Analytical Thinking (continued)

2. a. No, the cookbook line should not be eliminated. The cookbook is

b.

Cook–

Travel

Handy

It is probably unwise to focus all available resources on promoting the

travel guide. The company is already spending more on the

promotion of this product than on the other two products combined.

Case (75 minutes)

1. See the segmented statement on the second following page.

Supporting computations for the statement are given below:

Sales:

Membership dues (20,000 × $100) ………………………

$2,000,000

Non-member magazine subscriptions (2,500 × $30) ..

$ 75,000

Total revenue ………………………………………………….

$ 400,000

Assigned to Magazine Subscriptions Division

Salary and personnel costs:

Salaries

Personnel Costs

(25% of Salaries)

Membership Division ………………….

$210,000

$ 52,500

Corporate staff ………………………….

$920,000

Case (continued)

Some may argue that, except for the $50,000 in rental cost directly

Occupancy costs ($230,000 allocated + $50,000 direct to the Books

and Reports Division = $280,000):

Allocated to:

Membership Division

($230,000 × 0.2) …………………………………….

$ 46,000

Magazine Subscriptions Division

Books and Reports Division

Continuing Education Division

$280,000

Printing and paper costs ………………………………..

$320,000

Assigned to:

Magazine Subscriptions Division

(22,500 × $7) ………………………………………

$157,500

Books and Reports Division

(28,000 × $4) ………………………………………

112,000

269,500

Postage and shipping costs …………………………….

Books and Reports Division

(28,000 × $2) ………………………………………

$ 30,000

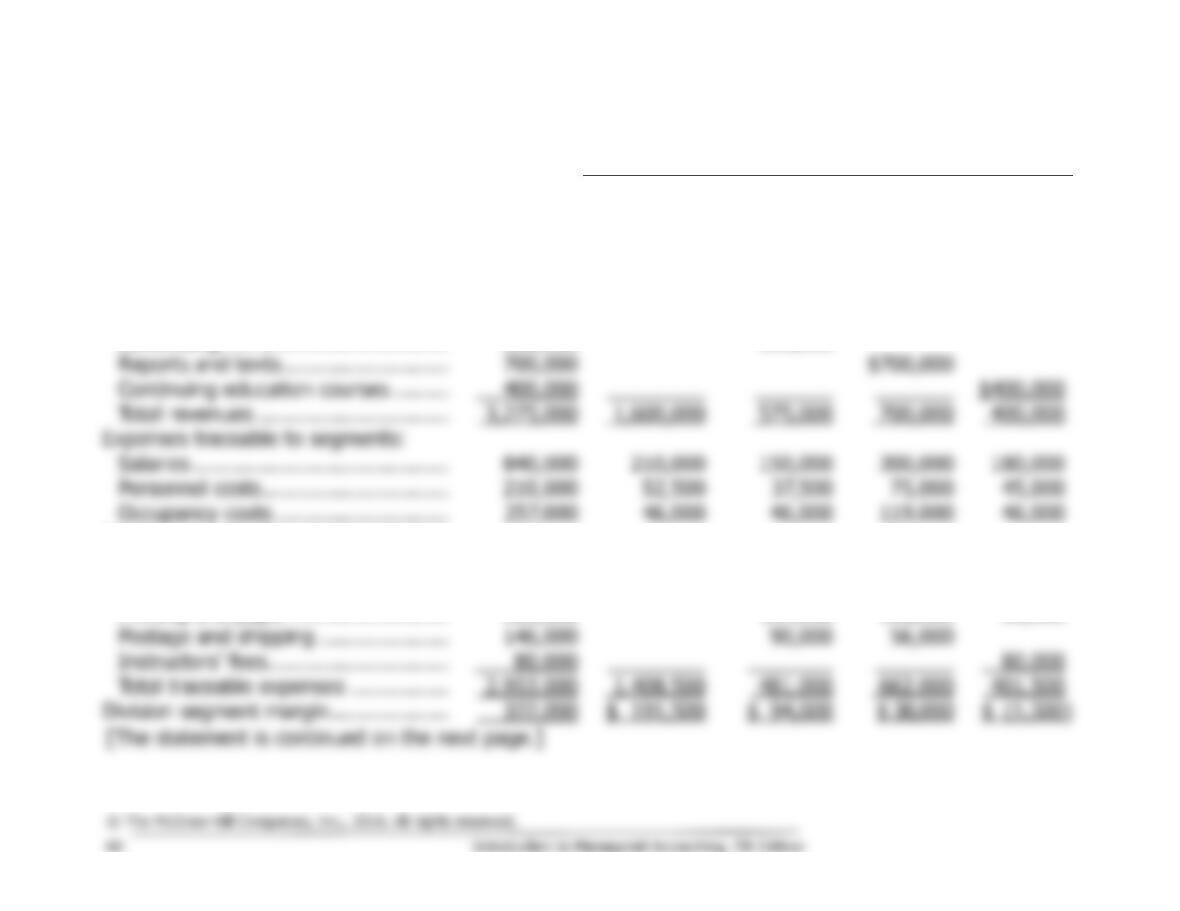

Case (continued)

Division

Association

Total

Membership

Magazine

Subscriptions

Books &

Reports

Continuing

Education

Sales:

Membership dues ………………………

$2,000,000

$1,600,000

$400,000

Non-member magazine

subscriptions ………………………….

75,000

75,000

Advertising ………………………………

100,000

100,000

Reports and texts ………………………

700,000

Continuing education courses ………

$400,000

575,000

Personnel costs …………………………

210,000

52,500

45,000

Occupancy costs ……………………….

257,000

46,000

46,000

119,000

46,000

Reimbursement of member costs to

local chapters …………………………..

600,000

600,000

Other membership services …………

500,000

500,000

Printing and paper …………………….

320,000

157,500

112,000

50,500

Postage and shipping …………………

146,000

90,000

481,000

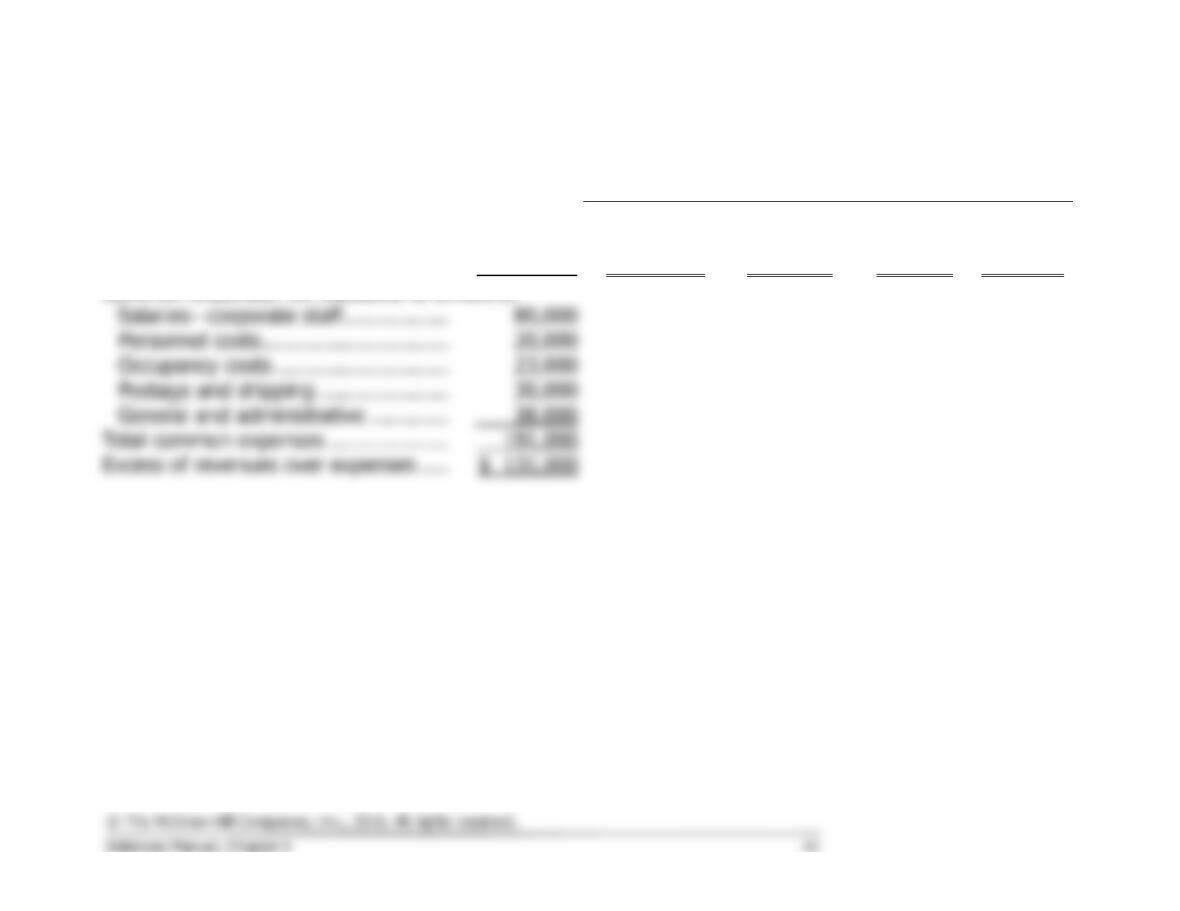

Case (continued)

[Continuation of the segmented income statement.]

Division

Association

Total

Membership

Magazine

Subscriptions

Books &

Reports

Continuing

Education

Division segment margin ……………….

322,000

$ 191,500

$ 94,000

$ 38,000

$ (1,500)

Common expenses not traceable to divisions:

38,000

Total common expenses ………………..

191,000

Case (continued)

2. While we do not favor the allocation of common costs to segments, the

most common reason given for this practice is that segment managers

need to be aware of the fact that common costs do exist and that they

must be covered.

Arguments against allocation of all costs:

• Allocation bases will need to be chosen arbitrarily because no cause-

Chapter 6

Take Two Solutions

Exercise 6-1 (15 minutes)

1. Under absorption costing, all manufacturing costs (variable and fixed)

are included in product costs.

Direct labor …………………………………………………………

Variable manufacturing overhead …………………………….

Fixed manufacturing overhead ($60,000 ÷ 250 units) …..

Absorption costing unit product cost …………………………

$700

2. Under variable costing, only the variable manufacturing costs are

included in product costs.

Direct materials ……………………………………………………

$100

Variable costing unit product cost …………………………….

$460

Exercise 6-3 (20 minutes)

1.

Year 1

Year 2

Year 3

Beginning inventories ……….

200

140

180

Ending inventories ……………

140

180

220

Change in inventories ……….

(60)

40

40

Fixed manufacturing

Variable costing net

operating income …………..

$1,080,400

$1,032,400

$ 996,400

Absorption costing net

operating income …………..

$1,018,800

Add (deduct) fixed

2. Because absorption costing net operating income was greater than

variable costing net operating income in Year 4, inventories must have

Exercise 6-4 (10 minutes)

Total

Company

Weedban

Greengrow

Sales* ……………………………..

$321,000

$96,000

$225,000

Variable expenses** …………..

195,900

38,400

157,500

Contribution margin ……………

125,100

57,600

67,500

Traceable fixed expenses ……..

Product line segment margin ..

Net operating income ………….

Exercise 6-8 (10 minutes)

Sales were below the company’s break–even sales and yet the company

earned a profit. The apparent contradiction is explained by the fact that the

CVP analysis is based on variable costing, whereas the income reported to

Exercise 6-9 (30 minutes)

1 a. Under variable costing, only the variable manufacturing costs are

included in product costs.

Year 1

Year 2

Direct materials ………………………………

$25

$25

Direct labor ……………………………………

Variable manufacturing overhead ……….

Variable costing unit product cost ……….

1 b.

Year 1

Year 2

Sales …………………………………………………

$2,400,000

$3,000,000

Variable expenses:

Variable cost of goods sold @ $45 per unit

1,800,000

2,250,000

Total variable expenses ………………………….

Contribution margin ………………………………

Fixed expenses:

Total fixed expenses ……………………………..

Net operating income (loss) ……………………

2 a. The unit product costs under absorption costing:

Year 1

Year 2

Direct materials ………………………………

$25

$25

Direct labor ……………………………………

Variable manufacturing overhead ……….

Fixed manufacturing overhead …………..

Absorption costing unit product cost ……

$53

$55

* $400,000 ÷ 50,000 units = $8 per unit.

Exercise 6-9 (continued)

2 b. The absorption costing income statements appears below:

Year 1

Year 2

Sales ……………………………………………..

$2,400,000

$3,000,000

Cost of goods sold…………………………….

Gross margin …………………………………..

Selling and administrative expenses ……..

Net operating income ………………………..

3. The net operating incomes are reconciled as follows:

Year 1

Year 2

Units in beginning inventory ……………………

0

10,000

+ Units produced …………………………………

50,000

40,000

= Units in ending inventory …………………….

Year 1

Year 2

Year 1

Year 2

Variable costing net operating income ……..

$ 40,000

$170,000

Deduct: Fixed manufacturing overhead cost

released from inventory under absorption

Add: Fixed manufacturing overhead cost

deferred in inventory under absorption

Exercise 6-11 (20 minutes)

1.

Division

Total

Company

East

Central

West

Sales …………………………

$1,000,000

$250,000

$400,000

$350,000

Variable expenses ………..

430,000

130,000

160,000

140,000

Contribution margin ……..

Traceable fixed expenses .

535,000

160,000

200,000

175,000

$ 40,000

Net operating loss ………..

2.

Incremental sales ($350,000 × 20%) …….

$70,000

Incremental contribution margin …………..

$42,000

Less incremental advertising expense …….

Incremental net operating income …………

Contribution margin ratio

Exercise 6-13 (20 minutes)

1. The company is using variable costing. The computations are:

Variable

Costing

Absorption

Costing

Direct materials ………………………

Unit product cost …………………….

2. a. No, $72,000 is not the correct figure to use because variable costing

is not generally accepted for external reporting purposes or for tax

purposes.

b. The Finished Goods inventory account should be stated at $87,000,

Exercise 6-14 (30 minutes)

1. Under variable costing, only the variable manufacturing costs are

included in product costs.

Direct materials……………………….

$ 50

Direct labor…………………………….

Variable manufacturing overhead ..

Variable costing unit product cost ..

2. The variable costing income statement appears below:

Sales …………………………………………………..

$3,990,000

Variable expenses:

Fixed expenses:

Fixed manufacturing overhead ………………..

Fixed selling and administrative expenses ….

Net operating loss …………………………..……..

3. The break-even point in units sold can be computed using the

contribution margin per unit as follows:

Selling price per unit …………..

$210

Variable cost per unit ………….

Contribution margin per unit ..

Exercise 6-15 (20 minutes)

1. Under absorption costing, all manufacturing costs (variable and fixed)

are included in product costs.

Variable manufacturing overhead ……………….

2. The absorption costing income statement appears below:

Sales (19,000 units × $210 per unit) ………………….

$3,990,000

Cost of goods sold (19,000 units × $187 per unit) …

Net operating loss ………………………………………….