Problem 3-18A (30 minutes)

1. The activity rates are computed as follows:

Activity Cost Pool

(a)

Estimated

Overhead

Cost

(b)

Expected

Activity

(a) ÷ (b)

Activity Rate

Labor related ………

$35,000

DLHs

per DLH

Material receipts ….

$10,450

receipts

per receipt

Relay assembly ……

relays

per relay

2. Overhead cost is assigned to the products as follows:

Product A

Activity Cost Pool

(a)

Activity

Rate

(b)

Actual

Activity

(a) × (b)

ABC Cost

Labor related …………

$5

per DLH

DLHs

$12,000

Material receipts …….

per receipt

400

receipts

Relay assembly ………

$7

per relay

170

relays

Total ……………………

$89,790

Product B

Activity Cost Pool

(a)

Activity

Rate

(b)

Actual

Activity

(a) × (b)

ABC Cost

Labor related …………

$5

per DLH

500

DLHs

$ 2,500

Material receipts …….

per receipt

208

receipts

General factory ………

$6

per MH

MHs

42,000

Total ……………………

$48,678

Problem 3-18A (continued)

Product C

Activity Cost Pool

(a)

Activity

Rate

(b)

Actual

Activity

(a) × (b)

ABC Cost

Labor related …………

$5

per DLH

3,500

DLHs

$17,500

Total ……………………

$72,962

Product D

Activity Cost Pool

Rate

Activity

ABC Cost

Labor related …………

$5

per DLH

DLHs

Material receipts …….

per receipt

receipts

Total ……………………

$85,020

(a)

Activity

(b)

Actual

(a) × (b)

3. The conventional system would assign 20% (8,000 MHs ÷ 40,000 MHs)

of all overhead costs to Product C. The ABC system would assign 50%

Communicating in Practice (30 minutes)

Date: Current Date

To: Maria Graham

From: Student’s Name

Subject: Overhead Allocation

I understand that you are thinking about purchasing a small manufacturing

company that assembles and packages its many products by hand. The

company currently uses direct labor hours to allocate overhead to its

products, but you plan to introduce automation. You have asked me to

comment on whether this technique should be continued.

Direct labor is an appropriate allocation base for overhead when overhead

Activity-based costing may be the best alternative. In activity-based

costing, overhead costs are allocated based on the activities required to

make the products and the resources that are consumed by these

activities. This technique is more complex than the approach the company

Teamwork In Action

Student answers will vary depending on the operations they observe at the

restaurant they visit and on how they define a unit and products. The

following are only suggestive of the answers that might be offered for a

fast food restaurant that sells hamburgers and beverages:

a.

Unit-level activities

and costs

Facility-level activities

Grilling a burger, assembling a hamburger,

making a milkshake, costs of ingredients,

Ethics Challenge (15 minutes)

Most people would probably feel that the most equitable way to divide the

dinner bill among a group of friends is for each person to pay for the cost

Case (150 minutes)

1. a. The predetermined overhead rate would be computed as follows:

b. The unit product cost per pound, using the company’s present costing

system, would be:

Mona Loa

Malaysian

Total unit product cost …………

2. a. Overhead rates by activity:

Activity Center

(a)

Estimated

Overhead

Costs

(b)

Expected

Activity

(a) ÷ (b)

Activity Rate

Purchasing ……….

$513,000

1,710 orders

$300 per order

Material handling .

$720,000

Blending …………..

$402,000

Packaging …………

$260,000

Case (continued)

Before we can determine the amount of overhead cost to assign to

the products we must first determine the activity for each of the

products in the six activity centers. The necessary computations

follow:

Number of purchase orders:

Mona Loa: 100,000 pounds ÷ 20,000 pounds per order = 5 orders

Malaysian: 2,000 pounds ÷ 500 pounds per order = 4 orders

Number of batches:

Malaysian: 2,000 pounds ÷ 500 pounds per batch = 4 batches

Number of setups:

Mona Loa: 10 batches × 3 setups per batch = 30 setups

Malaysian: 4 batches × 3 setups per batch = 12 setups

Roasting hours:

Malaysian: 1 hour × (2,000 pounds ÷ 100 pounds) = 20 hours

Blending hours:

Mona Loa: 0.5 hour × (100,000 pounds ÷ 100 pounds) = 500 hours

Malaysian: 0.5 hour × (2,000 pounds ÷ 100 pounds) = 10 hours

Packaging hours:

Malaysian: 0.1 hour × (2,000 pounds ÷ 100 pounds) = 2 hours

Case (continued)

Using the activity figures, manufacturing overhead costs can be

assigned to the two products as follows:

Mona Loa

Malaysian

Expected

Activity

Amount

Expected

Activity

Amount

Purchasing, at $300 per

order …………………….

5 orders

$ 1,500

4 orders

$1,200

Quality control, at $240

per batch ……………….

2,400

Roasting, at $10 per

Blending, at $12 per

blending hour ………….

6,000

Packaging, at $10 per

Total overhead cost ……

b. According to the activity-based costing system, the manufacturing

overhead cost per pound is:

Mona Loa

Malaysian

Total overhead cost assigned (above) (a) …

Number of pounds manufactured (b) ……….

Cost per pound (a) ÷ (b) ………………………

c. The unit product costs according to the activity-based costing system

are:

Mona Loa

Malaysian

Direct materials (given) ……….

$4.20

$3.20

Direct labor (given) …………….

Manufacturing overhead ………

Total unit product cost …………

$4.83

$7.15

Case (continued)

3. MEMO TO THE PRESIDENT: Analysis of CBI’s data shows that several

activities other than direct labor drive the company’s manufacturing

Case (continued)

ALTERNATIVE SOLUTION:

Most students will compute the manufacturing overhead cost per pound

Mona Loa

Malaysian

Total

Per Pound

(÷ 100,000)

Total

Per Pound

(÷ 2,000)

Purchasing ………..

$ 1,500

$0.015

$1,200

$0.600

Material handling ..

12,000

Quality control ……

Packaging …………

Total ………………..

$0.329

$7,300

$3.650

Note particularly how batch size impacts unit cost data. For example,

the cost to the company to process a purchase order is $300, regardless

of how many pounds of coffee are contained in the order. Twenty

Analytical Thinking (150 minutes)

1.

(a)

Estimated

Overhead

Costs

(b)

Expected Activity

(a) ÷ (b)

Activity Rate

Purchasing …………………….

$15,000

300

orders1

$50

per order

Material handling …………….

16,000

400

receipts2

$40

per receipt

Inspection ……………………..

18,000

600

inspection-hours

$30

per inspection-hour

Frame assembly ………………

12,000

assembly-hours

per assembly-hour

Machine related ………………

32,000

machine-hours4

per machine-hour

160 + 90 + 150 = 300

280 + 105 + 215 = 400

Total setup hours ……………………………………

4Standard: 10,000 units × 0.5 hours per unit …

Specialty: 2,500 units × 1.2 hours unit ………..

Total machine-hours ………………………………..

Analytical Thinking (continued)

Overhead cost charged to each product:

Standard

Specialty

Activity

Amount

Activity

Amount

Purchasing, at $50 per order:

Leather ……………………………..

50

$ 2,500

10

$ 500

Fabric ……………………………….

70

3,500

20

1,000

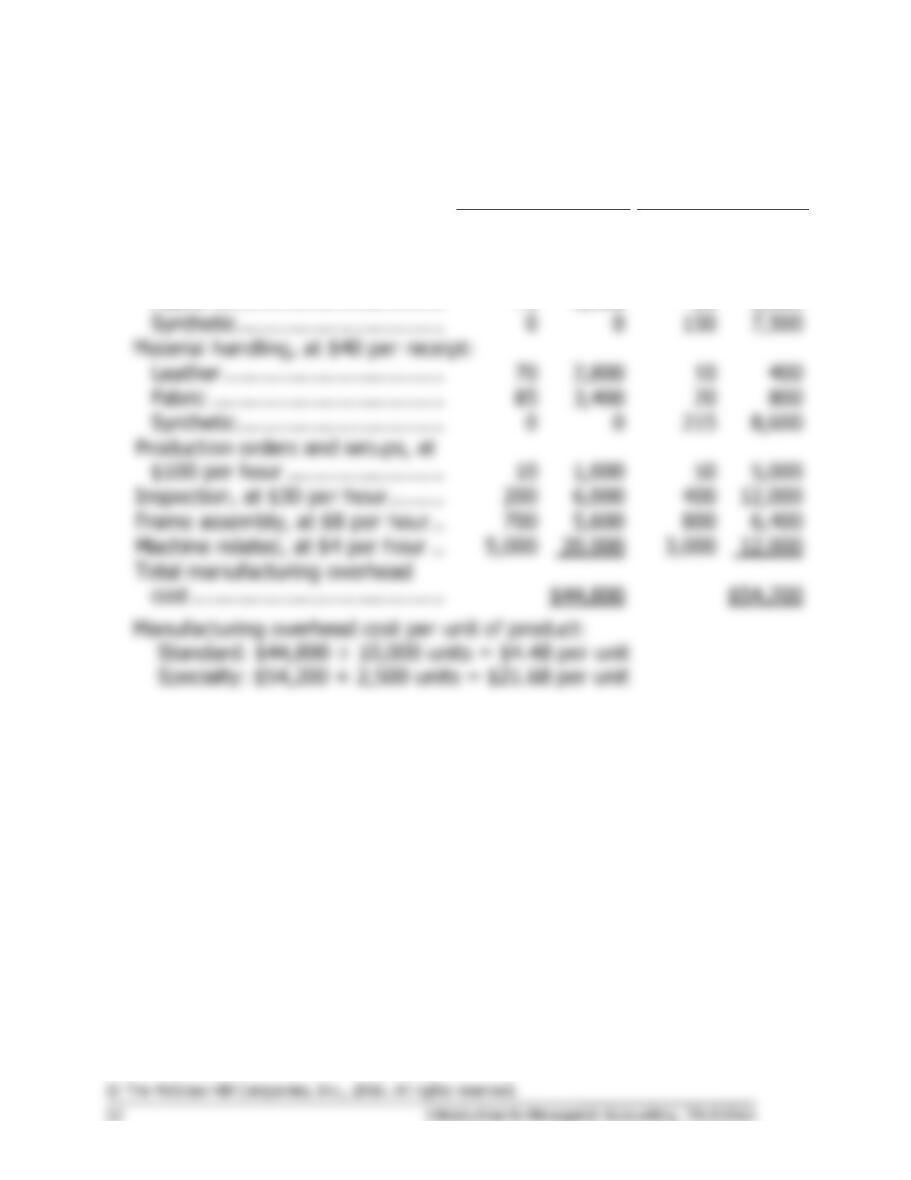

Synthetic …………………………...

7,500

Material handling, at $40 per receipt:

Synthetic …………………………...

8,600

10

1,000

50

5,000

Inspection, at $30 per hour………

Frame assembly, at $8 per hour ..

Machine related, at $4 per hour ..

5,000

20,000

12,000