Exercise 6-11 (20 minutes)

1.

Division

Total

Company

East

Central

West

Sales …………………………

$1,000,000

$250,000

$400,000

$350,000

Variable expenses ………..

390,000

130,000

120,000

140,000

Contribution margin ……..

120,000

Traceable fixed expenses .

535,000

160,000

200,000

175,000

$ 80,000

Net operating loss ………..

2.

Incremental sales ($350,000 × 20%) …….

$70,000

Incremental contribution margin …………..

$42,000

Less incremental advertising expense …….

Incremental net operating income …………

Contribution margin ratio

Exercise 6-12 (20 minutes)

1.

Sales (35,000 units × $25 per unit) …………….

$875,000

Variable expenses:

Variable cost of goods sold

(35,000 units × $12 per unit*) ………………

$420,000

Variable selling and administrative expenses

Contribution margin …………………………………

Fixed expenses:

Net operating income …………………………..….

*

Direct materials ………………………..

Direct labor ……………………………..

Variable manufacturing overhead ….

Total variable manufacturing cost ….

2. The difference in net operating income can be explained by the $20,000

in fixed manufacturing overhead deferred in inventory under the

absorption costing method:

Units in ending inventory = Units in beginning inventory + Units

Variable costing net operating income ………………….

$15,000

Absorption costing net operating income ………………

$35,000

Exercise 6-13 (20 minutes)

1. The company is using variable costing. The computations are:

Variable

Costing

Absorption

Costing

Direct materials ………………………

$ 9

$ 9

Unit product cost …………………….

2. a. No, $72,000 is not the correct figure to use because variable costing

is not generally accepted for external reporting purposes or for tax

purposes.

b. The Finished Goods inventory account should be stated at $90,000,

Exercise 6-14 (30 minutes)

1. Under variable costing, only the variable manufacturing costs are

included in product costs.

Direct materials……………………….

$ 50

Direct labor…………………………….

Variable manufacturing overhead ..

Variable costing unit product cost ..

2. The variable costing income statement appears below:

Sales …………………………………………………..

$3,990,000

Variable expenses:

Fixed expenses:

Net operating loss ………………………………….

3. The break-even point in units sold can be computed using the

contribution margin per unit as follows:

Selling price per unit …………..

$210

Variable cost per unit ………….

Contribution margin per unit ..

Exercise 6-15 (20 minutes)

1. Under absorption costing, all manufacturing costs (variable and fixed)

are included in product costs.

Variable manufacturing overhead ……………….

2. The absorption costing income statement appears below:

Sales (19,000 units × $210 per unit) ………………….

$3,990,000

Cost of goods sold (19,000 units × $185 per unit) …

3,515,000

Net operating income …………………………..…………

Exercise 6-16 (20 minutes)

1. The companywide break-even point is computed as follows:

The break-even point for the Chicago office is computed as follows:

Exercise 6-16 (continued)

The break-even point for the Minneapolis office is computed as follows:

2. $75,000 × 40% CM ratio = $30,000 increased contribution margin in

Minneapolis. Because the fixed costs in the office and in the company as

Exercise 6-16 (continued)

3. a. The segmented income statement follows:

Segments

Total Company

Chicago

Minneapolis

Amount

%

Amount

%

Amount

%

Sales ……………………..

$500,000

100.0

$200,000

100

$300,000

100

Variable expenses …….

b. The segment margin ratio rises and falls as sales rise and fall due to

the presence of fixed costs. The fixed costs are spread over a larger

base as sales increase.

Exercise 6-17 (15 minutes)

1. The company should focus its campaign on the Dental market. The

computations are:

Medical

Dental

Increased sales ………………………………………

Market CM ratio ………………………………………

2. The $48,000 in traceable fixed expenses in the previous exercise is now

partly traceable and partly common. When we segment Minneapolis by

market, only $33,000 remains a traceable fixed expense. This amount

Problem 6-18A (45 minutes)

1. The break-even point in units sold can be computed using the

contribution margin per unit as follows:

2 a. Under variable costing, only the variable manufacturing costs are

included in product costs.

