4-256

108.

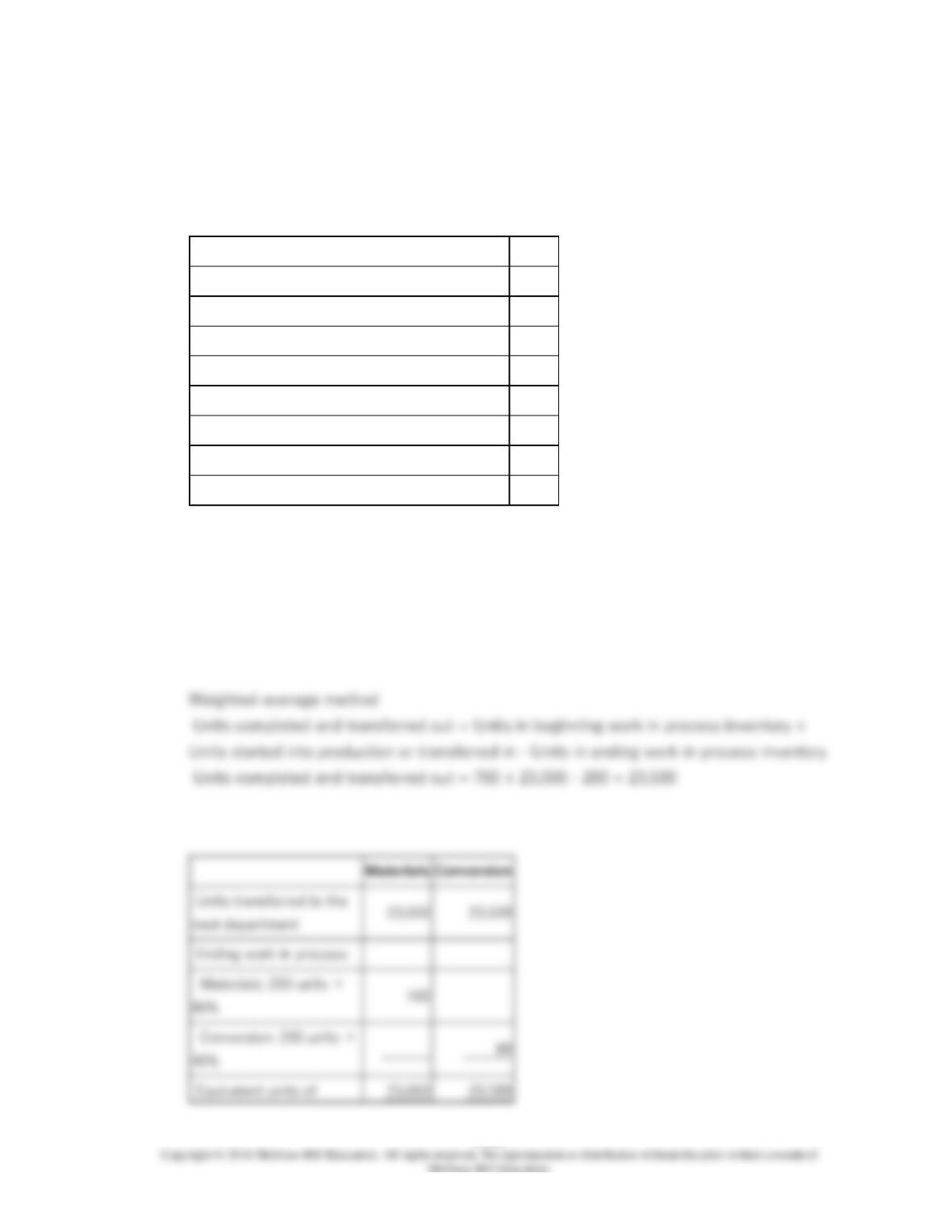

Carver Inc. uses the weighted-average method in its process costing system. The

following data concern the operations of the company’s first processing department for a

recent month.

Work in process, beginning:

Units in process

700

Percent complete with respect to materials

50%

Percent complete with respect to conversion

40%

Units started into production during the month

23,000

Work in process, ending:

Units in process

200

Percent complete with respect to materials

80%

Percent complete with respect to conversion

40%

Ending work in process:

Required:

Using the weighted-average method, determine the equivalent units of production for

materials and conversion costs.

4-257

4-258

109.

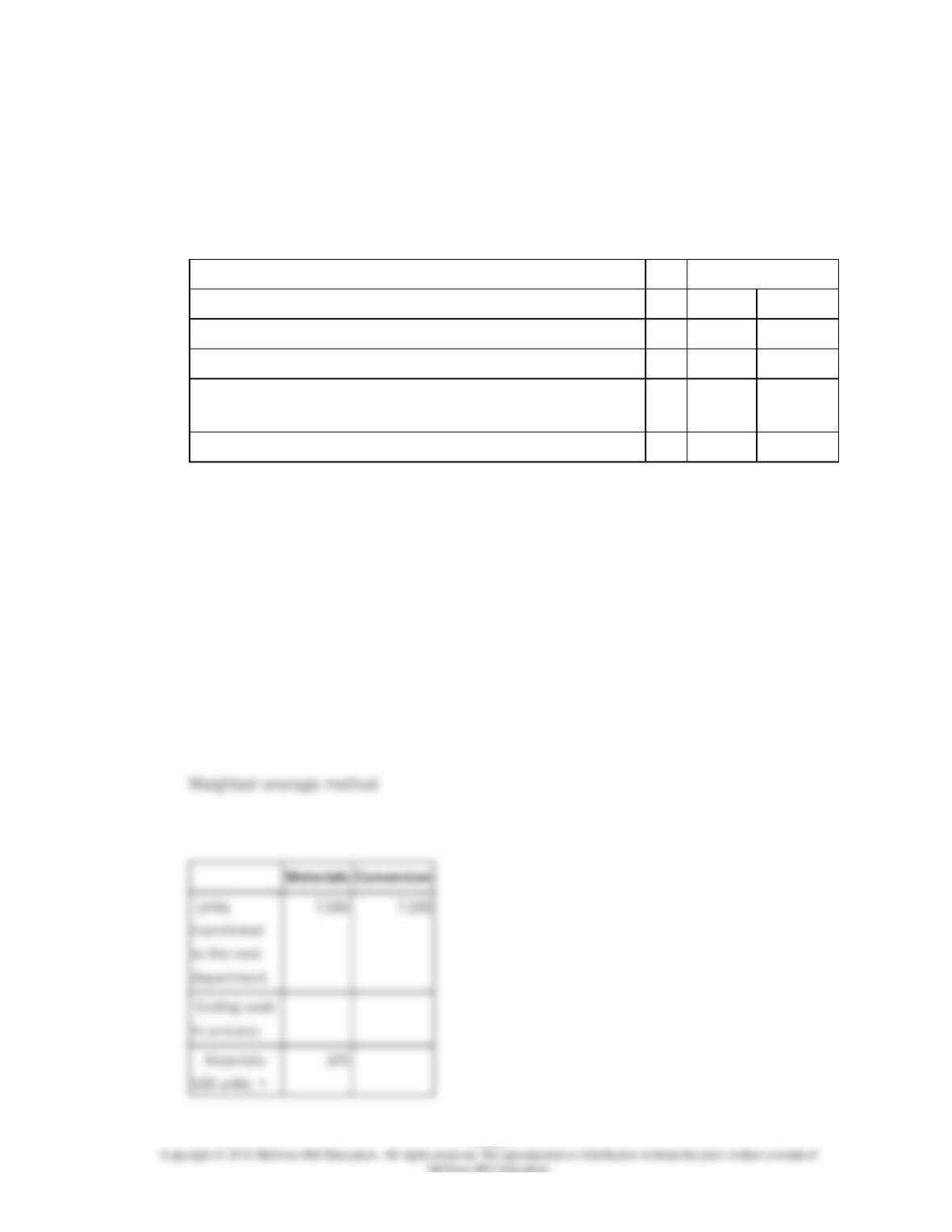

Jordon Corporation uses the weighted-average method in its process costing. The

following data pertain to its Materials Preparation Department for November.

Units in process, November 1: materials 80% complete, conversion 25% complete

800

Units started into production during November

6,300

Units completed and transferred to the next department

5,100

Units in process, November 30: materials 80% complete, conversion 25% complete

2,000

Work in process, ending:

Required:

Determine the equivalent units of production for the Materials Preparation Department

for November using the weighted-average method.

4-259

110.

Chargualaf Corporation uses the weighted-average method in its process costing. The

following data pertain to its Assembly Department for September.

Percent Complete

Units

Materials

Conversion

Work in process, September 1

400

60%

30%

Units started into production during September

9,100

Units completed during September and transferred to the next

department

8,600

Work in process, September 30

900

85%

25%

Units transferred to the next department

Ending work in process:

Equivalent units of production

Required:

Compute the equivalent units of production for both materials and conversion costs for

the Assembly Department for September using the weighted-average method.

4-260

111.

The following data have been provided by Allton Corporation, which uses the weighted-

average method in its process costing. The data are for the company’s Shaping

Department for October.

Percent Complete

Units

Materials

Conversion

Work in process, October 1

200

65%

45%

Units started into production during October

7,800

Units completed during October and transferred to the next

department

7,500

Work in process, October 31

500

65%

45%

Materials

Conversion

Ending work

Required:

Compute the equivalent units of production for both materials and conversion costs for the

Shaping Department for October using the weighted-average method.

4-261

4-262

112.

Barker Inc. uses the weighted-average method in its process costing system. The

following data concern the operations of the company’s first processing department for a

recent month.

Work in process, beginning:

Units in process

800

Percent complete with respect to

materials

50%

Percent complete with respect to

conversion

20%

Costs in the beginning inventory:

Materials cost

$2,440

Conversion cost

$4,928

Units started into production during

the month

15,000

Units completed and transferred out

15,600

Costs added to production during the

month:

Materials cost

$96,470

Conversion cost

$476,362

Work in process, ending:

Units in process

200

Percent complete with respect to

materials

50%

Percent complete with respect to

conversion

90%

Required:

Using the weighted-average method:

a. Determine the equivalent units of production for materials and conversion costs.

b. Determine the cost per equivalent unit for materials and conversion costs.

c. Determine the cost of units transferred out of the department during the month.

d. Determine the cost of ending work in process inventory in the department.

4-265

4-266

113.

Able Inc. uses the weighted-average method in its process costing system. The following

data concern the operations of the company’s first processing department for a recent

month.

Work in process, beginning:

Units in process

300

Percent complete with respect to

materials

60%

Percent complete with respect to

conversion

30%

Costs in the beginning inventory:

Materials cost

$342

Conversion cost

$2,394

Units started into production during

the month

21,000

Units completed and transferred out

20,700

Costs added to production during the

month:

Materials cost

$44,136

Conversion cost

$546,750

Work in process, ending:

Units in process

600

Percent complete with respect to

materials

80%

Percent complete with respect to

conversion

30%

Required:

a. Determine the equivalent units of production.

b. Determine the costs per equivalent unit.

c. Determine the cost of ending work in process inventory.

d. Determine the cost of the units transferred to the next department.

4-269

4-270

114.

Kamp Company uses the weighted-average method in its process costing. Information

about units processed during a recent month in the Curing Department follow:

Units

Conversion Percent Complete

Beginning work in process inventory

10,000

30%

Units started into production

150,000

Units completed and transferred out

140,000

Ending work in process inventory

20,000

40%

Units transferred to the next department

Ending work in process inventory:

Equivalent units of production

The beginning work in process inventory had $4,600 in conversion cost. During the month,

the Department incurred an additional $210,000 in conversion cost.

Required:

a. Determine the equivalent units of production for conversion for the month.

b. Determine the cost per equivalent unit of production for conversion for the month.

c. Determine the conversion cost assigned to the ending work in process inventory.

d. Determine the total conversion cost transferred out during the month.

4-271