Archives

Accounting Appendix A Homework An interest rate swap exchanges fixed interest payments for floating

Appendix A Derivatives QUESTIONS FOR REVIEW OF KEY TOPICS Question A–1 These instruments “derive” their values or contractually required cash flows from some other security or index. Question A–2 The FASB has taken the position that the income effects of […]

Accounting Appendix A Homework The Entries Still Would Be Interest Expense

Problem A–1 (continued) Requirement 6 Income Statement + (−) 2016 (8,000) Interest expense (1,000) Interest expense (1,759) Holding loss—interest rate swap 1,759 Holding gain—hedged note (9,000) Net effect—same as floating interest payment on swap 2017 (8,000) Interest expense 1,000 Interest […]

Accounting Chapter 01 Homework Environment And Theoretical Structure Financial Accounting

Alternate Exercises and Problems 1–1 Chapter 1 Environment and Theoretical Structure of Financial Accounting EXERCISES Exercise 1-1 Requirement 1 Haskins and Price Operating Cash Flow Year 1 Year 2 Cash collected $330,000 $450,000 Cash disbursements: Payment of rent (60,000) – […]

Accounting Chapter 02 Homework Concluded Requirement Interest

2. – 15,000 (cash) + 60,000 (equipment) + 45,000 (note payable) 3. + 270,000 (inventory) + 270,000 (accounts payable) 4. + 360,000 (accounts receivable) + 360,000 (revenue) – 210,000 (inventory) – 210,000 (expense) 5. – 20,000 (cash) – 20,000 (expense) […]

Accounting Chapter 03 Homework Sale Equipment For Cash No Gain Loss

Alternate Exercises and Problems 3–1 Chapter 3 The Balance Sheet and Financial Disclosures EXERCISES Exercise 3-1 1. b Note receivable, due in 2 years 10. a Inventories 2. a Accounts receivable 11. d Goodwill 3. –c Accumulated depreciation 12. f […]

Accounting Chapter 04 Homework Receipt Principal Note Receivable Payment Cash Dividends

Alternate Exercises and Problems 4–1 Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows EXERCISES Exercise 4-1 Requirement 1 APEX COMPUTER CORPORATION Income Statement For the Year Ended December 31, 2016 Revenues and gains: Sales ……………………………………………………….. […]

Accounting Chapter 05 Homework Happy would allocate the total selling price of the package

Alternate Exercises and Problems 5–1 Chapter 5 Revenue Recognition and Profitability Analysis EXERCISES Exercise 5–1 Happy first must identify each performance obligation’s share of the sum of the stand-alone selling prices of all performance obligations: Patio: $3,400 = 85% $3,400 […]

Accounting Chapter 05 Homework Note Also Can Calculate Gross Profit Directly

5–12 Intermediate Accounting, 8/e PROBLEMS Problem 5-1 Requirement 1 a. Number of performance obligations in the contract: 2. The unlimited access to facilities and classes for one year is one performance obligation. Because the discount voucher provides a material right […]

Accounting Chapter 06 Homework Present Value Ordinary Annuity 1 N From

* Future value of $1: n=10, i=8% (from Table 1) 2. FV = $30,000 x 3.20714* = $96,214 * Future value of $1: n=20, i=6% (from Table 1) 3. FV = $40,000 x 17.44940* = $697,976 * Future value of […]

Accounting Chapter 07 Homework Corrected Cash Balance Step

Sales revenue …………………………………………………….. 128,000 April 16, 2016 Cash (99% x $128,000) ……………………………………………… 126,720 Sales discounts (1% x $128,000) ………………………………… 1,280 Accounts receivable ……………………………………………. 128,000 Sales revenue …………………………………………………….. 128,000 May 6, 2016 Cash …………………………………………………………………….. 128,000 Accounts receivable ……………………………………………. 128,000 Alternate Exercises […]

Accounting Chapter 08 Homework Materials purchased f.o.b. shipping point on 12/28

Inventory 16 Freight-in 16 Accounts payable 16 Accounts payable 16 Returns Accounts payable 6 Accounts payable 6 Inventory 6 Purchase returns 6 Purchase returns 6 Inventory (beginning) 112 Purchases 265 Freight-in 16 Cost of goods sold: Beginning inventory $112 Purchases […]

Accounting Chapter 09 Homework Retained Earnings Millions 16 The

Alternate Exercises and Problems 9–1 Chapter 9 Inventories: Additional Issues EXERCISES Exercise 9-1 Requirement 1 (1) (2) Product Cost NRV Inventory Value [Lower of (1) or (2)] Gloves $360,000 $300,000 $300,000 Bats 260,000 320,000 260,000 Balls 150,000 125,000 125,000 Uniforms […]

Accounting Chapter 1 Objective 0101 topic Area Cash Versus Accrual Accounting blooms

Chapter 1 Environment and Theoretical Structure of Financial Accounting 114. Listed below are five terms followed by a list of phrases that describe or characterize each of the terms. Match each phrase with the correct number code for the term. […]

Accounting Chapter 1 Supplemental Schedules And Tables That Report More

Chapter 1 Environment and Theoretical Structure of Financial Accounting Answer: c Level of Learning: 1 Easy Learning Objective: 01-07 Topic Area: Objective, qualitative characteristics of financial reporting Blooms: Understand AACSB: Reflective thinking AICPA: BB Critical Thinking 75. Surefeet Corporation changed […]

Accounting Chapter 1 When There Agreement Between Measure Description

Chapter 1 Environment and Theoretical Structure of Financial Accounting True/False Questions 1. The primary function of financial accounting is to provide relevant financial information to parties external to business enterprises. Answer: True Level of Learning: 1 Easy Learning Objective: 01-01 […]

Accounting Chapter 10 All Rights Reserved Nore production Distribution Without The

Chapter 10 Property, Plant, and Equipment and Intangible Assets: Acquisition and Disposition Learning Objective: 10-06 Topic Area: Exchanges Blooms: Apply AACSB: Knowledge Application AICPA: FN Measurement Feedback: Equipment-new ($80,000 – 12,000) 68,000 Cash 12,000 Equipment-old (book value) 75,000 Gain 5,000 […]

Accounting Chapter 10 Company recorded Pretax Charge 1789 Million 1193 Million

Chapter 10 Property, Plant, and Equipment and Intangible Assets: Acquisition and Disposition Level of Learning: Medium Learning Objective: 10-04 Topic Area: Noncash acquisitions ‒ Donated assets Blooms: Apply AACSB: Knowledge Application AICPA: FN Measurement 111. On March 15, 2016, Ellis […]

Accounting Chapter 10 Costs incurred after discovery of a natural resource

Chapter 10 Property, Plant, and Equipment and Intangible Assets: Acquisition and Disposition True/False Questions 1. Property, plant, and equipment and intangible assets are long-term, revenue producing assets. Answer: True Level of Learning: Easy Learning Objective: 10-01 Topic Area: Types of […]

Accounting Chapter 10 Homework Communication Skills Addition Communication Case 1011 Judgment

RESEARCH AND DEVELOPMENT ➢ All research and development costs are charged to expense in the period incurred. R&D costs entail a high degree of uncertainty of future benefits. It is difficult to match R&D costs with future revenues. […]

Accounting Chapter 10 Homework English Sentences Grammatically Clear And Well

Case 10–4 (concluded) Requirement 5 The three steps used to determine the amount of interest capitalized during a period are: 1. Determine the average accumulated expenditures for the period. 2. Multiply average accumulated expenditures by the appropriate interest rate(s). 3. […]

Accounting Chapter 10 Homework Gain or Loss From Plant Asset Disposals

Student Name: Class: Requirement 1: Balance Balance 12/31/2015 Increase Decrease 12/31/2016 350,000$ 438,000$ 788,000$ 180,000 180,000 35,000 438,000$ Correct! 260,000$ 27,000 287,000$ Correct! 3,750$ 15,250 19,000$ Correct! Invoice cost Installation cost Cost recorded for new automobile 12/31/2016: Fair value of […]

Accounting Chapter 10 Homework Illustration 1014 Retirements And Abandonments Are

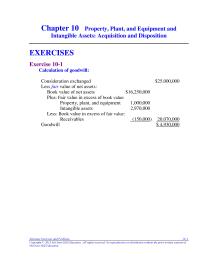

GOODWILL (continued) The Smithson Corporation acquired all of the outstanding common stock of the Rider Corporation in exchange for $18 million in cash. Smithson assumed all of Rider’s long-term debt which had a fair value of $12 million at date […]

Accounting Chapter 10 Homework No reproduction or distribution without the prior written consent of

Property, plant, and equipment 1,000,000 Intangible assets 2,970,000 Less: Book value in excess of fair value: Receivables (150,000) 20,070,000 Goodwill $ 4,930,000 Alternate Exercises and Problems 10–1 Chapter 10 Property, Plant, and Equipment and Intangible Assets: Acquisition and Disposition EXERCISES […]

Accounting Chapter 10 Homework Present Value 1 I8 From Table Record

Exercise 10–30 Requirement 1 According to U.S. GAAP, the following costs would be expensed as R&D: Research for new formulas $2,425,000 Development of a new formula 1,600,000 Total $4,025,000 The legal and filing fees are capitalized as an intangible asset. […]

Accounting Chapter 10 Homework Requires The Capitalization In process Ramp’d Indefinite

C CH HA AP PT TE ER R 1 10 0 P PR RO OP PE ER RT TY Y, , P PL LA AN NT T, , A AN ND D E EQ QU UI IP PM ME EN […]

Accounting Chapter 10 Homework Instead, IFRS requires that government grants be recognized in income

Exercise 10–9 Requirement 1 Tractor ($5,000 cash + 18,783† present value of note) …………. 23,783 Discount on note payable (difference) ……………………….. 6,217 Cash …………………………………………………………………. 5,000 Note payable (face amount) ……………………………………. 25,000 † Present value of note payment: PV = $25,000 […]

Accounting Chapter 10 Homework No reproduction or distribution without the prior written consent

Problem 10–8 (concluded) Requirement 3 If the exchange lacked commercial substance, no gain is recognized. Book value of old land + cash given = Initial value of new land $500,000 + 50,000 = $550,000 Journal entry (not required): New land […]

Accounting Chapter 10 Homework Research and development costs incurred to internally develop an intangible

Question 10–1 The difference between tangible and intangible long-lived, revenue-producing assets is that intangible assets lack physical substance and they primarily refer to the ownership of rights. Question 10–2 The cost of property, plant, and equipment and intangible assets includes […]

Accounting Chapter 10 Insurance After Equipment Placed Service 1200 Installation

Chapter 10 Property, Plant, and Equipment and Intangible Assets: Acquisition and Disposition Topic Area: Types of assets Topic Area: Costs to be capitalized Topic Area: Noncash acquisitions ‒ Deferred payments Topic Area: Dispositions Topic Area: Exchanges Topic Area: Self-constructed assets […]

Accounting Chapter 11 Blooms Understand Reflective Thinking

Chapter 11 Property, Plant, and Equipment and Intangible Assets: Utilization and Impairment 98. Listed below are five terms followed by a list of phrases that describe or characterize each of the terms. Match each phrase with the number for the […]

Accounting Chapter 11 Equipment And Intangible Assets utilization And Impairment book Value

Chapter 11 Property, Plant, and Equipment and Intangible Assets: Utilization and Impairment True/False Questions 1. The three factors in cost allocation of a depreciable asset are service life, allocation base, and allocation method. Answer: True Level of Learning: 1 Easy […]

Accounting Chapter 11 Homework Buildings Including Leasehold Improvements Are Generally Depreciated

IMPAIRMENT OF VALUE – A SUMMARY Type of Asset When to Test for Impairment Impairment Test To Be Held and Used: Tangible and finite- life intangible assets book value may not be recoverable. (undiscounted sum of estimated future cash flows […]

Accounting Chapter 11 Homework During The Three year Period Accumulated Depreciation Was

Sum-of-the-digits is {[8 (8 + 1)]÷2} = 36 2016 $220,000 x 8/36 = $48,889 2017 $220,000 x 7/36 = 42,778 Straight-line rate is 12.5% (1 ÷ 8 years) x 2 = 25% DDB rate 2016 $240,000 x 25% = $60,000 […]

Accounting Chapter 11 Homework Intermediate Accounting 8e Measuring Cost Allocation

CHAPTER 11 PROPERTY, PLANT, AND EQUIPMENT AND INTANGIBLE ASSETS: UTILIZATION AND IMPAIRMENT Overview This chapter completes our discussion of accounting for property, plant, and equipment and intangible assets. We address the allocation of the cost of these assets to the […]

Accounting Chapter 11 Homework Machine Selling Price 2016 Depreciation Through Date

Student Name: Class: Balance Balance 12/31/2015 Increase Decrease 12/31/2016 Land (1) 175,000$ 312,500$ –$ 487,500$ Land improvements – 192,000 – 192,000 Market price 50$ Fair value of shares 1,250,000$ Correct! (1) Plant facility acquired from King 1/6/2016 – allocation to […]

Accounting Chapter 11 Homework The Approximate Average Service Life Caterpillars Depreciable

fair value less cost to sell. An impairment loss is recognized for any write-down to fair value less cost to sell. Solutions Manual, Vol.1, Chapter 11 11–93 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without […]

Accounting Chapter 11 Homework The loss is the difference between book value and the recoverable amount

Problem 11–2 (continued) Requirement 2 CORD COMPANY Depreciation and Amortization Expense For the Year Ended December 31, 2016 Land Improvements: Cost $192,000 Straight-line rate (1 ÷ 12 years) x 8 1/3% Annual depreciation 16,000 Depreciation on land improvements for 2016: […]

Accounting Chapter 11 Homework When Impairment Loss Recognized The Carrying Amount

INTERNATIONAL FINANCIAL REPORTING STANDARDS Valuation of Intangible Assets. IAS No. 38 allows a company to value an intangible asset subsequent to initial valuation at (1) cost less accumulated amortization or (2) fair value, if fair value can be determined by […]

Accounting Chapter 11 Homework Because book value (£220 million) exceeds this amount, a loss is indicated

Exercise 11–24 Requirement 1 IFRS requires an impairment loss to be recognized when an asset’s book value exceeds the higher of the asset’s value–in-use (present value of estimated future cash flows) and fair value less costs to sell. In this […]

Accounting Chapter 11 Homework If a revaluation surplus account relating to the same asset had existed

Exercise 11–3 (concluded) 5. Units-of-production: $115,000 – 5,000 = $.50 per unit depreciation rate 220,000 units 2016 10,000 units x $.50 = $ 5,000 2017 25,000 units x $.50 = $12,500 Exercise 11–4 Building depreciation: $5,000,000 – 200,000 = $160,000 […]

Accounting Chapter 11 Homework Information is material if it can have an effect on a decision made by users

Problem 11–13 Requirement 1 Hecala’s cost of the mineral mine is $13,721,871, determined as follows: Mining site $10,000,000 Development costs 3,200,000 Restoration costs 521,871 † $13,721,871 † $600,000 x 30% = $180,000 700,000 x 30% = 210,000 800,000 x 40% […]

Accounting Chapter 11 Homework This amount is the difference between the initial value of

Question 11–1 The terms depreciation, depletion, and amortization all refer to the process of allocating the cost of property, plant, and equipment and finite-life intangible assets to periods of use. The only difference between the terms is that they refer […]

Accounting Chapter 11 Which The Following Types Subsequent Expenditures Normally

Chapter 11 Property, Plant, and Equipment and Intangible Assets: Utilization and Impairment Intermediate Accounting, Eighth Edition, Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 11–21 59. Granite Enterprises […]

Accounting Chapter 11 Wicker Corporation Operates Manufacturing Plant California

Chapter 11 Property, Plant, and Equipment and Intangible Assets: Utilization and Impairment AACSB: Analytical thinking AACSB: Communication AICPA: BB Critical thinking AICPA: FN Measurement 123. Gonzaga Company has used the double-declining-balance method for depreciation since it started business in 2012. […]

Accounting Chapter 12 During 2016 Clor Recognized 80000 Net Income

Chapter 12 Investments 63. Unrealized holding gains and losses on securities available for sale would have the following effects on retained earnings: Gains Losses a. Increase No change b. No change Decrease c. No change No change d. Increase Decrease […]

Accounting Chapter 12 Homework Classification Depends 1 Whether The Investments Contractual

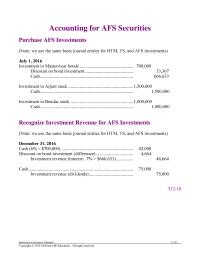

Accounting for AFS Securities Purchase AFS Investments (Note: we use the same basic journal entries for HTM, TS, and AFS investments) July 1, 2016 Investment in Masterwear bonds ……………………………………….. 700,000 Discount on bond investment …………………………………… 33,367 Cash ………………………………………………………………………. 666,633 Investment […]

Accounting Chapter 12 Homework Company Does Not Intend Sell The Impaired

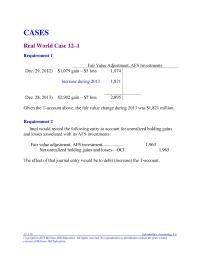

12–120 Intermediate Accounting, 8/e Real World Case 12–1 Requirement 1 Fair Value Adjustment, AFS Investments Dec. 29, 2012) $1,079 gain – $5 loss 1,074 Increase during 2013 1,821 Dec. 28, 2013) $2,902 gain – $7 loss 2,895 Given the T-account […]

Accounting Chapter 12 Homework Corporation Shares American Instruments Bonds Totals Dec 31

Problem 12–4 (concluded) Then, to record it at fair value, we increase the investment by $70 – 66.21 = $3.79 million: Fair value adjustment ………………………… ……….. 3.79 Net unrealized holding gains and losses—I/S ($70 – 66.21) 3.79 Because these are […]

Accounting Chapter 12 Homework Donald Company Bonds Include Only Interest And

Problem 12–11 Requirement 1 (note: requirement 1 has the same answer as does P 12–10) Purchase ($ in millions) Investment in Lavery Labeling shares …………………………………… 324 Cash …………………………………………………………………………….. 324 Net income No entry Dividends Cash (10 million shares x $2) […]

Accounting Chapter 12 Homework Exercise 126 The Fasb Accounting Standards Codification

Brief Exercise 12–15 Because the drop in the market price of stock is considered to be other-than- temporary, LED records the impairment of $450,000 ($4.50 x 100,000 shares) and reclassifies previously recognized unrealized losses of $100,000 ($1.00 x 100,000 shares) […]

Accounting Chapter 12 Homework Footnote Disclosures About The Reliability The Inputs

C CH HA AP PT TE ER R 1 12 2 I In nv ve es st tm me en nt ts s Overview In this chapter we cover various approaches used to account for investments that companies make in […]

Accounting Chapter 12 Homework However Only The Credit Loss Component Recognized

Question 12–1 Investment securities are classified as “held–to–maturity,” “trading,” or “available-for-sale” securities. Question 12–2 Increases and decreases in the market value between the time a debt security is acquired and the day it matures to a prearranged maturity value are […]

Accounting Chapter 12 Homework Investment in NXS common shares

Student Name: Class: Debit Credit 28 2 30 «- Correct! Cash Loss on sale of investments Investment in Kansas Abstractors bonds 5.6 5.6 «- Correct! 44 44 «- Correct! 5.7 «- Correct! 5.6 0.1 3 3 «- Correct! Gain on […]

Accounting Chapter 12 Homework Moving from a negative $145 (Jan.1) to a positive $30 requires an increase of

Exercise 12–12 (continued) Requirement 2 Accumulated ($ in 000s) Unrealized Available-for-Sale Securities Cost Fair Value Gain (Loss) IBM shares—Dec. 31, 2016 $1,345 $1,275 $(70) Moving from a negative $145 (Jan.1) to a negative $70 requires an increase of $75: ——————————————————————————–———– […]

Accounting Chapter 12 Homework So to reclassify that unrealized loss, Bloom would reverse that entry.

So, net income will be decreased by $250,000, OCI by $150,000, and comprehensive income by $400,000. Solutions Manual, Vol.1, Chapter 12 12–61 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of […]

Accounting Chapter 12 Homework This Fact The Case Stated Media Generals

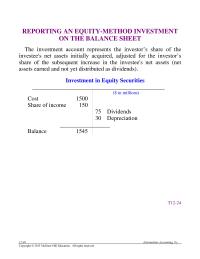

12-40 Intermediate Accounting, 8/e REPORTING AN EQUITY-METHOD INVESTMENT ON THE BALANCE SHEET The investment account represents the investor’s share of the investee’s net assets initially acquired, adjusted for the investor’s share of the subsequent increase in the investee’s net assets […]

Accounting Chapter 12 Homework Unlike for trading securities, unrealized holding gains and losses are not

Investment in Oracle bonds ………………………………………………… 200 Cash …………………………………………………………………………….. 200 Cash ………………………………………………………………………………… 3 Investment revenue ………………………………………………………… 3 Cash ………………………………………………………………………………… 10 Investment revenue ………………………………………………………… 10 Cash ………………………………………………………………………………… 205 Investment in Oracle bonds …………………………………………….. 200 Gain on sale of investments …………………………………………….. 5 Investment […]

Accounting Chapter 12 However All Market Value Changes Would Be reflected

Chapter 12 Investments Answer: 1) Insurance expense (difference) 81,000 Cash surrender value of life insurance ($70,000 – 56,000) 14,000 Cash (2016 premium) 95,000 2) Cash (death benefit) 6,000,000 Cash surrender value of life insurance (account balance) 70,000 Gain on life […]

Accounting Chapter 12 If the fair value of a held-to-maturity

Chapter 12 Investments Intermediate Accounting, Seventh Edition, © The McGraw-Hill Companies, Inc., 2016 12-41 xxx. Espana Corporation purchased $100,000 of Hales Inc. 6% bonds at par and classifies its investment as available for sale. Unfortunately, a combination of problems at […]

Accounting Chapter 12 Investment Short 80000 25 investment Revenue Dec Cash 24000

Chapter 12 Investments ACCUMULATED OTHER COMPREHENSIVE INCOME The components of accumulated other comprehensive income (loss) (“AOCI”) included in the accompanying consolidated balance sheets consist of the following: YEAR ENDED JUNE 30 2016 2015 2014 ($ in millions) Net unrealized investment […]

Accounting Chapter 12 Measurement 36 Ziggy Company Concluded That Investment Originally

Chapter 12 Investments True/False Questions 1. Securities classified as held to maturity could be reported as either current or long-term in a classified balance sheet, depending upon their maturity dates. Answer: True Level of Learning: 1 Easy Learning Objective: 12-01 […]

Accounting Chapter 13 Grossman Products Began Operations 2016 The

Chapter 13 Current Liabilities and Contingencies 109. Listed below are five terms followed by a list of phrases that describe or characterize each of the terms. Match each phrase with the number for the correct term. TERM PHRASE NUMBER 1. […]

Accounting Chapter 13 Homework A liability is accrued if it is both probable that a loss will

13–78 Intermediate Accounting, 8/e Communication Case 13–10 Suggested Grading Concepts and Grading Scheme: Content (80% ) 20 Identifies the situation as a change in estimate. The liability was originally (appropriately) estimated as $750,000. The final settlement indicates the estimate should […]

Accounting Chapter 13 Homework Company Seeking Civil Penalties And Injunctive Relief

CMA Exam Questions 1. b. If an enterprise intends to refinance short-term obligations on a long- term basis and demonstrates an ability to consummate the refinancing, the obligations should be excluded from current liabilities and classified as noncurrent. Under U.S. […]

Accounting Chapter 13 Homework Liability Refundable Deposits Sales Taxes Payable Accrued

Student Name: Class: Debit Credit 14,000,000 Maturity (January 31, 2017) 420,000 14,000,000 14,560,000 «- Correct! 14,560,000 «- Correct! 140,000 420,000 14,000,000 Interest payable Notes payable Cash Cash Interest revenue L & T Bank Interest receivable Notes receivable 140,000 Issuance of […]

Accounting Chapter 13 Homework Paid Sabbatical Leave Expense And Related Liability

Problem 13–12 (continued) Requirement 5 December 31, 2016 ($ in millions) Current Liabilities Accounts payable and accruals $ 43 6.5% bonds maturing on July 31, 2025, callable July 31, 2017 90 Current portion of 7% notes payable due May 2017 […]

Accounting Chapter 13 Homework Problem 131 Requirement Schilling Motors Cash

Cash ……………………………………………………… 6,000,000 Notes payable ………………………………………. 6,000,000 Interest expense ($6,000,000 x 14% x 4/12) …….. 280,000 Interest payable …………………………………… 280,000 Interest expense ($6,000,000 x 14% x 2/12) …….. 140,000 Interest payable (from adjusting entry) ………….. 280,000 Notes payable (face amount) […]

Accounting Chapter 13 Homework Professional Skills Development Activities The Following Are

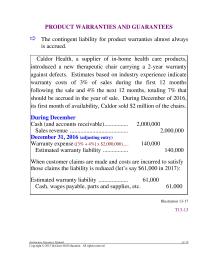

PRODUCT WARRANTIES AND GUARANTEES The contingent liability for product warranties almost always is accrued. Caldor Health, a supplier of in-home health care products, introduced a new therapeutic chair carrying a 2-year warranty against defects. Estimates based on industry experience […]

Accounting Chapter 13 Homework Such Disclosure Would Alert The Other Party

Exercise 13–8 Requirement 1 Cash …………………………………………………………….. 7,500 Deferred sales revenue ……………………………….. 7,500 Requirement 2 Cash …………………………………………………………….. 25,500 Liability—refundable deposits ……………………. 25,500 Requirement 3 Accounts receivable ……………………………………….. 856,000 Sales revenue ……………………………………………. 800,000 Sales taxes payable ([5% + 2%] x $800,000) ……… […]

Accounting Chapter 13 Homework The Low End The Range Accrued

Chapter 13 Current Liabilities and Contingencies QUESTIONS FOR REVIEW OF KEY TOPICS Question 13–1 A liability involves the past, the present, and the future. It is a present responsibility, to sacrifice assets in the future, caused by a transaction or […]

Accounting Chapter 13 Homework Most liabilities obligate the debtor to pay cash at specified times and

C CH HA AP PT TE ER R 1 13 3 C Cu ur rr re en nt t L Li ia ab bi il li it ti ie es s a an nd d C Co on nt ti […]

Accounting Chapter 13 Longterm Assets Until The Product Service Provided

Chapter 13 Current Liabilities and Contingencies True/False Questions 1. Some liabilities are not contractual obligations and may not be payable in cash. Answer: True Level of Learning: 1 Easy Learning Objective: 13–01 Topic Area: Characteristics of liabilities Blooms: Remember AACSB: […]

Accounting Chapter 13 The Following Facts Relate Gift Cards

Chapter 13 Current Liabilities and Contingencies Level of Learning: 2 Medium Learning Objective: 13–03 Topic Area: Advance collections – Deferred revenue Blooms: Analyze AACSB: Analytical thinking AICPA: FN Measurement 129. MullerB Company’s employees earn vacation time at the rate of […]

Accounting Chapter 13 There may be a future sacrifice of economic benefits

Chapter 13 Current Liabilities and Contingencies Answer: Number of coupons issued 2,000,000 Expected participation rate 80% Expected coupon redemptions 1,600,000 Divided by # of coupons per prize 5 Estimated prizes to be awarded 320,000 Number awarded to date (560,000 ÷ […]

Accounting Chapter 13 Volt Based on Prior Experience Warranty Costs Are

Chapter 13 Current Liabilities and Contingencies AACSB: Reflective Thinking AACSB: Diversity AICPA: FN Measurement AICPA: BB Global 64. Kline Company refinanced current debt as long-term debt on January 5, 2017. Kline’s fiscal year ended on December 31, 2016, and its […]

Accounting Chapter 14 Homework Communication Skills Addition Communication Cases 141

14-36 Intermediate Accounting, 8/e DEBT CONTINUED, WITH MODIFIED TERMS WHEN TOTAL CASH PAYMENTS EXCEED THE BOOK VALUE OF THE DEBT If the payments exceed the amount owed, the restructured debt agreement still provides interest on the debt – but less […]

Accounting Chapter 14 Homework December 31 December 31 Hsa Recorded The

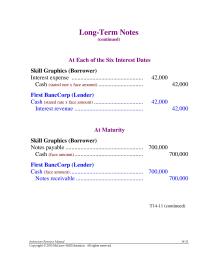

Long-Term Notes (continued) At Each of the Six Interest Dates Skill Graphics (Borrower) Interest expense ………………………………………… 42,000 Cash (stated rate x face amount) ………………………… 42,000 First BancCorp (Lender) Cash (stated rate x face amount) …………………………… 42,000 Interest revenue ………………………………………. 42,000 […]

Accounting Chapter 14 Homework Discount Bonds Payable Difference Bonds Payable

Exercise 14–4 1. January 1, 2016 Interest $4,000,000¥ x 11.46992 * = $45,879,680 Principal $80,000,000 x 0.31180 ** = 24,944,000 Present value (price) of the bonds $70,823,680 ¥ 5% x $80,000,000 * Present value of an ordinary annuity of $1: […]

Accounting Chapter 14 Homework In general, debt increases risk. Debt places owners in a subordinate position

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Judgment Case 14–9 Requirement 1 The debt to equity ratio is computed by dividing total liabilities by total shareholders’ equity. […]

Accounting Chapter 14 Homework Interest Expense Discount Bonds Payable Cash July

Student Name: Class: Cash Effective Increase in Outstanding Pay- Payment Interest Balance Balance ment 4.5% 5% 96,768 14,500 4,838 338 97,106 24,500 4,855 355 97,461 Cash Recorded Increase in Outstanding Pay- Payment Interest Balance Balance ment 4.5% 100,000 96,768 34,500 […]

Accounting Chapter 14 Homework No interest should be recorded after the restructuring

Exercise 14–34 Analysis: Book value: $12 million + 1.2 million = $13,200,000 Future payments: ($1 million x 2) + $11 million = 13,000,000 Gain to debtor $ 200,000 1. January 1, 2016 Interest payable (10% x $12,000,000) ……………………. 1,200,000 Notes […]

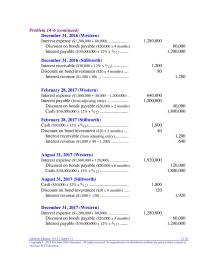

Accounting Chapter 14 Homework Present Value Ordinary Annuity 10 Table

Problem 14–6 (continued) December 31, 2016 (Western) Interest expense ($1,200,000 + 80,000) …………………. 1,280,000 Discount on bonds payable ($20,000 x 4 months) 80,000 Interest payable ($30,000,000 x 12% x 4/12) …….. 1,200,000 December 31, 2016 (Stillworth) Interest receivable ($30,000 x […]

Accounting Chapter 14 Homework Teaching Transparency Masters The Following Can Reproduced

CHAPTER 14 Bonds and Long-Term Notes Overview This chapter continues the presentation of liabilities. Specifically, the discussion focuses on the accounting treatment of long-term liabilities. Long-term notes and bonds are discussed, as well as the extinguishment of debt and troubled […]

Accounting Chapter 14 Homework The 2016 Statement Comprehensive Income Unrealized

Problem 14–20 (concluded) Requirement 4 Microsoft’s note states that “Because the convertible debt may be wholly or partially settled in cash, we are required to separately account for the liability and equity components of the notes.” As indicated in the […]

Accounting Chapter 14 Homework Those Who Support Separate Recognition

Real World Case 14–2 Requirement 1 ($ in millions) Cash (price given) ………………………………………………. 968 Discount on notes (difference) …………………………….. 832 Notes payable (face amount) ……………………………. 1,800 Requirement 2 ($ in millions) Fiscal Increase Outstanding Year-end Cash Interest Expense in Balance […]

Accounting Chapter 14 Homework Under The Modified Terms Total Cash Paid

Chapter 14 Bonds and Long-Term Notes QUESTIONS FOR REVIEW OF KEY TOPICS Question 14–1 Periodic interest is calculated as the effective interest rate times the amount of the debt outstanding during the period. This same principle applies to the flip […]

Accounting Chapter 14 Homework Unnatural will report the loss from the change in the fair value of the bonds in net

Principal $240,000,000 x 0.31180 ** = 74,832,000 Present value (price) of the bonds $212,471,040 ¥ 5% x $240,000,000 * present value of an ordinary annuity of $1: n=20, i=6% ** present value of $1: n=20, i=6% Cash (price determined above) […]

Accounting Chapter 14 Homework Because none of the change is due to the change in general interest rates

Exercise 14–20 1. January 1, 2016 Machinery ……………………………………………………………….. 4,000,000 Notes payable ………………………………………………………… 4,000,000 2. Amortization schedule $4,000,000 ÷ 3.16987 = $1,261,881 amount (from Table 4) installment of loan n = 4, i = 10% payment Cash Effective Decrease in Outstanding […]

Accounting Chapter 14 Include a debit to cash that has been increased by interest

Chapter 14 Bonds and Long-Term Notes Comprehensive income includes both net income and OCI. 108. On March 1, 2016, Doll Co. issued 10-year convertible bonds at 106. During 2019, the bonds were converted into common stock when the market price […]

Accounting Chapter 14 Increases Decreases Remains The Samed Equal The

Chapter 14 Bonds and Long-Term Notes True/False Questions 1. The specific provisions of a bond issue are described in a document called a bond indenture. Answer: True Level of Learning: 1 Easy Learning Objective: 14-01 Topic Area: Bond indenture Blooms: […]

Accounting Chapter 14 January 2016 Comet Products Issued 80 Million

Chapter 14 Bonds and Long-Term Notes AICPA: FN Measurement 165. Required: Determine the gain or loss that Health Foods would have reported in its 2016 income statement if it had redeemed (and retired) the debentures at fair value at the […]

Accounting Chapter 14 June 30 2017 Interest Payable Each Year

Chapter 14 Bonds and Long-Term Notes a. $252,369,000. b. $256,369,000. c. $256,200,000. d. $257,030,070. Answer: c Level of Learning: 3 Hard Learning Objective: 14-02 Learning Objective: 14-04 Topic Area: Determining interest ‒ Between interest dates Topic Area: Financial statement disclosures […]

Accounting Chapter 14 Wolfs Fiscal year The Calendar Year Wolf Uses

Chapter 14 Bonds and Long-Term Notes 141. On January 1, 2016, Cool Universe issued 10% bonds dated January 1, 2016, with a face amount of $20 million. The bonds mature in 2025 (10 years). For bonds of similar risk and […]

Accounting Chapter 15 Answer Level Learning Hard Learning Objective 1509

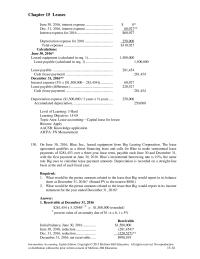

Chapter 15 Leases Intermediate Accounting, Eighth Edition, Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 15–21 59. What would be the amount of interest expense recorded with payment […]

Accounting Chapter 15 Blooms Remember Reflective Thinking Measurement

Chapter 15 Leases 148. Peridot Leasing entered into an agreement to lease warehouses to AMC Foods. a. The agreement calls for ownership of the aircraft to be transferred to AMC Foods at the end of the lease term. b. The […]

Accounting Chapter 15 Homework For both sales-type and direct-financing leases, the lessor’s gross investment

CPA Exam Questions (concluded) 5. a. In a capital lease with a bargain purchase option, the lessee will control the asset for its total useful life. Therefore, the depreciation should be allocated over the 8-year life of the asset. $240,000 […]

Accounting Chapter 15 Homework Implicit Interest Rate Years 300000 Years 365760

Student Name: Class: 365,760$ 348,685$ 17,075 365,760$ Correct! (b) By Rhone-Metro (the lessor) (a) By Western Soya Co. (the lessee) Present value of minimum lease payments Plus: Present value of the lessee-guaranteed residual value Since at least one criterion is […]

Accounting Chapter 15 Homework In a Type B lease, the lessee records interest the normal way

Brief Exercise 15-17 Income Statement: Lease revenue (straight-line amount) ……………………… $25,000* Depreciation ($176,000 ÷ 12 years) …………………………….. (14,667)** Increase in earnings (pretax) ………………………… $10,333 In a Type B lease, the lessor records lease revenue on a straight-line basis. The lessor, […]

Accounting Chapter 15 Homework Present Value Minimum Lease Payments Discounted Lower

Exercise 15-9 1. Receivable at December 31, 2016 $562,907 x 5.32948 = $3,000,000 (rounded) present value of an annuity due of $1: n=6, i=5% Net Receivable Initial balance, June 30, 2016 …………. $3,000,000 June 30, 2016 reduction …………………. […]

Accounting Chapter 15 Homework Requirement Capital Lease Lessee Direct Financing Lease

Cash …………………………………….. 40,000 December 31, 2016 Rent expense …………………………….. 40,000 Cash …………………………………….. 40,000 Cash ………………………………………… 40,000 Rent revenue …………………………. 40,000 December 31, 2016 Cash ………………………………………… 40,000 Rent revenue …………………………. 40,000 Depreciation expense ($350,000 ÷ 5 years) 70,000 Accumulated depreciation ………. […]

Accounting Chapter 15 Homework Requirement December 31 2017 Yard Art Landscaping

Problem 15-15 (continued) Not required in the problem, but helpful to see that the present value calculation is precisely the reverse of the lessor’s calculation of quarterly payments: Amount to be recovered (fair value) $26,427 Less: Present value of the […]

Accounting Chapter 15 Homework Requirement Since 1 Title The Conveyer Does

Problem 15-9 (continued) Requirement 2 The lessee’s incremental borrowing rate (12%) is more than the lessor’s implicit rate (10%). So, both parties’ calculations should be made using a 10% discount rate: Application of Classification Criteria 1 Does the agreement specify […]

Accounting Chapter 15 Homework So Ifrs Would Produce The Same Results

Problem 15-19 Requirement 1 Application of Classification Criteria 1 Does the agreement specify that ownership of the asset transfers to the lessee? NO 2 Does the agreement contain a bargain purchase option? NO 3 Is the lease term equal to […]

Accounting Chapter 15 Homework The Impact Any Changes Will Significant Us

Chapter 15 Leases QUESTIONS FOR REVIEW OF KEY TOPICS Question 15-1 Regardless of the legal form of the agreement, a lease is accounted for as either a rental agreement or a purchase/sale accompanied by debt financing depending on the substance […]

Accounting Chapter 15 Homework The residual value influences the lessee only by the fact

EFFECT OF A BARGAIN PURCHASE OPTION A bargain purchase option (BPO) is a provision of some lease contracts that gives the lessee the option of purchasing the leased property at a “bargain” price. The expectation that the option price will […]

Accounting Chapter 15 Homework Topic Est Time Min Operating Lease Operating

15-32 Intermediate Accounting, 8/e INTERNATIONAL FINANCIAL REPORTING STANDARDS Present value of minimum lease payments. Under IAS No. 17, both parties to a lease generally use the rate implicit in the lease to discount minimum lease payments. Under U.S. GAAP, lessors […]

Accounting Chapter 15 Homework Total 1250958 Since Interstates Cost 1050000 Was

Problem 15-25 (concluded) 4. Expenses for year ended December 31, 2016 June 30, 2016 interest ………………………………………. $ 0 Dec. 31, 2016 interest ………………………………………. 121,855** Interest for 2016 ………………………………………….. $121,855 June 30, 2016 amortization……………………………….. 0 Dec. 31, 2016 amortization ………………………………. 441,052** […]

Accounting Chapter 15 Homework Type Lease Amortization Schedule Lease Payments

Exercise 15-23 1. January 1, 2016 Lease receivable (fair value / present value) …………………… 500,000 Inventory of equipment (lessor’s cost) …………………….. 500,000 Lease receivable ……………………………………………………. 4,242 Cash (initial direct costs) ………………………………………… 4,242 Cash (lease payment)…………………………………………………. 184,330 Lease receivable ………………………………………………… 184,330 […]

Accounting Chapter 15 Homework Under Ias No 17 Both Parties Lease

C CH HA AP PT TE ER R 1 15 5 L Le ea as se es s Overview In the previous chapter, we saw how companies account for their long-term debt. The focus of that discussion was bonds and […]

Accounting Chapter 15 In a Type B lease, the lessee amortizes its right

Chapter 15 Leases AACSB: Knowledge application AICPA: FN Measurement Feedback: Lease receivable (PV of lease payments [“selling price”]) 80,000 Profit on ROU asset sold (difference) …… 14,000 Asset (lessor’s cost: book value) ……… 66,000 Interest revenue = (10% x ½ […]

Accounting Chapter 15 Scape Leased Equipment User Inc January 2016

Chapter 15 Leases Intermediate Accounting, Eighth Edition, Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 15–61 130. On June 30, 2016, Blue, Inc., leased equipment from Big Leasing […]

Accounting Chapter 15 There Bargain Purchase Option And Reagan Guarantees

Chapter 15 Leases True/False Questions 1. At the inception of a lease agreement, the company’s debt to equity ratio and rate of return on assets are both affected whether the lease is classified as a capital lease or as an […]

Accounting Chapter 16 A temporary difference originates in one period and reverses

Chapter 16 Accounting for Income Taxes True/False Questions 1. A temporary difference originates in one period and reverses, or turns around, in one or more later periods. Answer: True Level of Learning: 1 Easy Learning Objective: 16-01 Topic Area: Temporary […]

Accounting Chapter 16 Homework Deferred Tax Liability Determined Above Income Tax

Problem 16–1 (continued) Requirement 2 ($ in thousands) Current Future Year Taxable 2017 Amount Pretax accounting income 220 Temporary difference: 2016 services (10) 10 2017 services (25) 25 Taxable income (income tax return) 205 Enacted tax rate 40% 40% Tax […]

Accounting Chapter 16 Homework Deltas Disclosure Note States We Periodically Assess

Problem 16–8 (continued) Requirement 4 ($ in millions) Current Future Future Year Taxable Deductible 2017 Amounts Amounts [2018] [2018] Pretax accounting income 183 Permanent difference: Life insurance premiums 2 Temporary differences: Casualty insurance (reversing) 30 Subscriptions—2016 (reversing)* (18) Subscriptions—2017 ($35 […]

Accounting Chapter 16 Homework Income Tax Expense To Balance Deferred Tax

Chapter 16 Accounting for Income Taxes _____________________________________________________________________________ QUESTIONS FOR REVIEW OF KEY TOPICS Question 16–1 Income tax expense is comprised of both the current and the deferred tax consequences of events and transactions already recognized. Specifically, the $12.3 million expense […]

Accounting Chapter 16 Homework Journal entry at the end of 2016

Student Name: Class: 2016 2017 2018 2019 60,000$ 80,000$ 70,000$ 70,000$ (39,600) (52,800) (18,000) (9,600) Cumulative Temporary 2016 2017 2018 2019 Difference (39,600) (52,800) (18,000) (9,600) (9,600) (22,800) 12,000 20,400 –$ «- Correct! (22,800) 12,000 20,400 9,600$ «- Correct! 12,000 […]

Accounting Chapter 16 Homework Please Let Know You Have Any Questions

CASES Analysis Case 16–1 Requirement 1 Temporary differences originate in one or more years and reverse in one or more future years. Differing depreciation methods are a common example of a temporary difference. On the other hand, permanent differences are […]

Accounting Chapter 16 Homework Pretax Accounting Income Temporary Difference Installment Income

C CH HA AP PT TE ER R 1 16 6 A Ac cc co ou un nt ti in ng g f fo or r I In nc co om me e T Ta ax xe es s Overview […]

Accounting Chapter 16 Homework Straight-line depreciation for financial reporting

Exercise 16–20 (concluded) Requirement 2 ($ in thousands) Operating loss before income taxes $(375 ) Income tax benefit—net operating loss 150 Net loss $(225) Solutions Manual, Vol.2, Chapter 16 16–41 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction […]

Accounting Chapter 16 Homework Tax Payable Currently Deferred Tax Liability Future

Alternate Exercises and Problems 16–1 Deferred tax asset ($90,000 x 40%) 36,000 Income tax payable (given) 285,000 Deferred tax liability ([$80 million – 50 million] x 35%) 10.5 Income tax payable ($50 million x 35%) 17.5 Chapter 16 Accounting for […]

Accounting Chapter 16 Homework Temporary Differences Depreciation Warranty Expense 977 Taxable

Exercise 16–7 1. Liability—loss contingency 2. Liability—subscriptions 3. Prepaid rent 4. Accrued bond interest payable 5. Prepaid insurance 6. Unrealized loss on investments (shareholders’ equity account) 7. Warranty liability 8. Liability—unearned rent revenue 9. Accumulated depreciation; and thus depreciable assets […]

Accounting Chapter 16 Homework The Enacted Tax Rate 40 Each Year

TEMPORARY AND PERMANENT DIFFERENCES Kent Land Management reported pretax income in 2016, 2017, and 2018 of $100 million except for an additional income of $40 million from installment sales and $5 million interest from investments in municipal bonds in 2016. […]

Accounting Chapter 16 Homework What Might Contribute RadioShack’s Need Record Valuation

1-32 Intermediate Accounting, 8/e Dealing with Uncertainty GAAP allows companies to recognize in the financial statements the tax benefit of a position it takes only if it is “more likely than not” (greater than 50% chance) to be sustained if […]

Accounting Chapter 16 In 2016, Magic Table Inc. decides to add a 36-month warranty

Chapter 16 Accounting for Income Taxes a. An increase in a deferred tax asset. b. A decrease in a deferred tax asset. c. An increase in a deferred tax liability. d. A decrease in a deferred tax liability. Answer: b […]

Accounting Chapter 16 Income Taxes And The Tax Basis Was

Chapter 16 Accounting for Income Taxes Probability table: Amount of the tax benefit that management expects to sustain $60 $36 $12 Percentage likelihood that the tax position will be sustained at this level 25% 30% 45% Cumulative probability that the […]

Accounting Chapter 16 The enacted tax rate for 2015 and 2016 is 40%, and it is 35% for years

Chapter 16 Accounting for Income Taxes current year, the temporary difference is $45,000,000, and Doubtful determines that the balance in the valuation account should now be $5,000,000. Taxable income is $15,000,000 and the tax rate is 40% for all years. […]

Accounting Chapter 17 Assume the actuary estimates the net cost of providing health

Chapter 17 Pensions and Other Postretirement Benefits Answer: c Level of Learning: 3 Hard Learning Objective: 17-10 Topic Area: Other postretirement plans – EPBO and APBO Blooms: Apply AACSB: Knowledge application AICPA: FN Measurement Feedback: APBO (12/31/2016) = EPBO (12/31/2016) […]

Accounting Chapter 17 Homework After the two amortization amounts are

Problem 17–16 (continued) Requirement 5 To record gains and losses ($ in millions) Loss—OCI ($5 loss on change of PBO assumption) 5 PBO …………………………………………….. 5 Plan assets ………………………………………… 12 Gain—OCI ($36 actual return on assets exceeds $24 gain expected) 12 […]

Accounting Chapter 17 Homework Balance Jan 2016 Service Cost Interest Cost

Exercise 17–4 Requirement 1 ($ in millions) Pension expense (total) …………………………………………… 14 Plan assets (expected return on assets) ………………………….. 4 PBO ($10 service cost + $6 interest cost) …………………….. 16 Amortization of net loss—OCI (current amortization)* .. 2 Requirement 2 […]

Accounting Chapter 17 Homework Items The Statement Comprehensive Income And

Chapter 17 Pensions and Other Postretirement Benefits QUESTIONS FOR REVIEW OF KEY TOPICS Question 17–1 Pension plans are arrangements designed to provide income to individuals during their retirement years. Funds are set aside during an employee’s working years so that […]

Accounting Chapter 17 Homework Now Requires Companies Record Obligation

ATTRIBUTION Jessica Farrow was hired by Global Communications at age 22 at the beginning of 2005 and is expected to retire at the end of 2044 at age 61. The retirement period is estimated to be 20 years. Global’s employees […]

Accounting Chapter 17 Homework Plan Assets Expected Return Plan Assets

Problem 17–7 Requirement 1 ($ in 000s) Net gain (previous gains exceeded previous losses) $170 10% of $1,400 ($1,400 is greater than $1,100) 140 Excess at the beginning of the year $ 30 Average remaining service period years ÷ 15 […]

Accounting Chapter 17 Homework PV of retirement annuity at end of 2041

Student Name: Class: 19,200$ 174,872$ 32,220$ Correct! 270,000$ 68,040$ 619,702$ 122,174$ Correct! 122,174$ (108,743) 13,431$ (7,612) 5,819$ PV of retirement annuity at end of 2016 Pension benefit at end of 2016 Less: Interest cost Service cost Projected benefit obligation Requirement […]

Accounting Chapter 17 Homework Service Cost And Net Interest Cost income Are

C CH HA AP PT TE ER R 1 17 7 P Pe en ns si io on ns s a an nd d O Ot th he er r P Po os st tr re et ti ir re […]

Accounting Chapter 17 Homework The Gain And Loss Becomes Part The

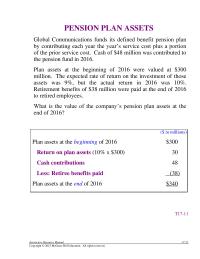

PENSION PLAN ASSETS Global Communications funds its defined benefit pension plan by contributing each year the year’s service cost plus a portion of the prior service cost. Cash of $48 million was contributed to the pension fund in 2016. Plan […]

Accounting Chapter 17 Homework The Present Value The Retirement

Interest cost 36 Expected return on the plan assets ($27 actual, less $3 gain) (24) Pension expense $72 PBO 72 Plan assets 60 Cash (given) 60 PBO 27 Plan assets (given) 27 Alternate Exercises and Problems 17–1 Chapter 17 Pensions […]

Accounting Chapter 17 Homework They Are Instead Reported The Statement Comprehensive

Exercise 17–22 (concluded) Requirement 2 ($ in millions) Service cost 72 DBO (2016 service cost) 60 DBO (past service cost) 12 Net interest cost (7.5% x [$360 – 240]) 9 Plan assets (7.5% x $240: interest income) 18 DBO (7.5% […]

Accounting Chapter 17 Pensions And Other Postretirement Benefits level Learning Medium learning

Chapter 17 Pensions and Other Postretirement Benefits Intermediate Accounting, Eighth Edition, Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 17–81 168. The following is an incomplete pension spreadsheet […]

Accounting Chapter 17 Plan Assets Fair Value Increased During The

Chapter 17 Pensions and Other Postretirement Benefits True/False Questions 1. The projected benefit obligation may be less reliable than the accumulated benefit obligation. Answer: True Level of Learning: 1 Easy Learning Objective: 17-02 Topic Area: Pension obligation – ABO-Vested-PBO Blooms: […]

Accounting Chapter 17 This The Accrual Basis Which Also Used

Chapter 17 Pensions and Other Postretirement Benefits Answer: 1. ($ in millions) Reported in income statement: Service cost–2016 $ 150 Past service cost 24 Service cost $ 174 Net interest cost (10% x [$960 – 600]) $ 36 Reported as […]

Accounting Chapter 17 Using the service method, calculate the amount of prior

Chapter 17 Pensions and Other Postretirement Benefits Level of Learning: 2 Medium Learning Objective: 17-06 Topic Area: Pension expense – Net loss or net gain Blooms: Apply AACSB: Knowledge application AICPA: FN Measurement 149. Waddle Company amended its defined benefit […]

Accounting Chapter 17 With Respect Ralph What Oregon’s Accumulated

Chapter 17 Pensions and Other Postretirement Benefits Long-term expected return on plan assets 9% Assuming no other relevant data exist, what is the pension expense for the year? a. $190,000. b. $ 92,400. c. $ 60,000. d. $170,000. Answer: b […]

Accounting Chapter 18 A stock split in which the par per share is reduced

Chapter 18 Shareholders’ Equity TERM PHRASE NUMBER 1. Reverse stock split Designed to increase the market value of stock. ____ 2. Retained earnings Reduces the net proceeds from selling shares. ____ 3. Cumulative A feature of most preferred stock. ____ […]

Accounting Chapter 18 Homework Common Stock Par Authorized 5000000 Shares Issued

Student Name: Class: Debit Credit 150,000 «- Correct! 1,650,000 1,650,000 1,650,000 «- Correct! 1,400,000 200,000 1,200,000 «- Correct! 1,400,000 200,000 1,600,000 «- Correct! Common stock Paid-in capital – excess of par Cash Retained Earnings Cash Cash November 9, 2018 Retired […]

Accounting Chapter 18 Homework Paidin Capital Reacquired Shares Retained Earnings

Common stock (60 million shares x $1 par) ……………… 60 Paid-in capital – excess of par (difference) ………………. 540 February 14 Legal expenses (1 million shares x $10 per share) …………. 10 Common stock (1 million shares x $1 par) […]

Accounting Chapter 18 The firm was authorized to issue100,000 shares of

Chapter 18 Shareholders’ Equity 56. The shareholders’ equity of Red Corporation includes $200,000 of $1 par common stock and $400,000 par value of 6% cumulative preferred stock. The board of directors of Red declared cash dividends of $50,000 in 2016 […]

Accounting Chapter 18 What Does this Mean answer Preferred Shares Are Noncumulative

Chapter 18 Shareholders’ Equity 128. Fowler Co.’s balance sheet showed the following at December 31, 2016: Common stock, $10 par $100,000 Paid-in capital—excess of par 50,000 Retained earnings 20,000 A cash dividend is declared on December 31, 2016, and is […]

Accounting Chapter 18 What Was Shareholders Equity December 31 2016a

Chapter 18 Shareholders’ Equity True/False Questions 1. Mandatorily redeemable preferred stock is reported as a liability. Answer: True Level of Learning: 1 Easy Learning Objective: 18-03 Topic Area: Stock—Classes of shares Blooms: Remember AACSB: Reflective thinking AICPA: FN Measurement 2. […]

Accounting Chapter 19 Earnings Available Common The Numerator The Eps

Chapter 019 Share-Based Compensation and Earnings per Share Intermediate Accounting, Eighth Edition, © The McGraw-Hill Companies, Inc., 2016 19–41 94. When computing earnings per share, noncumulative preferred dividends not declared should be: a. Ignored. b. Deducted from earnings for the […]

Accounting Chapter 19 Except for tax considerations the potentially

Chapter 019 Share-Based Compensation and Earnings per Share Intermediate Accounting, Eighth Edition, © The McGraw-Hill Companies, Inc., 2016 19-1 True/False Questions 1. GAAP requires using intrinsic value accounting for employee stock options. Answer: False Level of Learning: 1 Easy Learning […]

Accounting Chapter 19 Homework Eps Subsequent Years For Comparative Purposes Net

$25.50 fair value per share x 12 million shares granted = $306 million fair value of award ($ in millions) Compensation expense ($306 million ÷ 3 years) .. 102 Paid-in capital – restricted stock …………….. 102 x 12 million shares […]

Accounting Chapter 19 Homework Share Millions Except Per Share Amounts 2014

Student Name: Class: 2$ Debit Credit 40 «- Correct! 16 16 «- Correct! Tax expense Paid-in capital – stock options Deferred tax asset 40 «- Correct! 16 16 «- Correct! 320 80 40 360 «- Correct! 64 32 32 «- […]

Accounting Chapter 19 On June 1, 2016, the company’s common stock split 2 for 1

Chapter 019 Share-Based Compensation and Earnings per Share Intermediate Accounting, Eighth Edition, © The McGraw-Hill Companies, Inc., 2016 19–81 Topic Area: Basic EPS—Earnings after preferred dividends Blooms: Apply AACSB: Knowledge application AICPA: FN Measurement 153. Sugarland Industries reported a net […]

Accounting Chapter 19 That Is The shares Are Added The Denominator

Chapter 019 Share-Based Compensation and Earnings per Share 131. Listed below are five terms followed by a list of phrases that describe or characterize each of the terms. Match each phrase with the number for the most correct term. TERM […]

Accounting Chapter 19 The Disclosure Note Indicates That The Effect

Chapter 019 Share-Based Compensation and Earnings per Share Topic Area: Stock plans—Restricted stock Blooms: Remember AACSB: Reflective thinking AICPA: BB Legal AICPA: FN Measurement 175. The tax code differentiates between qualified and nonqualified incentive plans. What are the major differences […]

Accounting Chapter 19 Under U.S. GAAP, for stock options, a deferred tax asset (DTA)

Chapter 019 Share-Based Compensation and Earnings per Share Intermediate Accounting, Eighth Edition, © The McGraw-Hill Companies, Inc., 2016 19–21 46. What is the entry to record the expiration of 10% of the options on December 31, 2020? a. Paid-in capital—stock […]

Accounting Chapter 2 Critical Thinking intermediate Accounting Eighth Edition Copyright 2015

Chapter 2 Review of the Accounting Process 60. Permanent accounts would not include: a. Interest expense. b. Salaries and wages payable. c. Prepaid rent. d. Deferred revenues. Answer: a Level of Learning: 2 Medium Learning Objective: 02-01 Learning Objective: 02-07 […]

Accounting Chapter 2 December 31 2016 The End Larrys Used

Chapter 2 Review of the Accounting Process True/False Questions 1. Owners’ equity can be expressed as assets minus liabilities. Answer: True Level of Learning: 1 Easy Learning Objective: 02-01 Topic Area: The basic model – Accounting equation Blooms: Remember AACSB: […]

Accounting Chapter 2 Homework Correct Liabilities And Shareholders’ Equity Current Liabilities

Student Name: Class: Date Account Debit Credit (7) 2,000 2,000 «- Correct! (8) 1,000 1,000 «- Correct! Prepaid rent Rent expense Sales revenue Unearned revenue (1) 10,000 10,000 «- Correct! (2) 1,500 1,500 «- Correct! (3) 1,500 1,500 «- Correct! […]

Accounting Chapter 2 Interest Receivable 12 Year 3000 1500 Prepaid

Chapter 2 Review of the Accounting Process Use the following to answer questions 125–127: The adjusted trial balance for China Tea Company at December 31, 2016, is presented below: Debit Credit Cash 10,500 Accounts receivable 150,000 Prepaid rent 5,000 Inventory […]

Accounting Chapter 2 The Following Adjusting Entries Were Prepared December

Chapter 2 Review of the Accounting Process Using the chart of accounts provided, indicate by account number the account or accounts that would be debited and credited in the following transactions and indicate the type of transaction as: (1) an […]

Accounting Chapter 20 Goosen Company bought a copyright for $90,000 on January 1

Chapter 20 Accounting Changes b. A patent balance of $102 million. c. Patent amortization expense of $15 million. d. Patent amortization expense of $7.5 million. Answer: b Level of Learning: 3 Hard Learning Objective: 20-04 Topic Area: Change in accounting […]

Accounting Chapter 20 Homework Calculation of annual depreciation after the change:

Student Name: Class: Debit Credit Requirement 2: 2016 2015 (210,000) (159,600) 315,000$ 239,400$ Correct! Correct! 3.15$ 2.39$ Correct! Correct! Income tax expense Net income Earnings per common share Earnings per share: 525,000$ 399,000$ Problem 20-01 McGraw-Hill/Irwin Instructor Requirement 1: CECIL-BOOKER […]

Accounting Chapter 20 Homework Estimated Remaining Life Years New

Bearing reports the change prospectively; previous financial statements are not revised. Instead, the company simply employs the straight-line method from then on. The undepreciated cost remaining at the time of the change would be depreciated straight-line over the remaining useful […]

Accounting Chapter 20 Instead The Company Simply Employs The Straightline Method

Chapter 20 Accounting Changes 103 Listed below are five terms followed by a list of phrases that describe or characterize each of the terms. Match each phrase with the number for the correct term. TERM PHRASE NUMBER 1. Prospective approach […]

Accounting Chapter 20 Lifo Fifo Inventory Costing Change From Average

Chapter 20 Accounting Changes True/False Questions 1. Most, but not all, changes in accounting principle are reported using the retrospective approach. Answer: True Level of Learning: 1 Easy Learning Objective: 20-01 Topic Area: Types of accounting changes Topic Area: Distinguish […]

Accounting Chapter 20 Recall That Lifo Inventory Consists Layers Added in

Chapter 20 Accounting Changes 20–52 Spiceland/Sepe/Nelson, Intermediate Accounting, Eighth Edition 118. Lindy Company’s auditor discovered two errors. No errors were corrected during 2015. The errors are described as follows: (1.) Merchandise costing $4,000 was sold to a customer for $9,000 […]

Accounting Chapter 21 December 31 2015 And 10000 At December 31

Chapter 21 The Statement of Cash Flows True/False Questions 1. Amounts held in cash equivalent investments must be reported separately from amounts held as cash in the statement of cash flows. Answer: False Level of Learning: 2 Medium Learning Objective: […]

Accounting Chapter 21 Financing cash outflow Interest received on cash savings

Chapter 21 The Statement of Cash Flows Answer: a Level of Learning: 2 Medium Learning Objective: 21-09 Topic Area: IFRS ‒ Statement of cash flows Blooms: Remember AACSB: Reflective thinking AACSB: Diversity AICPA: FN Measurement AICPA: BB Global 104. Companies […]

Accounting Chapter 21 Homework Depreciation expense and the loss on sale of land are not cash outflows

(decrease) (decrease) 1 600 0 0 600 Cash (paid to suppliers of goods) 600 2 600 18 0 618 Inventory 18 Cash (paid to suppliers of goods) 618 3 600 0 558 558 5. Summary Entry Cost of goods sold […]

Accounting Chapter 21 Homework Investing Activities Sale Building Purchase Investment Purchase

Student Name: Class: Dec. 31 Changes Dec. 31 2015 Debits Credits 2016 30 12 42 3 2 5 12 3 9 30 30 – 100 60 160 200 50 250 100 26 126 90 35 80 135 575 715 Notes […]

Accounting Chapter 21 Homework Mr Lowell Had Just Hung The Phone

RETAINED EARNINGS The stock dividend caused a $13 million reduction of retained earnings. Net income increased retained earnings by $12 million. The net reduction of $1 million accounted for by these two entries leaves unexplained $5 million […]

Accounting Chapter 21 Interest Payments And Interest Received Must

Chapter 21 The Statement of Cash Flows Intermediate Accounting, Eighth Edition, Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 21–21 Use the following to answer questions 56–60: Each […]

Accounting Chapter 21 The Statement Cash Flows salaries Payable notes

Chapter 21 The Statement of Cash Flows Level of Learning: 3 Hard Learning Objective: 21-03 Learning Objective: 21-08 Topic Area: Cash paid for expenses – Direct method Topic Area: Reconstruct events and transactions Blooms: Apply AACSB: Knowledge application AICPA: FN […]

Accounting Chapter 3 Assets classified as property, plant, and equipment

Chapter 3 The Balance Sheet and Financial Disclosures True/False Questions 1. The balance sheet reports a company’s financial position at a point in time. Answer: True Level of Learning: 1 Easy Learning Objective: 03-01 Topic Area: The Balance Sheet Blooms: […]

Accounting Chapter 3 Homework You May Wish Discuss This Class So

3-14 Intermediate Accounting, 8/e FINANCIAL DISCLOSURES (continued) Management responsibilities ➢ Annual reports include a management’s responsibility section that: Asserts the responsibility of management for the information contained in the annual report as well as an assessment of the […]

Accounting Chapter 3 Homework A subsequent event is a significant development that takes place after

CHAPTER 3 THE BALANCE SHEET AND FINANCIAL DISCLOSURES Overview Chapter 1 stressed the importance of the financial statements in helping investors and creditors predict future cash flows. The balance sheet, along with accompanying disclosures, provides relevant information useful in helping […]

Accounting Chapter 3 Homework Note payable Current maturities of long-term debt

Student Name: Class: 25,000 15,000 70,000 Land held for sale Bond sinking fund Total investments 110,000 595,000 (160,000) 435,000 10,000 894,000$ Equipment Less: Accumulated depreciation Net property, plant, and equipment Intangible assets: Patents Total assets 30,000$ 80,000 30,000$ 65,000 420,000 […]

Accounting Chapter 3 November 20 2016b The Property Plant And

Chapter 3 The Balance Sheet and Financial Disclosures Blooms: Apply AACSB: Analytic AICPA: FN Risk Analysis 87. Compute the debt to equity ratio for Marjoram Company. Round your answer to two decimal places. Answer: ($108,400 + 100,000) / ($70,000 + […]

Accounting Chapter 3 Unqualified Opinion Independent And Professional Report About

Chapter 3 The Balance Sheet and Financial Disclosures a. 0.75. b. 1.13. c. 0.53. d. 1.80. Answer: b Level of Learning: 3 Hard Learning Objective: 03-08 Topic Area: Financing Ratios Blooms: Apply AACSB: Analytic AICPA: FN Risk Analysis Feedback: Debt […]

Accounting Chapter 4 Homework Cash Flows From Operating Activities Net Income

Problem 4–7 (concluded) Earnings per share:* Income from continuing operations $2.74 Discontinued operations 0.42 Net income $3.16 *Weighted-average shares = 1,000,000 + (400,000÷2) = 1,200,000 Note: The depreciation expense error is a prior period adjustment (to retained earnings) and is […]

Accounting Chapter 4 Homework For each period for which an income statement is presented

Exercise 4–21 (concluded) TIGER ENTERPRISES Statement of Cash Flows For the Year Ended December 31, 2016 ($ in thousands) Cash flows from operating activities: Collections from customers $ 7,080 Prepayment of insurance (130) Payment to inventory suppliers (3,460) Payment for […]

Accounting Chapter 4 Homework Income Taxes Total Expenses Net Income Earnings

Student Name: Class: 2016 2015 4,000,000$ 3,000,000$ 2,570,000 1,680,000 1,430,000 1,320,000 750,000 635,000 340,000 282,000 Problem 04-01 McGraw-Hill/Irwin Instructor for the Years Ended December 31 Comparative Income Statements REED COMPANY Selling Sales revenue Cost of goods sold Gross profit Operating […]

Accounting Chapter 4 Homework Requirement Firms Reported Restructuring Charges

Case 4–5 (concluded) Requirement 5 All of the following information is disclosed in notes to financial statements that include the period in which an exit or disposal activity is initiated and any subsequent period until the activity is completed: a. […]

Accounting Chapter 4 Homework Us Gaap Could Classified Either Operating Cash

Exercise 4–3 Requirement 1 GENERAL LIGHTING CORPORATION Income Statement For the Year Ended December 31, 2016 Revenues and gains: Sales ……………………………………………………….. $2,350,000 Interest …………………………………………………….. 80,000 Total revenues and gains ………………………… 2,430,000 Expenses and losses: Cost of goods sold …………………………………….. $1,200,300 […]

Accounting Chapter 4 Homework Us Gaap Such That Costs For Repairs

Question 4–1 The income statement is a change statement that reports transactions—revenues, expenses, gains, and losses—that cause owners’ equity to change during a specified reporting period. Question 4–2 Income from continuing operations includes the revenue, expense, gain, and loss transactions […]

Accounting Chapter 4 Measurement 101 Net Income Often Referred Quot the Bottom

Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows 94. Calstone, Inc., prepares a single, continuous statement of comprehensive income. The following situations occurred during the company’s 2016 fiscal year: 1. Land that had been held […]

Accounting Chapter 4 Nore production or distribution without the prior written

Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows c. Loss on the sale of equipment. d. Accounts receivable increase. Answer: c Level of Learning: 2 Medium Learning Objective: 04-08 Topic Area: Topic Area: Statement of […]

Accounting Chapter 4 The Income Statement Comprehensive Income

Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows Intermediate Accounting, Eighth Edition, Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 4–41 Use the […]

Accounting Chapter 5 Bullseye Sells Gift Cards Redeemable For

a. John is expected to receive $100 for his tutoring services provided that he keeps track of his hours. b. Melody’s Piano will get paid for the 50 pianos sold provided that the pianos are non-defective after the customer takes […]

Accounting Chapter 5 Company Vulnerable Risks Associated With Holding Inventory

• V: ROE = ROA x Equity multiplier, so ROA = ROE / Equity multiplier = 0.16/1.9 = 8.4% • W: ROE = 16% = Net income / Avg. equity = 20 / {[w + 130]/2}; w = 120. • […]

Accounting Chapter 5 Desert Homes Adh Constructed New Subdivision During

c. $1,850,000 d. $1,800,000 Answer: b Level of Learning: 2 Medium Learning Objective: 05-07 Topic Area: When (or as) performance obligation(s) satisfied – Gift cards Blooms: Apply AACSB: Analytic AICPA: FN Measurement Feedback: Sale of a gift card created deferred […]

Accounting Chapter 5 Homework Disclosure The Objective Help Investors Understand The

CHAPTER 5 Revenue Recognition and Profitability Analysis Overview In Chapter 4 we discussed net income and its presentation in the income statement. In Chapter 5 we focus on revenue recognition, which determines when and how much revenue appears in the […]

Accounting Chapter 5 Homework Goal, help investors understand the nature, amount, timing and uncertainty

FRANCHISE ARRANGEMENTS • Assume that TrueTech starts selling TechStop franchises. TrueTech charges franchisees an initial fee in exchange for (a) the exclusive right to operate the only TechStop in a particular area for a five-year period, (b) the equipment necessary […]

Accounting Chapter 5 Homework However 2016 Has Been Tough Year And

COST RECOVERY METHOD ➢ The cost recovery method defers all gross profit recognition until cash equal to the cost of the item sold has been recovered. On November 1, 2016, the Belmont Corporation, a real estate developer, sold a tract […]

Accounting Chapter 5 Homework Jampj Pfizer Net Income Net Sales

Intermediate Accounting, 8/e 5–121 Problem 5–11 Requirement 1 Year Revenue recognized Gross profit recognized 2016 –0– – 0 – 2017 –0– 2018 $10,000,000 $1,800,000 Total $10,000,000 $1,800,000 – 0 – Requirement 2 2016 2017 2018 Construction in progress 2,400,000 3,600,000 […]

Accounting Chapter 5 Homework LearnIT plus That Vendor specific Objective Evidence

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw–Hill Education. Brief Exercise 5–16 If a seller is purchasing distinct goods or services from a customer at the fair value of […]

Accounting Chapter 5 Homework Lets Assume That Truetech Bases The Estimate

RECOGNIZING REVENUE FOR CONTRACTS WITH MULTIPLE PERFORMANCE OBLIGATIONS ➢ Goal: Separate complex contracts into parts that can be viewed on a stand-alone basis. Steps 2 and 4 are critical to this process. ➢ Step 2: Identify the performance obligation(s) in […]

Accounting Chapter 5 Homework Note These General Conditions Typically Will Lead

T5–41 Instructor’s Resource Manual, Chapter 5 5-61 Copyright © 2015 McGraw-Hill Education. All rights reserved. DUPONT FRAMEWORK ➢ The DuPont Framework helps identify how profitability, activity, and financial leverage trade off to determine return to shareholders: Return on equity = […]

Accounting Chapter 5 Homework Or Company Could Defer Too Much Revenue

Intermediate Accounting, 8/e 5–141 Problem 5–19 (continued) 2017 Installment receivables …………………………………………… 400,000 Inventory …………………………………………………………… 280,000 Deferred gross profit …………………………………………… 120,000 To record installment sales Cash …………………………………………………………………….. 250,000 Installment receivables ……………………………………….. 250,000 To record cash collections from installment sales Deferred gross […]

Accounting Chapter 5 Homework Question 526 Receivables Turnover Ratio Net Sales

Intermediate Accounting, 8/e 5–1 Chapter 5 Revenue Recognition and Profitability Analysis QUESTIONS FOR REVIEW OF KEY TOPICS Question 5–1 The five key steps in applying the core revenue recognition principle are: 1. Identify the contract with a customer. 2. Identify […]

Accounting Chapter 5 Homework Requirement Under The Expected Cost Plus Margin

Intermediate Accounting, 8/e 5–41 Exercise 5–7 (concluded) Requirement 3 Value of the coupon: 40% discount $125 carriage fee = $ 50 Estimated redemption 30% Stand-alone selling price of coupon $ 15 Stand-alone selling price of a normal subscription […]

Accounting Chapter 5 Homework Review Questions Continued 2016 Actual Costs 20000

Intermediate Accounting, 8/e 5–81 Exercise 5–31 Requirement 1 Cost of goods sold ($1,000,000 – 600,000) $400,000 Add: Gross profit if using cost recovery method 100,000 Cash collected $500,000 Requirement 2 Gross profit percentage = $600,000 ÷ $1,000,000 = 60% Cash […]

Accounting Chapter 5 Homework Therefore Super Rise Will Revise The Transaction

Intermediate Accounting, 8/e 5–101 Problem 5-2 (concluded) Requirement 3 Creative then allocates the total selling price based on stand-alone selling prices, as follows: The journal entry to record the sale is: Cash ($780 × 100,000 units) 78,000,000 Sales revenue 74,100,000 […]

Accounting Chapter 5 Homework To record cash collections from installment sales

Student Name: Class: Requirement 1: 2016 Cost recovery %: $180,000 $300,000 = 60% =40% Correct! Requirement 2: Date Account Debit Credit 2016 300,000 Correct! 180,000 120,000 120,000 120,000 48,000 48,000 2017 400,000 Correct! 280,000 120,000 250,000 250,000 85,000 85,000 To […]

Accounting Chapter 5 Homework We can calculate gross profit directly as

Intermediate Accounting, 8/e 5–61 Exercise 5–21 SUMMARY Revenue Recognized Over Time Revenue Recognized Upon Completion Situation 2016 2017 2018 2016 2017 2018 1 $166,667 $233,333 $100,000 $0 $0 $500,000 2 $166,667 $(66,667) $100,000 $0 $0 $200,000 3 $166,667 $(266,667) $(100,000) […]

Accounting Chapter 5 Homework When other parties are involved in providing goods

Case 5–7 (concluded) In the future, when a card is redeemed, the deferred revenue account would be reduced and revenue recognized for deferred revenue related to ten punches. Sales of ice cream cones to people who do not have cards […]

Accounting Chapter 5 How Much The Transaction Price Would Allocated

construction contracts c. Cost of construction 2,000,000 Gross profit 1,000,000 Revenue from long-term construction contracts 3,000,000 d. Construction in progress 1,200,000 Cost of construction 600,000 Revenue from long-term construction contracts 1,800,000 Answer: d Level of Learning: 3 Hard Learning Objective: […]

Accounting Chapter 5 March 20 Three The Most Senior Drivers

Use the following information for questions 256-257 On July 1, Wiggins Associates enters into a contract to provide consulting services to Pennsylvania University (PU). The contract is anticipated to last four months and is intended to achieve significant cost savings […]

Accounting Chapter 5 Pac The Pac Contract Price 150 Million

287. Assume that, on April 1, 2016, a customer visits MicrosoftStore.com and purchases Microsoft Windows 7 Ultimate for $170. Windows 7 Ultimate comes in a DVD format which the customer can use permanently, and Microsoft does not expect that its […]

Accounting Chapter 5 Recognition of franchise fee revenue is dependent on judgments of

74. When the cost recovery method is used to account for a long-term construction contract under IFRS, an equal amount of cost and revenue is typically recognized during the early life of the contract, such that high initial gross profit […]

Accounting Chapter 5 Sellers should recognize revenue over time for a long term

True/False Questions 1. Companies recognize revenue when goods or services are transferred to customers for the amount the company expects to be entitled to receive in exchange for those goods or services. Answer: True Level of Learning: 1 Easy Learning […]

Accounting Chapter 5 What Sdhs Journal Entry Record Revenue

AACSB: Analytic AICPA: FN Risk Analysis Feedback: Avg. collection period = 365 / (accounts receivable turnover) = 365 / (net sales / {avg A/R}) = 365 / (115 /{20 + 16} /2) = 57.13 days 192. Dowling’s return on equity […]

Accounting Chapter 6 Homework Amount of money paid/received in excess of

Exercise 6–19 Requirement 1 PVA = $400,000 (10.59401* ) = $4,237,604 = Liability * Present value of an ordinary annuity of $1: n = 20, i = 7% (from Table 4) Requirement 2 PVAD = $400,000 (11.33560* ) = $4,534,240 […]

Accounting Chapter 6 Homework An ordinary annuity exists when the cash flows occur

Question 6–1 Interest is the amount of money paid or received in excess of the amount borrowed or lent. Question 6–2 Compound interest includes interest not only on the original invested amount but also on the accumulated interest from previous […]

Accounting Chapter 6 Homework Present Value Ordinary Annuity 1 N20 I6

FUTURE VALUE OF AN ANNUITY DUE Sally Rogers wants to accumulate a sum of money to pay for graduate school. Rather than investing a single amount today that will grow to a future value, she decides to invest $10,000 […]

Accounting Chapter 6 Homework Present Value Techniques Annuities Because Financial Instruments

CHAPTER 6 TIME VALUE OF MONEY CONCEPTS Overview Time value of money concepts, specifically future value and present value, are essential in a variety of accounting situations. These concepts and the related computational procedures are the subjects of this chapter. […]

Accounting Chapter 6 Homework The Companys Balance Sheet Would Include Liability

Problem 6–11 Requirement 1 PVAD = Annuity amount x Annuity factor Annuity amount = PVAD Annuity factor Annuity amount = $800,000 7.24689* * Present value of an annuity due of $1: n = 10, i = 8% (from Table 6) […]

Accounting Chapter 6 Homework Use the Present and Future Value Tables in the text

Student Name: Class: Yearly Time Interest Cash Flow Period Rate *Factor PVA PV Years 1-5 70,000$ 5 8% 3.99271 279,490$ Years 6-10 70,000 5 10% 3.79079 265,355 Problem 06-05 McGraw-Hill/Irwin Instructor Estimated Cash Flows CLAUSSEN PURCHASE 265,355 5 8% 0.68058 […]

Accounting Chapter 6 Objective 0607 topic Area Present Value Annuity Due blooms

Chapter 6 Time Value of Money Concepts True/False Questions 1. Compound interest includes interest earned on interest. Answer: True Level of Learning: 1 Easy Learning Objective: 06-01 Topic Area: Simple versus compound interest Blooms: Remember AACSB: Reflective Thinking AICPA: BB […]

Accounting Chapter 6 Present Value Ordinary annuity 2 Effective Yield 3 Monetary Liability4

Chapter 6 Time Value of Money Concepts 59. Zulu Corporation hires a new chief executive officer and promises to pay her a signing bonus of $2 million per year for 10 years, starting five years after she joins the company. […]

Accounting Chapter 6 The bonds pay no interest during the period of time

Chapter 6 Time Value of Money Concepts Intermediate Accounting, Eighth Edition, Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 6–39 93. Bison Mfg. is considering two options for […]