Problem 6-18A (continued)

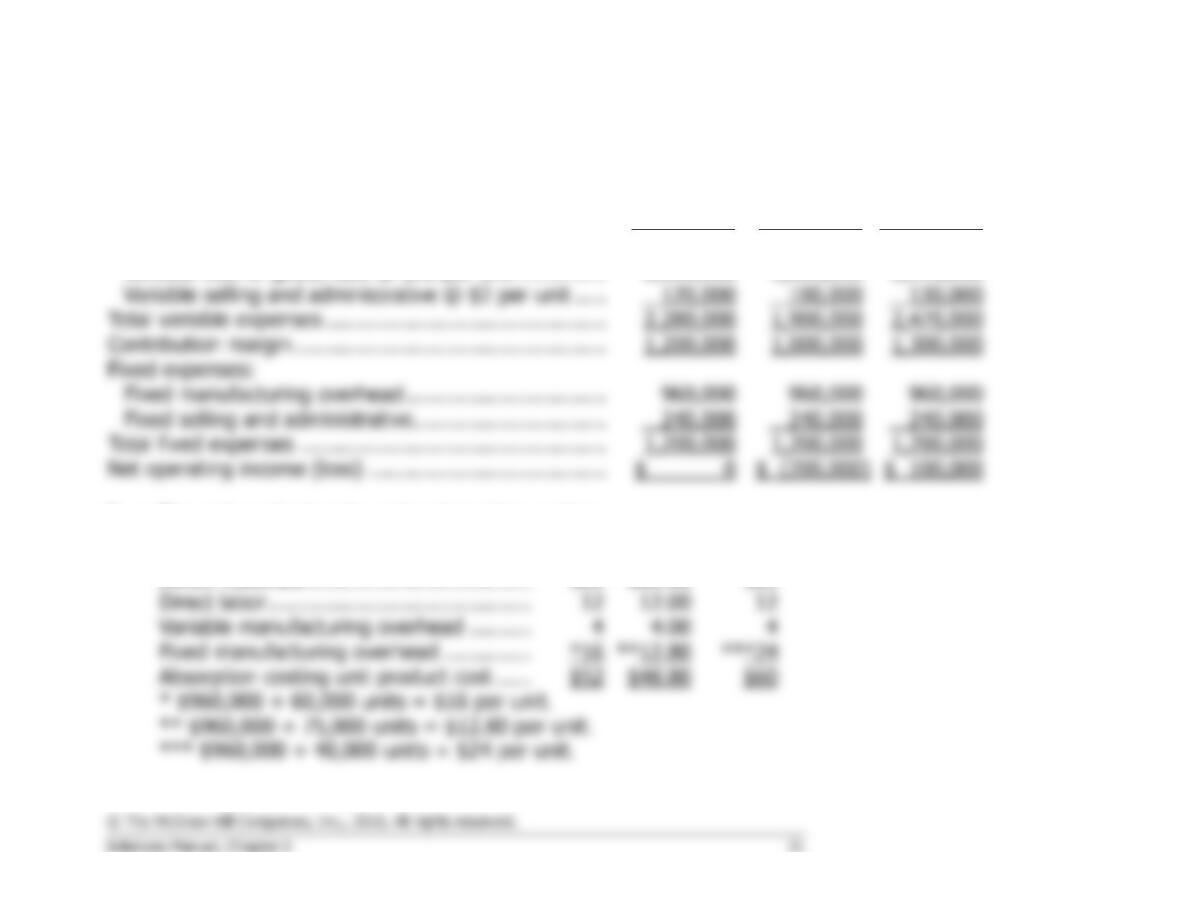

2 b. The variable costing income statements appear below:

Year 1

Year 2

Year 3

Sales ………………………………………………………………

$3,480,000

$2,900,000

$3,770,000

Variable expenses:

Variable cost of goods sold @ $36 per unit …………..

2,160,000

1,800,000

2,340,000

Total variable expenses ………………………………………

2,280,000

Contribution margin …………………………………………..

Fixed expenses:

Fixed manufacturing overhead …………………………..

Total fixed expenses ………………………………………….

Net operating income (loss) ………………………………..

3 a. The unit product costs under absorption costing:

Year 1

Year 2

Year 3

Direct materials ………………………………

$20

$20.00

$20

Direct labor ……………………………………

Variable manufacturing overhead ……….

Fixed manufacturing overhead …………..

Absorption costing unit product cost ……

* $960,000 ÷ 60,000 units = $16 per unit.

Problem 6-18A (continued)

3 b. The absorption costing income statements appears below:

Year 1

Year 2

Year 3

Sales ……………………………………………..

