Chapter 9

Performance Measurement in Decentralized

Organizations

Solutions to Questions

9-1 In a decentralized organization,

decision-making authority isn’t confined to a few

9-2 The benefits of decentralization include:

(1) by delegating day-to–day problem solving to

lower-level managers, top management can

concentrate on bigger issues such as overall

strategy; (2) empowering lower-level managers

9-3 The manager of a cost center has

control over cost, but not revenue or the use of

9-4 Margin is the ratio of net operating

income to total sales. Turnover is the ratio of

9-5 Residual income is the net operating

income an investment center earns above the

company’s minimum required rate of return on

operating assets.

profitable investment opportunity whose rate of

return exceeds the company’s required rate of

return but whose rate of return is less than the

investment center’s current ROI. The residual

income approach overcomes this problem

9-8 An MCE of less than 1 means that the

production process includes non-value-added

9-9 A company’s balanced scorecard should

be derived from and support its strategy.

9-10 The balanced scorecard is constructed

to support the company’s strategy, which is a

The Foundational 15

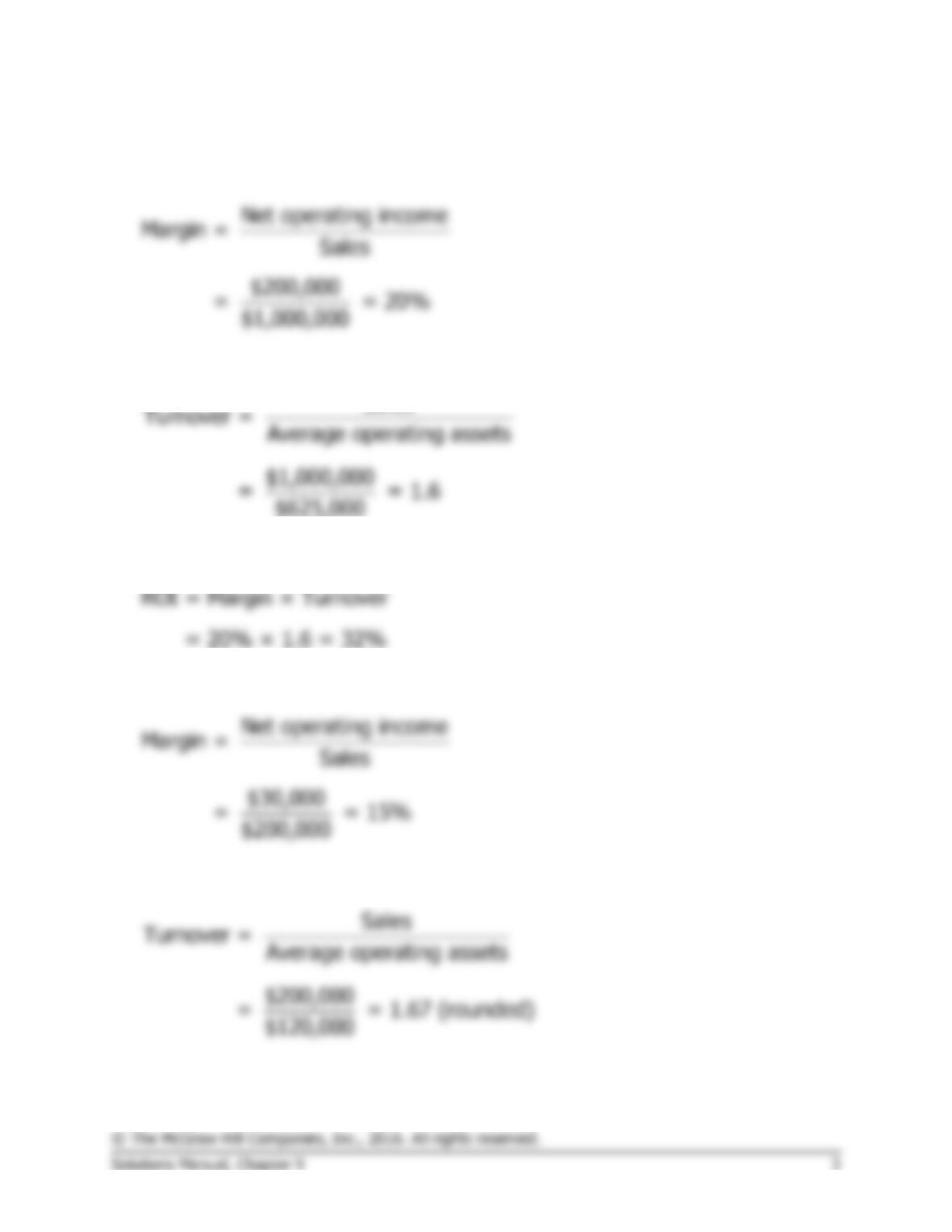

1. Last year’s margin is:

2. Last year’s turnover is:

Sales

3. Last year’s return on investment (ROI) is:

4. The margin for this year’s investment opportunity is:

5. The turnover for this year’s investment opportunity is:

The Foundational 15 (continued)

6. The ROI for this year’s investment opportunity is:

7., 8., and 9.

If the company pursues the investment opportunity, this year’s margin,

turnover, and ROI would be:

Sales

Turnover = Average operating assets

$1,000,000 + $200,000

= $625,000 + $120,000

$1

= ,200,000 = 1.61 (rounded)

$745,000

10. The CEO would not pursue the investment opportunity because it

lowers her ROI from 32% to 30.9%. The owners of the company

The Foundational 15 (continued)

11. Last year’s residual income is:

Average operating assets ………………….

$625,000

Net operating income ………………………

$200,000

Residual income …………………………..

$106,250

12. The residual income for this year’s investment opportunity is:

Average operating assets ………………….

$120,000

Net operating income ………………………

Residual income …………………………..

13. If the company pursues the investment opportunity, this year’s

residual income will be:

Average operating assets ………………….

$745,000

Net operating income ………………………

$230,000

Residual income …………………………..

$118,250

14. The CEO would pursue the investment opportunity because it would

raise her residual income by $12,000.

15. The CEO and the company would not want to pursue this investment

opportunity because it does not exceed the minimum required return:

Average operating assets ………………….

Net operating income ………………………

Residual income …………………………..

$ (8,000)

Exercise 9-1 (10 minutes)

1.

Net operating income

Margin = Sales

$600,000

= = 8%

$7,500,000

Exercise 9-2 (10 minutes)

Average operating assets ………………….

$2,800,000

Net operating income ……………………….

Exercise 9-3 (20 minutes)

=

9.0 days

2. Only process time is value-added time; therefore the manufacturing

cycle efficiency (MCE) is:

3. If the MCE is 30%, then 30% of the throughput time was spent in

value-added activities. Consequently, the other 70% of the throughput

time was spent in non-value-added activities.

