Problem 2-25A (continued)

5. The amount of overhead cost in Work in Process was:

$24,000 direct materials cost × 160% = $38,400

The amount of direct labor cost in Work in Process is:

1.

a.

Raw Materials ………………………………

200,000

Accounts Payable …………………….

200,000

b.

Work in Process …………………………...

185,000

Raw Materials ………………………….

185,000

Manufacturing Overhead ………………..

63,000

Utilities Expense …………………………..

Accounts Payable …………………….

d.

Work in Process …………………………...

Manufacturing Overhead ………………..

90,000

Salaries Expense …………………………..

110,000

Salaries and Wages Payable ……….

430,000

e.

Manufacturing Overhead ………………..

54,000

Accounts Payable …………………….

54,000

f.

Advertising Expense ………………………

136,000

Accounts Payable …………………….

136,000

g.

Manufacturing Overhead ………………..

76,000

Depreciation Expense…………………….

19,000

Accumulated Depreciation ………….

95,000

Manufacturing Overhead ………………..

102,000

Rent Expense ………………………………

18,000

Accounts Payable …………………….

120,000

Work in Process …………………………...

390,000

Manufacturing Overhead ……………

390,000

Problem 2-26A (continued)

j.

Finished Goods …………………………….

770,000

Work in Process ……………………….

770,000

Accounts Receivable ………………………

Sales ……………………………………..

Cost of Goods Sold ………………………..

800,000

Problem 2-26A (continued)

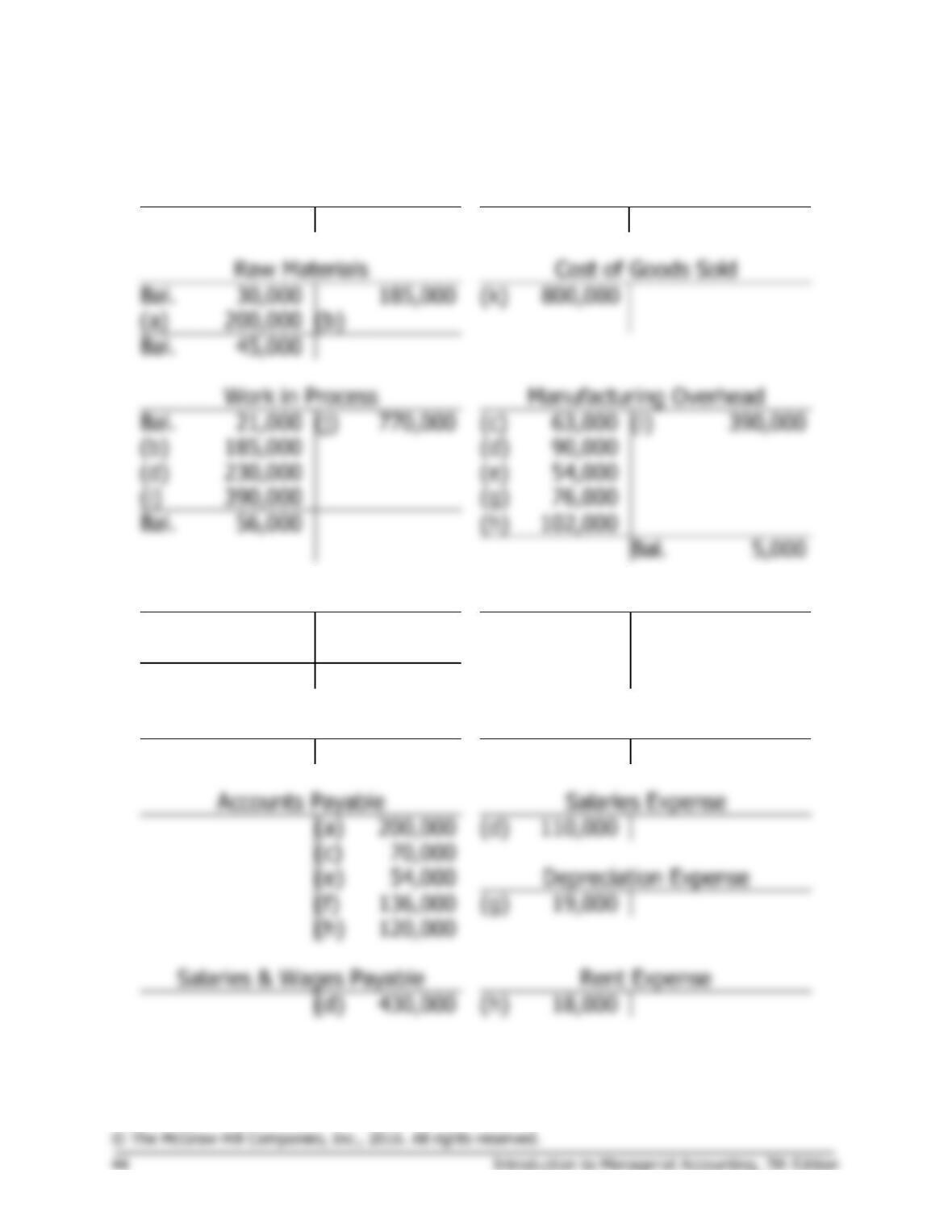

2.

Accounts Receivable

Sales

(k)

1,200,000

(k)

1,200,000

Bal.

30,000

185,000

(k)

800,000

(a)

(b)

Bal.

45,000

Bal.

21,000

(j)

770,000

(c)

63,000

(b)

(d)

(d)

230,000

(e)

54,000

390,000

(g)

76,000

Bal.

56,000

(h)

102,000

Bal.

Finished Goods

Advertising Expense

Bal.

60,000

(k)

800,000

(f)

136,000

(j)

770,000

Bal.

30,000

Accumulated Depreciation

Utilities Expense

(g)

95,000

(c)

7,000

(a)

200,000

(d)

110,000

(c)

(e)

54,000

(f)

(g)

(h)

120,000

(d)

430,000

(h)

18,000

Problem 2-26A (continued)

3.

Froya Fabrikker A/S

Schedule of Cost of Goods Manufactured

Direct materials:

Raw materials inventory, beginning ……..

$ 30,000

Purchases of raw materials …………………

Materials available for use ………………….

Raw materials inventory, ending ………….

$185,000

Direct labor ……………………………………….

Total manufacturing costs …………………….

Add: Work in process, beginning ……………

Deduct: Work in process, ending ……………

Cost of goods manufactured …………………

4.

Manufacturing Overhead ………………………

5,000

Cost of Goods Sold …………………………

5,000

Schedule of cost of goods sold:

Finished goods inventory, beginning …….

$ 60,000

Add: Cost of goods manufactured ………..

Goods available for sale …………………….

Deduct: Overapplied overhead …………….

Adjusted cost of goods sold ………………..

Problem 2-26A (continued)

5.

Froya Fabrikker A/S

Income Statement

Sales ……………………………………………..

$1,200,000

Cost of goods sold …………………………….

795,000

Gross margin …………………………………..

405,000

Selling and administrative expenses:

Net operating income ………………………..

6.

Direct materials …………………………………………………

$ 8,000

Direct labor ………………………………………………………

9,200

Total manufacturing cost …………………………………….

Add markup (60% × $32,800) ……………………………..

Total billed price of Job 412 …………………………..…….

Problem 2-27A (60 minutes)

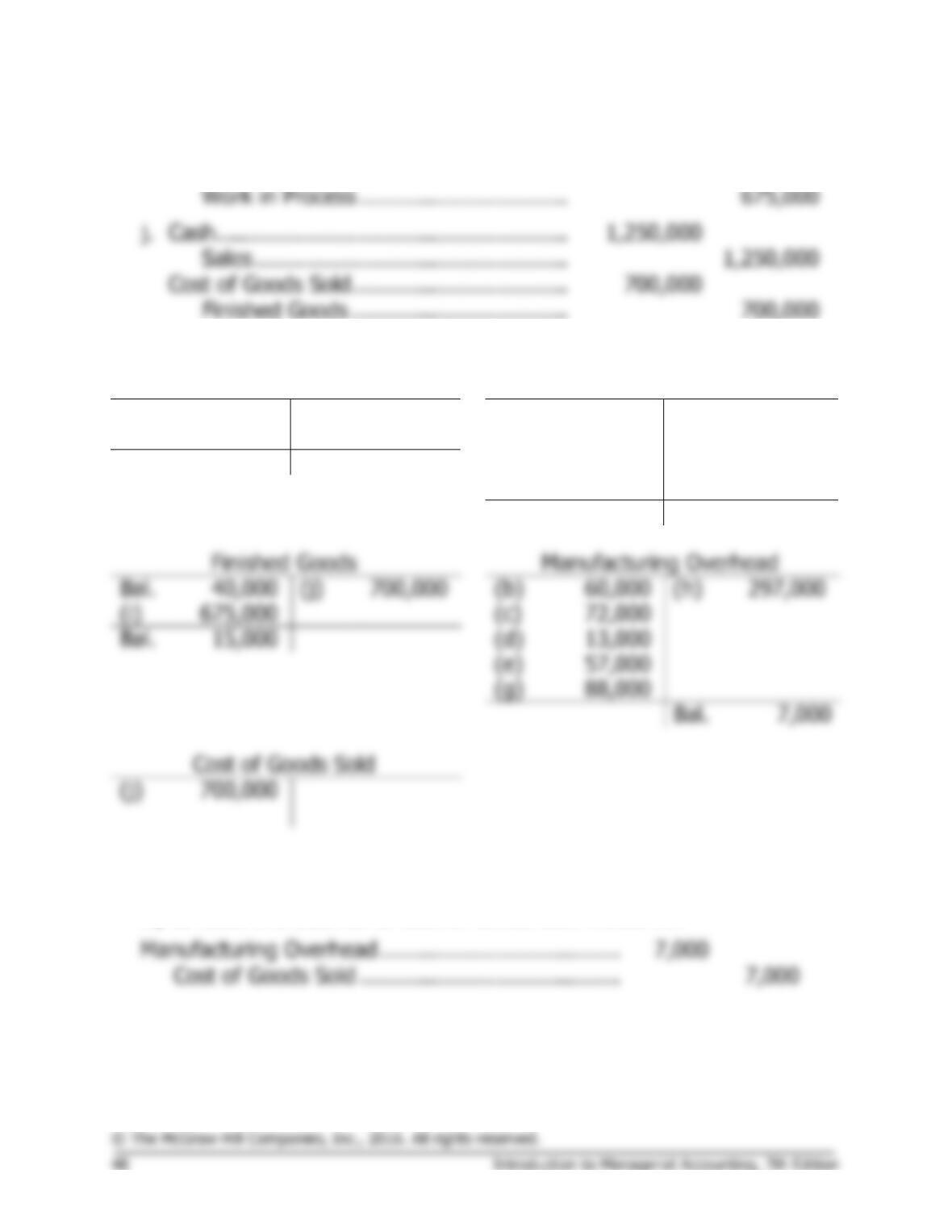

1.

a.

Raw Materials ………………………………….

275,000

Cash …………………………………………

275,000

b.

Work in Process ……………………………….

220,000

Manufacturing Overhead ……………………

60,000

Raw Materials ……………………………..

280,000

Work in Process ……………………………….

180,000

Manufacturing Overhead ……………………

Salaries Expense ………………………………

90,000

Cash …………………………………………

405,000

d.

Manufacturing Overhead ……………………

13,000

Rent Expense ………………………………….

Manufacturing Overhead ……………………

f.

Advertising Expense ………………………….

140,000

Cash …………………………………………

140,000

g.

Manufacturing Overhead ……………………

88,000

Depreciation Expense ………………………..

12,000

Accumulated Depreciation ……………..

100,000

Work in Process ……………………………….

297,000

Manufacturing Overhead ……………….

297,000

Problem 2-27A (continued)

i.

Finished Goods ………………………………..

675,000

Cash ………………………………………………

Cost of Goods Sold …………………………...

700,000

2.

Raw Materials

Work in Process

Bal.

25,000

(b)

280,000

Bal.

10,000

(i)

675,000

(a)

275,000

(b)

220,000

Bal.

20,000

(c)

180,000

(h)

297,000

Bal.

32,000

Bal.

40,000

(j)

(b)

60,000

(h)

(i)

675,000

(c)

72,000

Bal.

15,000

(d)

13,000

(e)

57,000

(g)

88,000

Bal.

(j)

700,000

3. Manufacturing overhead is overapplied by $7,000 for the year. The en-

try to close this balance to Cost of Goods Sold would be:

Problem 2-27A (continued)

4.

Gold Nest Company

Income Statement

Sales ……………………………………………..

$1,250,000

Selling and administrative expenses:

Net operating income ………………………..

Cost of goods sold

Problem 2-28A (60 minutes)

1. and 2.

Cash

Accounts Receivable

Bal.

63,000

(m)

785,000

Bal.

102,000

(l)

850,000

(l)

850,000

(k)

925,000

Bal.

128,000

Bal.

177,000

(a)

Bal.

Bal.

15,000

Videos in Process

Bal.

45,000

(j)

Bal.

(k)

(b)

(j)

550,000

(f)

82,000

Bal.

31,000

(i)

Bal.

37,000

Studio and Equipment

Accumulated Depreciation

Bal.

730,000

Bal.

210,000

(d)

84,000

Bal.

294,000

Studio Overhead

Depreciation Expense

(b)

30,000

* (i)

290,000

(d)

21,000

(c)

72,000

(d)

63,000

(f)

110,000

(g)

(n)

9,400

Bal.

(g)

Problem 2-28A (continued)

Administrative Salaries Expense

Sales

(f)

95,000

(k)

925,000

(k)

(n)

(m)

500,000

Bal.

185,000

Bal.

(c)

130,000

Bal.

Bal.

Bal.

3. Overhead is overapplied for the year by $9,400. Entry (n) above records

the closing of this overapplied overhead balance to Cost of Goods Sold.

4.

Supreme Videos, Inc.

Income Statement

For the Year Ended December 31

Sales of videos …………………………………….

$925,000

Cost of goods sold ($600,000 – $9,400) …….

130,000

Administrative salaries …………………………

Insurance expense ……………………………..

Case (60 minutes)

1.

a.

Estimated total manufacturing overhead cost

Predetermined =

overhead rate Estimated total amount of the allocation base

2.

a.

Fabricating

Department

Machining

Department

Assembly

Department

Estimated manufacturing

overhead cost (a) ………

$350,000

$400,000

$ 90,000

Predetermined overhead

rate (a) ÷ (b) ……………

Fabricating Department:

Machining Department:

Assembly Department:

Total applied overhead …………………

Estimated direct labor

3. The bulk of the labor cost on the Koopers job is in the Assembly De-

partment, which incurs very little overhead cost. The department has an

overhead rate of only 30% of direct labor cost as compared to much

higher rates in the other two departments. Therefore, as shown above,

Case (continued)

bid too high and lost the job. Too much overhead cost was assigned to

the job for the kind of work being done on the job in the plant.

4. The company’s bid was:

Direct materials …………………………………….

$ 4,600

Direct labor ………………………………………….

9,500

Manufacturing overhead applied (above) ……

Total manufacturing cost ………………………..

$27,400

Bidding rate …………………………………………

Total bid price ………………………………………

$41,100

If departmental overhead rates had been used, the bid would have

been:

Direct materials …………………………………….

$ 4,600

Direct labor ………………………………………….

9,500

Manufacturing overhead applied (above) ……

Total manufacturing cost ………………………..

$22,860

Bidding rate …………………………………………

Total bid price ………………………………………

$34,290

5.

a.

Actual overhead cost …………………………………

$864,000

Applied overhead cost ($580,000 × 140%) …….

812,000

Underapplied overhead cost ………………………..

$ 52,000

Case (continued)

b.

Department

Fabricating

Machining

Assembly

Total Plant

Actual overhead

Ethics Challenge (45 minutes)

1. Shaving 5% off the estimated direct labor-hours in the predetermined

overhead rate will result in an artificially high overhead rate. The artifi–

2. This question may generate lively debate. Where should Terri Ronsin’s

loyalties lie? Is she working for the general manager of the division or

for the corporate controller? Is there anything wrong with the “Christ-

mas bonus”? How far should Terri go in bucking her boss on a new job?

While individuals can certainly disagree about what Terri should do,

some of the facts are indisputable. First, understating direct labor-hours

artificially inflates the overhead rate. This has the effect of inflating the

Ethics Challenge (continued)

In the actual situation that this case is based on, the corporate control-

ler’s staff were aware of the general manager’s accounting tricks, but