$3,480,000

$2,900,000

$3,770,000

Cost of goods sold…………………………….

3,120,000

2,440,000

3,620,000

Gross margin …………………………………..

Selling and administrative expenses ……..

Net operating income (loss) ………………..

4.

Year 1

Year 2

Year 3

Units sold …………………………………………………..

60,000

50,000

65,000

Break-even point in units ……………………………….

60,000

60,000

60,000

Units above (below) break-even point ………………

Variable costing net operating income (loss) ………

Absorption costing net operating income (loss) …..

$ 120,000

Problem 6-19A (30 minutes)

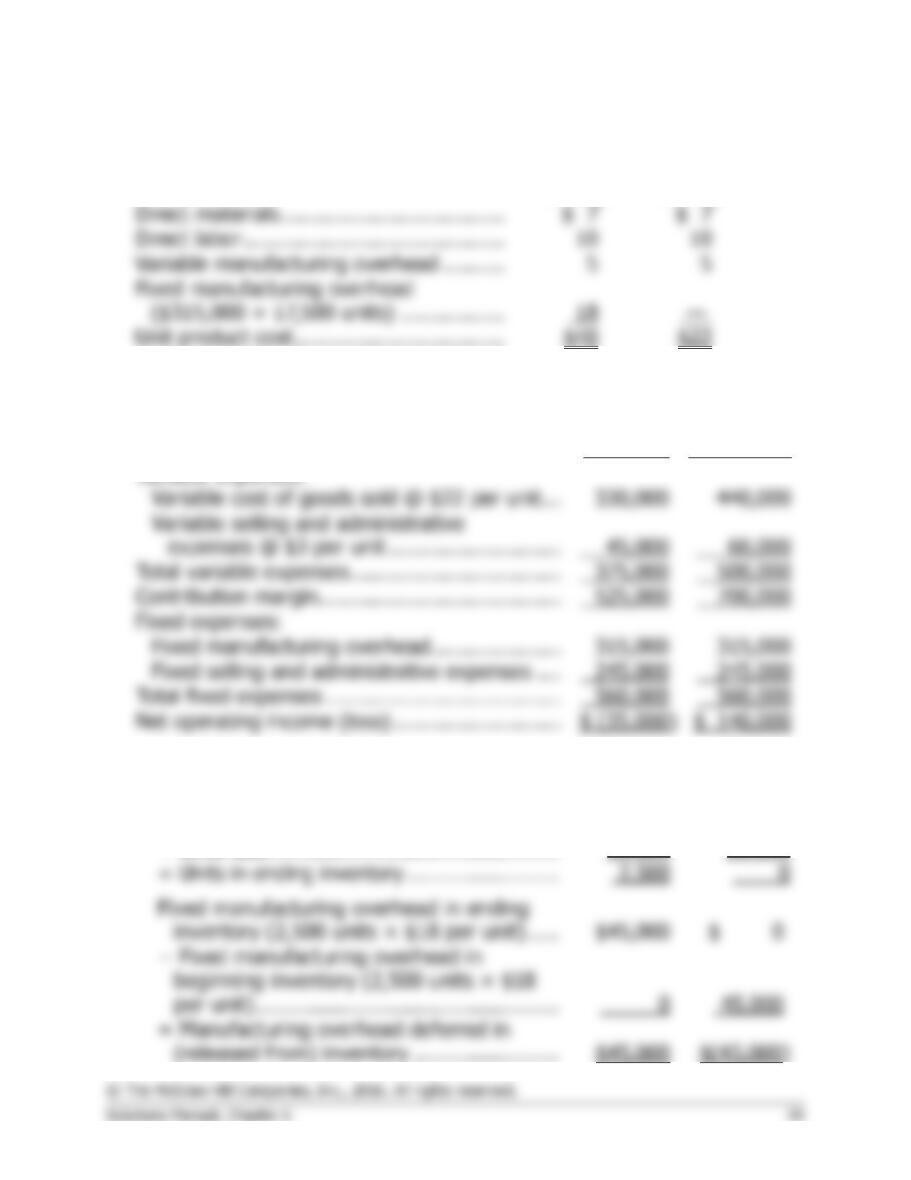

1. The unit product cost under variable costing is computed as follows:

Direct materials ……………………..

$ 4

Direct labor …………………………..

With this figure, the variable costing income statements can be

prepared:

Year 1

Year 2

Unit sales ……………………………………………

40,000 units

50,000 units

Sales …………………………………………………

$1,000,000

$1,250,000

Variable expenses:

80,000

Total variable expenses ………………………….

560,000

130,000

Total fixed expenses ……………………………..

400,000

Net operating income …………………………...

$ 40,000

$ 150,000

Problem 6-19A (continued)

2. The reconciliation of absorption and variable costing follows:

Year 1

Year 2

Units in beginning inventory ……………………

0

5,000

+ Units produced …………………………..…….

45,000

45,000

40,000

50,000

Year 1

Year 2

$30,000

Year 1

Year 2

Variable costing net operating income (loss)

$40,000

$150,000

30,000

Absorption costing net operating income …..

$70,000

$120,000

Problem 6-20A (45 minutes)

1. a. The unit product cost under absorption costing is:

Direct materials …………………………..…

$20

Direct labor …………………………………..

Variable manufacturing overhead ……….

Absorption costing unit product cost …..

$40

b. The absorption costing income statement is:

Sales (8,000 units × $75 per unit)……………………..

$600,000

Cost of goods sold (8,000 units × $40 per unit) ……

320,000

Gross margin ………………………………………………..

Net operating income ……………………………………..

$ 32,000

2. a. The unit product cost under variable costing is:

Direct materials ……………………….

$20

Direct labor …………………………....

8

Variable manufacturing overhead …

2

Variable costing unit product cost…

$30

b. The variable costing income statement is:

Sales (8,000 units × $75 per unit) ………………

$600,000

Variable expenses:

Contribution margin …………………………………

Fixed expenses:

Net operating income ……………………………….

Problem 6-20A (continued)

3. The difference in the ending inventory relates to a difference in the

handling of fixed manufacturing overhead costs. Under variable costing,

these costs have been expensed in full as period costs. Under

absorption costing, these costs have been added to units of product at

the rate of $10 per unit ($100,000 ÷ 10,000 units produced = $10 per

Problem 6-21A (30 minutes)

1.

Sales Territory

Total Company

Northern

Southern

Amount

%

Amount

%

Amount

%

Sales ………………………………………..

$750,000

100.0

$300,000

100

$450,000

100

Variable expenses ………………………..

336,000

44.8

156,000

52

180,000

40

Territorial segment margin …………….

186,000

24.8

$ 24,000

$162,000

Common fixed expenses* ……………..

150,000

20.0

Net operating income …………………..

$ 36,000

4.8

*378,000 – $228,000 = $150,000

Product Line

Northern Territory

Paks

Tibs

Amount

%

Amount

%

Amount

%

Sales ……………………………………….

$300,000

100.0

$50,000

100

$250,000

100

Variable expenses ……………………….

156,000

52.0

11,000

22

145,000

58

Contribution margin …………………….

48.0

Traceable fixed expenses ……………..

70,000

23.3

60

Sales territory segment margin ……..

$ 24,000

8.0

*$120,000 – $70,000 = $50,000

Problem 6-21A (continued)

2. Two insights should be brought to the attention of management. First,

compared to the Southern territory, the Northern territory has a low

3. Again, two insights should be brought to the attention of management.

First, the Northern territory has a poor sales mix. Note that the territory

sells very little of the Paks product, which has a high contribution margin

Problem 6-22A (45 minutes)

1.

a. and b.

Absorption

Costing

Variable

Costing

Direct materials ………………………………

Direct labor ……………………………………

Variable manufacturing overhead ……….

Unit product cost …………………………….

2.

July

August

Unit sales ………………………………………………

15,000

20,000

Sales ……………………………………………………

$900,000

$1,200,000

Variable expenses:

Total variable expenses …………………………….

500,000

Contribution margin…………………………………

Fixed expenses:

Fixed manufacturing overhead …………………

Fixed selling and administrative expenses ….

245,000

Total fixed expenses ………………………………..

560,000

Net operating income (loss) ………………………

$ 140,000

3.

July

August

Units in beginning inventory ……………………

0

2,500

+ Units produced ………………………………….

17,500

17,500

− Units sold…………………………………………

15,000

20,000

Problem 6-22A (continued)

July

August

Variable costing net operating income

4. As shown in the reconciliation in part (3) above, $45,000 of fixed

manufacturing overhead cost was deferred in inventory under

absorption costing at the end of July because $18 of fixed

manufacturing overhead cost “attached” to each of the 2,500 unsold