Learning

and

Growth

+

+

Financial

Customer

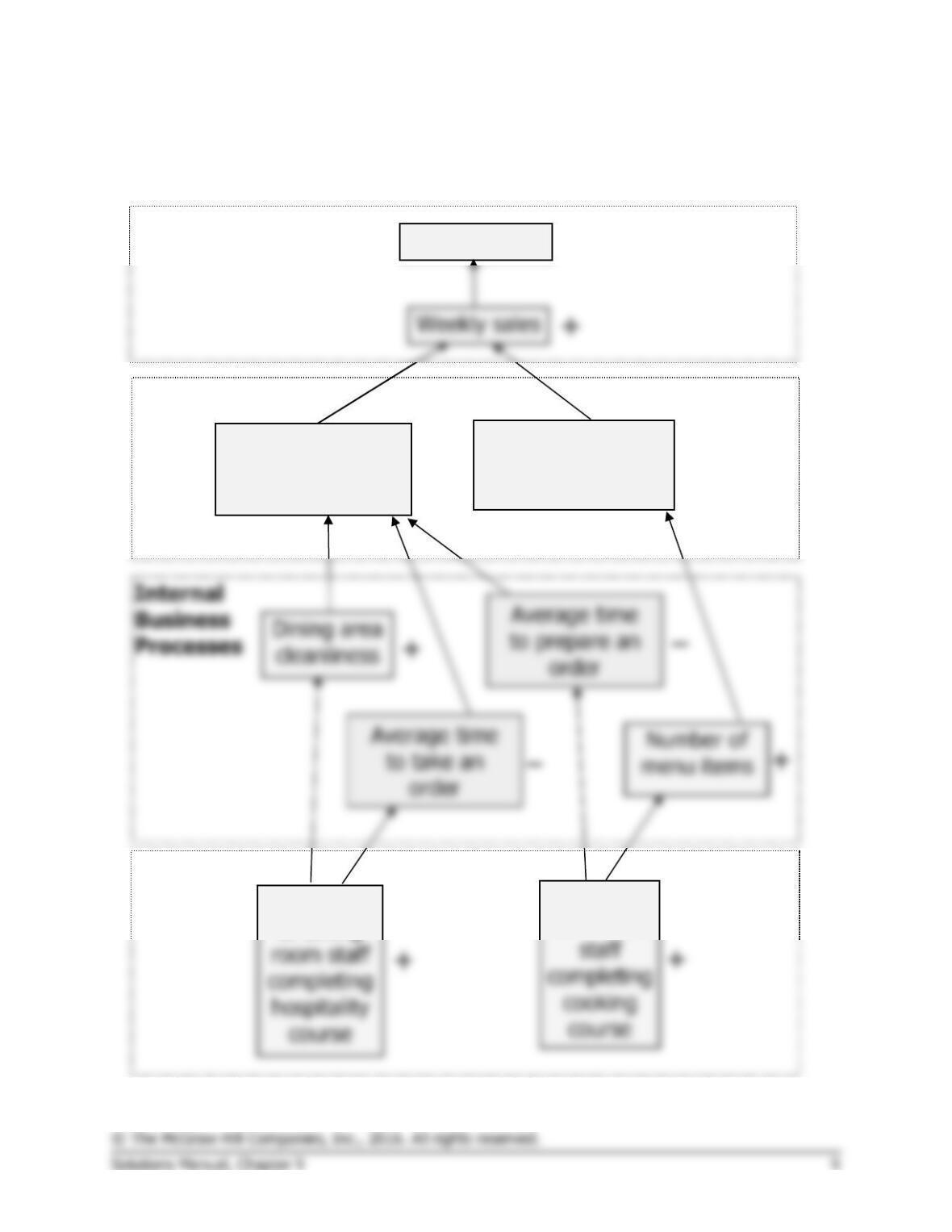

Exercise 9-4 (45 minutes)

1. Students’ answers may differ in some details from this solution.

+

+

+

Weekly profit

Percentage

of kitchen

+

Customer

satisfaction with

service

Customer

satisfaction with

menu choices

+

+

Percentage

of dining

Exercise 9-4 (continued)

2. The hypotheses underlying the balanced scorecard are indicated by the

arrows in the diagram. Reading from the bottom of the balanced

scorecard, the hypotheses are:

o If the percentage of dining room staff that complete the basic

hospitality course increases, then the average time to take an order

with service will increase.

o If the average time to take an order decreases, then customer

satisfaction with service will increase.

o If the average time to prepare an order decreases, then customer

satisfaction with service will increase.

Exercise 9-4 (continued)

3. Management will be able to tell if a hypothesis is false if an

improvement in a performance measure at the bottom of an arrow does

Exercise 9-5 (15 minutes)

Division

Alpha

Bravo

Charlie

Sales ……………………………..

$4,000,000

$11,500,000

*

$3,000,000

Net operating income ………..

$160,000

$920,000

*

$210,000

*

Average operating assets …..

$800,000

*

Margin …………………………..

Turnover ………………………..

Return on investment (ROI) .

Exercise 9-6 (20 minutes)

1. ROI computations:

Net operating income Sales

ROI = ×

2.

Osaka

Yokohama

Average operating assets (a) ………………….

$1,000,000

$4,000,000

Net operating income …………………………..

Residual income ………………………………….

3. No, the Yokohama Division is simply larger than the Osaka Division and

for this reason one would expect that it would have a greater amount of

Exercise 9-7 (45 minutes)

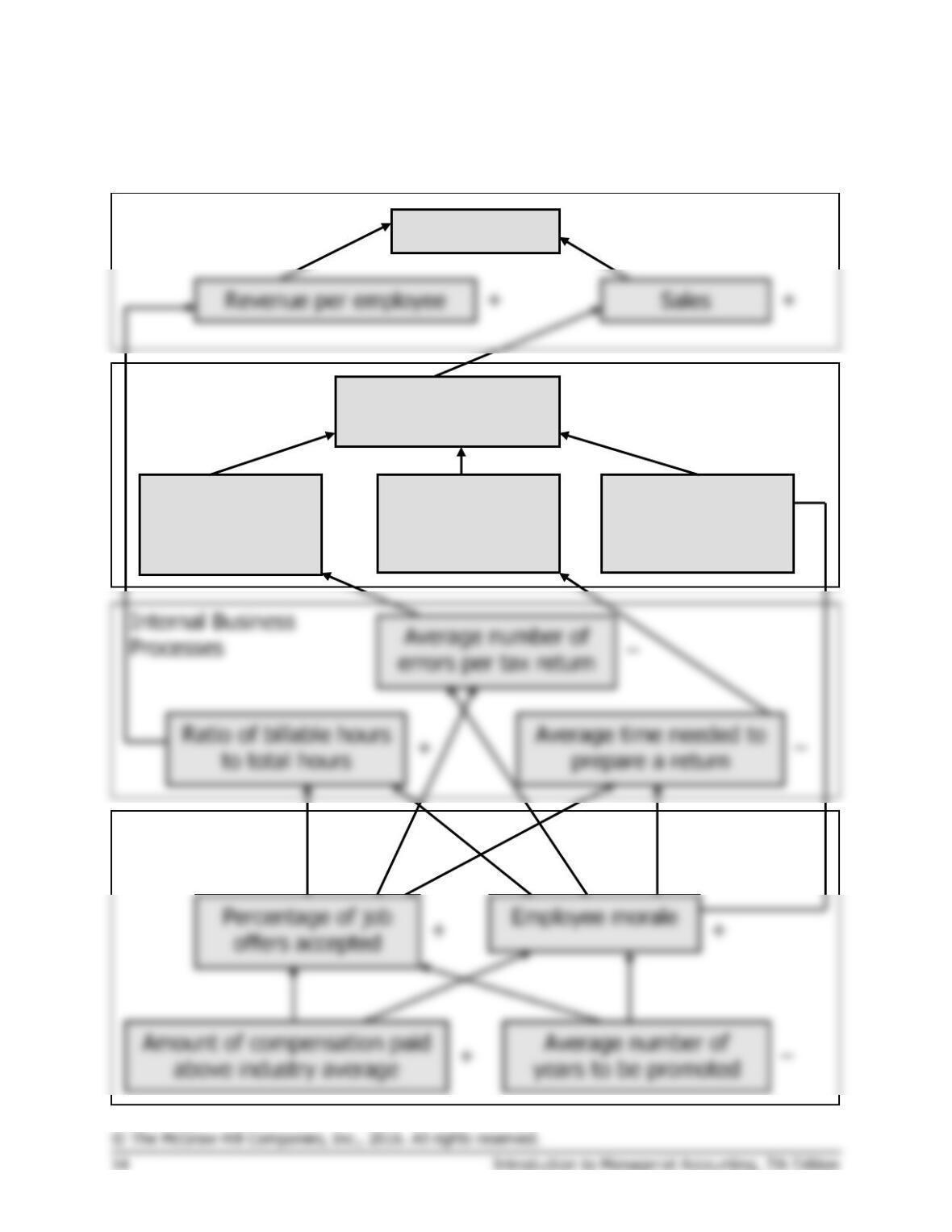

1. Students’ answers may differ in some details from this solution.

+

+

+

+

+

+

Profit margin

Financial

Customer

Learning

And Growth

Customer

satisfaction with

effectiveness

Customer

satisfaction with

efficiency

Customer

satisfaction with

service quality

Number of new

customers acquired

+

+

+

+

+

Exercise 9-7 (continued)

2. The hypotheses underlying the balanced scorecard are indicated by the

arrows in the diagram. Reading from the bottom of the balanced

scorecard, the hypotheses are:

° If the amount of compensation paid above the industry average

increases, then the percentage of job offers accepted and the level of

employee morale will increase.

° If employee morale increases, then the ratio of billable hours to total

hours should increase while the average number of errors per tax

return and the average time needed to prepare a return should

decrease.

° If employee morale increases, then the customer satisfaction with

service quality should increase.

Exercise 9-7 (continued)

Each of these hypotheses can be questioned. For example, Ariel’s

customers may define effectiveness as minimizing their tax liability

which is not necessarily the same as minimizing the number of errors in

3. The performance measure “total dollar amount of tax refunds

generated” would motivate Ariel’s employees to aggressively search for

tax minimization opportunities for its clients. However, employees may

be too aggressive and recommend questionable or illegal tax practices

Exercise 9-7 (continued)

4. Each office’s individual performance should be based on the scorecard

measures only if the measures are controllable by those employed at

the branch offices. In other words, it would not make sense to attempt

Exercise 9-8 (15 minutes)

1. ROI computations:

Net operating income Sales

ROI = ×

Sales Average operating assets

2. The manager of the New South Wales Division seems to be doing the

better job. Although its margin is three percentage points lower than the

margin of the Queensland Division, its turnover is higher (a turnover of

Exercise 9-9 (15 minutes)

Company A

Company B

Company C

Sales …………………………………..

$9,000,000

*

$7,000,000

*

$4,500,000

*

Net operating income ……………..

*

Minimum required rate of return:

*

Residual income ……………………

*

Exercise 9-10 (20 minutes)

1.

(b)

(c)

Net

Average

(a)

Operating

Operating

ROI

Sales

Income*

Assets

(b) ÷ (c)

2. The ROI increases by 2.5% for each $100,000 increase in sales. This

happens because each $100,000 increase in sales brings in an additional

profit of $25,000. When this additional profit is divided by the average

Increase in sales ……………………………………………

Contribution margin ratio …………………………………

Average operating assets …………………………………

Increase in return on investment (c) ÷ (d) ………….