Chapter 4

Process Costing

Solutions to Questions

4-1 A process costing system should be

used in situations where a homogeneous

product is produced on a continuous basis in

large quantities.

4-2 Job-order and processing costing are

similar in the following ways:

1. Job-order costing and process costing have

4-3 Cost accumulation is simpler under

process costing because costs only need to be

assigned to departments—not individual jobs. A

4-5 The journal entry to record the transfer

of work in process from the Mixing Department

to the Firing Department is:

Work in Process, Firing …………………………..

XXXX

Work in Process, Mixing………………………….

XXXX

4-6 The costs that might be added in the

transferred to the next department (or to

finished goods) during the period plus the

equivalent units in the department’s ending

work in process inventory.

The Foundational 15

1. The journal entries would be recorded as follows:

Work in Process—Mixing …………………………..

120,000

Work in Process—Mixing …………………………..

2. The journal entry would be recorded as follows:

Work in Process—Mixing …………………………..

3. The “units completed and transferred to finished goods” is computed

as follows:

Started into production during the month ……………..

37,500

Total pounds in process …………………………………….

42,500

Deduct work in process, June 30 …………………………

Completed and transferred out during the month ……

4. and 5.

The equivalent units of production for materials and conversion are

computed as follows:

Equivalent Units

Materials

Conversion

Units transferred out …………………………..

34,500

34,500

Work in process, ending:

The Foundational 15 (continued)

6. and 7.

Materials

Conversion

8. and 9.

The cost per equivalent unit for materials and conversion is computed

10. and 11.

The cost of ending work in process inventory for materials and

conversion is computed as follows:

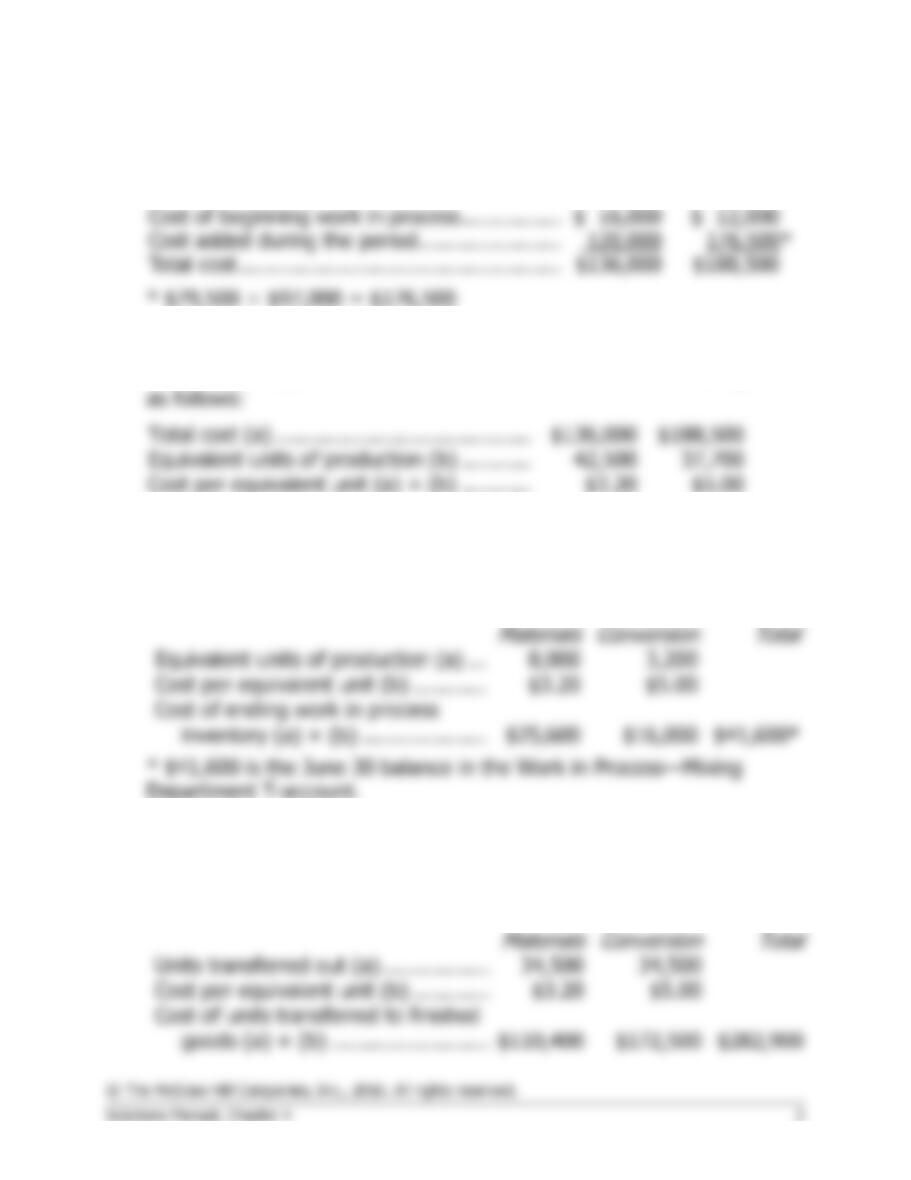

12. and 13.

The cost of materials and conversion transferred to finished goods is

computed as follows:

The Foundational 15 (continued)

14. The journal entry to record the transfer of costs from Work in

15. The total cost to be accounted for and the total cost accounted for is:

Costs to be accounted for:

Cost of beginning work in process inventory …….

$ 28,000

Costs added to production during the period ……

Cost of ending work in process inventory ………..

$ 41,600

Total cost accounted for ………………………………

Exercise 4-1 (20 minutes)

a. To record issuing raw materials for use in production:

Work in Process—Molding Department ……… 23,000

Work in Process—Firing Department …………. 8,000

Raw Materials ………………………………… 31,000

b. To record direct labor costs incurred:

d. To record transfer of unfired, molded bricks from the Molding

Department to the Firing Department:

Work in Process—Firing Department …………. 57,000

Work in Process—Molding Department … 57,000

Exercise 4-2 (10 minutes)

Weighted-Average Method

Equivalent Units

Materials

Conversion

Units transferred out ………………….

190,000

190,000

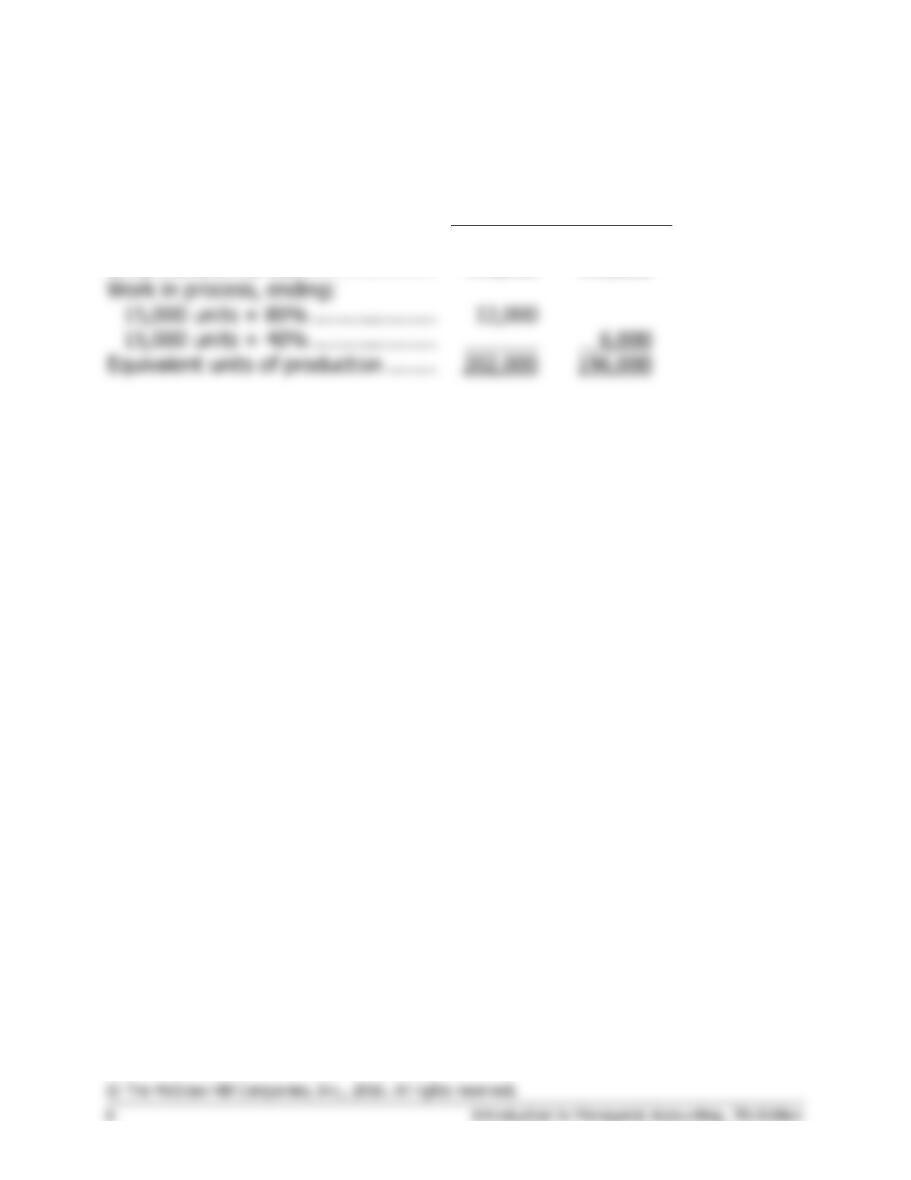

Work in process, ending:

Equivalent units of production ……..

Exercise 4-3 (10 minutes)

Weighted-Average Method

1.

Materials

Labor

Overhead

Cost added during the period ……..

Total cost (a) ………………………….

Equivalent units of production (b) .

Cost per equivalent unit (a) ÷ (b) .

Cost of beginning work in process

2.

Cost per equivalent unit for materials …..

$ 7.34

Cost per equivalent unit for labor ………..

Cost per equivalent unit for overhead …..

13.00

Exercise 4-4 (10 minutes)

Materials

Conversion

Total

Ending work in process inventory:

Equivalent units of production ……

2,000

800

Cost per equivalent unit ……………

Units completed and transferred out:

Cost per equivalent unit ……………

Cost of units transferred out ………

$278,586

$367,629

Exercise 4-5 (10 minutes)

Baking Department

Cost Reconciliation

Costs to be accounted for:

Cost of beginning work in process inventory .

$ 3,570

Costs added to production during the period .

43,120

Total cost to be accounted for ………………….

$46,690

Costs accounted for as follows:

Cost of ending work in process inventory ……

$ 2,860

Cost of units completed and transferred out ..

*

Total cost accounted for ………………………….

Exercise 4-6 (10 minutes)

Weighted-Average Method

1.

Tons of Pulp

Work in process, June 1 ……………………………………

20,000

Started into production during the month ……………..

Total tons in process ………………………………………..

Deduct work in process, June 30 …………………………

Completed and transferred out during the month ……

2.

Equivalent Units

Materials

Labor and

Overhead

Units transferred out …………………………..

Work in process, ending:

Equivalent units of production ……………….

Exercise 4-7 (10 minutes)

Work in Process—Cooking …………

42,000

Raw Materials Inventory ………

42,000

Work in Process—Cooking …………

50,000

Work in Process—Molding …………

36,000

Wages Payable …………………..

86,000

Work in Process—Cooking …………

75,000

Work in Process—Molding …………

Work in Process—Cooking …….

Finished Goods ……………………….

Work in Process—Molding …….

Exercise 4-8 (30 minutes)

Weighted-Average Method

1.

Materials

Conversion

Equivalent units of production …………………….

Units transferred to the next production

2.

Materials

Conversion

Cost of beginning work in process ………………

$ 1,500

$ 4,000

Cost added during the period …………………….

54,000

Cost per equivalent unit (a) ÷ (b) ……………….

3.

Materials

Conversion

Total

Ending work in process inventory:

Equivalent units of production

(see above) ……………………

10,000

3,000

$2.00

$3,000

Units completed and transferred out:

department ……………………

175,000

$2.00

Exercise 4-9 (15 minutes)

Weighted-Average Method

1.

Materials

Labor

Overhead

Units transferred to the next

department ………………………………..

42,000

42,000

42,000

Work in process, ending:

2.

Materials

Labor

Overhead

Exercise 4-10 (10 minutes)

Weighted-Average Method

Materials

Labor &

Overhead

Pounds transferred to the Packing Department

during July* ………………………………………………

375,000

375,000

400,000

390,000

Exercise 4-11 (30 minutes)

Weighted-Average Method

1.

Equivalent units of production

Pulping

Conversion

Transferred to next department ……………………

Ending work in process:

Equivalent units of production ……………………..

2.

Cost per equivalent unit

Pulping

Conversion

Cost of beginning work in process …………….

Cost added during the period …………………..

Total cost (a) …………………………..…………..

Equivalent units of production (b) …………….

159,000

Cost per equivalent unit, (a) ÷ (b) ……………

$0.65

$0.20

3.

Cost of ending work in process inventory and units transferred out

Pulping

Conversion

Total

Ending work in process inventory:

Equivalent units of production…

8,000

2,000

Cost per equivalent unit ………..

$0.65

$0.20

Units completed and transferred out:

Cost per equivalent unit ………..

$0.65

$0.20

$31,400

Exercise 4-11 (continued)

4.

Cost reconciliation

Costs to be accounted for:

Costs added to production during the period

Costs accounted for as follows:

Cost of beginning work in process inventory

Exercise 4-12 (20 minutes)

Weighted-Average Method

1. Computation of equivalent units in ending inventory:

Materials

Labor

Overhead

Equivalent units of production …

2. Cost of ending work in process inventory and units transferred out:

Materials

Labor

Overhead

Total

Ending work in process inventory:

Cost of ending work in

$47,280

Units completed and transferred out:

Cost of units completed

Equivalent units of

3. Cost reconciliation:

Total cost to be accounted for ………………………

$599,780

Costs accounted for as follows:

Problem 4-13A (60 minutes)

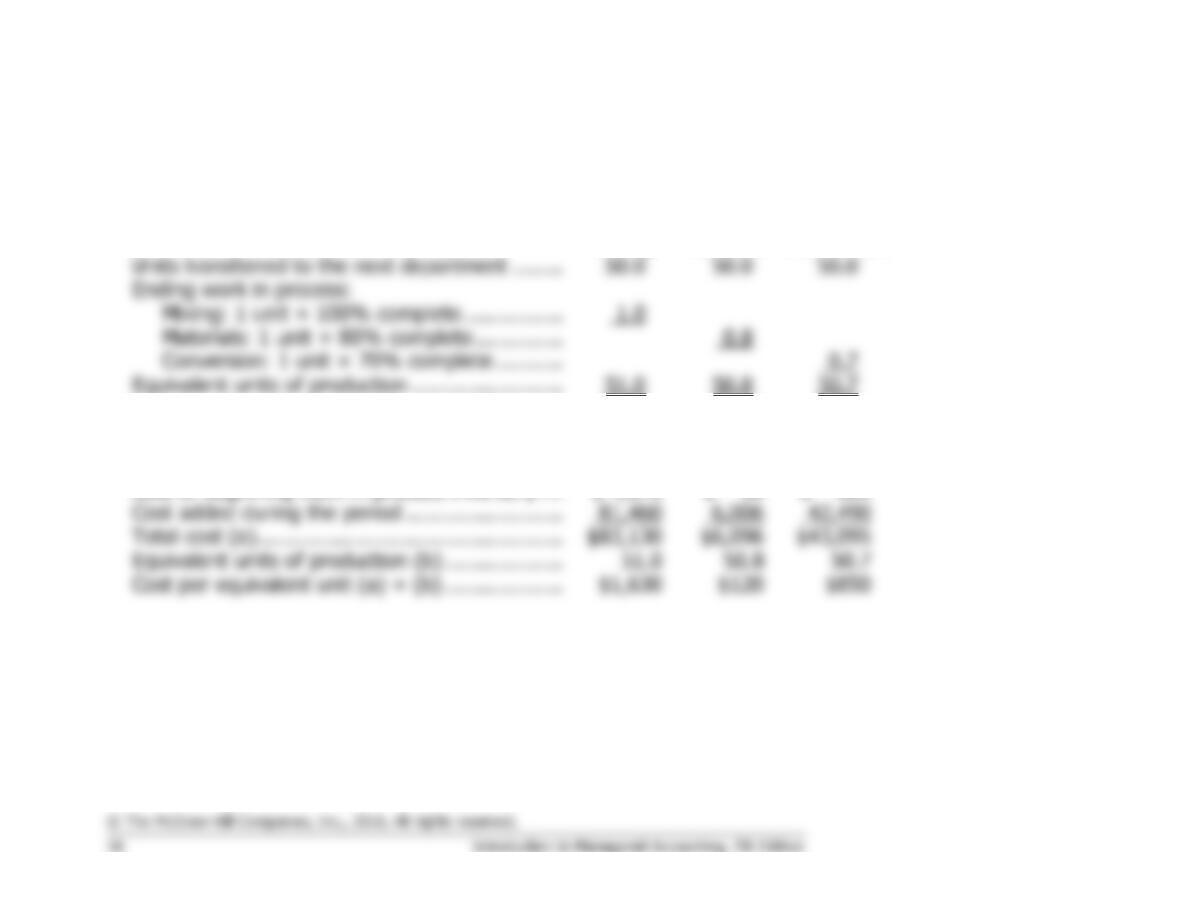

Weighted-Average Method

1. Computation of equivalent units in ending inventory:

Mixing

Materials

Conversion

Units transferred to the next department ……..

1.0

Equivalent units of production ……………………

2. Costs per equivalent unit:

Mixing

Materials

Conversion

Cost of beginning work in process inventory ….

$ 1,670

$ 90

$ 605

Total cost (a) ………………………………………….

Equivalent units of production (b) ……………….

Problem 4-13A (continued)

3. Costs of ending work in process inventory and units transferred out:

Mixing

Materials

Conversion

Total

Ending work in process inventory:

Units completed and transferred out:

4. Cost reconciliation:

Cost to be accounted for:

Cost added to production during the period

Costs accounted for as follows:

Cost of beginning work in process inventory

Problem 4-14A (45 minutes)

Weighted-Average Method

1.

Equivalent units of production

Materials

Conversion

Transferred to next department* ………………….

170,000

170,000

Ending work in process:

Equivalent units of production ……………………..

2.

Cost per equivalent unit

Materials

Conversion

Cost of beginning work in process …………….

Cost added during the period …………………..

Total cost (a) …………………………..…………..

Equivalent units of production (b) …………….

179,000

Cost per equivalent unit, (a) ÷ (b) ……………

$1.30

3.

Cost of ending work in process inventory and units transferred out

Materials

Conversion

Total

Ending work in process inventory:

Equivalent units of production…

15,000

9,000

Cost per equivalent unit ………..

$1.30

$11,700

Units completed and transferred out:

170,000

Cost per equivalent unit ………..

$1.30