Chapter 2

Job-Order Costing

Solutions to Questions

2-1 By definition, manufacturing overhead

consists of costs that cannot be practically traced

2-2 The first step is to estimate the total

amount of the allocation base (the denominator)

that will be required for next period’s estimated

level of production. The second step is to esti–

2-3 The job cost sheet is used to record all

costs that are assigned to a particular job. These

2-4 Some production costs such as a factory

manager’s salary cannot be traced to a particular

product or job, but rather are incurred as a result

2-5 If actual manufacturing overhead cost is

applied to jobs, the company must wait until the

seasonal factors or variations in output. For this

reason, most companies use predetermined over-

2-6 The measure of activity used as the allo-

cation base should drive the overhead cost; that

is, the allocation base should cause the overhead

cost. If the allocation base does not really cause

the overhead, then costs will be incorrectly at-

covered. Costs are recovered only by selling to

customers—not by allocating costs.

head rate is based on estimates.

2-9 Underapplied overhead occurs when the

overapplied overhead is disposed of by closing

out the amount to Cost of Goods Sold. The ad-

2-10 Manufacturing overhead may be un-

derapplied for several reasons. Control over over–

head spending may be poor. Or, some of the

2-11 Underapplied overhead implies that not

enough overhead was assigned to jobs during the

2-12 A plantwide overhead rate is a single

overhead rate used throughout a plant. In a mul-

tiple overhead rate system, each production de-

partment may have its own predetermined over-

head rate and its own allocation base. Some

sive.

The Foundational 15

1. The estimated total manufacturing overhead cost is computed as fol-

lows:

Y = $10,000 + ($1.00 per DLH)(2,000 DLHs)

Estimated fixed manufacturing overhead ………………

$10,000

$12,000

DLHs

2. The manufacturing overhead applied to Jobs P and Q is computed as

follows:

Actual direct labor hours worked (a) ……………

Predetermined overhead rate per DLH (b) …….

Manufacturing overhead applied (a) × (b) …….

3. The direct labor hourly wage rate can be computed by focusing on ei-

ther Job P or Job Q as follows:

Direct labor cost (a) …………………………………

The Foundational 15

4. Job P’s unit product cost and Job Q’s assigned manufacturing costs are

computed as follows:

Total manufacturing cost assigned to Job P:

Direct materials …………………………..

$13,000

Direct labor ………………………………..

Total manufacturing cost (a) ………….

$42,400

Number of units in the job (b) ………..

Direct materials …………………………..

Direct labor ………………………………..

5. The journal entries are recorded as follows:

Raw Materials …………………..

22,000

22,000

Work in Process ………………..

21,000

21,000

6. The journal entry is recorded as follows:

Work in Process ………………..

28,500

The Foundational 15

7. The journal entry is recorded as follows:

8. The Schedule of Cost of Goods Manufactured is as follows:

Direct materials:

Raw materials inventory, beginning ……………

$ 0

Add: Purchases of raw materials ……………….

22,000

Deduct: Raw materials inventory, ending …….

Raw materials used in production ………………

$21,000

Direct labor ………………………………………………

Total manufacturing costs …………………………..

Deduct: Ending work in process inventory……….

$42,400

9. The journal entry is recorded as follows:

10. The completed T-account is as follows:

Work in Process

Beg. Bal.

0

(a)

21,000

(b)

28,500

(c)

11,400

(d)

End. Bal.

18,500

The Foundational 15

11. The Schedule of Cost of Goods Sold is as follows:

Finished goods inventory, beginning ………………

$ 0

Cost of goods available for sale …………………….

Deduct: Finished goods inventory, ending ……….

12. The journal entry is recorded as follows:

13. The amount of underapplied overhead is computed as follows:

Actual direct labor-hours (a) ………………….

1,900

Manufacturing overhead applied (a) × (b) ..

Actual manufacturing overhead ………………

Deduct: Manufacturing overhead applied ….

14. The journal entry is recorded as follows:

15. The income statement is as follows:

Sales …………………………..…………………………

$60,000

Exercise 2-1 (10 minutes)

The estimated total manufacturing overhead cost is computed as follows:

Y = $94,000 + ($2.00 per DLH)(20,000 DLHs)

Estimated fixed manufacturing overhead ………………

$ 94,000

Estimated total manufacturing overhead cost …………

= Predetermined overhead rate …………………..

per DLH

Exercise 2-2 (10 minutes)

Actual direct labor-hours ………………………..

10,800

× Predetermined overhead rate ……………….

= Manufacturing overhead applied ……………

Exercise 2-3 (10 minutes)

1. Total direct labor-hours required for Job A-500:

Direct labor cost (a) ……………………………….

$108

Direct labor wage rate per hour (b) …………..

$12

2. Unit product cost for Job A-500:

Total manufacturing cost (a) ……………………

Number of units in the job (b) ………………….

Exercise 2-4 (15 minutes)

a.

Raw Materials ………………..

80,000

Accounts Payable ……….

80,000

Work in Process ……………..

62,000

Work in Process ……………..

Manufacturing Overhead…..

11,000

Manufacturing Overhead…..

Various Accounts ……….

Exercise 2-5 (20 minutes)

Parts 1 and 2.

Cash

Raw Materials

(a)

94,000

(a)

94,000

(b)

89,000

(c)

132,000

Bal.

5,000

(d)

143,000

(c)

Bal.

(e)

152,000

342,000

Bal.

(b)

152,000

(f)

342,000

(c)

(g)

(d)

143,000

22,000

Bal.

364,000

Bal.

Exercise 2-6 (20 minutes)

1.

Cost of Goods Manufactured

Direct materials:

Raw materials inventory, beginning……………

$12,000

Add: Purchases of raw materials ……………….

30,000

Total raw materials available ……………………

Deduct: Raw materials inventory, ending ……

Raw materials used in production ……………..

Direct labor ………………………………………………

87,000

Total manufacturing costs …………………………...

Add: Beginning work in process inventory……….

56,000

220,000

Deduct: Ending work in process inventory ………

Cost of goods manufactured ………………………..

$155,000

2.

Cost of Goods Sold

Finished goods inventory, beginning ………………

$ 35,000

Add: Cost of goods manufactured …………………

155,000

Goods available for sale ………………………………

Deduct: Finished goods inventory, ending……….

Unadjusted cost of goods sold ……………………..

148,000

Add: Underapplied overhead ………………………..

Adjusted cost of goods sold …………………………

$152,000

Exercise 2-7 (10 minutes)

1.

Manufacturing overhead incurred (a) ………

$215,000

Actual direct labor-hours ………………………

11,500

× Predetermined overhead rate …………….

$209,300

2. Because manufacturing overhead is underapplied, the cost of goods sold

Exercise 2-8 (10 minutes)

Direct material …………………….

$10,000

Direct labor ………………………..

Manufacturing overhead:

$12,000 × 125% ……………….

Exercise 2-9 (30 minutes)

1.

a.

Raw Materials Inventory ………………………

210,000

Accounts Payable …………………………….

210,000

b.

Work in Process …………………………………

178,000

Manufacturing Overhead ……………………..

12,000

Raw Materials Inventory ……………………

190,000

Work in Process …………………………………

90,000

Manufacturing Overhead ……………………..

