2-195

106.

On August 1, Shead Corporation had $35,000 of raw materials on hand. During the month,

the company purchased an additional $56,000 of raw materials. During August, $69,000 of

raw materials were requisitioned from the storeroom for use in production. These raw

materials included both direct and indirect materials. The indirect materials totaled $6,000.

Prepare journal entries to record these events. Use those journal entries to answer the

following questions:

The credits to the Manufacturing Overhead account as a consequence of the raw

materials transactions in August total:

2-196

107.

Dillon Corporation applies manufacturing overhead to jobs using a predetermined

overhead rate of 75% of direct labor cost. Any under or overapplied manufacturing

overhead cost is closed out to Cost of Goods Sold at the end of the month. During May,

the following transactions were recorded by the company:

Raw materials (all direct materials):

Purchased during the month

$38,000

Used in production

$35,000

Labor:

Direct labor-hours worked during the

month

3,150

Direct labor cost incurred

$30,000

Manufacturing overhead cost incurred

(total)

$24,500

Inventories:

Raw materials (all direct), May 31

$8,000

Work in process, May 1

$9,000

Work in process, May 31

$12,000*

*Contains $4,400 in direct labor cost.

Used in production

Purchases

The balance on May 1 in the Raw Materials inventory account was:

2-197

2-198

108.

Dillon Corporation applies manufacturing overhead to jobs using a predetermined

overhead rate of 75% of direct labor cost. Any under or overapplied manufacturing

overhead cost is closed out to Cost of Goods Sold at the end of the month. During May,

the following transactions were recorded by the company:

Raw materials (all direct materials):

Purchased during the month

$38,000

Used in production

$35,000

Labor:

Direct labor-hours worked during the

month

3,150

Direct labor cost incurred

$30,000

Manufacturing overhead cost incurred

(total)

$24,500

Inventories:

Raw materials (all direct), May 31

$8,000

Work in process, May 1

$9,000

Work in process, May 31

$12,000*

*Contains $4,400 in direct labor cost.

The amount of direct materials cost in the May 31 Work in Process inventory account

was:

2-199

2-200

109.

Dillon Corporation applies manufacturing overhead to jobs using a predetermined

overhead rate of 75% of direct labor cost. Any under or overapplied manufacturing

overhead cost is closed out to Cost of Goods Sold at the end of the month. During May,

the following transactions were recorded by the company:

Raw materials (all direct materials):

Purchased during the month

$38,000

Used in production

$35,000

Labor:

Direct labor-hours worked during the

month

3,150

Direct labor cost incurred

$30,000

Manufacturing overhead cost incurred

(total)

$24,500

Inventories:

Raw materials (all direct), May 31

$8,000

Work in process, May 1

$9,000

Work in process, May 31

$12,000*

*Contains $4,400 in direct labor cost.

The entry to dispose of the under or overapplied manufacturing overhead cost for the

2-201

month would include:

2-202

110.

Dillon Corporation applies manufacturing overhead to jobs using a predetermined

overhead rate of 75% of direct labor cost. Any under or overapplied manufacturing

overhead cost is closed out to Cost of Goods Sold at the end of the month. During May,

the following transactions were recorded by the company:

Raw materials (all direct materials):

Purchased during the month

$38,000

Used in production

$35,000

Labor:

Direct labor-hours worked during the

month

3,150

Direct labor cost incurred

$30,000

Manufacturing overhead cost incurred

(total)

$24,500

Inventories:

Raw materials (all direct), May 31

$8,000

Work in process, May 1

$9,000

Work in process, May 31

$12,000*

*Contains $4,400 in direct labor cost.

The Cost of Goods Manufactured for May was:

Direct materials

$35,000

Direct labor

2-203

111.

Echo Corporation uses a job-order costing system and applies overhead to jobs using a

predetermined overhead rate. During the year the company’s Finished Goods inventory

account was debited for $360,000 and credited for $338,800. The ending balance in the

Finished Goods inventory account was $36,600. At the end of the year, manufacturing

overhead was overapplied by $15,900.

The balance in the Finished Goods inventory account at the beginning of the year was:

2-204

112.

Echo Corporation uses a job-order costing system and applies overhead to jobs using a

predetermined overhead rate. During the year the company’s Finished Goods inventory

account was debited for $360,000 and credited for $338,800. The ending balance in the

Finished Goods inventory account was $36,600. At the end of the year, manufacturing

overhead was overapplied by $15,900.

If the applied manufacturing overhead was $169,300, the actual manufacturing overhead

cost for the year was:

2-205

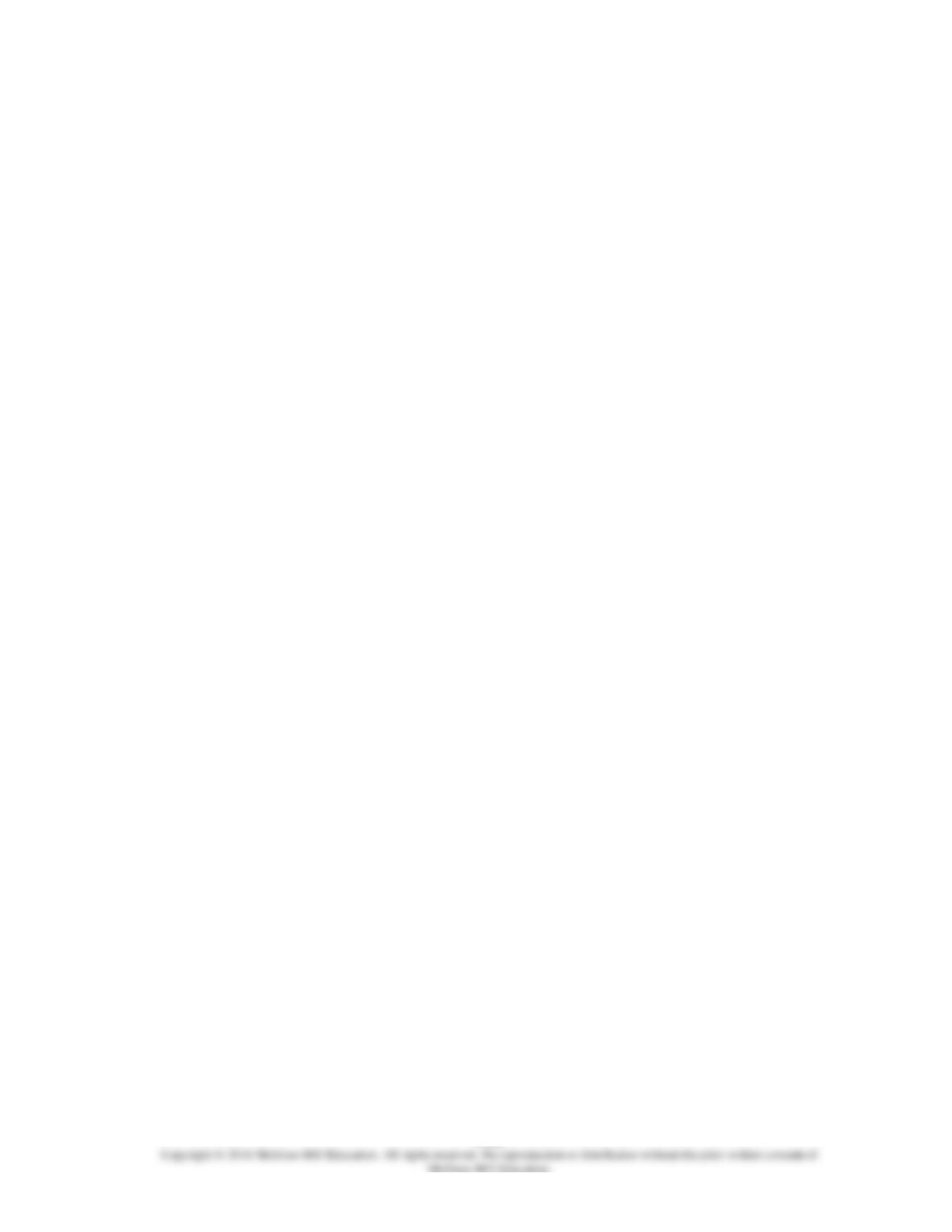

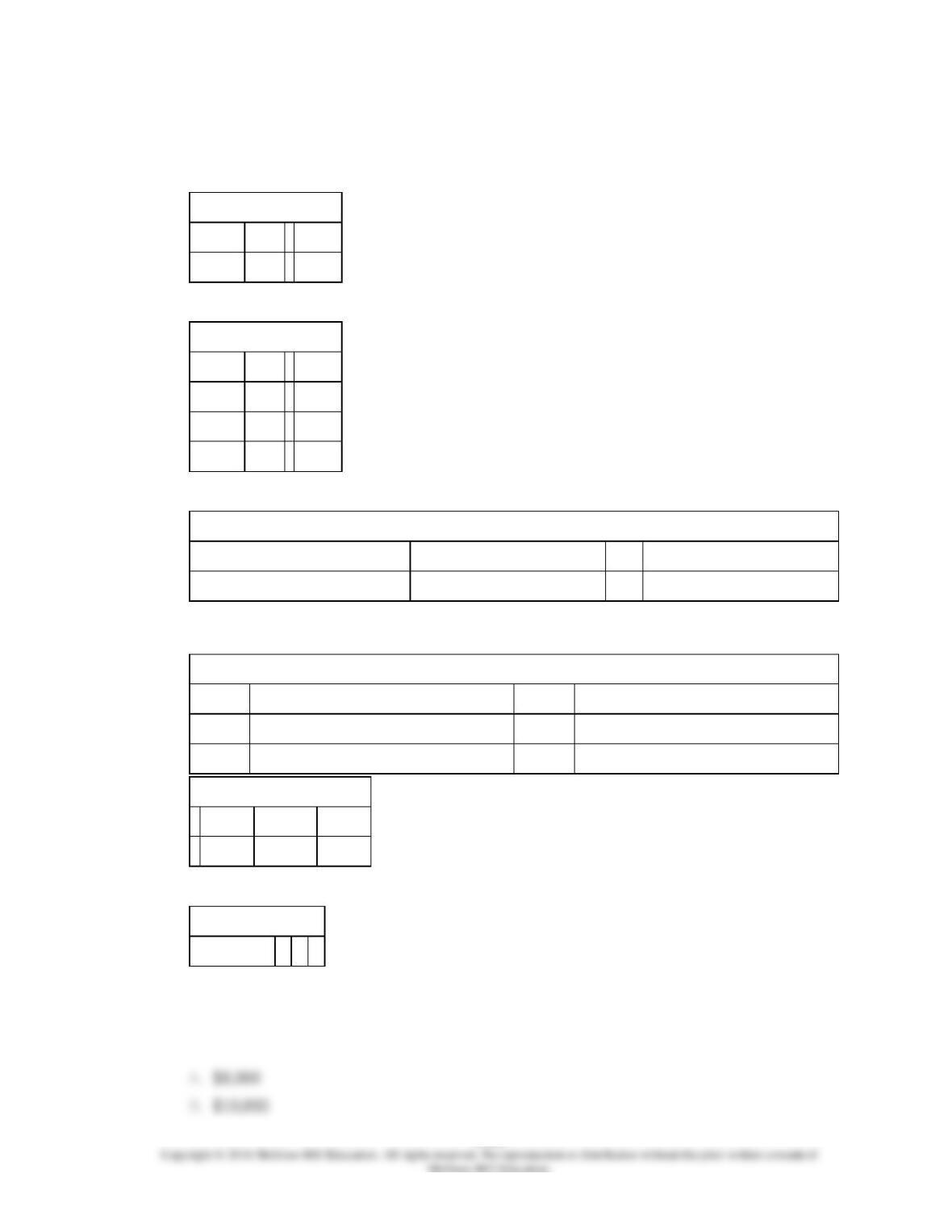

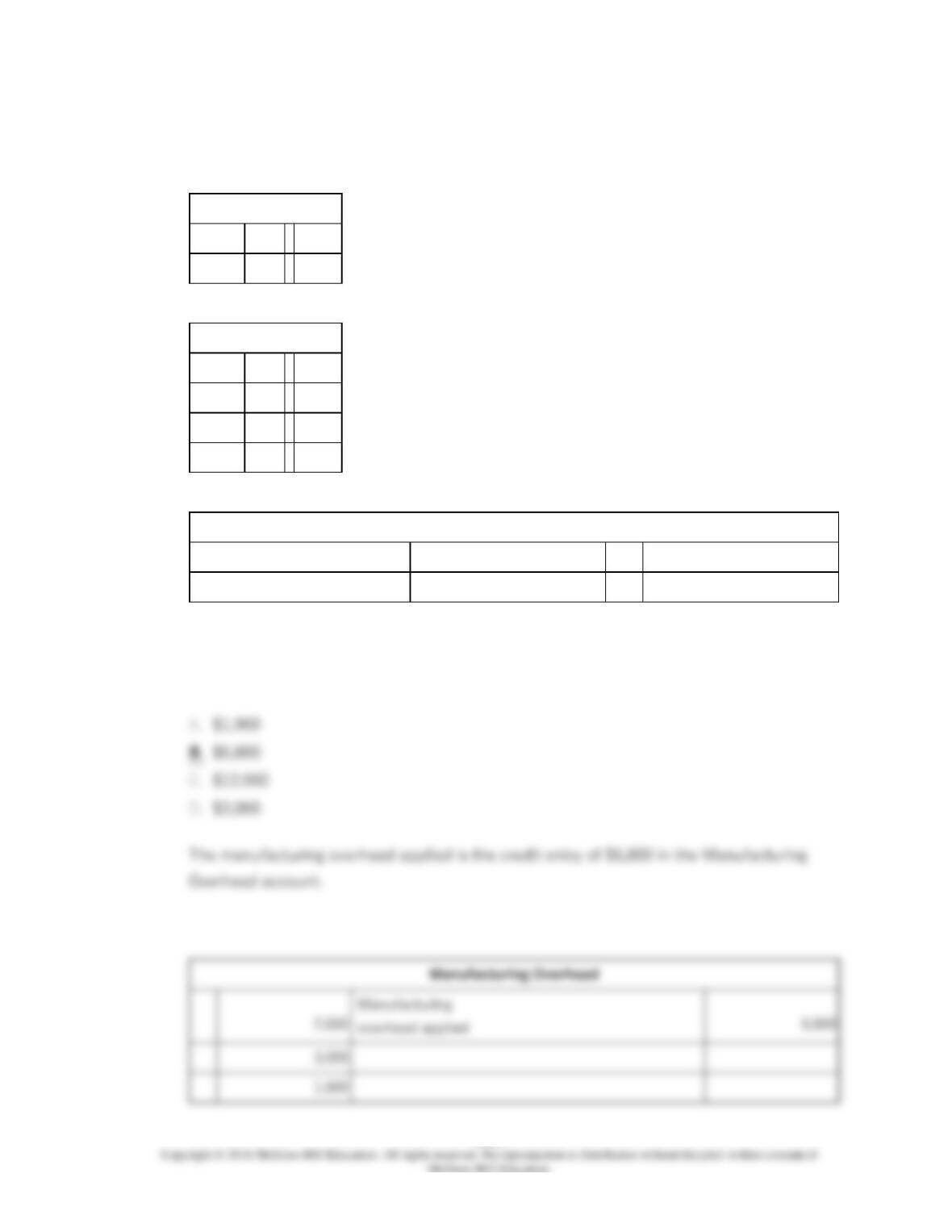

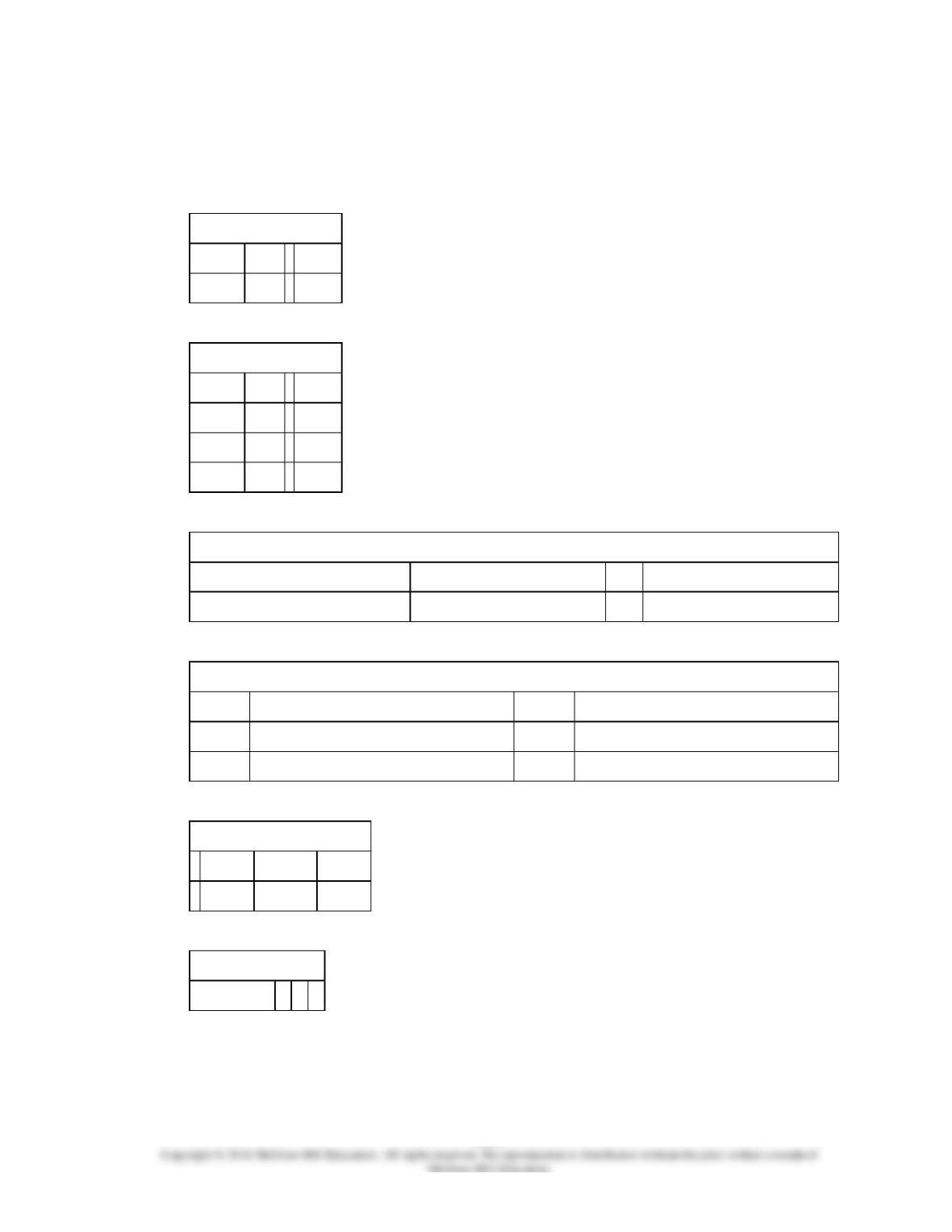

113.

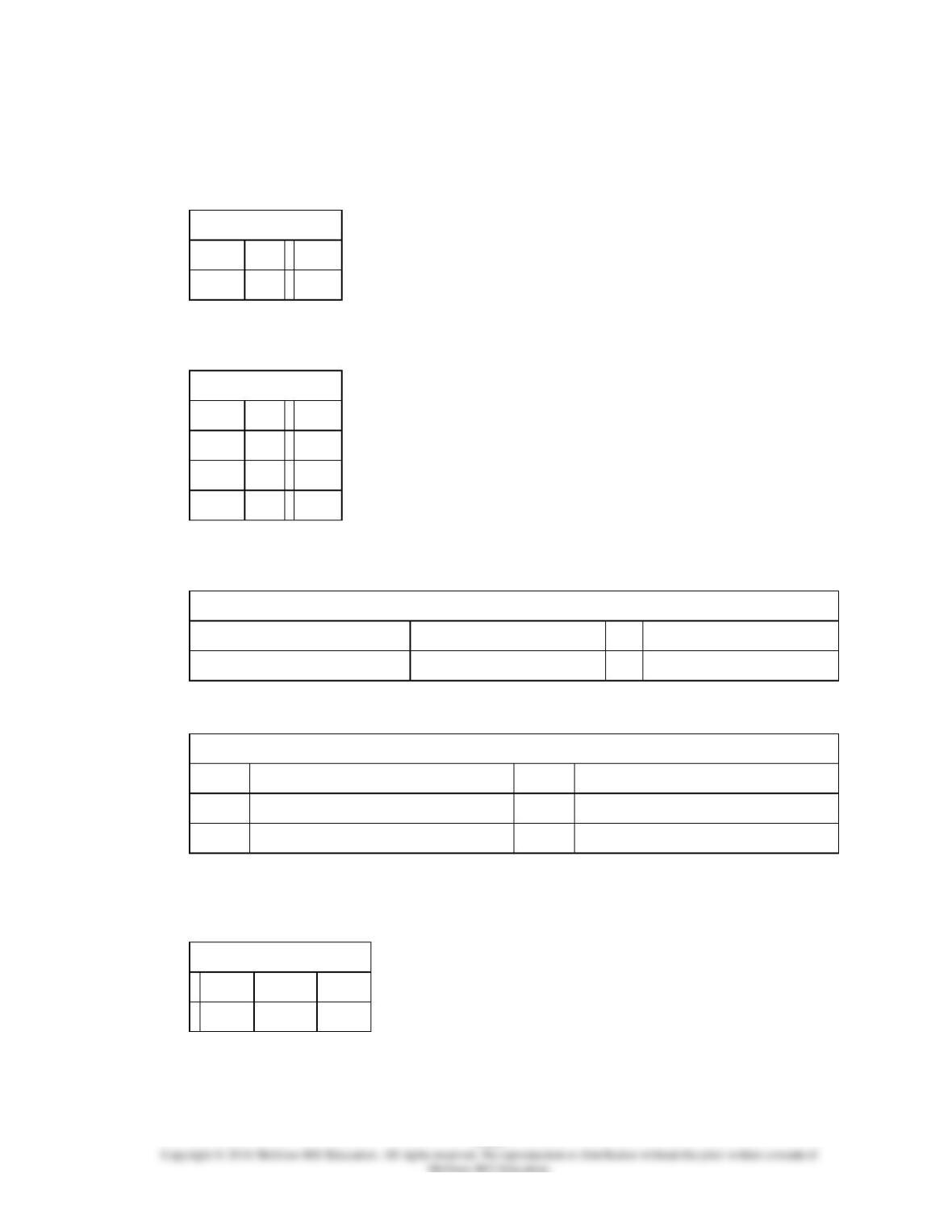

The following partially completed T-accounts summarize transactions for Farwest

Corporation during the year:

Raw Materials

Beg Bal

4,700

10,000

6,900

Work in Process

Beg Bal

4,600

26,300

7,400

8,000

6,800

Finished Goods

Beg Bal

1,900

22,900

26,300

Manufacturing Overhead

2,600

6,800

3,000

1,900

Wages & Salaries Payable

12,300

Beg Bal

1,400

11,000

2-206

Cost of Goods Sold

22,900

The Cost of Goods Manufactured was:

2-207

114.

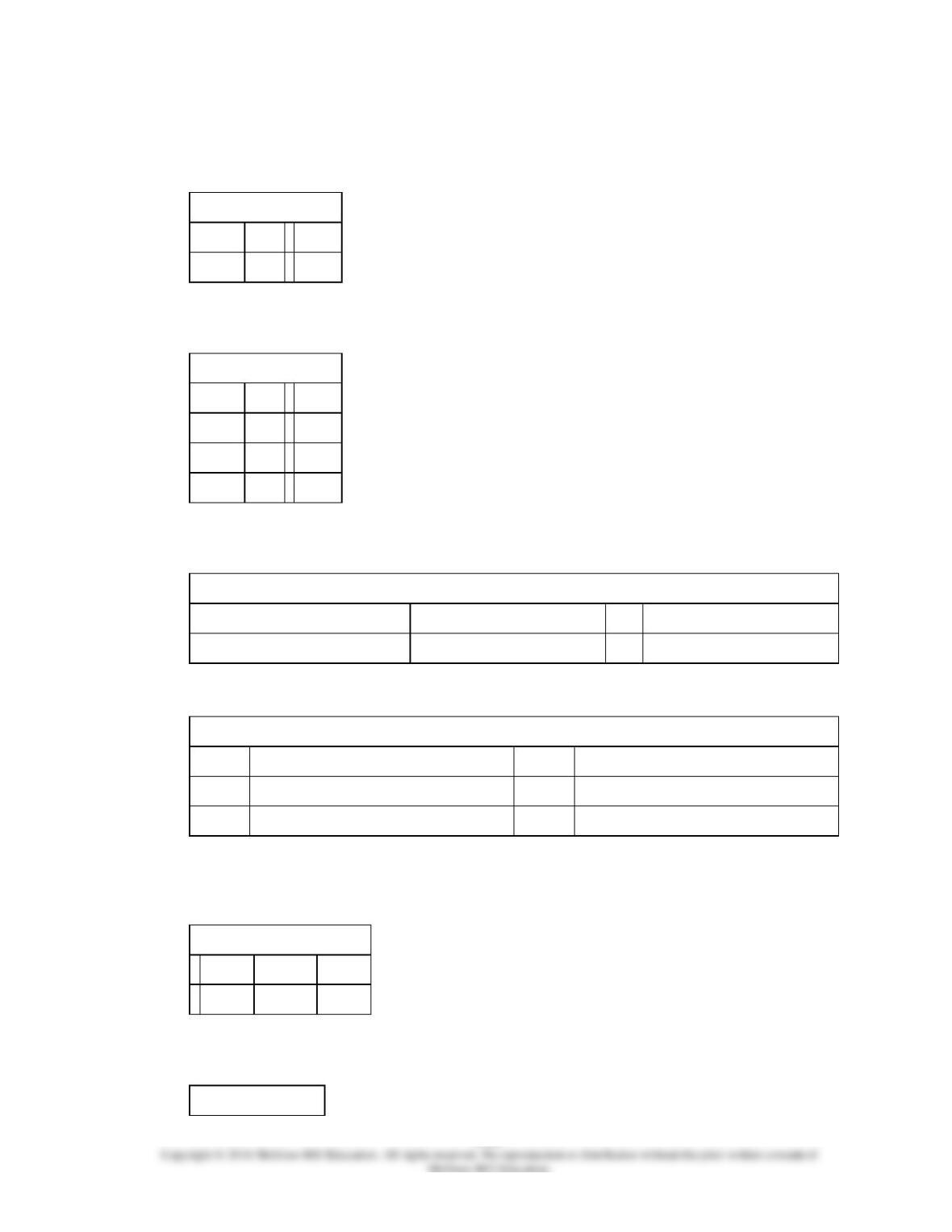

The following partially completed T-accounts summarize transactions for Farwest

Corporation during the year:

Raw Materials

Beg Bal

4,700

10,000

6,900

Work in Process

Beg Bal

4,600

26,300

7,400

8,000

6,800

Finished Goods

Beg Bal

1,900

22,900

26,300

Manufacturing Overhead

2,600

6,800

3,000

1,900

Wages & Salaries Payable

12,300

Beg Bal

1,400

11,000

Cost of Goods Sold

22,900

The direct labor cost was:

2-209

2-210

115.

The following partially completed T-accounts summarize transactions for Farwest

Corporation during the year:

Raw Materials

Beg Bal

4,700

10,000

6,900

Work in Process

Beg Bal

4,600

26,300

7,400

8,000

6,800

Finished Goods

Beg Bal

1,900

22,900

26,300

Manufacturing Overhead

2,600

6,800

3,000

1,900

Wages & Salaries Payable

12,300

Beg Bal

1,400

11,000

Cost of Goods Sold

22,900

The direct materials cost was:

2-211

2-212

116.

The following partially completed T-accounts summarize transactions for Farwest

Corporation during the year:

Raw Materials

Beg Bal

4,700

10,000

6,900

Work in Process

Beg Bal

4,600

26,300

7,400

8,000

6,800

Finished Goods

Beg Bal

1,900

22,900

26,300

The manufacturing overhead applied was:

2-213

2-214

117.

The following partially completed T-accounts summarize transactions for Farwest

Corporation during the year:

Raw Materials

Beg Bal

4,700

10,000

6,900

Work in Process

Beg Bal

4,600

26,300

7,400

8,000

6,800

Finished Goods

Beg Bal

1,900

22,900

26,300

Manufacturing Overhead

2,600

6,800

3,000

1,900

Wages & Salaries Payable

12,300

Beg Bal

1,400

11,000

Cost of Goods Sold

22,900

The manufacturing overhead was: