7-201

145.

Muecke Inc. is working on its cash budget for April. The budgeted beginning cash balance is

$40,000. Budgeted cash receipts total $150,000 and budgeted cash disbursements total

$158,000. The desired ending cash balance is $50,000.

To attain its desired ending cash balance for April, the company needs to borrow:

7-202

146.

The Adams Corporation, a merchandising firm, has budgeted its activity for November

according to the following information:

• Sales at $450,000, all for cash.

• Merchandise inventory on October 31 was $200,000.

• The cash balance November 1 was $18,000.

• Selling and administrative expenses are budgeted at $60,000 for November and are paid for

in cash.

• Budgeted depreciation for November is $25,000.

• The planned merchandise inventory on November 30 is $230,000.

• The cost of goods sold is 70% of the selling price.

• All purchases are paid for in cash.

• There is no interest expense or income tax expense.

The budgeted cash receipts for November are:

7-203

147.

The Adams Corporation, a merchandising firm, has budgeted its activity for November

according to the following information:

• Sales at $450,000, all for cash.

• Merchandise inventory on October 31 was $200,000.

• The cash balance November 1 was $18,000.

• Selling and administrative expenses are budgeted at $60,000 for November and are paid for

in cash.

• Budgeted depreciation for November is $25,000.

• The planned merchandise inventory on November 30 is $230,000.

• The cost of goods sold is 70% of the selling price.

• All purchases are paid for in cash.

• There is no interest expense or income tax expense.

The budgeted cash disbursements for November are:

7-204

148.

The Adams Corporation, a merchandising firm, has budgeted its activity for November

according to the following information:

• Sales at $450,000, all for cash.

• Merchandise inventory on October 31 was $200,000.

• The cash balance November 1 was $18,000.

• Selling and administrative expenses are budgeted at $60,000 for November and are paid for

in cash.

• Budgeted depreciation for November is $25,000.

• The planned merchandise inventory on November 30 is $230,000.

• The cost of goods sold is 70% of the selling price.

• All purchases are paid for in cash.

• There is no interest expense or income tax expense.

The budgeted net income for November is:

7-205

149.

Carter Lumber sells lumber and general building supplies to building contractors in a medium-

sized town in Montana. Data regarding the store’s operations follow:

o Sales are budgeted at $380,000 for November, $390,000 for December, and $400,000 for

January.

o Collections are expected to be 70% in the month of sale, 27% in the month following the

sale, and 3% uncollectible.

o The cost of goods sold is 65% of sales.

o The company desires to have an ending merchandise inventory equal to 80% of the

following month’s cost of goods sold. Payment for merchandise is made in the month following

the purchase.

o Other monthly expenses to be paid in cash are $22,000.

o Monthly depreciation is $20,000.

o Ignore taxes.

Balance Sheet

October 31

Assets

Cash

$13,000

Accounts receivable, net of allowance for uncollectible accounts

77,000

Inventory

197,600

Property, plant and equipment, net of $502,000 accumulated depreciation

992,000

Total assets

$1,279,600

Liabilities and Stockholders’ Equity

Accounts payable

$240,000

Common stock

780,000

Retained earnings

259,600

Total liabilities and stockholders’ equity

$1,279,600

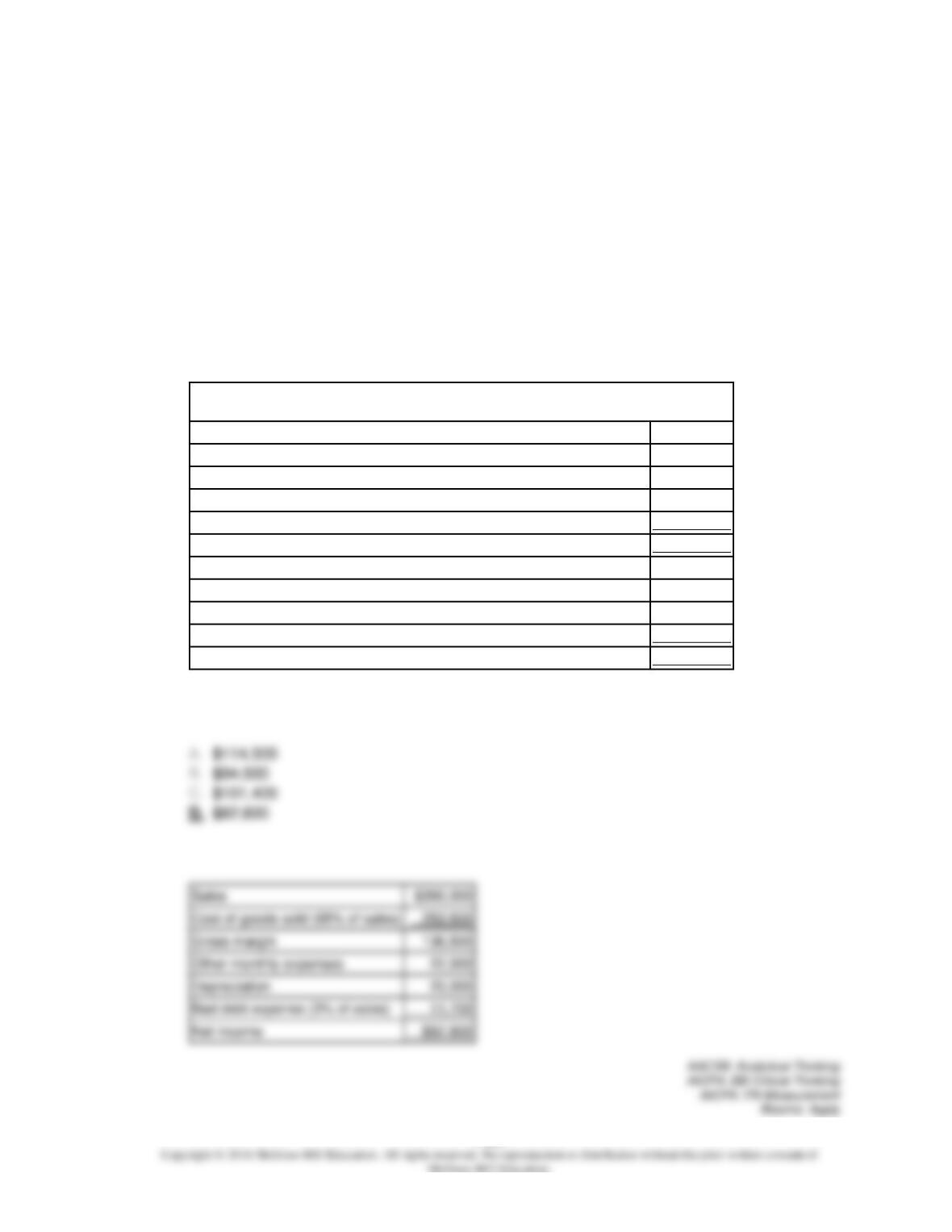

Sales

Cost of goods sold (65% of sales)

Gross margin

Other monthly expenses

Depreciation

Bad debt expense (3% of sales)

11,700

Net income

$82,800

The net income for December would be:

7-206

7-207

150.

Carter Lumber sells lumber and general building supplies to building contractors in a medium-

sized town in Montana. Data regarding the store’s operations follow:

o Sales are budgeted at $380,000 for November, $390,000 for December, and $400,000 for

January.

o Collections are expected to be 70% in the month of sale, 27% in the month following the

sale, and 3% uncollectible.

o The cost of goods sold is 65% of sales.

o The company desires to have an ending merchandise inventory equal to 80% of the

following month’s cost of goods sold. Payment for merchandise is made in the month following

the purchase.

o Other monthly expenses to be paid in cash are $22,000.

o Monthly depreciation is $20,000.

o Ignore taxes.

Balance Sheet

October 31

Assets

Cash

$13,000

Accounts receivable, net of allowance for uncollectible accounts

77,000

Inventory

197,600

Property, plant and equipment, net of $502,000 accumulated depreciation

992,000

Total assets

$1,279,600

Liabilities and Stockholders’ Equity

Accounts payable

$240,000

Common stock

780,000

Retained earnings

259,600

Total liabilities and stockholders’ equity

$1,279,600

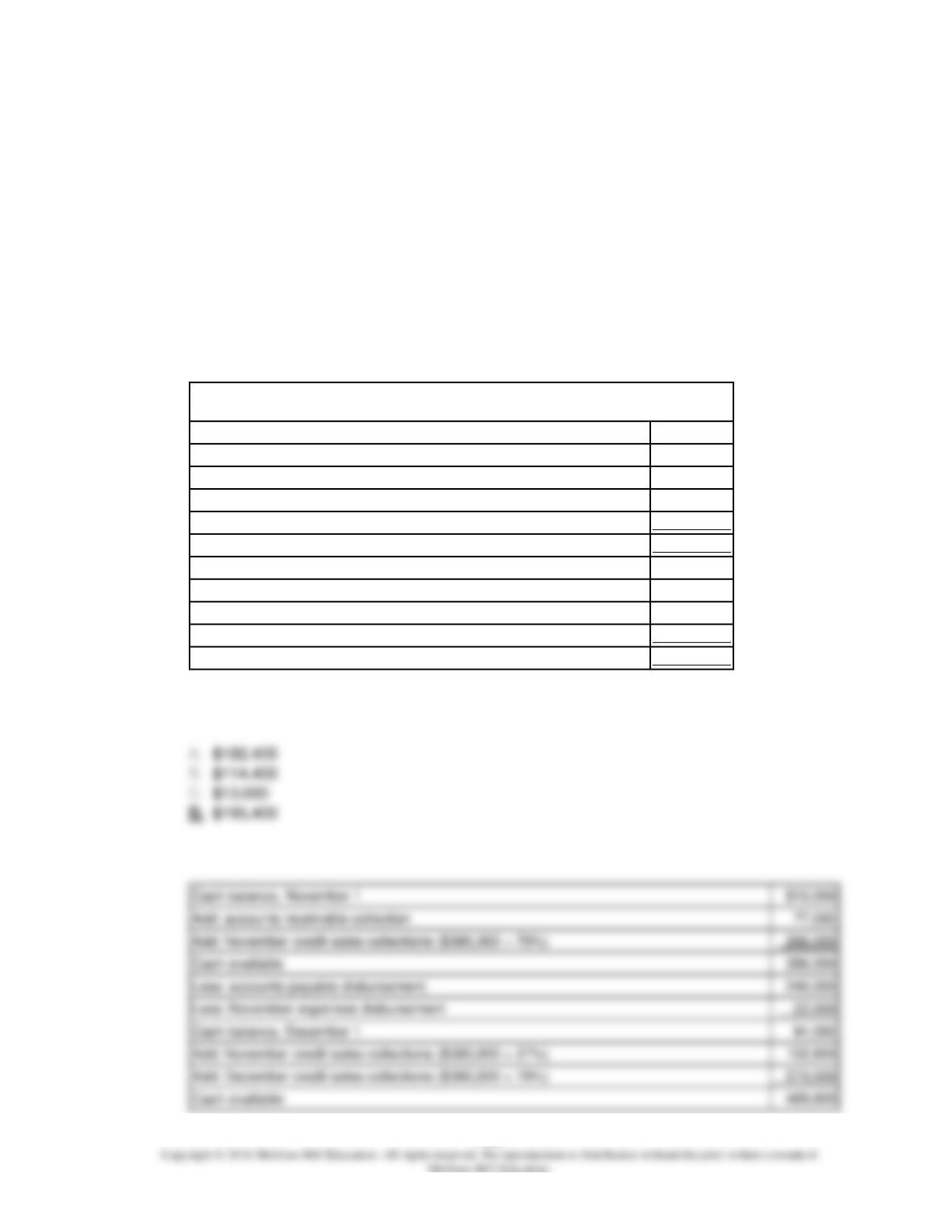

Cash balance, November 1

Add: accounts receivable collection

77,000

Add: November credit sales collections ($380,000 × 70%)

Cash available

Less: accounts payable disbursement

Less: November expenses disbursement

Cash balance, December 1

Add: November credit sales collections ($380,000 × 27%)

The cash balance at the end of December would be:

7-208

7-209

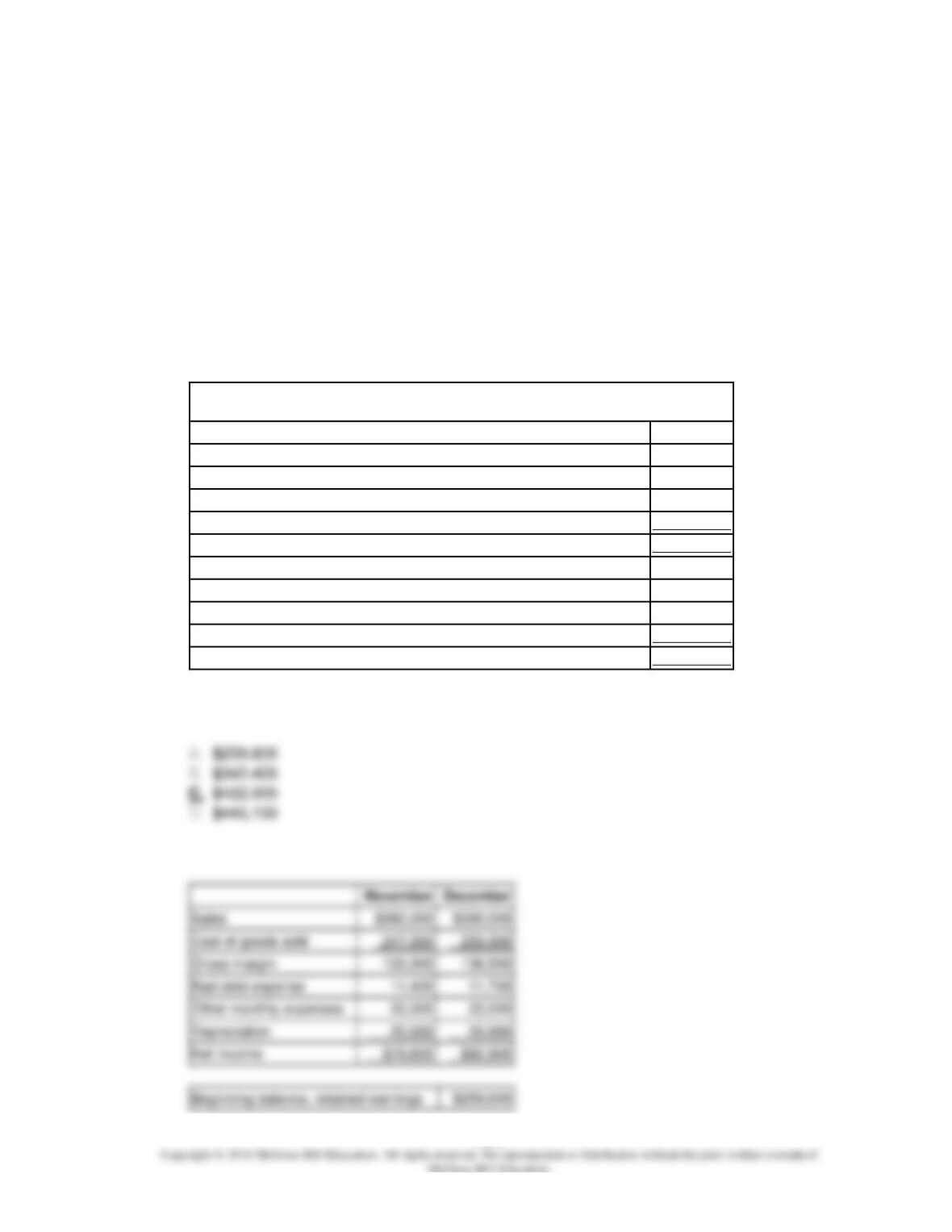

151.

Carter Lumber sells lumber and general building supplies to building contractors in a medium-

sized town in Montana. Data regarding the store’s operations follow:

o Sales are budgeted at $380,000 for November, $390,000 for December, and $400,000 for

January.

o Collections are expected to be 70% in the month of sale, 27% in the month following the

sale, and 3% uncollectible.

o The cost of goods sold is 65% of sales.

o The company desires to have an ending merchandise inventory equal to 80% of the

following month’s cost of goods sold. Payment for merchandise is made in the month following

the purchase.

o Other monthly expenses to be paid in cash are $22,000.

o Monthly depreciation is $20,000.

o Ignore taxes.

Balance Sheet

October 31

Assets

Cash

$13,000

Accounts receivable, net of allowance for uncollectible accounts

77,000

Inventory

197,600

Property, plant and equipment, net of $502,000 accumulated depreciation

992,000

Total assets

$1,279,600

Liabilities and Stockholders’ Equity

Accounts payable

$240,000

Common stock

780,000

Retained earnings

259,600

Total liabilities and stockholders’ equity

$1,279,600

The accounts receivable balance, net of uncollectible accounts, at the end of December

would be:

7-210

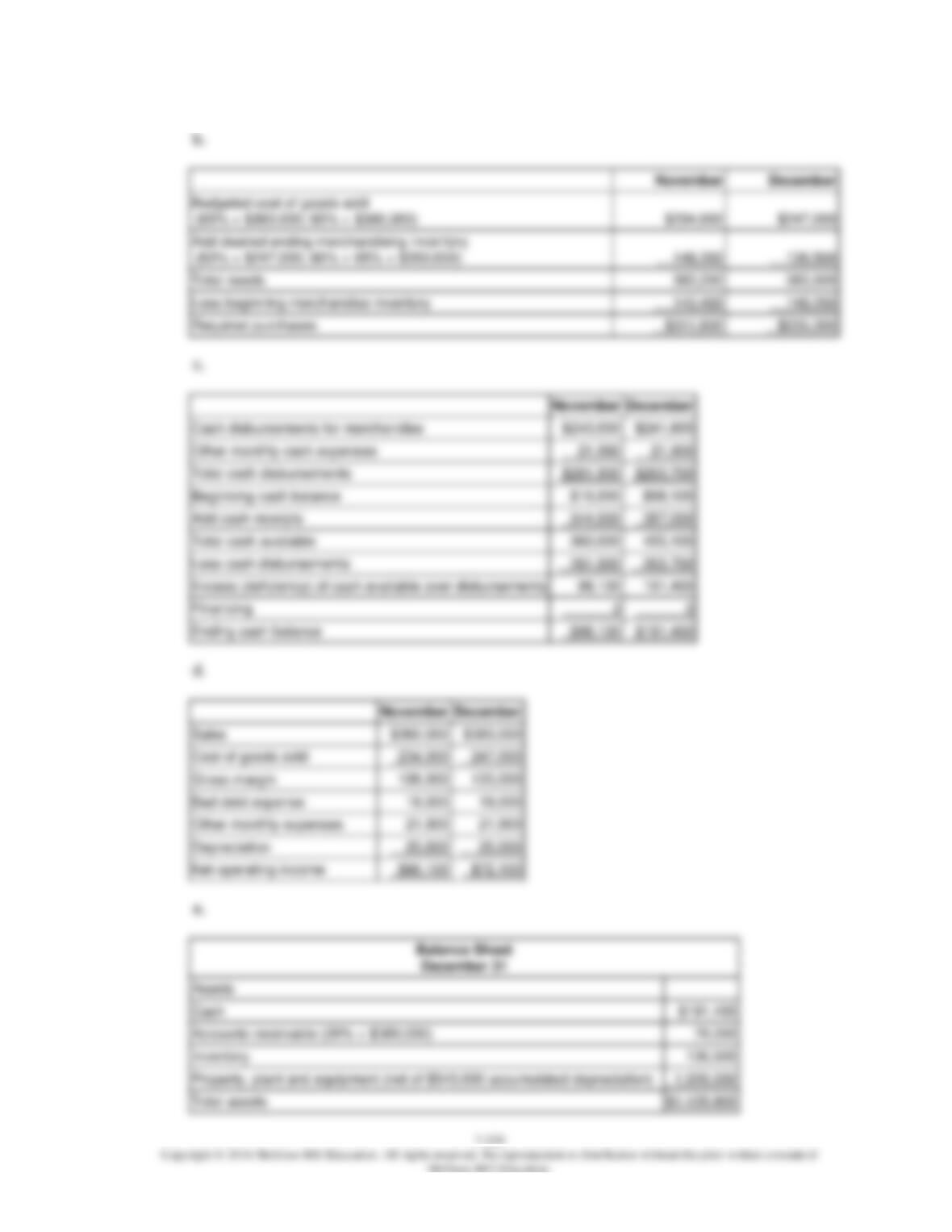

152.

Carter Lumber sells lumber and general building supplies to building contractors in a medium-

sized town in Montana. Data regarding the store’s operations follow:

o Sales are budgeted at $380,000 for November, $390,000 for December, and $400,000 for

January.

o Collections are expected to be 70% in the month of sale, 27% in the month following the

sale, and 3% uncollectible.

o The cost of goods sold is 65% of sales.

o The company desires to have an ending merchandise inventory equal to 80% of the

following month’s cost of goods sold. Payment for merchandise is made in the month following

the purchase.

o Other monthly expenses to be paid in cash are $22,000.

o Monthly depreciation is $20,000.

o Ignore taxes.

Balance Sheet

October 31

Assets

Cash

$13,000

Accounts receivable, net of allowance for uncollectible accounts

77,000

Inventory

197,600

Property, plant and equipment, net of $502,000 accumulated depreciation

992,000

Total assets

$1,279,600

Liabilities and Stockholders’ Equity

Accounts payable

$240,000

Common stock

780,000

Retained earnings

259,600

Total liabilities and stockholders’ equity

$1,279,600

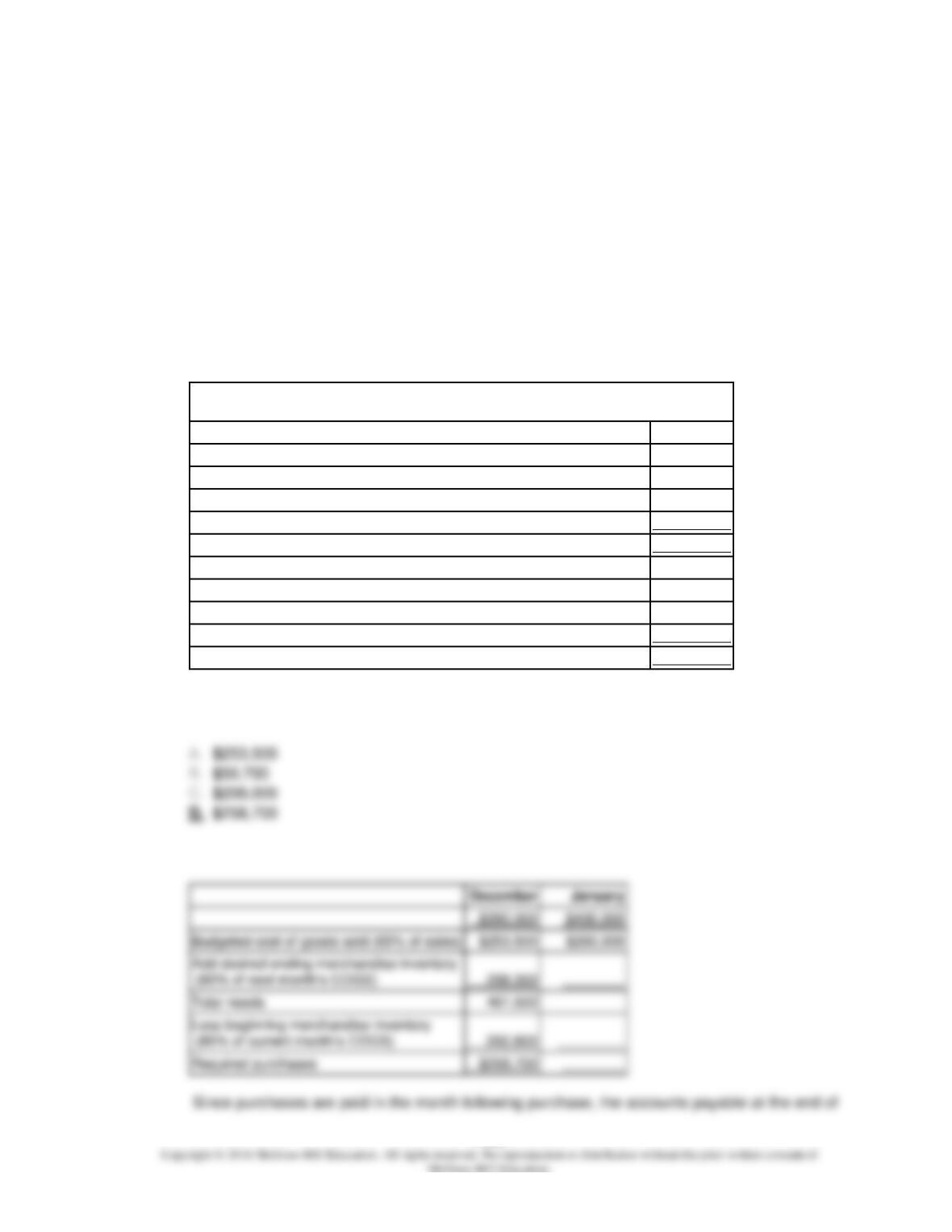

Budgeted cost of goods sold (65% of sales)

Total needs

Required purchases

$258,700

Accounts payable at the end of December would be:

7-211

7-212

153.

Carter Lumber sells lumber and general building supplies to building contractors in a medium-

sized town in Montana. Data regarding the store’s operations follow:

o Sales are budgeted at $380,000 for November, $390,000 for December, and $400,000 for

January.

o Collections are expected to be 70% in the month of sale, 27% in the month following the

sale, and 3% uncollectible.

o The cost of goods sold is 65% of sales.

o The company desires to have an ending merchandise inventory equal to 80% of the

following month’s cost of goods sold. Payment for merchandise is made in the month following

the purchase.

o Other monthly expenses to be paid in cash are $22,000.

o Monthly depreciation is $20,000.

o Ignore taxes.

Balance Sheet

October 31

Assets

Cash

$13,000

Accounts receivable, net of allowance for uncollectible accounts

77,000

Inventory

197,600

Property, plant and equipment, net of $502,000 accumulated depreciation

992,000

Total assets

$1,279,600

Liabilities and Stockholders’ Equity

Accounts payable

$240,000

Common stock

780,000

Retained earnings

259,600

Total liabilities and stockholders’ equity

$1,279,600

Sales

Cost of goods sold

Gross margin

Bad debt expense

Other monthly expenses

Depreciation

Net income

Retained earnings at the end of December would be:

7-213

Essay Questions

7-214

154.

Caprice Corporation is a wholesaler of industrial goods. Data regarding the store’s operations

follow:

o Sales are budgeted at $350,000 for November, $320,000 for December, and $300,000 for

January.

o Collections are expected to be 80% in the month of sale, 16% in the month following the

sale, and 4% uncollectible.

o The cost of goods sold is 70% of sales.

o The company desires an ending merchandise inventory equal to 60% of the cost of goods

sold in the following month. Payment for merchandise is made in the month following the

purchase.

o The November beginning balance in the accounts receivable account is $78,000.

o The November beginning balance in the accounts payable account is $254,000.

Required:

a. Prepare a Schedule of Expected Cash Collections for November and December.

b. Prepare a Merchandise Purchases Budget for November and December.

7-215

155.

Clay Corporation has projected sales and production in units for the second quarter of the

coming year as follows:

April

May

June

Sales

50,000

40,000

60,000

Production

60,000

50,000

50,000

Cash-related production costs are budgeted at $5 per unit produced. Of these production

costs, 40% are paid in the month in which they are incurred and the balance in the following

month. Selling and administrative expenses will amount to $100,000 per month. The accounts

payable balance on March 31 totals $190,000, which will be paid in April.

All units are sold on account for $14 each. Cash collections from sales are budgeted at 60%

in the month of sale, 30% in the month following the month of sale, and the remaining 10% in

the second month following the month of sale. Accounts receivable on April 1 totaled $500,000

($90,000 from February’s sales and $410,000 from March’s sales).

Required:

a. Prepare a schedule for each month showing budgeted cash disbursements for Clay

Corporation.

b. Prepare a schedule for each month showing budgeted cash receipts for Clay Corporation.

a.

$300,000

$250,000

$250,000

7-216

7-217

156.

Mate Boomerang Corporation manufactures and sells plastic boomerangs. Expected

boomerang sales (in units) for the upcoming months are as follows:

July

Aug.

Sept.

Oct.

Nov.

Dec.

Budgeted

unit sales

12,000

15,000

10,000

8,000

7,000

11,000

Mate likes to maintain a finished goods inventory equal to 10% of the next month’s estimated

sales. Seven ounces of plastic resin are needed to produce every boomerang. Mate likes to

have enough plastic resin on hand at the end of the month to cover 25% of the next month’s

production requirements.

Required:

How many ounces of plastic resin should Mate plan on purchasing during the month of

October?

Production Budget:

7-218

7-219

157.

