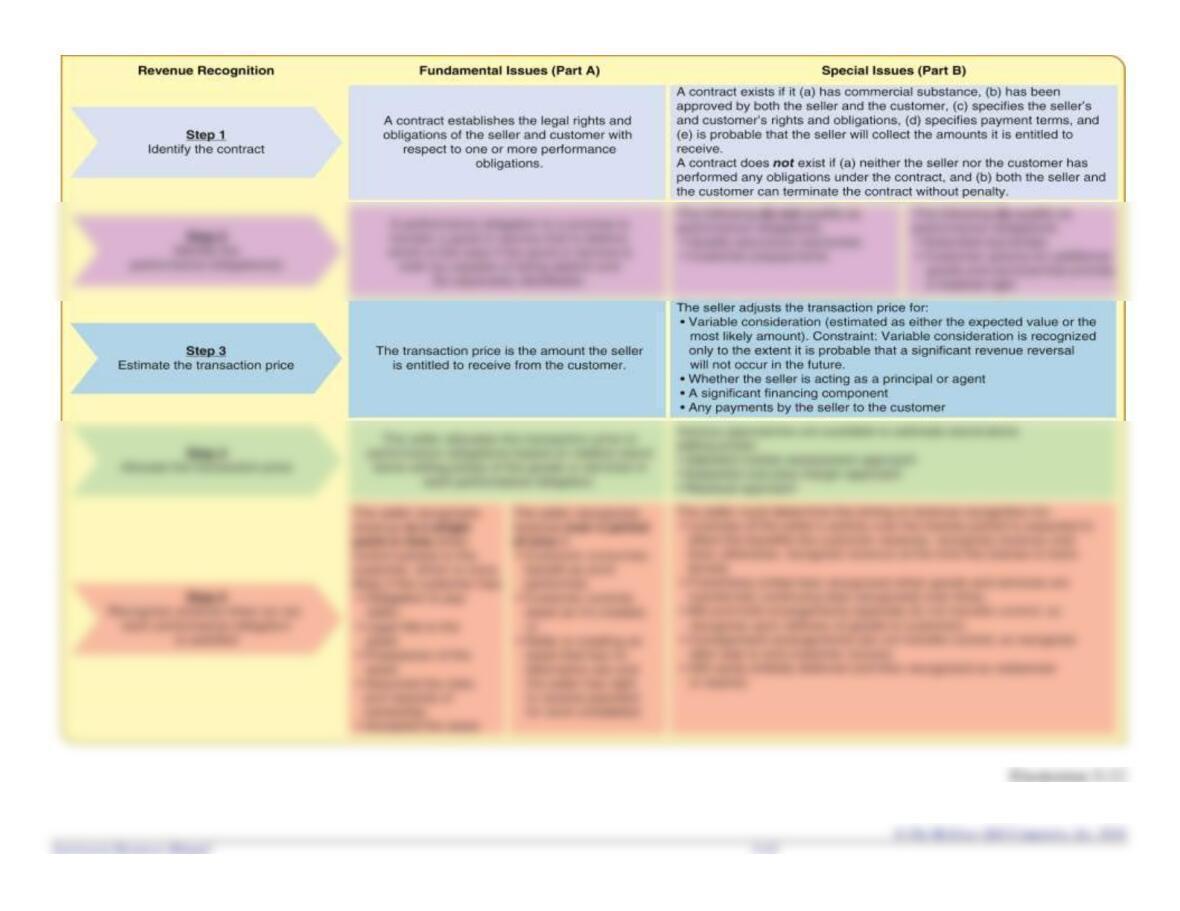

FRANCHISE ARRANGEMENTS

• Assume that TrueTech starts selling TechStop franchises. TrueTech charges

franchisees an initial fee in exchange for (a) the exclusive right to operate the

only TechStop in a particular area for a five-year period, (b) the equipment

necessary to distribute and repair TrueTech products, and (c) training services

to be provided over a two-year period. Similar equipment and training can be

purchased elsewhere. What are the performance obligations in this

arrangement, and when would TrueTech recognize revenue for each of them?

Determining the performance obligations:

▪ The exclusive five-year right to operate the only TechStop in a particular

area is distinct because it can be used with other goods or services

• TrueTech would allocate the initial franchise fee to three separate performance

obligations based on their relative stand-alone prices: (1) the right to operate a

TechStop, (2) equipment, and (3) training. TrueTech would recognize revenue

• What if TrueTech also charges franchisees an additional fee for ongoing

services provided by TrueTech? In that case, TrueTech would recognize

T5-28

REVENUE DISCLOSURES

➢ Income Statement: Include

Revenue,

components.

➢ Balance Sheet: Include

Accounts Receivable: Unconditional right to receive payment, depending

➢ Disclosure: Lots of it.

Goal, help investors understand the nature, amount, timing and uncertainty

of revenues and cash flows.

Required disclosures include:

T5-29

T5-30

COMPANIES ENGAGED IN LONG-TERM CONTRACTS

Company Type of Industry or Product

Oracle Corp. Computer software, license and consulting fees

Lockheed Martin Corporation Aircraft, missiles and spacecraft

Hewlett-Packard Information technology

Northrop Grumman Newport News Shipbuilding

Nortel Networks Corp Networking solutions and services to support

Illustration 5-23

T5–31

RECOGNIZING REVENUE FOR LONG–TERM CONTRACTS

Applying the 5-step process to long-term contracts is complicated in two ways:

➢ Step 2, “Identify the performance obligation(s) in the contract,” is important

because long-term contracts typically include many products and services that

could be viewed as separate performance obligations.

These products and services are capable of being distinct, but

➢ Step 5, “Recognize revenue when (or as) each performance obligation is

satisfied,” is important because there can be a big difference for long-term

contracts between recognizing revenue over time and recognizing revenue only

when the contract has been completed. Most long-term contracts qualify for

revenue recognition over time, either because

the seller is creating an asset that the customer controls as it is completed, or

T5–32

RECOGNIZING REVENUE FOR LONG-TERM CONTRACTS

AT A POINT IN TIME VS. OVER TIME

At the beginning of 2016, the Harding Construction Company received a contract to

build an office building for $5 million. The project is estimated to take three years to

complete. According to the contract, Harding will bill the buyer in installments over

the construction period according to a prearranged schedule. Information related to

the contract is as follows:

2016 2017 2018

Construction costs incurred

during the year $1,500,000 $1,000,000 $1,600,000

Construction costs incurred

Illustration 5–24

T5–33

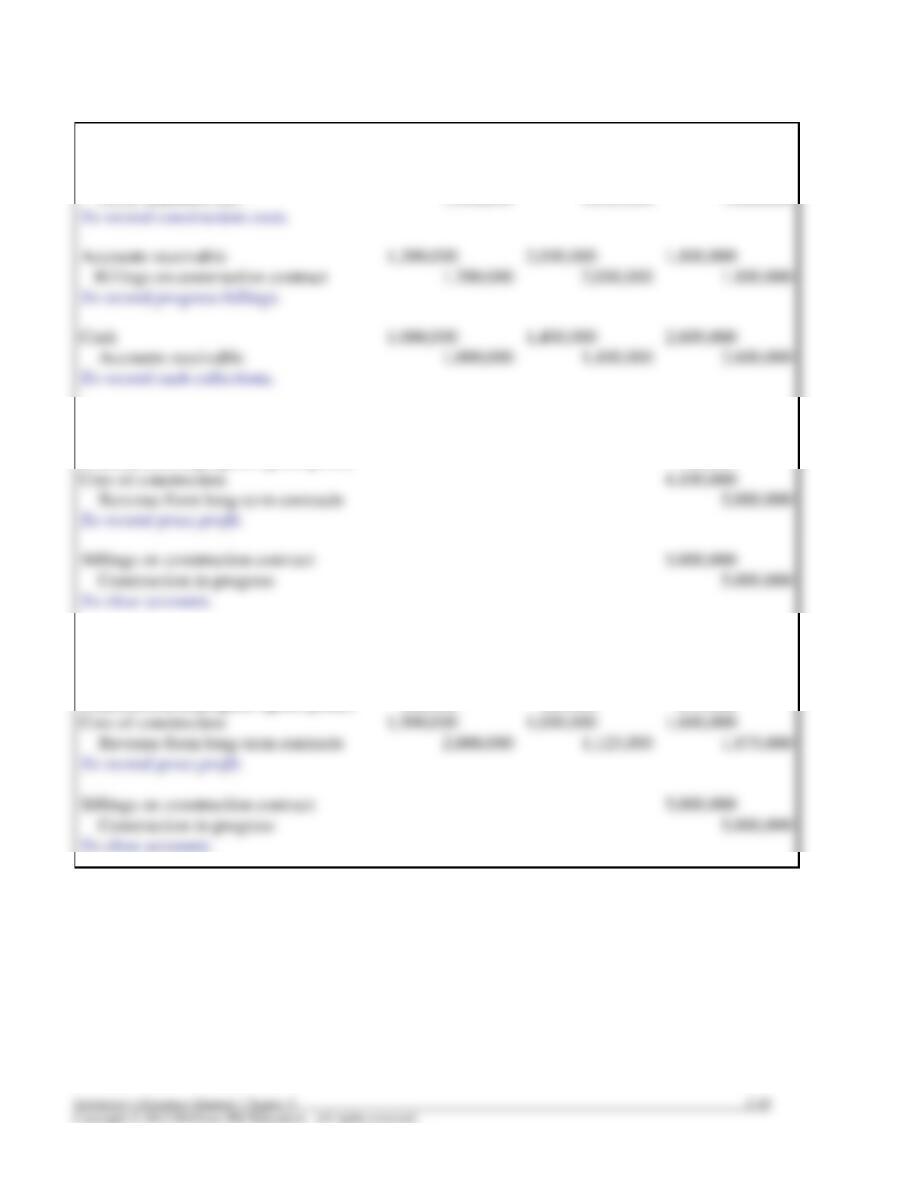

JOURNAL ENTRIES

2016

2017

2018

BOTH APPROACHES:

Construction in progress

1,500,000

1,000,000

1,600,000

Cash, materials, etc.

1,500,000

1,000,000

1,600,000

Accounts receivable

1,200,000

2,000,000

1,800,000

Billings on construction contract

1,200,000

2,000,000

1,800,000

Cash

1,000,000

1,400,000

2,600,000

Accounts receivable

1,000,000

1,400,000

2,600,000

REVENUE RECOGNIZED UPON

COMPLETION:

Construction in progress (gross profit)

900,000

Cost of construction

Revenue from long-term contracts

Billings on construction contract

Construction in progress

REVENUE RECOGNIZED OVER

TIME ACCORDING TO

PERCENTAGE-OF-COMPLETION:

Construction in progress (gross profit)

500,000

125,000

275,000

Cost of construction

1,500,000

1,000,000

1,600,000

Revenue from long-term contracts

2,000,000

1,125,000

1,875,000

Billings on construction contract

5,000,000

Construction in progress

5,000,000

Illustrations 5-24a,b,e

T5–34

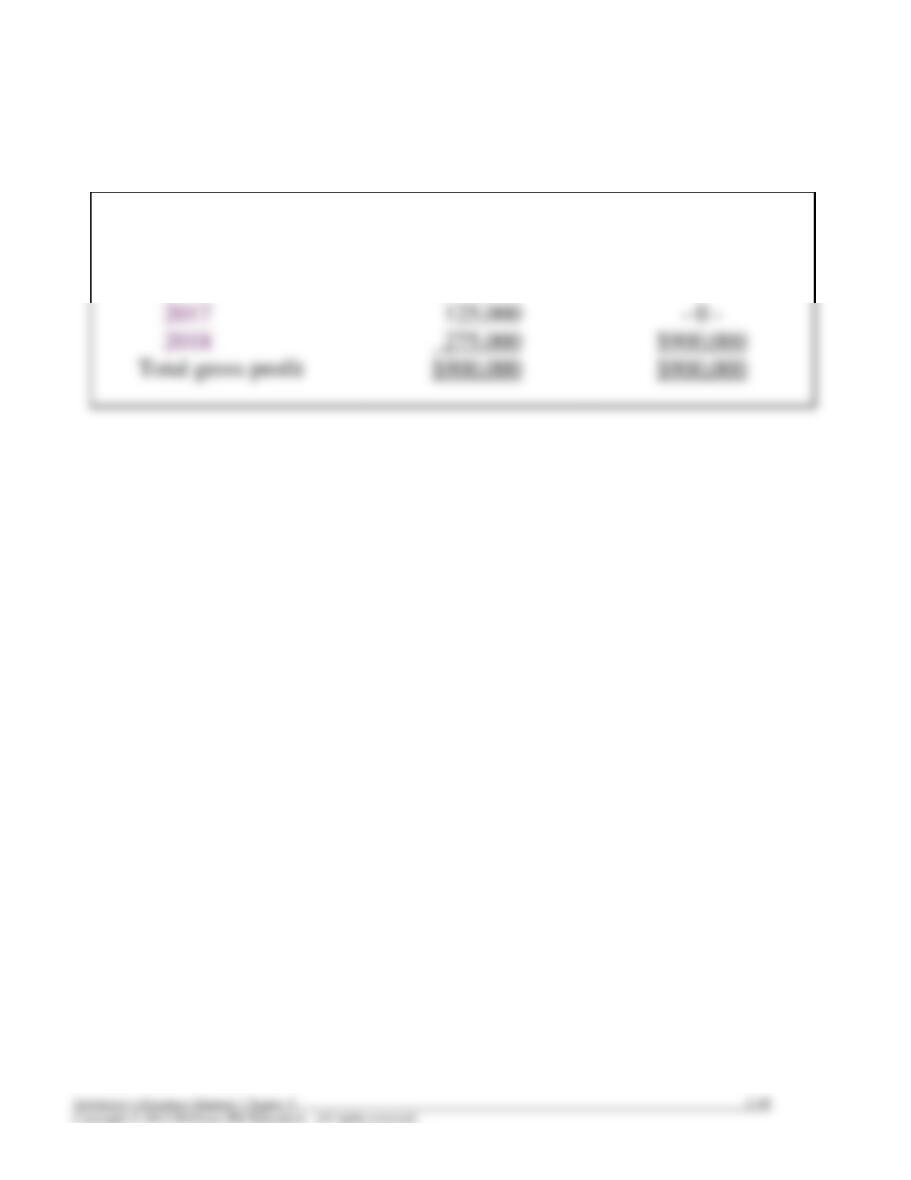

THE SAME TOTAL INCOME IS RECOGNIZED

REGARDLESS OF REVENUE TIMING

Over Time

Upon Completion

Gross profit recognized:

2016

$500,000

– 0 –

$900,000

T5–35

CALCULATING REVENUE

RECOGNIZED OVER TIME

2016

2017

2018

Construction costs:

Construction costs incurred during the year

$1,500,000

$1,000,000

$1,600,000

Construction costs incurred in prior years

-0-

1,500,000

2,500,000

Actual construction costs to date

$1,500,000

$2,500,000

$4,100,000

Estimated remaining costs to complete

1,500,000

Total cost (estimated + actual)

$3,750,000

$4,000,000

$4,100,000

Contract price

$5,000,000

$5,000,000

$5,000,000

Multiplied by:

X

X

X

Equals:

Cumulative revenue earned to date

$2,000,000

$3,125,000

Minus:

Revenue recognized in prior periods

– 0-

(2,000,000)

(3,125,000)

$1,125,000

(in thousands)

Cost of construction

1,500

1,000

1,600

Revenue from long-term contracts

2,000

1,125

1,875

Equals:

_________

__________

_________

Ilustration 5-24c

T5–36

REVENUE AND COST OF CONSTRUCTION:

REVENUE RECOGNIZED OVER TIME

2016

Revenue recognized in 2016 ($5,000,000 x 40%)

$2,000,000

Cost of construction

Gross profit

$ 500,000

2017

Revenue recognized to date ($5,000,000 x 62.5%)

$3,125,000

Less: Revenue recognized in 2016

Revenue recognized in 2017

$1,125,000

Cost of construction

2018

Revenue recognized to date ($5,000,000 x 100%)

$5,000,000

Less: Revenue recognized in 2016 and 2017

Revenue recognized in 2018

$1,875,000

Cost of construction

Illustration 5-24d

T5–37

BALANCE SHEET PRESENTATION

Balance Sheet

(End of year)

2016

2017

Projects for which Revenue Recognized Upon Completion:

Current assets:

Accounts receivable

$ 200,000

$800,000

Costs ($1,500,000) in excess of billings ($1,200,000)

300,000

Current liabilities:

Billings ($3,200,000) in excess of costs ($2,500,000)

700,000

According to Percentage of Completion:

Accounts receivable

Costs and profit ($2,000,000) in excess of billings ($1,200,000)

Billings ($3,200,000) in excess of costs and profit ($3,125,000)

Illustration 5-24f

T5–38

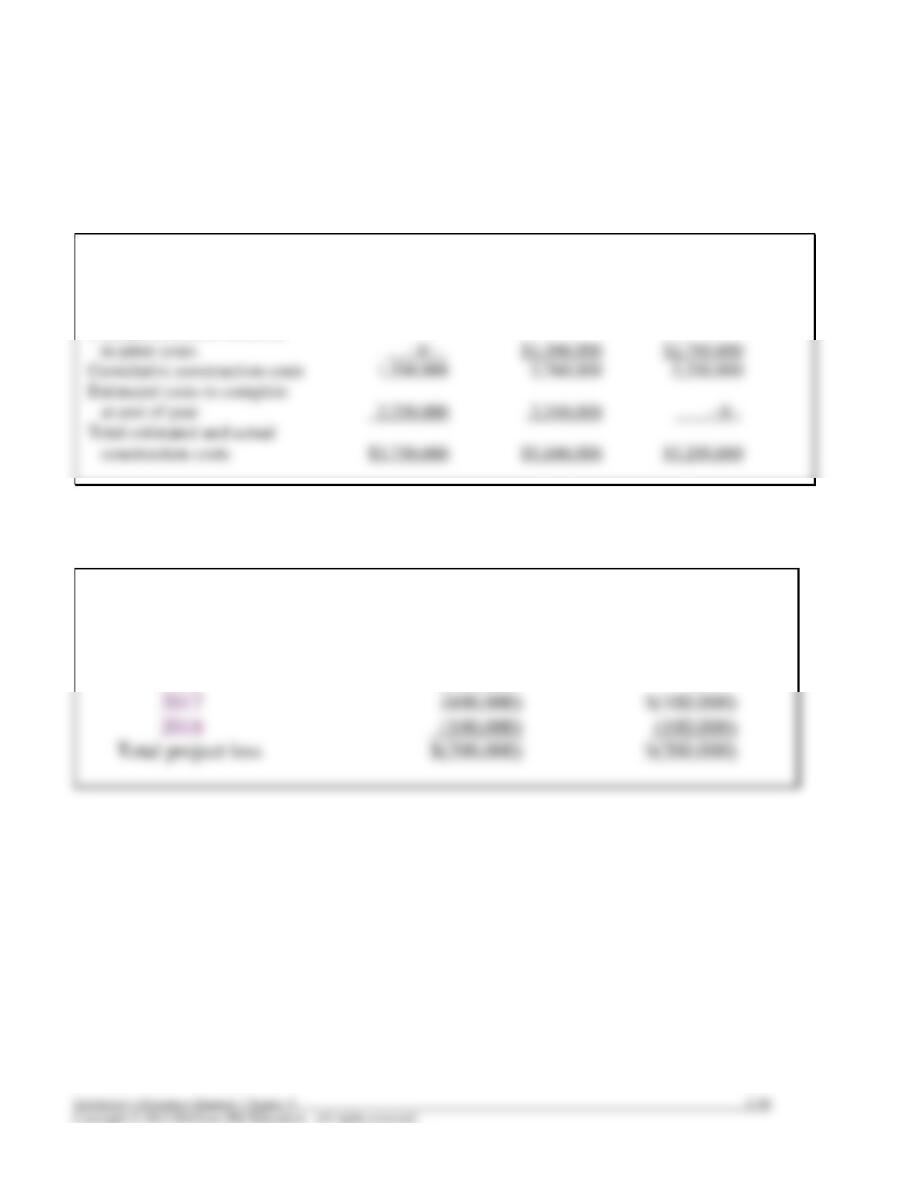

LONG-TERM CONTRACT LOSSES

➢ An estimated loss on a long-term contract is fully recognized in the first period that

the loss is anticipated, regardless of the revenue recognition method used.

2016 2017 2018

Construction costs incurred

during the year $1,500,000 $1,260,000 $2,440,000

Construction costs incurred

Comparison of Periodic Gross Profit (Loss)

Percentage-of–

completion

Completed Contract

Gross profit (loss) recognized:

2016

$500,000

– 0 –

2018

T5–39

ACTIVITY RATIOS

➢ Activity ratios measure a company’s efficiency in managing its assets.

Asset turnover ratio = Net sales

Average total assets

T5–40

PROFITABILITY RATIOS

➢ Profitability ratios assist in evaluating various aspects of a company’s profit-making

activities.

Profit margin on sales = Net income

Net sales

Return on assets = Net income

Average total assets

Return on shareholders’ = Net income

equity Average total equity