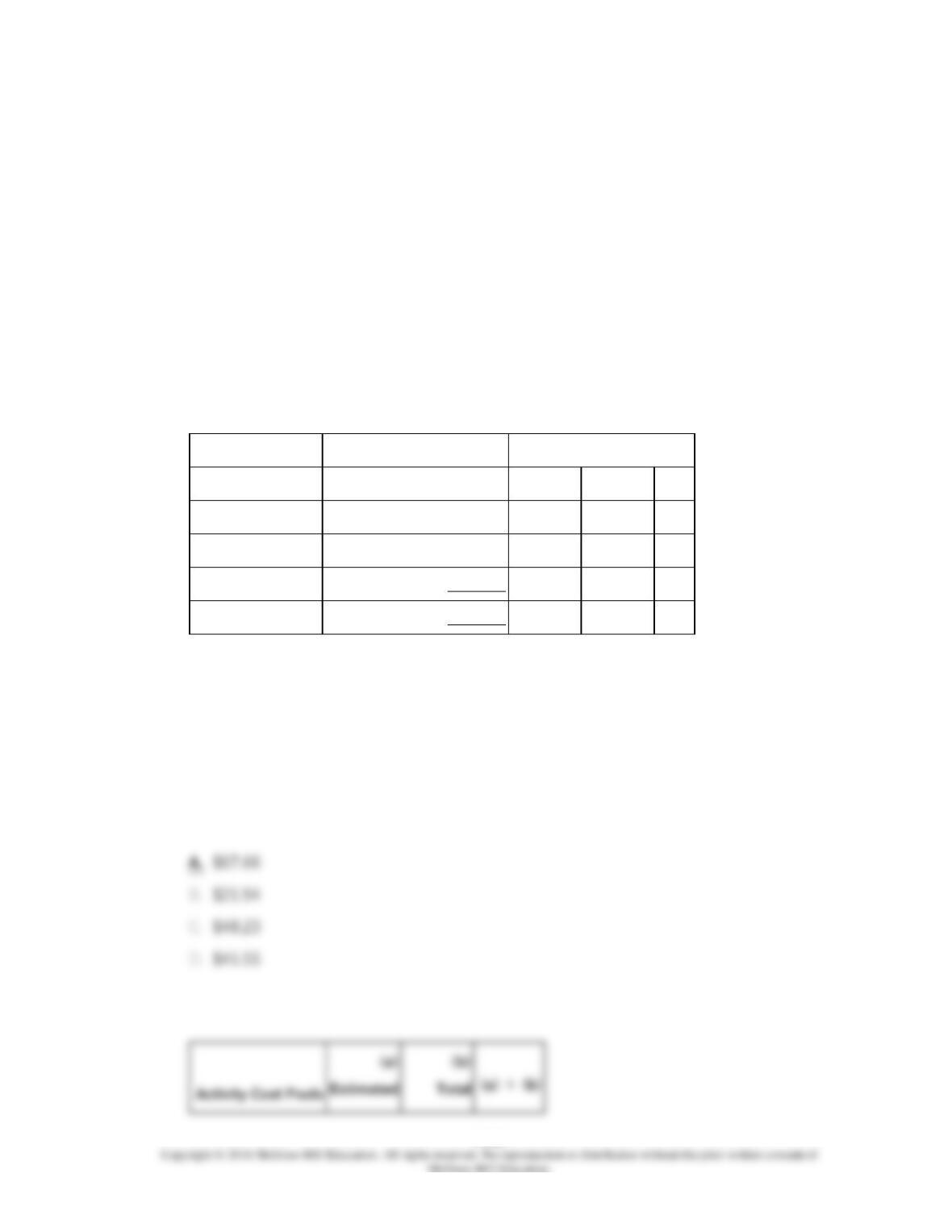

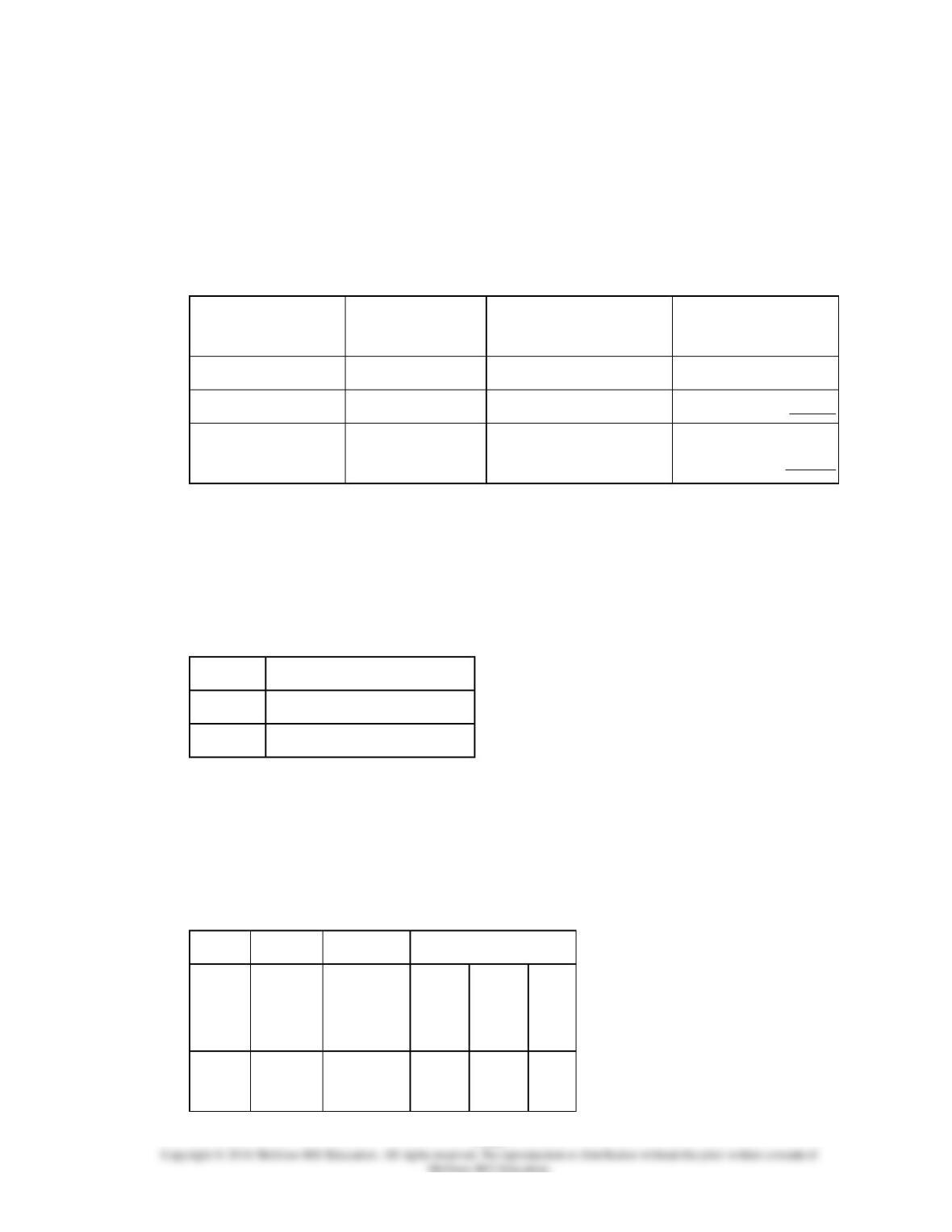

Adams Company has two products: A and B. The annual production and sales of Product A

is 500 units and of Product B is 900 units. The company has traditionally used direct labor-

hours (DLHs) as the basis for applying all manufacturing overhead to products. Product A

requires 0.4 direct labor-hours per unit and Product B requires 0.5 direct labor-hours per

unit. The total estimated overhead for next period is $67,522.