110,000

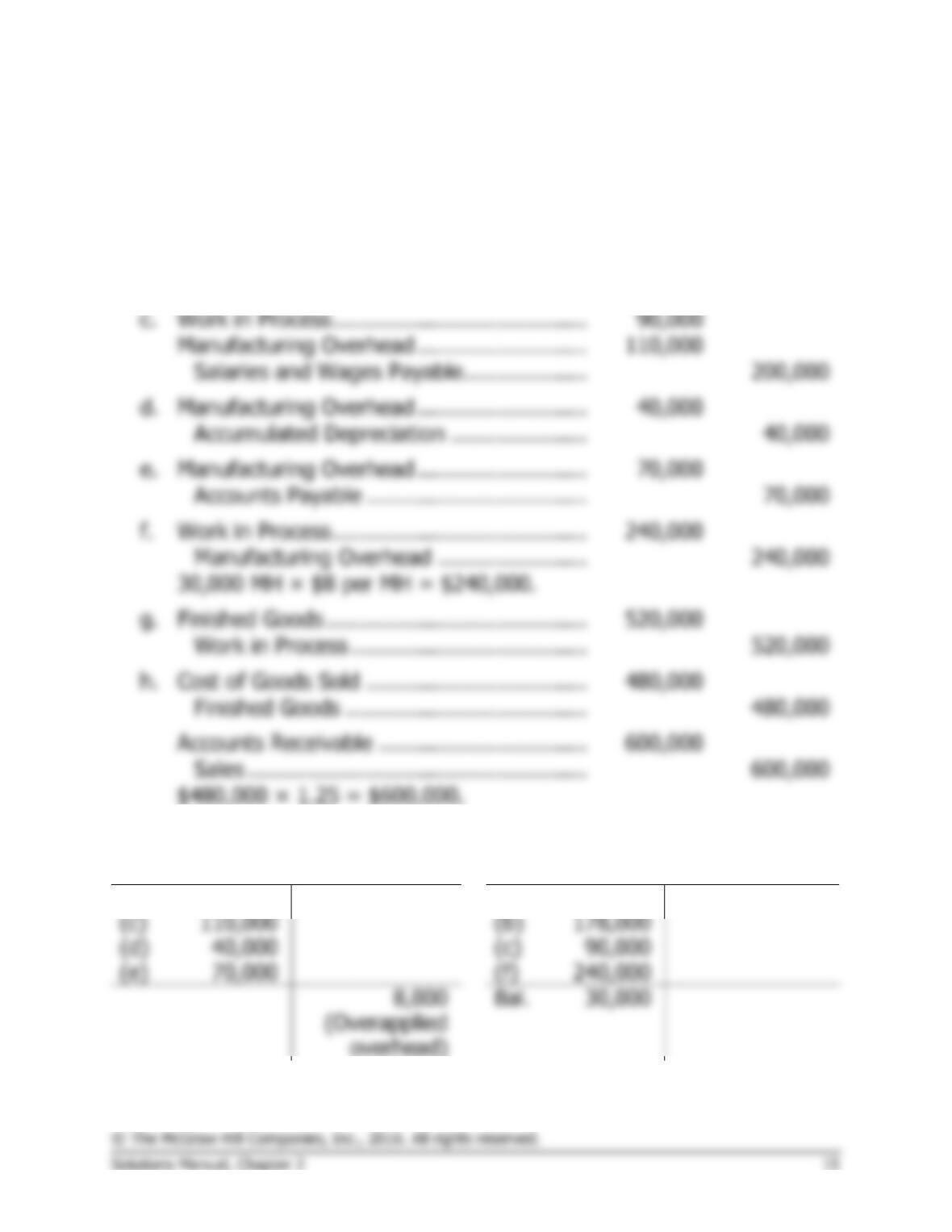

d.

Manufacturing Overhead ……………………..

40,000

Accumulated Depreciation …………………

Manufacturing Overhead ……………………..

70,000

Accounts Payable …………………………….

Work in Process …………………………………

Manufacturing Overhead …………………..

240,000

30,000 MH × $8 per MH = $240,000.

g.

Finished Goods ………………………………….

520,000

Work in Process ………………………………

520,000

Cost of Goods Sold …………………………….

480,000

Finished Goods ……………………………….

480,000

Accounts Receivable …………………………..

600,000

Sales …………………………………………….

600,000

$480,000 × 1.25 = $600,000.

2.

Manufacturing Overhead

Work in Process

(b)

12,000

(f)

240,000

Bal.

42,000

(g)

520,000

(d)

40,000

(c)

90,000

(e)

70,000

(f)

Bal.

30,000

Exercise 2-10 (10 minutes)

Yes, overhead should be applied to value the Work in Process inventory at

year-end.

Exercise 2-11 (30 minutes)

1. Mason Company’s schedule of cost of goods manufactured is as follows:

Direct materials:

Beginning raw materials inventory ………………

$ 7,000

Add: Purchases of raw materials …………………

118,000

Raw materials available for use …………………..

Deduct: Ending raw materials inventory ……….

Raw materials used in production ……………….

$110,000

Direct labor ………………………………………………

Manufacturing overhead ……………………………..

90,000

Total manufacturing costs …………………………...

Add: Beginning work in process inventory ……….

Deduct: Ending work in process inventory ……….

Cost of goods manufactured…………………………

2. Mason Company’s schedule of cost of goods sold is as follows:

Beginning finished goods inventory ………….

$ 20,000

Add: Cost of goods manufactured ……………

275,000

Goods available for sale ………………………..

Deduct: Ending finished goods inventory ….

Unadjusted cost of goods sold ………………..

Deduct: Overapplied overhead ……………….

Adjusted cost of goods sold ……………………

3.

Mason Company

Income Statement

Sales …………………………..…………………………

$524,000

Cost of goods sold ($260,000 – $10,000) ……….

250,000

Gross margin ……………………………………………

Selling and administrative expenses:

Selling expenses …………………………………….

Administrative expense …………………………...

Net operating income ………………………………..

Exercise 2-12 (15 minutes)

1.

Actual manufacturing overhead costs ……..

$473,000

Overapplied overhead cost ……………………

2.

Direct materials:

Raw materials inventory, beginning ……..

$ 20,000

Add purchases of raw materials …………..

400,000

Raw materials available for use …………..

420,000

Deduct raw materials inventory, ending ..

Raw materials used in production ………..

390,000

Less indirect materials ……………………….

Direct labor ……………………………………….

Total manufacturing costs …………………….

Add: Work in process, beginning ……………

960,000

Deduct: Work in process, ending ……………

Cost of goods manufactured …………………

Exercise 2-13 (30 minutes)

1.

Units

Produced

Manufacturing

Overhead

High activity level (First quarter) …

80,000

$300,000

Low activity level (Third quarter) …

Change ………………………………….

Total overhead cost (First quarter) ………………………..

Variable cost element ($2.00 per unit × 80,000 units) .

Fixed cost element …………………………………………….

Estimated fixed manufacturing overhead ………………

$2.00 per unit × 60,000 units …………………………..

120,000

Estimated total manufacturing overhead cost …………

$260,000

Total manufacturing cost and unit product cost:

Exercise 2-13 (continued)

2. The fixed portion of the manufacturing overhead cost is causing the unit

3. The unit product cost can be stabilized by using a predetermined over-

head rate that is based on expected activity for the entire year. The cost

formula created in requirement 1 can be adapted to compute the annual

Estimated total manufacturing overhead cost …………

The annual predetermined overhead rate is computed as follows:

Estimated total manufacturing overhead ….

$960,000

÷ Estimated total units produced ……………

200,000

= Predetermined overhead rate ……………..

$4.80

per unit

Using a predetermined overhead rate of $4.80 per unit, the unit product

costs would stabilize as shown below:

Quarter

First

Second

Third

Fourth

Direct materials ……………..

$240,000

$120,000

$ 60,000

$180,000

Direct labor …………………..

Number of units produced .

Unit product cost ……………