Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

Topic Area: Types of assets

Topic Area: Costs to be capitalized

Topic Area: Noncash acquisitions ‒ Deferred payments

Topic Area: Dispositions

Topic Area: Exchanges

Topic Area: Self-constructed assets

Blooms: Understand

AACSB: Reflective thinking

AICPA: BB Critical Thinking

AICPA: FN Measurement

Problems

93. On July 1, 2016, Jekel & Hyde Inc. purchased land and incurred other costs relative to the

construction of a new warehouse. A summary of economic activities is listed below:

Purchase price

$185,000

Title insurance

$1,500

Legal fees to purchase land

$1,000

Cost of razing old building on lot

8,500

Proceeds from sale of salvageable materials

(1,200

)

Property taxes, January 1, 2016–June 30, 2016

3,000

Cost of grading and filling building site

9,000

Cost of building construction

620,000

Interest on construction loan

12,000

Cost of constructing driveway

8,000

Cost of parking lot and fencing

12,000

Required:

Indicate the accounts that would be affected by the above transactions and the resulting

balance in each account. Apply the interest on the construction loan to the cost of the building

only.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

94. Mad Hatter Enterprises purchased new equipment for $365,000, terms f.o.b. shipping point.

Other costs connected with the purchase were as follows:

State sales tax

29,200

Freight costs

5,600

Insurance while in transit

800

Insurance after equipment placed in service

1,200

Installation costs

2,000

Insurance for the first year of operations

2,400

Testing

700

Required:

Determine the capitalized cost of the equipment.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

95. During the current year, Brewer Company acquired all of the outstanding common stock of

Miller Inc. paying $12,000,000 cash. The book values and fair values of Miller's assets and

liabilities acquired are listed below:

Book Value

Fair Value

Accounts receivable

$1,800,000

$ 1,625,000

Inventories

2,700,000

4,000,000

Property, plant, and equipment

9,000,000

11,625,000

Accounts payable

3,000,000

3,000,000

Bonds payable

4,500,000

4,125,000

Required:

Prepare the journal entry to record the acquisition by Brewer Company.

96. On August 15, 2016, Willis Inc. acquired all of the outstanding common stock of Bork Inc.

paying $7,400,000 cash. The book values and fair values of Willis' assets and liabilities are

listed below:

Book Value

Fair Value

Accounts receivable

$1,080,000

$ 975,000

Inventories

1,620,000

2,400,000

Property, plant, and equipment

5,400,000

6,975,000

Accounts payable

1,800,000

1,800,000

Bonds payable

2,700,000

2,475,000

Required:

Prepare the journal entry to record the acquisition by Willis Inc.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

Use the following to answer questions 97 and 98:

In its 2013 annual report to shareholders, Boston Beer Company, Inc. included the following in a

disclosure note:

E. Property, Plant and Equipment

Property, plant and equipment for the years ended December 28, 2013, and December 29, 2012,

consisted of the following ($ in thousands):

2013

2012

Machinery and plant equipment

$ 259,664

$183,828

Kegs

60,350

46,899

Land

23,260

24,515

Building and building improvements

44,234

36,667

Office equipment and furniture

14,581

12,580

Leasehold improvements

7,600

6,193

409,689

310,682

Less: accumulated depreciation

143,131

120,734

$266,558

$189,948

The Company recorded depreciation related to these assets of $23,565 thousand in the 2013 fiscal

year.

Also, Boston Beer reported the following information in the annual report ($ in thousands):

Years ended

12/28/13

12/29/12

Cash flows for investing

activities:

Purchases of property,

plant, and equipment

(100,655)

(66,010)

Proceeds on disposal of

property, plant, and equipment

18

41

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

97. Use a T- account to show the balances and changes during 2013 in Boston Beer's: Property,

Plant and Equipment account and its Accumulated depreciation—Property, Plant &

Equipment account.

98. Show the journal entry to record Boston Beer's sale of property, plant and equipment during

2013.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

Use the following to answer questions 99 and 100:

In its 2016 annual report to shareholders, Plank Breweries included the following note:

Fixed Assets

Fixed assets consist of the following (in $ thousands):

December 31,

2016

2015

Brewery and retail

$ 14,465

$ 14,246

Equipment

Furniture and fixtures

918

772

Leasehold improvements

13,808

13,563

Construction in progress

584

165

Assets held for sale

_______

4

29,775

28,750

Less accumulated depreciation

(9,555

)

(7,625

)

$ 20,220

$ 21,125

Total depreciation expense was approximately $2.121 million and $2.179 million for the years ended

December 31, 2016 and 2015, respectively.

Also, Plank Breweries reported the following information in its annual report (in $ thousands):

Years Ended December 31,

2016

2015

Acquisition of fixed assets

1,279

808

Proceeds from sale of fixed assets

15

157

Required:

99. Use a T- account to show the balances and changes during 2016 in Plank Breweries:

Fixed assets account and Accumulated depreciation—fixed assets account (in $ thousands).

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

100. Show the journal entry to record Plank's disposal of the fixed assets during 2016.

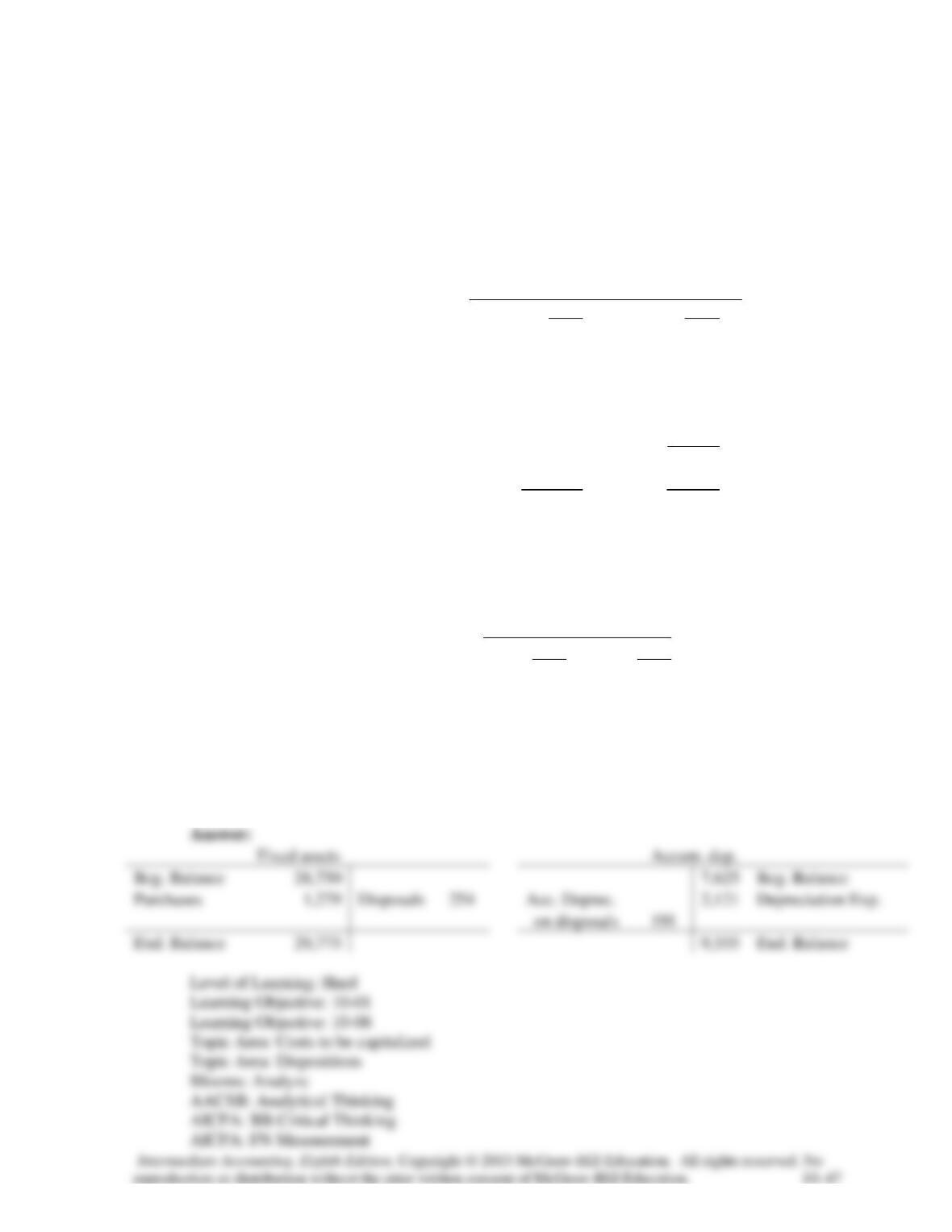

101. In its 2016 annual report to shareholders, Custard Cup Inc. included the following note:

Note 4 Property, Plant, and Equipment

Property, plant, and equipment (PPE) at December 31, 2016, and December 31, 2015,

consisted of the following:

2016

2015

(In millions)

Machinery and equipment

$244

$237

Buildings and

90

89

improvements

Office furniture and

6

6

fixtures

_______

_______

340

332

Less: Accumulated

depreciation and

183

165

Amortization

_______

_______

157

167

Land

15

15

Construction in progress

24

6

$196

$188

Depreciation expense for property, plant and equipment was $26 million in 2016.

Required: Compute the Accumulated depreciation on PPE disposed of by Custard Cup during

2016.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

102. Schefter Mining operates a copper mine in Wyoming. Acquisition, exploration, and

development costs totaled $8.2 million. Extraction activities began on July 1, 2016. After the

copper is extracted in approximately six years, Schefter is obligated to restore the land to its

original condition, including constructing a park. The company’s controller has provided the

following three cash flow possibilities for the restoration costs:

Cash Flow Probability

1. $700,000 30%

2. 800,000 25%

3. 900,000 45%

The company’s credit-adjusted, risk-free rate of interest is 5%, and its fiscal year ends on

December 31.

Required:

1. What is the initial cost of the copper mine? (Round computations to nearest whole dollar.)

2. How much accretion expense will Schefter report in its 2016 income statement?

3. What is the book value of the asset retirement obligation that Schefter will report in its

2016 balance sheet?

4. Assume that actual restoration costs incurred in 2022 totaled $860,000. What amount of

gain or loss will Schefter recognize on retirement of the liability?

Answer:

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

103. Calegari Mining paid $2 million to obtain the rights to operate a coal mine in Tennessee.

Costs of exploring for the coal deposit totaled $1,500,000, and development costs of $5

million were incurred in preparing the mine for extraction, which began on January 2, 2016.

After the coal is extracted in approximately five years, Calegari is obligated to restore the land

to its original condition. The company’s controller has provided the following three cash flow

possibilities for the restoration costs:

Cash Flow Probability

1. $1,000,000 10%

2. 1,400,000 60%

3. 1,800,000 30%

The company’s credit-adjusted, risk-free rate of interest is 7%, and its fiscal year ends on

December 31.

Required:

1. What is the initial cost of the coal mine? (Round computations to nearest whole dollar.)

2. How much accretion expense will Calegari report in its 2016 and 2017 income

statements?

3. What is the book value of the asset retirement obligation that Calegari will report in its

2016 and 2017 balance sheets?

4. Assume that actual restoration costs incurred in 2021 totaled $1,370,000. What amount of

gain or loss will Calegari recognize on retirement of the liability?

Answer:

104. During the current year, Peterson Data Corporation acquired all of the outstanding common

stock of Junior Jackson Inc. (JJI), paying $36 million in cash. Peterson recorded the assets

acquired as follows:

Accounts receivable

$2,500,000

Inventory

9,000,000

Property, plant, and equipment

25,500,000

Goodwill

6,000,000

The book value of JJI's assets and owners' equity before the acquisition were $22 million and

$18 million, respectively.

Required: Compute the fair value of JJI's liabilities that Peterson assumed in the acquisition.

105. During the current year, Compton Crate Corporation acquired all of the outstanding common

stock of Little Lacy Ltd. (LLL), paying $60 million in cash. Compton recorded the assets

acquired as follows:

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

Accounts receivable

$5,500,000

Inventory

18,000,000

Property, plant, and equipment

45,500,000

Goodwill

22,000,000

The book value of LLL's assets and owners' equity before the acquisition were $50 million

and $30 million, respectively.

Required: Compute the fair value of LLL's liabilities that Compton assumed in the

acquisition.

106. On January 3, 2016, Michelson & Sons acquired a tract of land just outside the city limits. The

land and existing building were purchased for $2.4 million. Michelson paid $400,000 and

signed a noninterest-bearing note requiring the company to pay the remaining $2,000,000 on

December 31, 2017. An interest rate of 7% properly reflects the time value of money for this

type of loan agreement. Transfer taxes, title insurance, and other costs totaling $24,000 were

paid at closing.

During February, the old building was demolished at a cost of $120,000, and an additional

$100,000 was paid to clear and grade the land. Construction of a new building began on

March 1 and was completed on October 30. Construction expenditures were as follows:

March 30 $ 800,000

June 30 1,200,000

July 30 1,200,000

September 1 600,000

Michelson did not borrow specifically for the construction project, but did have the

following debt outstanding throughout 2016:

$6,000,000, 8% long-term note payable

$2,000,000, 5% long-term note payable

In December, the company purchased equipment and office furniture and fixtures for a

lump-sum price of $800,000. The fair values of the equipment and the furniture and fixtures

were $540,000 and $360,000, respectively. In December, Michelson paid $340,000 for the

construction of parking lots and landscaping.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

Required:

1. Determine the initial values of the various assets that Michelson acquired or constructed

during 2016.

2. How much interest expense will Michelson report in its 2016 income statement?

Answer:

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

107. Watson Company purchased assets of Holmes Ltd. at auction for $1,300,000. An independent

appraisal of the fair value of the assets acquired is listed below:

Land

$214,500

Building

357,500

Equipment

572,000

Inventories

286,000

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

Required:

Prepare the journal entry to record the purchase of the assets.

Answer:

108. Eli Company purchased assets of Whitney Inc. at auction for $1,560,000. An independent

appraisal of the fair value of the assets acquired is listed below:

Land

$171,600

Building

514,800

Equipment

600,600

Inventories

429,000

Required:

Prepare the journal entry to record the purchase of the assets.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

109. Cool Globe Inc. entered into two transactions, as follows:

1. Purchased equipment paying $20,000 down and signed a noninterest-bearing note requiring

the balance to be paid in four annual installments of $20,000 on the anniversary date of the

contract. Based on Cool Globe's 12% borrowing rate for such transactions, the implicit

interest cost is $19,253.

2. Purchased a tract of land in exchange for $10,000 cash down payment and a noninterest-

bearing note requiring five $10,000 annual payments, with the first annual payment in one

year. The fair value of the land is $46,000.

Required:

Prepare the journal entries for these transactions.

110. Beacon Inc. received a gift of land and building in Twin Pines Park as an inducement to

relocate. The land and buildings have fair values of $45,000 and $455,000.

Required: Prepare journal entries to record the above transactions.