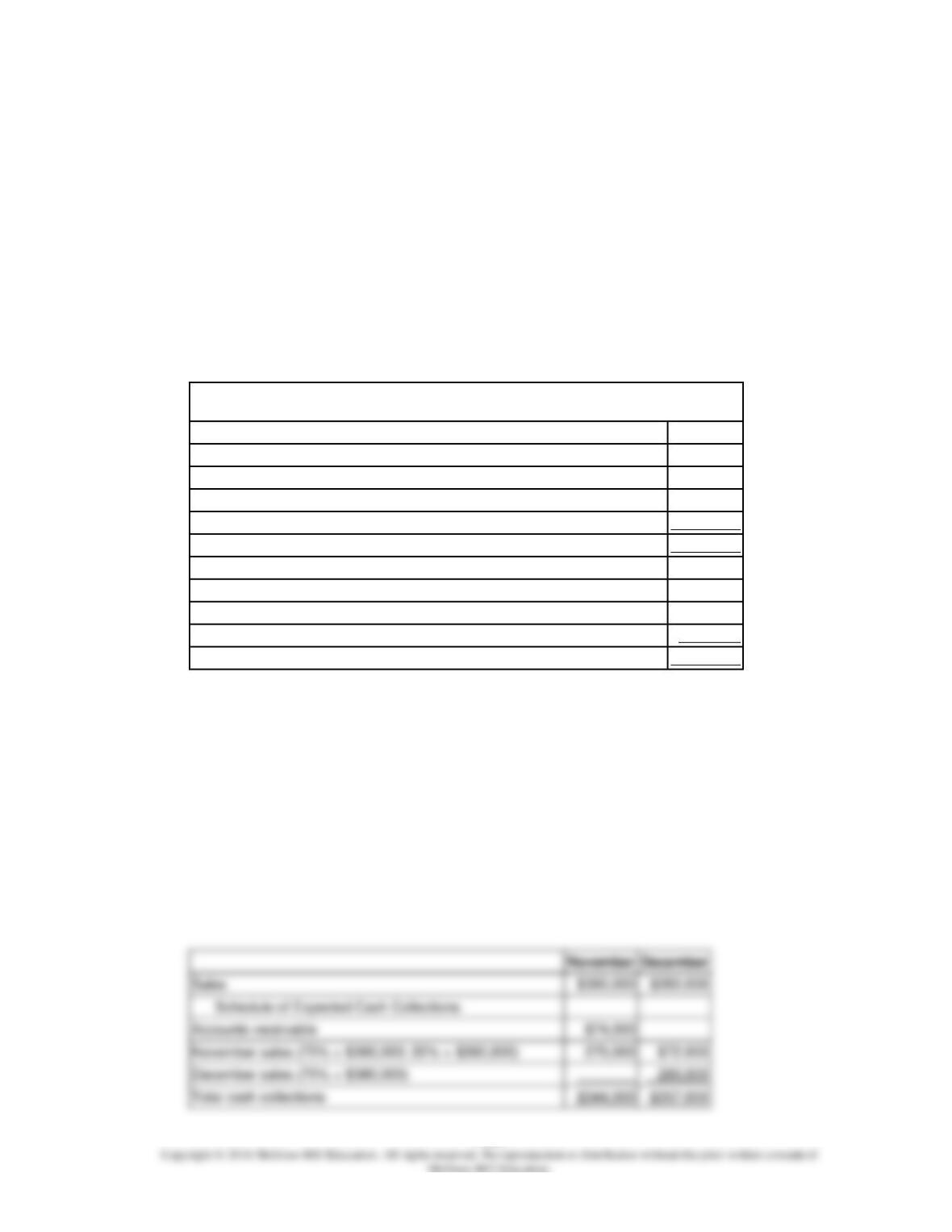

Weldon Industrial Gas Corporation supplies acetylene and other compressed gases to

industry. Data regarding the store’s operations follow:

o Sales are budgeted at $360,000 for November, $380,000 for December, and $350,000 for

January.

o Collections are expected to be 75% in the month of sale, 20% in the month following the

sale, and 5% uncollectible.

o The cost of goods sold is 65% of sales.

o The company desires an ending merchandise inventory equal to 60% of the cost of goods

sold in the following month.

o Payment for merchandise is made in the month following the purchase.

o Other monthly expenses to be paid in cash are $21,900.

o Monthly depreciation is $20,000.

o Ignore taxes.

Balance Sheet

October 31

Assets

Cash

$16,000

Accounts receivable (net of allowance for uncollectible accounts)

74,000

Merchandise inventory

140,400

Property, plant and equipment (net of $500,000 accumulated depreciation)

1,066,000

Total assets

$1,296,400

Liabilities and Stockholders’ Equity

Accounts payable

$240,000

Common stock

640,000

Retained earnings

416,400

Total liabilities and stockholders’ equity

$1,296,400

Sales

Schedule of Expected Cash Collections

Accounts receivable

November sales (75% × $360,000; 20% × $360,000)

Required:

a. Prepare a Schedule of Expected Cash Collections for November and December.

b. Prepare a Merchandise Purchases Budget for November and December.

c. Prepare Cash Budgets for November and December.

d. Prepare Budgeted Income Statements for November and December.

e. Prepare a Budgeted Balance Sheet for the end of December.

a.