The company is considering switching to an activity-based costing system for the purpose

of computing unit product costs for external reports. The new activity-based costing

system would have three overhead activity cost pools-Activity 1, Activity 2, and General

Factory-with estimated overhead costs and expected activity as follows:

Expected Activity

Activity Cost Pools

Estimated Overhead Costs

Product A

Product B

Total

Activity 1

$6,915

300

200

500

Activity 2

24,948

2,100

700

2,800

General Factory

35,659

200

450

650

Total

$67,522

(Note: The General Factory activity cost pool’s costs are allocated on the basis of direct

labor-hours.)

The predetermined overhead rate under the traditional costing system is closest to:

3-545

3-546

137.

Adams Company has two products: A and B. The annual production and sales of Product A

is 500 units and of Product B is 900 units. The company has traditionally used direct labor-

hours (DLHs) as the basis for applying all manufacturing overhead to products. Product A

requires 0.4 direct labor-hours per unit and Product B requires 0.5 direct labor-hours per

unit. The total estimated overhead for next period is $67,522.

The company is considering switching to an activity-based costing system for the purpose

of computing unit product costs for external reports. The new activity-based costing

system would have three overhead activity cost pools-Activity 1, Activity 2, and General

Factory-with estimated overhead costs and expected activity as follows:

Expected Activity

Activity Cost Pools

Estimated Overhead Costs

Product A

Product B

Total

Activity 1

$6,915

300

200

500

Activity 2

24,948

2,100

700

2,800

General Factory

35,659

200

450

650

Total

$67,522

(Note: The General Factory activity cost pool’s costs are allocated on the basis of direct

labor-hours.)

The overhead cost per unit of Product A under the traditional costing system is closest

to:

3-547

3-548

138.

Adams Company has two products: A and B. The annual production and sales of Product A

is 500 units and of Product B is 900 units. The company has traditionally used direct labor-

hours (DLHs) as the basis for applying all manufacturing overhead to products. Product A

requires 0.4 direct labor-hours per unit and Product B requires 0.5 direct labor-hours per

unit. The total estimated overhead for next period is $67,522.

The company is considering switching to an activity-based costing system for the purpose

of computing unit product costs for external reports. The new activity-based costing

system would have three overhead activity cost pools-Activity 1, Activity 2, and General

Factory-with estimated overhead costs and expected activity as follows:

Expected Activity

Activity Cost Pools

Estimated Overhead Costs

Product A

Product B

Total

Activity 1

$6,915

300

200

500

Activity 2

24,948

2,100

700

2,800

General Factory

35,659

200

450

650

Total

$67,522

(Note: The General Factory activity cost pool’s costs are allocated on the basis of direct

labor-hours.)

The predetermined overhead rate (i.e., activity rate) for Activity 1 under the activity-based

costing system is closest to:

3-549

3-550

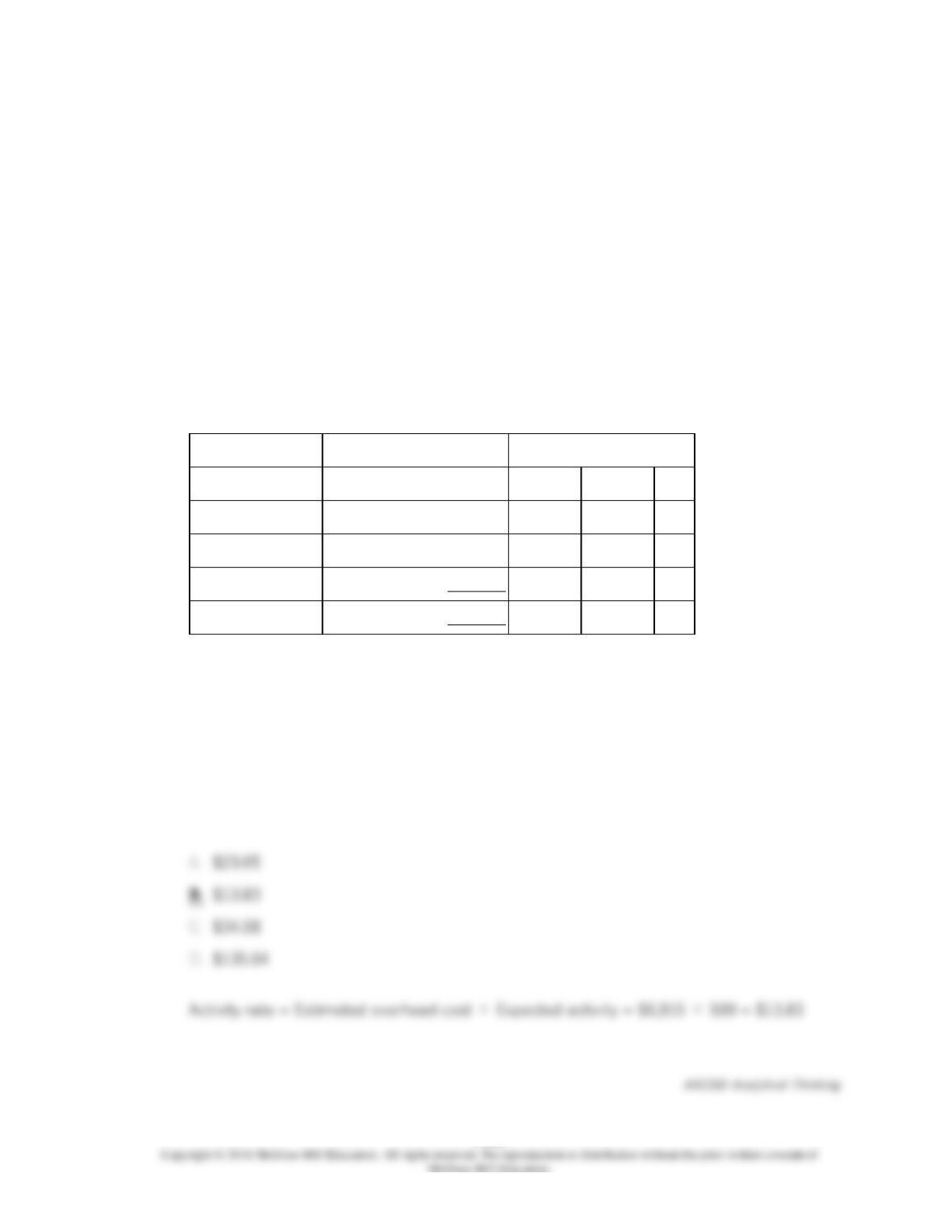

139.

Adams Company has two products: A and B. The annual production and sales of Product A

is 500 units and of Product B is 900 units. The company has traditionally used direct labor-

hours (DLHs) as the basis for applying all manufacturing overhead to products. Product A

requires 0.4 direct labor-hours per unit and Product B requires 0.5 direct labor-hours per

unit. The total estimated overhead for next period is $67,522.

The company is considering switching to an activity-based costing system for the purpose

of computing unit product costs for external reports. The new activity-based costing

system would have three overhead activity cost pools-Activity 1, Activity 2, and General

Factory-with estimated overhead costs and expected activity as follows:

Expected Activity

Activity Cost Pools

Estimated Overhead Costs

Product A

Product B

Total

Activity 1

$6,915

300

200

500

Activity 2

24,948

2,100

700

2,800

General Factory

35,659

200

450

650

Total

$67,522

(Note: The General Factory activity cost pool’s costs are allocated on the basis of direct

labor-hours.)

The overhead cost per unit of Product A under the activity-based costing system is

closest to:

3-551

3-552

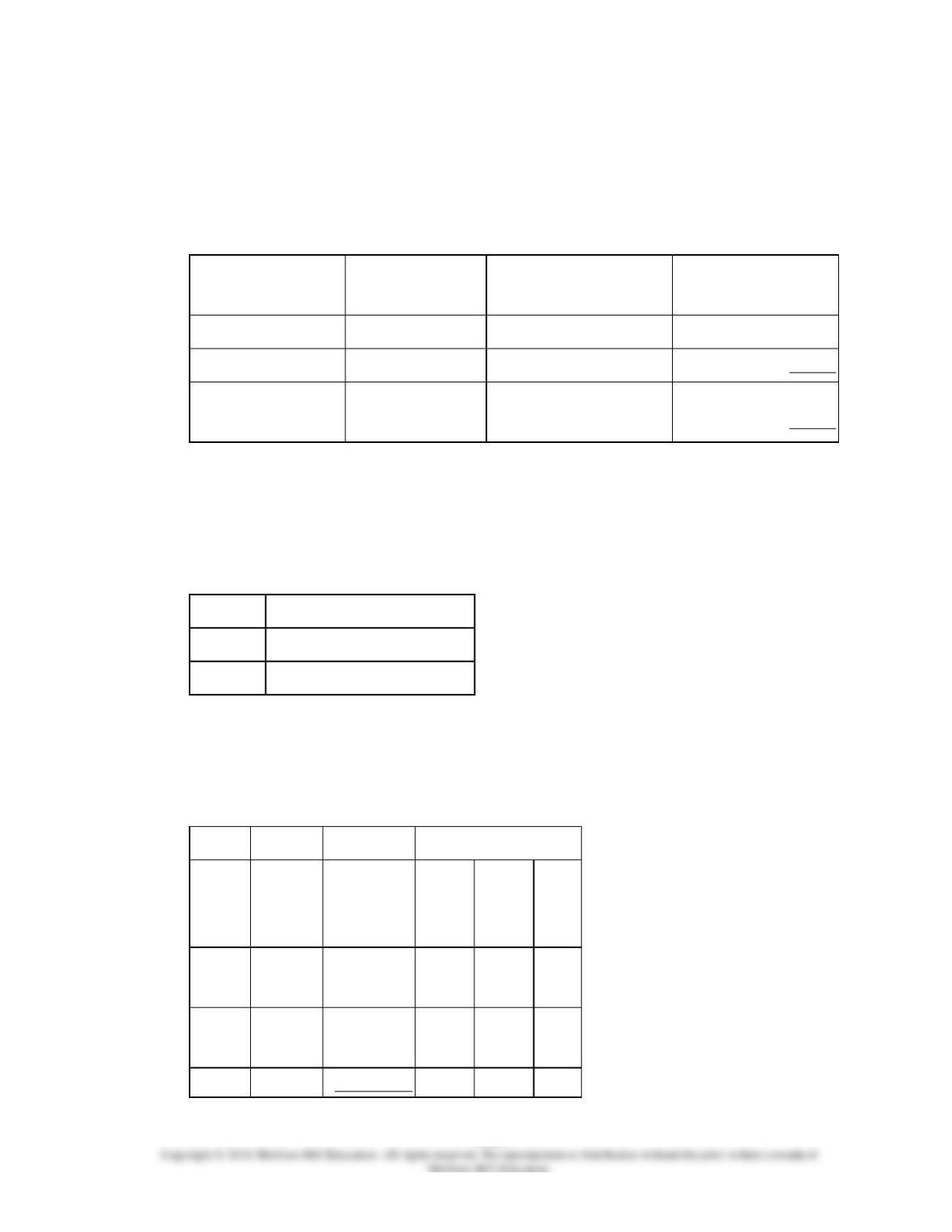

140.

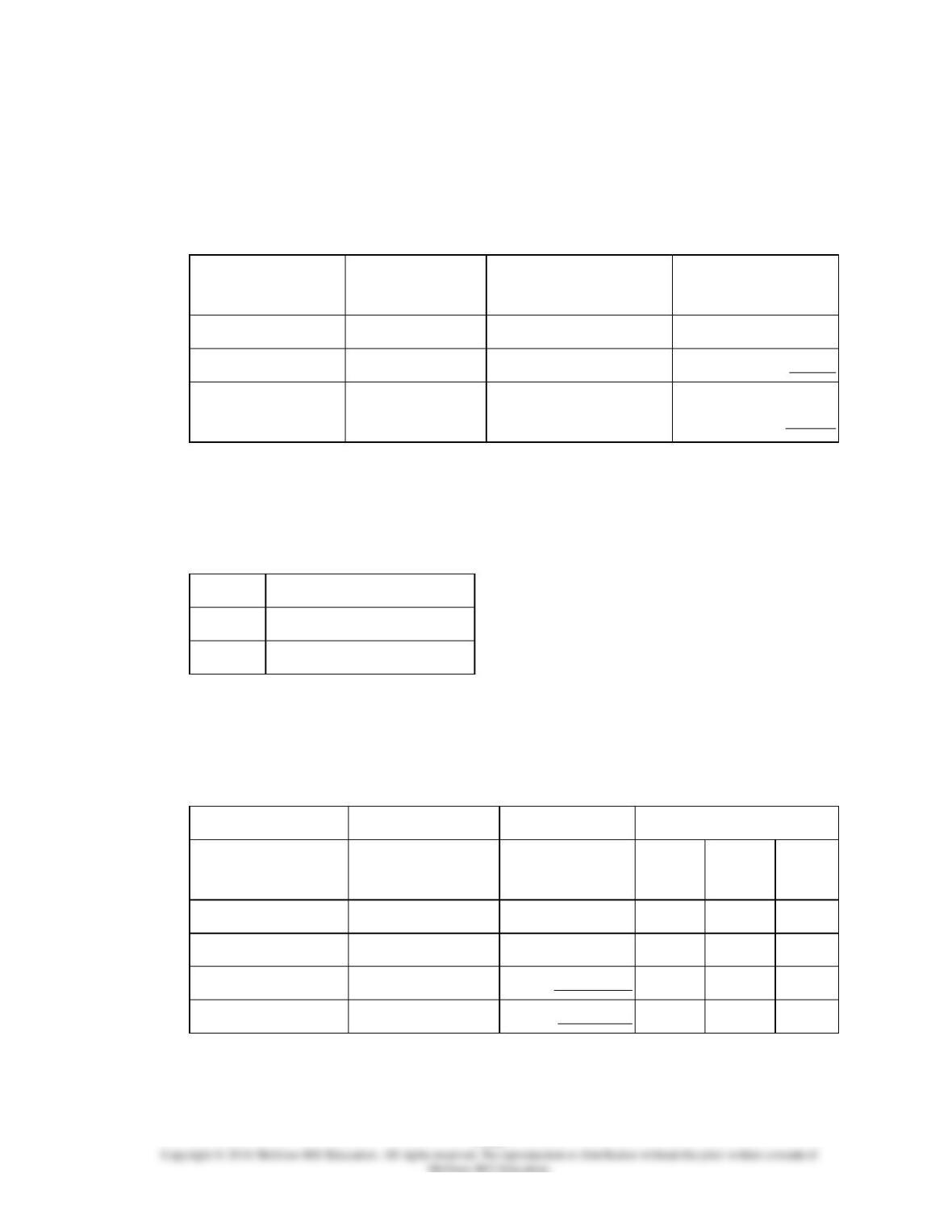

Minon, Inc., manufactures and sells two products: Product J1 and Product E7. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours Per

Unit

Total Direct Labor-

Hours

Product J1

800

7.0

5,600

Product E7

700

8.0

5,600

Total direct labor-

hours

11,200

The direct labor rate is $19.90 per DLH. The direct materials cost per unit for each

product is given below:

Direct Materials Cost per Unit

Product J1

$268.20

Product E7

$165.80

The company is considering adopting an activity-based costing system with the following

activity cost pools, activity measures, and expected activity:

Expected Activity

Activity

Cost

Pools

Activity

Measures

Estimated

Overhead

Cost

Product

J1

Product

E7

Total

Labor-

related

DLHs

$372,512

5,600

5,600

11,200

Machine

setups

setups

41,670

300

200

500

General

MHs

404,504

3,000

2,900

5,900

3-553

factory

$818,686

If the company allocates all of its overhead based on direct labor-hours using its

traditional costing method, the predetermined overhead rate would be closest to:

3-554

141.

Minon, Inc., manufactures and sells two products: Product J1 and Product E7. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours Per

Unit

Total Direct Labor-

Hours

Product J1

800

7.0

5,600

Product E7

700

8.0

5,600

Total direct labor-

hours

11,200

The direct labor rate is $19.90 per DLH. The direct materials cost per unit for each

product is given below:

Direct Materials Cost per Unit

Product J1

$268.20

Product E7

$165.80

The company is considering adopting an activity-based costing system with the following

activity cost pools, activity measures, and expected activity:

Expected Activity

Activity

Cost

Pools

Activity

Measures

Estimated

Overhead

Cost

Product

J1

Product

E7

Total

Labor-

related

DLHs

$372,512

5,600

5,600

11,200

3-555

Machine

setups

setups

41,670

300

200

500

General

factory

MHs

404,504

3,000

2,900

5,900

$818,686

If the company allocates all of its overhead based on direct labor-hours using its

traditional costing method, the overhead assigned to each unit of Product J1 would be

closest to:

3-556

142.

Minon, Inc., manufactures and sells two products: Product J1 and Product E7. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours Per

Unit

Total Direct Labor-

Hours

Product J1

800

7.0

5,600

Product E7

700

8.0

5,600

Total direct labor-

hours

11,200

The direct labor rate is $19.90 per DLH. The direct materials cost per unit for each

product is given below:

Direct Materials Cost per Unit

Product J1

$268.20

Product E7

$165.80

The company is considering adopting an activity-based costing system with the following

activity cost pools, activity measures, and expected activity:

Expected Activity

Activity

Cost

Pools

Activity

Measures

Estimated

Overhead

Cost

Product

J1

Product

E7

Total

Labor-

related

DLHs

$372,512

5,600

5,600

11,200

3-557

Machine

setups

setups

41,670

300

200

500

General

factory

MHs

404,504

3,000

2,900

5,900

$818,686

The activity rate for the Labor-Related activity cost pool under activity-based costing is

closest to:

3-558

143.

Minon, Inc., manufactures and sells two products: Product J1 and Product E7. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours Per

Unit

Total Direct Labor-

Hours

Product J1

800

7.0

5,600

Product E7

700

8.0

5,600

Total direct labor-

hours

11,200

The direct labor rate is $19.90 per DLH. The direct materials cost per unit for each

product is given below:

Direct Materials Cost per Unit

Product J1

$268.20

Product E7

$165.80

The company is considering adopting an activity-based costing system with the following

activity cost pools, activity measures, and expected activity:

Expected Activity

Activity Cost Pools

Activity Measures

Estimated

Overhead Cost

Product

J1

Product

E7

Total

Labor-related

DLHs

$372,512

5,600

5,600

11,200

Machine setups

setups

41,670

300

200

500

General factory

MHs

404,504

3,000

2,900

5,900

$818,686

The overhead applied to each unit of Product J1 under activity-based costing is closest

to:

3-559

3-560

3-561

144.

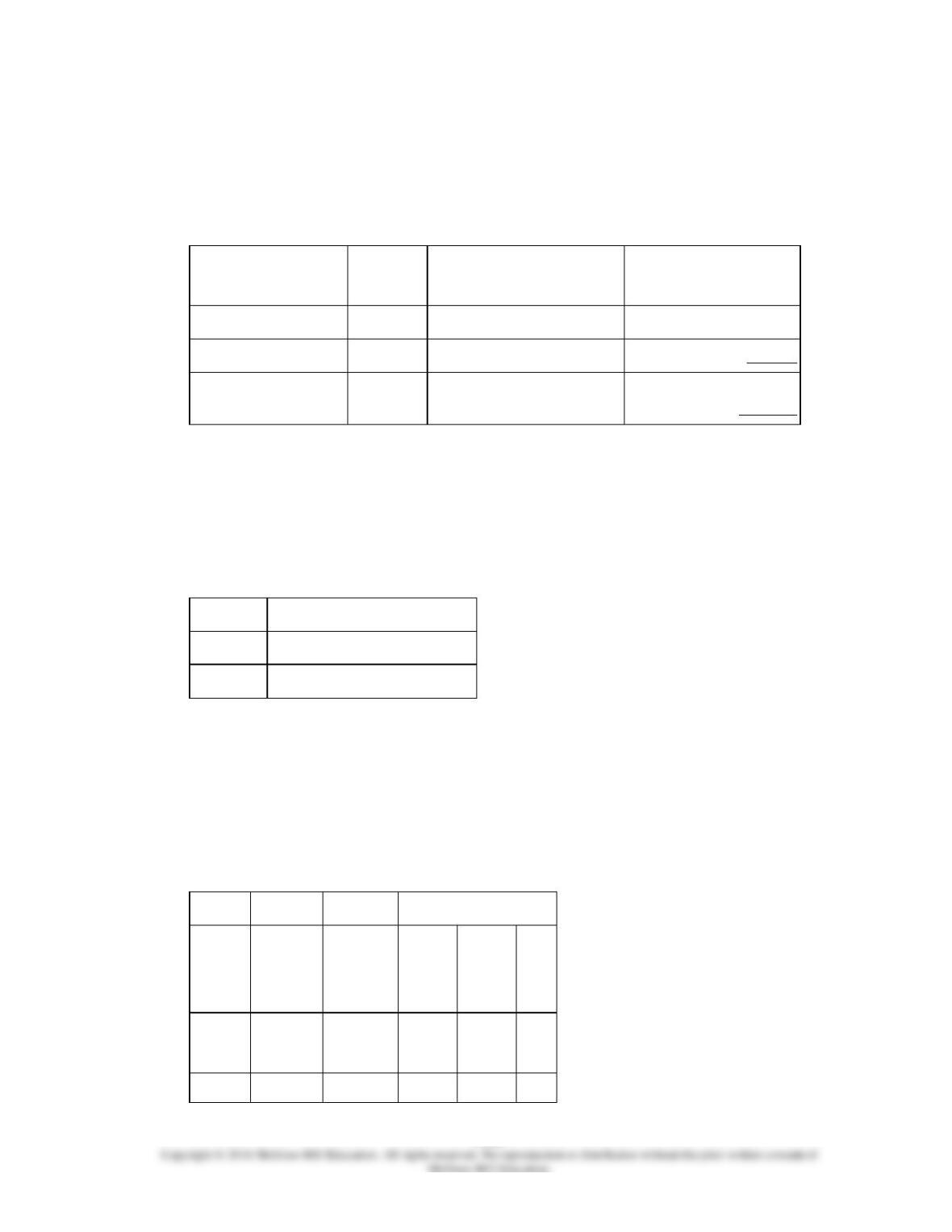

Punches, Inc., manufactures and sells two products: Product H7 and Product Y2. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours Per Unit

Total Direct Labor-Hours

Product H7

100

6.0

600

Product Y2

900

4.0

3,600

Total direct labor-hours

4,200

The direct labor rate is $17.80 per DLH. The direct materials cost per unit for each

product is given below:

Direct Materials Cost per Unit

Product H7

$132.50

Product Y2

$266.40

The company is considering adopting an activity-based costing system with the following

activity cost pools, activity measures, and expected activity:

Expected Activity

Activity

Cost

Pools

Activity

Measures

Estimated

Overhead

Cost

Product

H7

Product

Y2

Total

Labor-

related

DLHs

$205,296

600

3,600

4,200

Machine

setups

38,380

400

600

1,000

3-562

setups

General

factory

MHs

528,198

3,400

3,200

6,600

$771,874

If the company allocates all of its overhead based on direct labor-hours using its

traditional costing method, the overhead assigned to each unit of Product Y2 would be

closest to: