3-383

Which of the following statements concerning the unit product cost of Product A8 is true?

3-384

3-385

65.

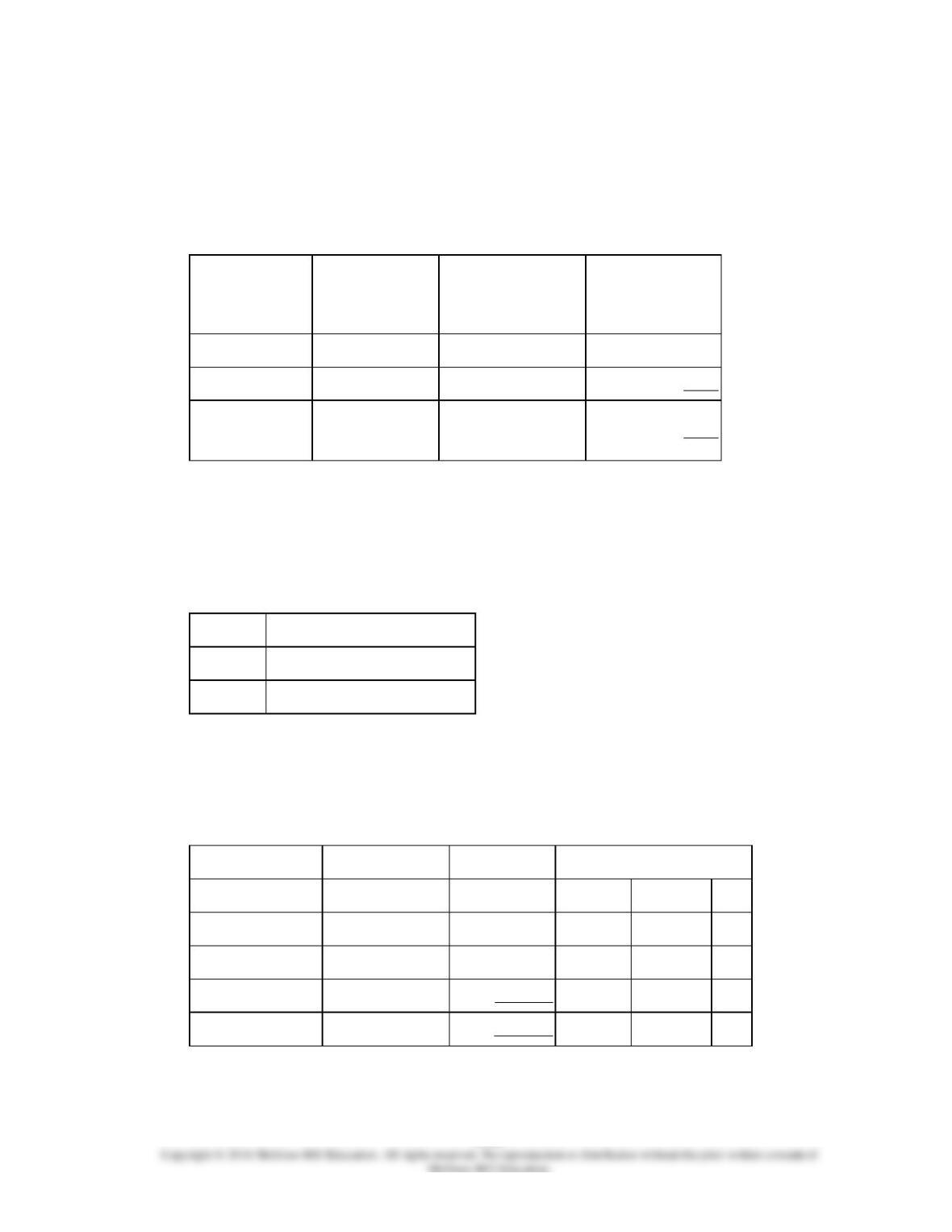

Hane Corporation uses the following activity rates from its activity-based costing to assign

overhead costs to products:

Activity Cost Pools

Activity Rate

Assembling products

$8.90

per assembly

hour

Processing customer

orders

$31.23

per customer

order

Setting up batches

$43.72

per batch

Data for one of the company’s products follow:

Product U94W

Number of assembly hours

389

Number of customer orders

53

Number of batches

61

How much overhead cost would be assigned to Product U94W using the activity-based

costing system?

3-387

66.

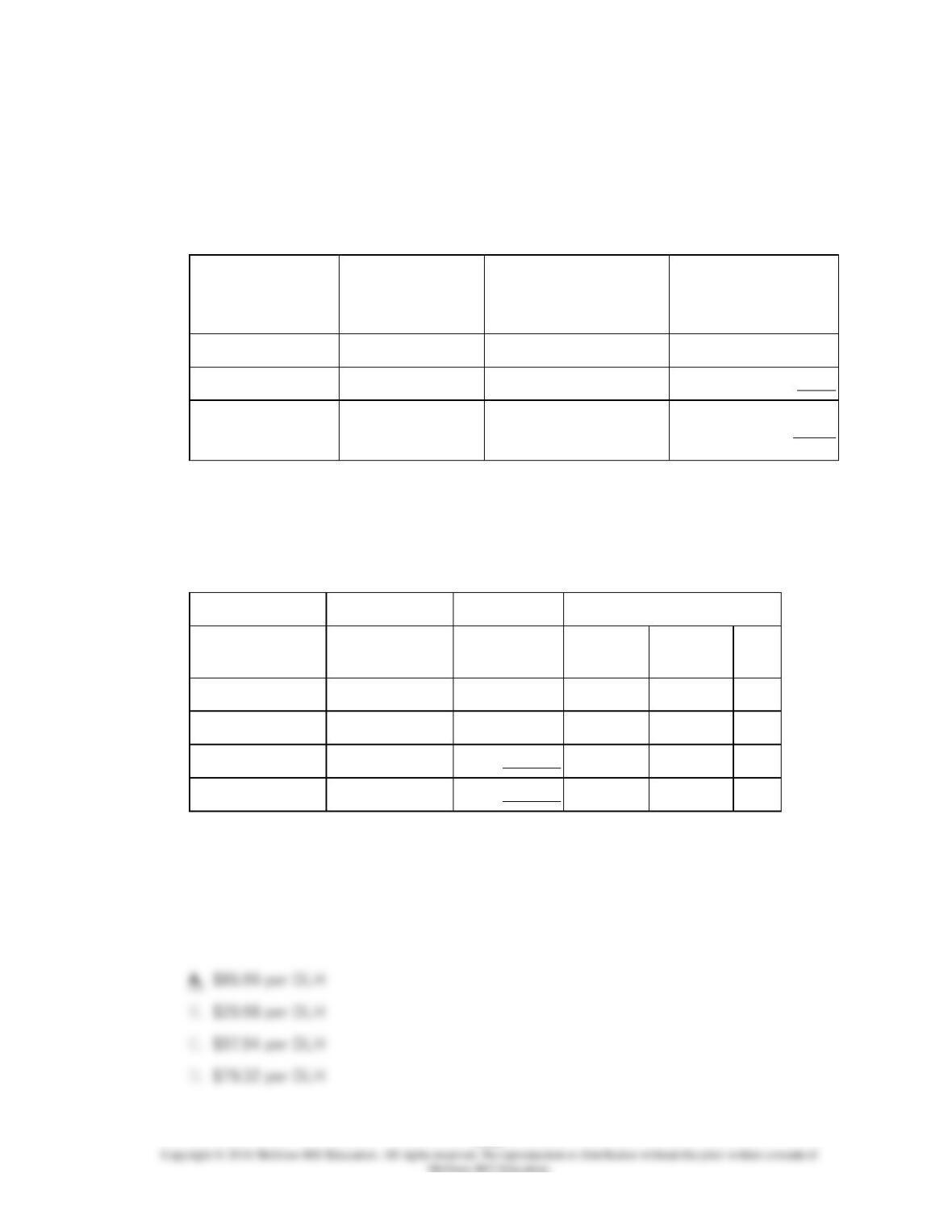

Activity rates from Lippard Corporation’s activity-based costing system are listed below.

The company uses the activity rates to assign overhead costs to products:

Activity Cost Pools

Activity Rate

Processing customer orders

$31.62

per customer order

Assembling products

$2.86

per assembly hour

Setting up batches

$46.61

per batch

Processing customer orders

per customer order

Assembling products

per assembly hour

Setting up batches

per batch

3,588.97

Total overhead cost

Last year, Product H50E involved 9 customer orders, 666 assembly hours, and 77 batches.

How much overhead cost would be assigned to Product H50E using the activity-based

costing system?

3-389

67.

Gould Corporation uses the following activity rates from its activity-based costing to

assign overhead costs to products:

Activity Cost Pools

Activity Rate

Setting up batches

$59.06

per batch

Processing customer orders

$72.66

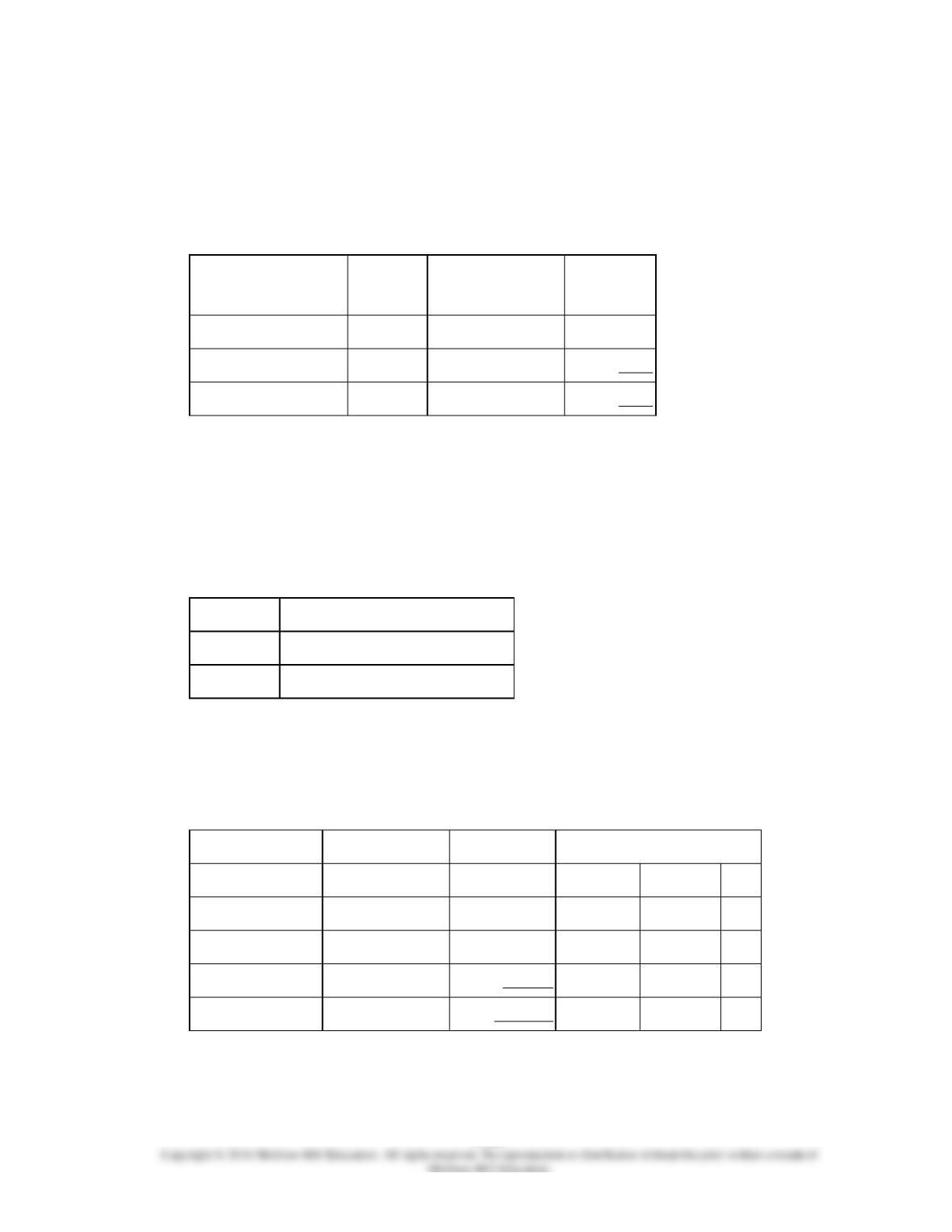

per customer order

Assembling products

$3.75

per assembly hour

Data concerning two products appear below:

Product

K91B

Product

F65O

Number of batches

84

50

Number of customer

orders

32

43

Number of assembly

hours

483

890

How much overhead cost would be assigned to Product K91B using the activity-based

costing system?

3-391

3-392

68.

Trisdale, Inc., manufactures and sells two products: Product V5 and Product X3. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours Per

Unit

Total Direct Labor-

Hours

Product V5

900

5.0

4,500

Product X3

1,000

3.0

3,000

Total direct labor-

hours

7,500

The company’s total manufacturing overhead is $372,695. If the company allocates all of

its overhead based on direct labor-hours, the predetermined overhead rate would be

closest to:

3-393

69.

Sow, Inc., manufactures and sells two products: Product I4 and Product P3. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours

Per Unit

Total Direct

Labor-Hours

Product I4

700

8.0

5,600

Product P3

400

9.0

3,600

Total direct labor-

hours

9,200

The direct labor rate is $24.70 per DLH. The direct materials cost per unit for each

product is given below:

Direct Materials Cost per Unit

Product I4

$136.60

Product P3

$145.70

The company is considering adopting an activity-based costing system with the following

activity cost pools, activity measures, and expected activity:

Estimated

Expected Activity

Activity Cost Pools

Activity Measures

Overhead Cost

Product I4

Product P3

Total

Labor-related

DLHs

$210,404

5,600

3,600

9,200

Product testing

tests

59,983

300

400

700

General factory

MHs

613,015

3,300

3,200

6,500

$883,402

3-394

The unit product cost of Product P3 under the company’s traditional costing method in

which all overhead is allocated on the basis of direct labor-hours is closest to:

3-395

70.

Molinas, Inc., manufactures and sells two products: Product G1 and Product S8. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours Per

Unit

Total Direct Labor-

Hours

Product G1

800

8.0

6,400

Product S8

1,000

5.0

5,000

Total direct labor-

hours

11,400

The company is considering adopting an activity-based costing system with the following

activity cost pools, activity measures, and expected activity:

Estimated

Expected Activity

Activity Cost Pools

Activity Measures

Overhead Cost

Product G1

Product S8

Total

Labor-related

DLHs

$239,172

6,400

5,000

11,400

Product testing

tests

55,524

400

300

700

General factory

MHs

685,580

3,400

3,600

7,000

$980,276

If the company allocates all of its overhead based on direct labor-hours using its

traditional costing method, the predetermined overhead rate would be closest to:

3-396

3-397

71.

Finken, Inc., manufactures and sells two products: Product H9 and Product L0. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours Per

Unit

Total Direct Labor-

Hours

Product H9

400

5.0

2,000

Product L0

800

6.0

4,800

Total direct labor-

hours

6,800

Direct materials

The direct labor rate is $16.10 per DLH. The direct materials cost per unit is $256.40 for

Product H9 and $125.00 for Product L0. The estimated total manufacturing overhead is

$441,772.

The unit product cost of Product L0 under the company’s traditional costing method in

which all overhead is allocated on the basis of direct labor-hours is closest to:

3-398

3-399

72.

Whiteley, Inc., manufactures and sells two products: Product M5 and Product P4. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours

Per Unit

Total Direct

Labor-Hours

Product M5

200

9.0

1,800

Product P4

100

12.0

1,200

Total direct labor-hours

3,000

The direct labor rate is $27.50 per DLH. The direct materials cost per unit for each

product is given below:

Direct Materials Cost per Unit

Product M5

$185.20

Product P4

$244.20

The company is considering adopting an activity-based costing system with the following

activity cost pools, activity measures, and expected activity:

Estimated

Expected Activity

Activity Cost Pools

Activity Measures

Overhead Cost

Product M5

Product P4

Total

Labor-related

DLHs

$117,330

1,800

1,200

3,000

Product testing

tests

9,499

400

300

700

General factory

MHs

641,606

5,000

4,800

9,800

$768,435

3-400

The unit product cost of Product P4 under activity-based costing is closest to:

3-401

3-402

73.

Lamon, Inc., manufactures and sells two products: Product J9 and Product R6. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours Per

Unit

Total Direct Labor-

Hours

Product J9

300

9.0

2,700

Product R6

900

7.0

6,300

Total direct labor-

hours

9,000

The company is considering adopting an activity-based costing system with the following

activity cost pools, activity measures, and expected activity:

Estimated

Expected Activity

Activity Cost Pools

Activity Measures

Overhead Cost

Product J9

Product R6

Total

Labor-related

DLHs

$302,490

2,700

6,300

9,000

Machine setups

setups

60,088

400

300

700

General factory

MHs

95,282

3,700

3,400

7,100

$457,860

If the company allocates all of its overhead based on direct labor-hours using its

traditional costing method, the overhead assigned to each unit of Product J9 would be

closest to: