Exercise 9–24

1. To include the $4 million in year 2016 purchases and increase retained earnings

to what it would have been if 2015 cost of goods sold had not included the $4

million purchases:

Analysis:

2015 2016

Beginning inventory Beginning inventory

Purchases O Purchases U

Less: Ending inventory

Cost of goods sold O

2. The 2015 financial statements that were incorrect as a result of the errors would

3. A “prior period adjustment” to retained earnings would be reported, and a

Exercise 9–25

Requirement 1

The $42,000 should have been charged to purchases instead of advertising

expense. This error caused 2015 net purchases and thus cost of goods sold to be

understated and advertising expense to be overstated by $42,000. The understatement

of ending inventory for the $30,000 in merchandise held on consignment caused 2015

cost of goods sold to be overstated.

Analysis: U = Understated

O = Overstated

2015

Beginning inventory

Plus: net purchases U by 42,000

Requirement 2

Exercise 9–26

List A List B

e 1. Gross profit ratio a. Reduction in selling price below the original

selling price.

Exercise 9–27

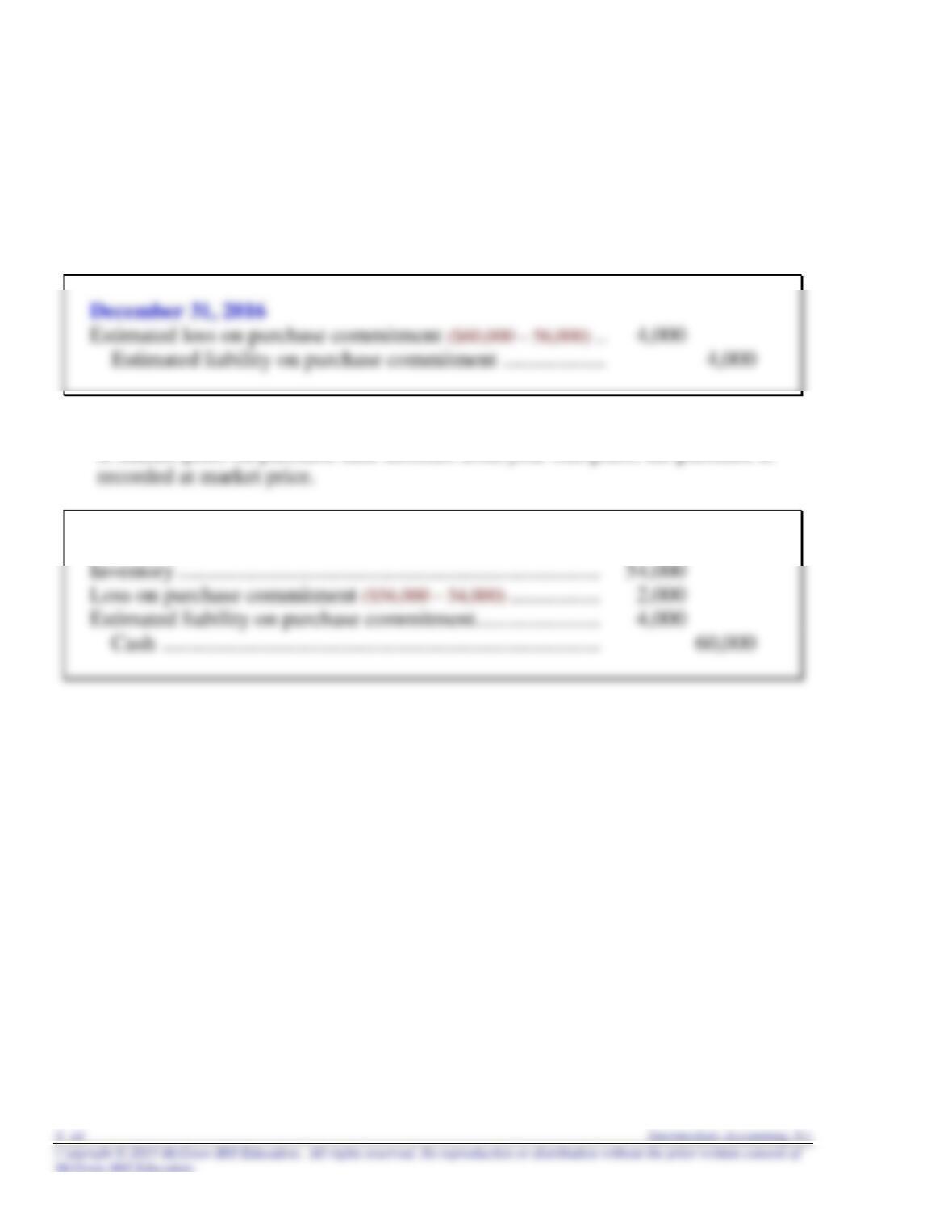

Requirement 1

If market price at year-end is less than contract price for outstanding purchase

commitments, a loss is recorded for the difference.

Requirement 2

If market price on purchase date declines from year-end price, the purchase is

March 21, 2017

Exercise 9–28

If market price is less than the contract price, the purchase is recorded at the

market price.

June 15, 2016

Purchases (market price) ………………………………………………… 85,000

June 30, 2016

If market price on purchase date declines from year-end price, the purchase is

recorded at market price.

August 20, 2016

Purchases (market price) ………………………………………………… 120,000

9–46 Intermediate Accounting, 8/e

CPA / CMA REVIEW QUESTIONS

CPA Exam Questions

1. c. Net realizable value = 388,000 ($408,000 selling price – $20,000 costs to

sell.)

2. c.

Inventory, 1/1 $ 80,000

Add: Purchases 330,000

CPA Exam Questions (concluded)

3. d.

Cost Retail

Beginning inventory and purchases $600,000 $920,000

Net markups _______ 40,000

4. c. The understatement of beginning inventory and the overstatement of ending

9–48 Intermediate Accounting, 8/e

CMA Exam Questions

1. b. The conventional retail inventory method adds beginning inventory, net

purchases, and markups (but not markdowns) to calculate a cost percentage.

2. d. The failure to record a sale means that both accounts receivable and sales

3. d. The overstatement (double counting) of inventory at the end of year 1

caused year 1 cost of goods sold (BI + Purchases – EI) to be understated and

Problem 9–1

Requirement 1

Product

NRV per unit

A

$16 – (15% x $16) = $13.60

B

$18 – (15% x $18) = $15.30

C

$ 8 – (15% x $8) = $ 6.80

D

$ 6 – (15% x $6) = $ 5.10

$13 – (15% x $13) = $11.05

(1)

(2)

Product

(units)

Cost

NRV

Inventory

Value

[Lower of

(1) and (2)]

A (1,000)

$10,000

$13,600

$10,000

B (800)

12,000

12,000

C (600)

1,800

4,080

1,800

D (200)

1,400

1,020

1,020

E (600)

8,400

6,630

6,630

$33,600

$31,450

Requirement 2

Inventory book value would be $31,450, the lower of aggregate inventory cost

PROBLEMS

9–50 Intermediate Accounting, 8/e

Problem 9–2

Requirement 1

Lower of cost and NRV

Product

Cost

Net

Realizable

Value

(a)

By

Individual

Products

(b)

By

Product

Type

(c)

By Total

Inventory

Tools:

Hammers

$ 500

$ 550

$ 500

Saws

2,000

1,800

1,800

Screwdrivers

600

780

600

$3,100

$3,130

$3,100

Paint products:

1-gallon cans

2,500

Paint brushes

400

450

400

$3,400

$2,950

2,950

$6,500

$6,080

$5,800

$6,050

$6,080

Requirement 2

(a) Individual products

Problem 9–3

Requirement 1

Fruit Marshmallow Chocolate

Toppings Toppings Topping

Estimate of cost of goods sold:

Cost percentage 80% 70% 65%

x Net sales $200,000 $55,000 $20,000

Requirement 2

The two main factors that could cause the estimates of the inventory lost to be

over- or understated are:

9–52 Intermediate Accounting, 8/e

Problem 9–4

1. Average cost

Cost

Retail

Beginning inventory

$ 90,000

$180,000

Plus: Purchases

355,000

580,000

Freight-in

Less: Purchase returns

(7,000)

Less: Net markdowns

Abnormal spoilage

Goods available for sale

442,200

745,000

Less:

Normal spoilage

(3,000)

Sales:

Net sales ($540,000 – 10,000)

Estimated ending inventory at retail

$208,000

Estimated ending inventory at cost (59.36% x $208,000)

Estimated cost of goods sold

$318,731

Problem 9–4 (concluded)

2. Conventional

Cost

Retail

Beginning inventory

$ 90,000

$180,000

Plus: Purchases

355,000

580,000

Freight-in

9,000

Less: Purchase returns

Less: Abnormal spoilage

Less: Net markdowns

_______

Goods available for sale

442,200

745,000

Less:

Normal spoilage

Net sales ($540,000 – 10,000)

Employee discounts

Estimated ending inventory at retail

$208,000

Estimated ending inventory at cost (58.41% x $208,000)

9–54 Intermediate Accounting, 8/e

Problem 9–5

Requirement 1

Employee discounts must be deducted in the retail column.

$250,000

= $312,500 – 250,000 = $62,500 = Employee discounts

.80

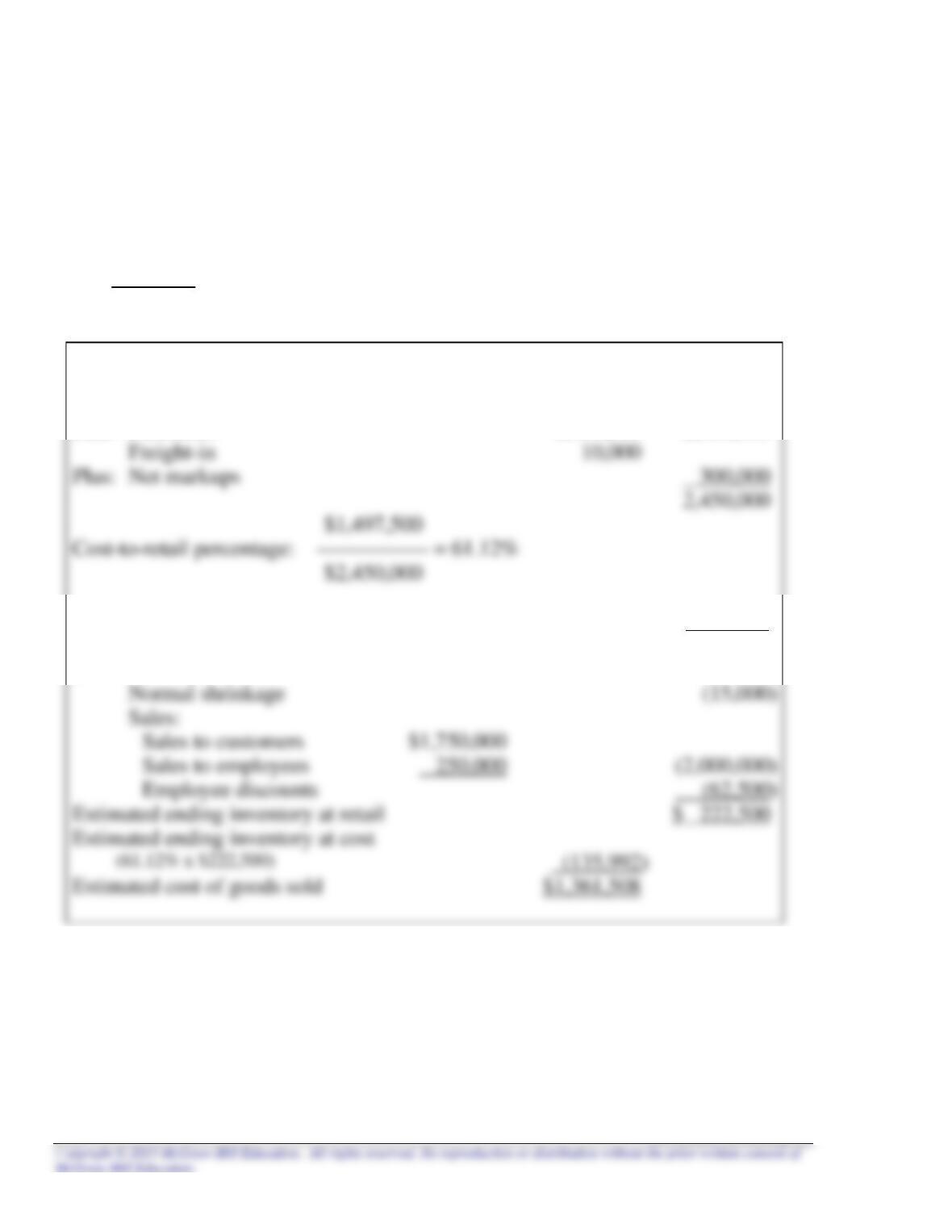

Cost

Retail

Beginning inventory

$ 100,000

$ 150,000

Plus: Purchases

1,387,500

2,000,000

Freight-in

Plus: Net markups

2,450,000

Less: Net markdowns

________

(150,000)

Goods available for sale

1,497,500

2,300,000

Less:

Normal shrinkage

Sales:

Sales to customers $1,750,000

Employee discounts

Estimated ending inventory at retail

$ 222,500

Estimated cost of goods sold

$1,361,508

Problem 9–5 (concluded)

Requirement 2

Cost

Retail

Beginning inventory

$ 100,000

$ 150,000

Plus: Purchases

1,387,500

2,000,000

Freight-in

Plus: Net markups

Less: Net markdowns

________

Goods available for sale (including beginning inventory)

1,497,500

2,300,000

Less:

Normal shrinkage

Sales:

Sales to customers $1,750,000

Employee discounts

Estimated ending inventory at retail

$ 222,500

Estimated ending inventory at cost:

Beginning inventory $150,000 $100,000

Estimated cost of goods sold

$1,350,375

$1,397,500

Cost-to-retail percentage: = 65%

9–56 Intermediate Accounting, 8/e

Problem 9–6

Requirement 1

Cost

Retail

Beginning inventory

$ 20,000

$ 30,000

Plus: Purchases

100,151

146,495

Freight-in

Less: Purchase returns

Plus: Net markups ($2,500 – 265)

175,930

Less: Net markdowns

_______

(800)

Goods available for sale

$123,151

175,130

Less:

Normal spoilage

Net sales

Estimated ending inventory at retail

$ 34,900

Requirement 2

The difference between the inventory estimate per retail method and the amount

per physical count may be due to:

Problem 9–7

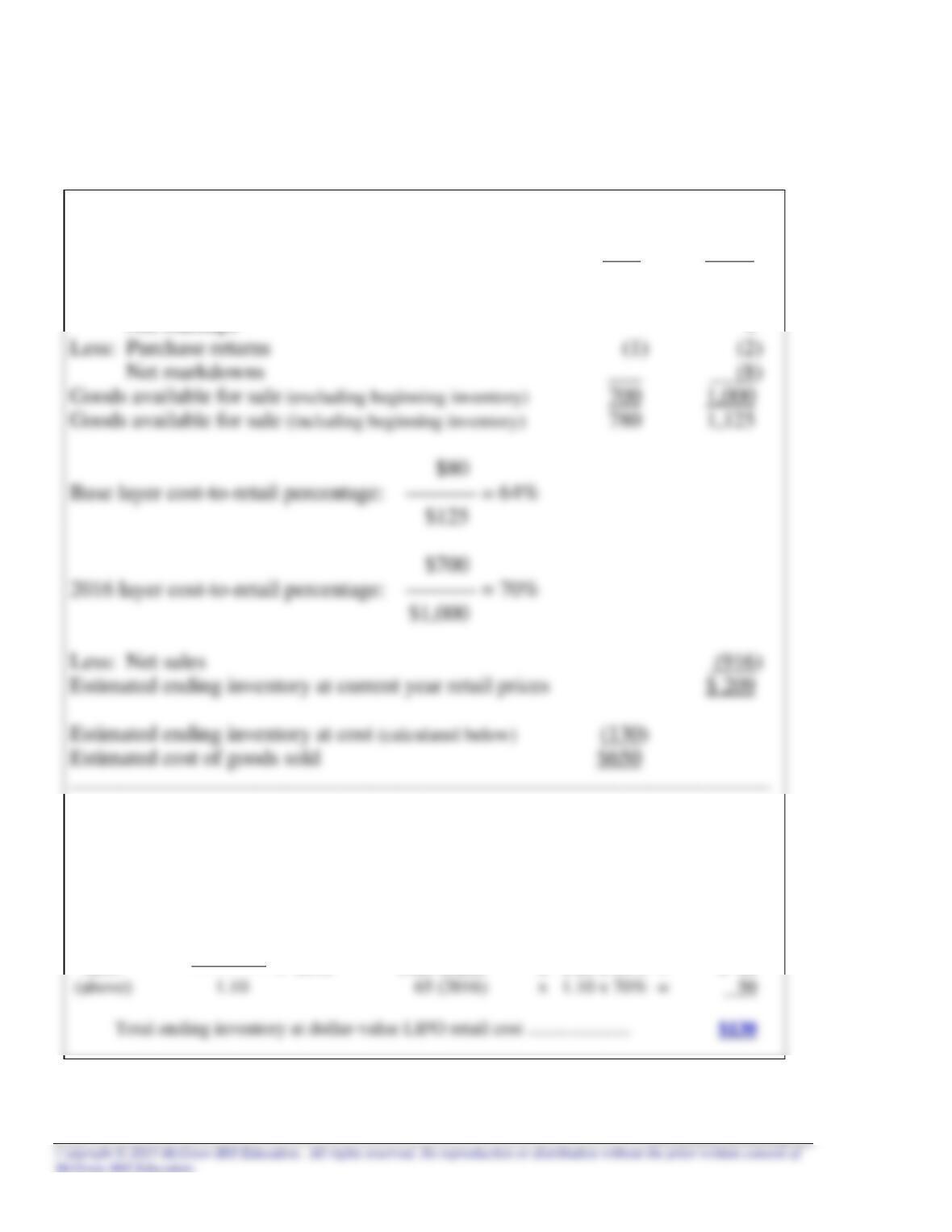

($ in 000s) Cost Retail

Beginning inventory $ 80 $ 125

Cost-to-retail percentages:

Average cost ratio: $780 ÷ $1,125 = .6933

9–58 Intermediate Accounting, 8/e

Problem 9–8

($ in 000s)

Cost

Retail

Beginning inventory

$ 80

$ 125

Plus: Net purchases

671

1,006

Freight-in

30

Net markups

4

Less: Purchase returns

Net markdowns

___

Goods available for sale (excluding beginning inventory)

700

1,000

Goods available for sale (including beginning inventory)

780

1,125

Less: Net sales

Estimated ending inventory at current year retail prices

Estimated ending inventory at cost (calculated below)

Estimated cost of goods sold

Step 1 Step 2 Step 3

Ending Ending Inventory Inventory

Inventory Inventory Layers Layers

at Year-End at Base Year at Base Year Converted to

Retail Prices Retail Prices Retail Prices Cost

$209

$209 = $190 $125 (base) x 1.00 x 64% = $ 80

Problem 9–9

Employee discounts must be deducted in the retail column.

2016:

$2,400

= $3,000 – 2,400 = $600 = Employee discounts

.80

Cost

Retail

Beginning inventory

$ 28,000

$ 40,000

Plus: Net purchases

85,000

108,000

Freight-in

2,000

Net markups

10,000

Less: Net markdowns

Goods available for sale (excluding beginning inventory)

116,000

Goods available for sale (including beginning inventory)

115,000

156,000

Estimated ending inventory at current year retail prices

Estimated ending inventory at cost (below)

(35,950)

Estimated cost of goods sold

$ 79,050

___________________________________________________________________________

Step 1 Step 2 Step 3

Ending Ending Inventory Inventory

Inventory Inventory Layers Layers

at Year-End at Base Year at Base Year Converted to

Retail Prices Retail Prices Retail Prices Cost

$53,000

9–60 Intermediate Accounting, 8/e

Problem 9–9 (concluded)

2017:

Cost

Retail

Beginning inventory

$ 35,950

$ 53,000

Plus: Net purchases

90,000

114,000

Freight-in

2,500

Net markups

8,000

Less: Net markdowns

Goods available for sale (excluding beginning inventory)

Goods available for sale (including beginning inventory)

Estimated ending inventory at current year retail prices

Estimated ending inventory at cost (below)

Estimated cost of goods sold

$ 85,706

___________________________________________________________________________

Step 1 Step 2 Step 3

Ending Ending Inventory Inventory

Inventory Inventory Layers Layers

at Year-End at Base Year at Base Year Converted to

Retail Prices Retail Prices Retail Prices Cost

$63,800

$63,800 = $58,000 $40,000 (base) x 1.00 x 70% = $28,000