Analytical Thinking (continued)

Allocation of common fixed expenses on the basis of sales revenue:

Velcro

Metal

Nylon

Total

Sales ……………………………..

$165,000

$300,000

$340,000

$805,000

Percentage of total sales ……

20.497%

37.267%

42.236%

100.0%

Product fixed expenses ……..

$169,441

$161,366

$400,000

Unit contribution margin (b) .

268,943

*Total common fixed expense × percentage of total sales

If the company sells 172,983 units of the Velcro product, 211,801 units of

the Metal product, and 268,943 units of the Nylon product, the company

will indeed break even overall. However, the apparent break-evens for two

of the products are higher than their normal annual sales.

Velcro

Metal

Nylon

Normal annual sales volume ….

Analytical Thinking (continued)

If the managers drop the Velcro and Metal products, the company would

face a loss of $60,000 computed as follows:

Velcro

Metal

Nylon

Total

Sales ……………………….

dropped

dropped

$340,000

$340,000

Variable expenses ………

100,000

Contribution margin ……

$240,000

Fixed expenses* ………..

Net operating loss ………

By dropping the two products, the company would go from making a profit

of $40,000 to suffering a loss of $60,000. The reason is that the two

dropped products were contributing $100,000 toward covering common

fixed expenses and toward profits. This can be verified by looking at a

segmented income statement like the one that will be introduced in a later

chapter.

Velcro

Metal

Nylon

Total

Sales ……………………………..

$165,000

$300,000

$340,000

$805,000

Variable expenses …………….

100,000

Contribution margin ………….

240,000

Product fixed expenses ……..

80,000

Product segment margin ……

$180,000

Common fixed expenses …….

Net operating income ………..

Teamwork in Action

1. The answer to this question will vary from school to school.

2. Managers will hire more support staff, such as security and vending

personnel, for big games that predictably draw more people. These

on.

3. The answer to this question will vary from school to school, but a clear

distinction should be drawn between the costs that are variable with

4. The answer to this question will vary from school to school. The lost

5. The answer to this question will vary from school to school.

Chapter 5

Take Two Solutions

Exercise 5-4 (10 minutes)

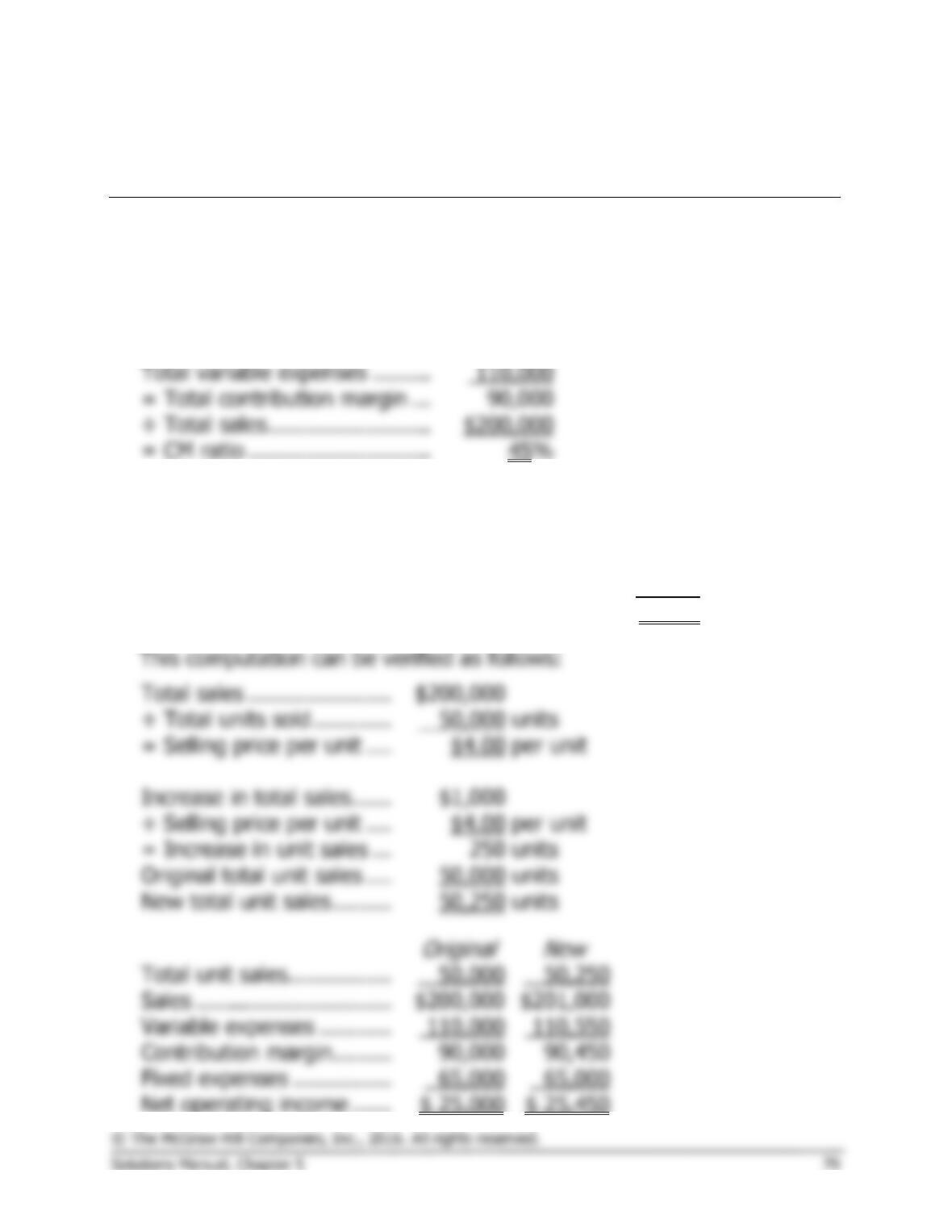

1. The company’s contribution margin (CM) ratio is:

Total sales ……………………….

$200,000

÷ Total sales …………………….

$200,000

= CM ratio ……………………….

2. The change in net operating income from an increase in total sales of

$1,000 can be estimated by using the CM ratio as follows:

Change in total sales …………………………………

$1,000

× CM ratio ………………………………………………

45

%

= Estimated change in net operating income ….

$ 450

÷ Total units sold …………

units

per unit

Increase in total sales ……

Original total unit sales ….

units

New total unit sales ………

units

Sales …………………………

Variable expenses ………..

Contribution margin ………

Exercise 5-5 (20 minutes)

1. The following table shows the effect of the proposed change in monthly

advertising budget:

Sales With

Additional

Current

Advertising

Sales

Budget

Difference

Sales …………………………

$200,000

$209,000

$ 9,000

Variable expenses ………..

Net operating income ……

$ 400

Alternative Solution 1

Expected total contribution margin:

$209,000 × 60% CM ratio ………………

$125,400

Change in fixed expenses:

Change in net operating income …………

Less incremental advertising expense ….

Exercise 5-5 (continued)

2. The $2 increase in variable expense will cause the unit contribution

margin to decrease from $60 to $58 with the following impact on net

operating income:

Exercise 5-6 (20 minutes)

1. The equation method yields the break-even point in unit sales, Q, as

follows:

2. The equation method can be used to compute the break-even point in

dollar sales as follows:

3. The formula method gives an answer that is identical to the equation

method for the break-even point in unit sales:

Exercise 5-6 (continued)

4. The formula method also gives an answer that is identical to the

equation method for the break-even point in dollar sales:

Exercise 5-7 (10 minutes)

1. The equation method yields the required unit sales, Q, as follows:

2. The formula approach yields the required unit sales as follows:

Exercise 5-8 (10 minutes)

1. To compute the margin of safety, we must first compute the break-even

unit sales.

2. The margin of safety as a percentage of sales is as follows:

Exercise 5-9 (20 minutes)

1. The company’s degree of operating leverage would be computed as

follows:

Contribution margin (a) ……………………..

Net operating income (b) ……………………

2. A 5% increase in sales should result in a 16.88% increase in net

operating income, computed as follows:

3. The new income statement reflecting the change in sales is:

Amount

Percent

of Sales

Sales ………………………

$94,500

100%

Original net operating income (a) ………………………

Change in net operating income (b) …………………..

Exercise 5-10 (20 minutes)

1. The overall contribution margin ratio can be computed as follows:

2. The overall break-even point in dollar sales can be computed as follows:

3. To construct the required income statement, we must first determine

the relative sales mix for the two products:

Claimjumper

Makeover

Total

Original dollar sales ……

$30,000

$70,000

$100,000

Percent of total …………

Sales at break-even ……

Claimjumper

Makeover

Total

Sales ………………………

Variable expenses* …….

Contribution margin ……

Fixed expenses …………

Net operating income …

Exercise 5-15 (15 minutes)

1.

Total

Per

Unit

Sales (15,000 games) ………

$300,000

$20

Variable expenses ……………

90,000

6

Contribution margin …………

Fixed expenses ……………….

Net operating income ………

2. a. Sales of 18,000 games represent a 20% increase over last year’s

sales. Because the degree of operating leverage is 10, net operating

income should increase by 10 times as much, or by 200% (10 ×

20%).

Total expected net operating income …………….

Exercise 5-17 (30 minutes)

= $108,000 ÷ $20

= 5,400 stoves, or, at $50 per stove, $270,000 in sales

Alternative solution:

2. An increase in variable expenses as a percentage of the selling price

would result in a higher break-even point. If variable expenses increase

as a percentage of sales, then the contribution margin will decrease as a

percentage of sales. With a lower CM ratio, more stoves would have to

be sold to generate enough contribution margin to cover the fixed costs.

3.

Present:

8,000 Stoves

Proposed:

10,000 Stoves*

Total

Per Unit

Total

Per Unit

Sales ……………………….

$400,000

$50

$450,000

$45

**

Exercise 5-17 (continued)

4.

Profit

= Unit CM × Q − Fixed expenses

= ($45 − $30) × Q − $108,000

= ($15) × Q − $108,000

= $143,000

Q

= $143,000 ÷ $15

Q

= 9,533 stoves (rounded)

Alternative solution: