Alternate Exercises and Problems 8–1

Chapter 8 Inventories: Measurement

EXERCISES

Exercise 8-1

PERPETUAL SYSTEM PERIODIC SYSTEM

($ in 000s)

Purchases

Inventory 265 Purchases 265

Accounts payable 265 Accounts payable 265

Freight

Sales

Accounts receivable 350 Accounts receivable 350

End of period

No entry Cost of goods sold (below) 264

Inventory (ending) 123

8–2 Intermediate Accounting, 8/e

Exercise 8-2

Inventory balance before additional transactions $317,000

Alternate Exercises and Problems 8–3

Exercise 8-3

Requirement 1

Purchase price = 50 units x $800 = $40,000 x .75 = $30,000

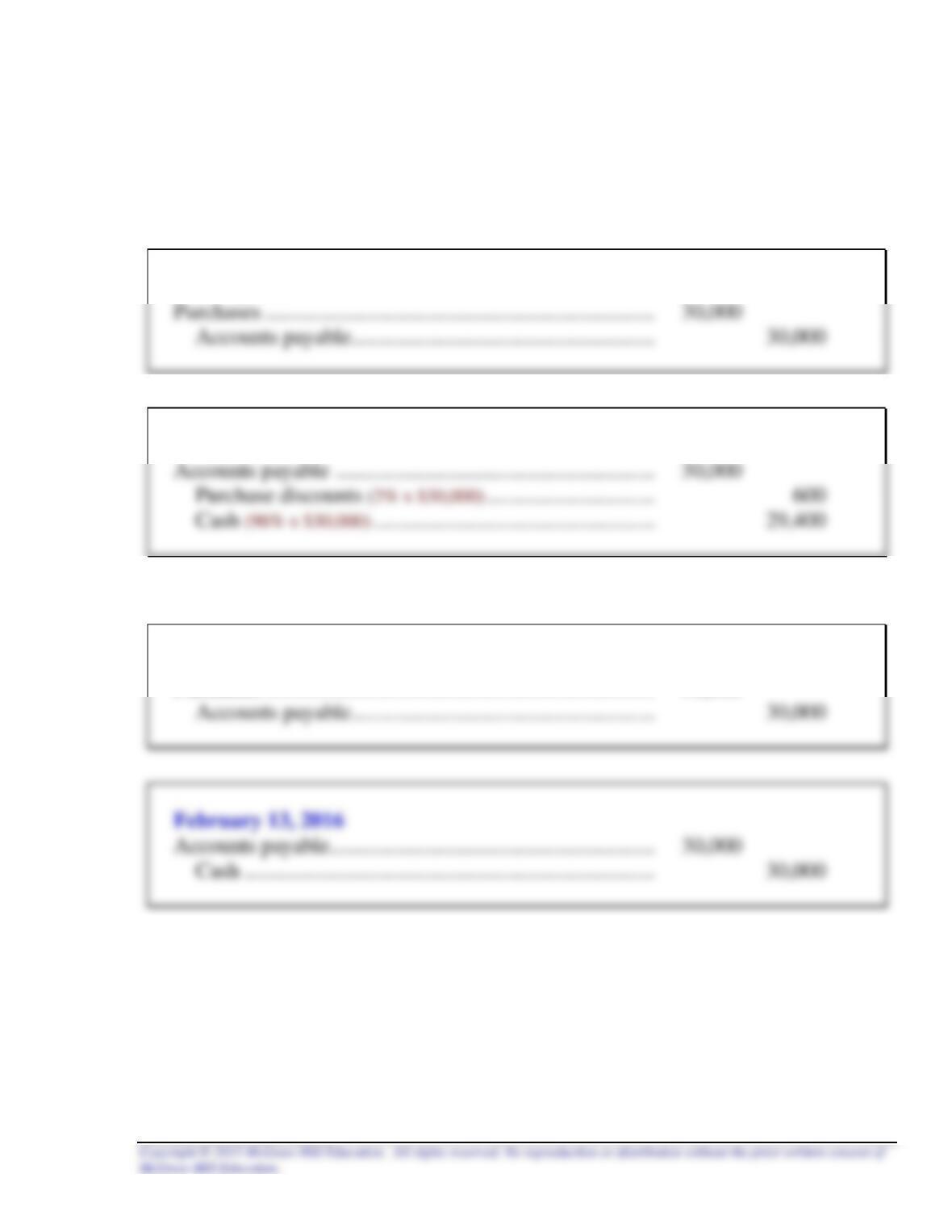

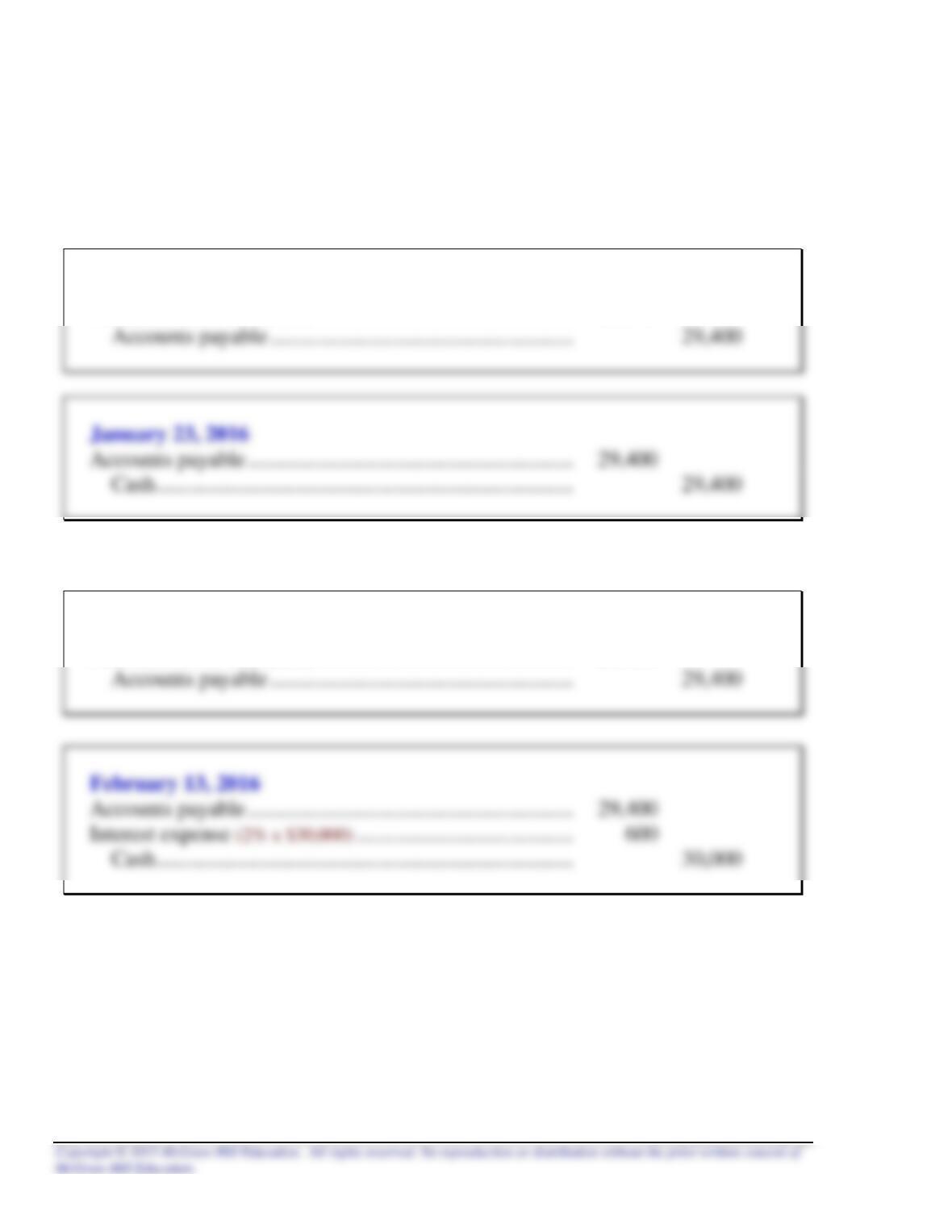

January 14, 2016

January 23, 2016

Requirement 2

January 14, 2016

Purchases ……………………………………………………………… 30,000

8–4 Intermediate Accounting, 8/e

Exercise 8-3 (concluded)

Requirement 3

Requirement 1:

January 14, 2016

Purchases (98% x $30,000)…………………………………………. 29,400

Requirement 2:

January 14, 2016

Purchases (98% x $30,000)…………………………………………. 29,400

Alternate Exercises and Problems 8–5

Exercise 8-4

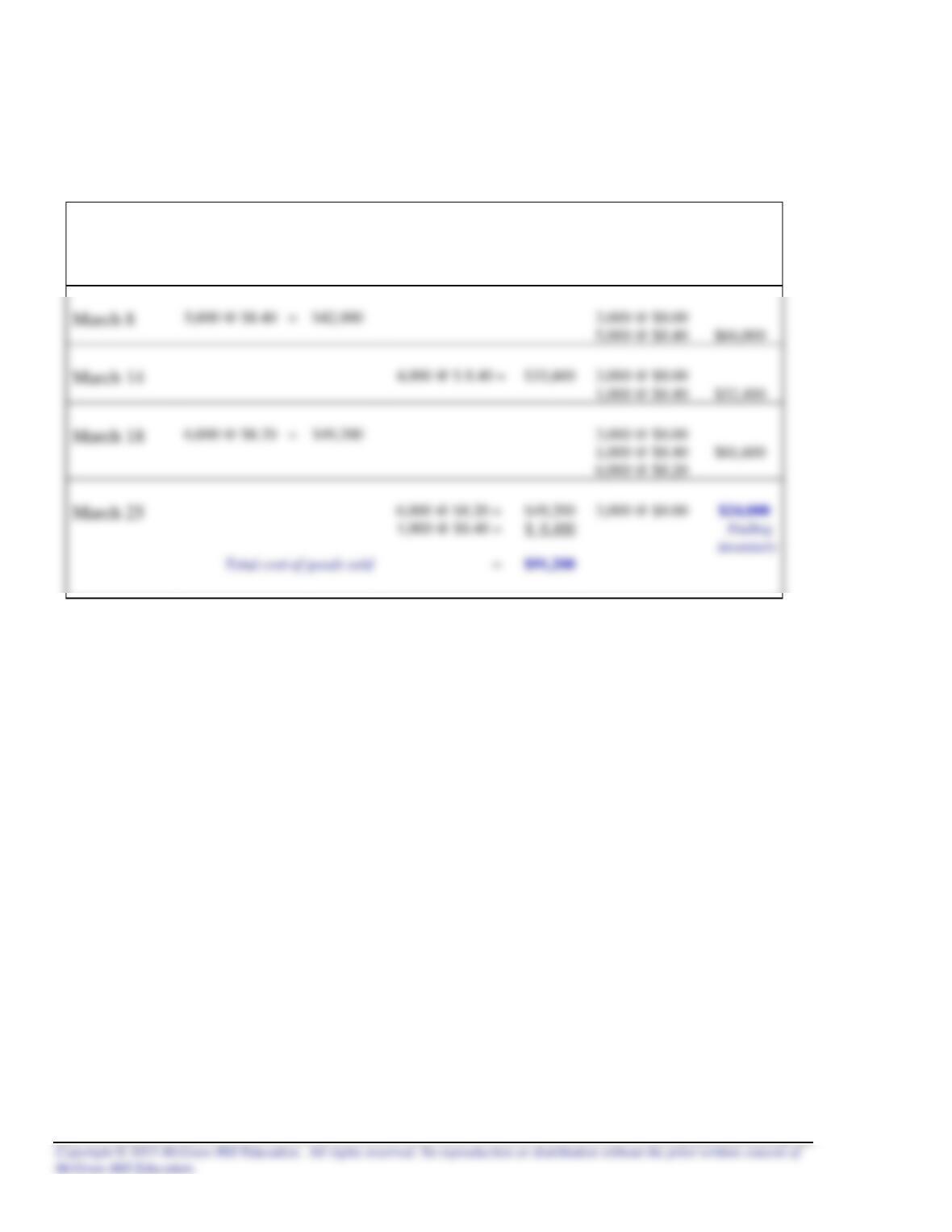

First-in, first-out (FIFO)

Cost of goods sold:

Date of Cost of

sale Units sold Units Sold Total Cost

March 14 3,000 (from BI) $8.00 $24,000

1,000 (from 3/8 purchase) 8.40 8,400

8–6 Intermediate Accounting, 8/e

Exercise 8-4 (continued)

Last-in, first-out (LIFO)

Date

Purchased

Sold

Balance

Beginning

inventory

3,000 @ $8.00 = $24,000

3,000 @ $8.00 $24,000

Alternate Exercises and Problems 8–7

Exercise 8-4 (concluded)

Average cost

Date

Purchased

Sold

Balance

Beginning

inventory

3,000 @ $8.00 = $24,000

3,000 @ $8.00 $24,000

March 14

4,000 @ $8.25 $33,000

10,000 units

8–8 Intermediate Accounting, 8/e

Exercise 8-5

Requirement 1

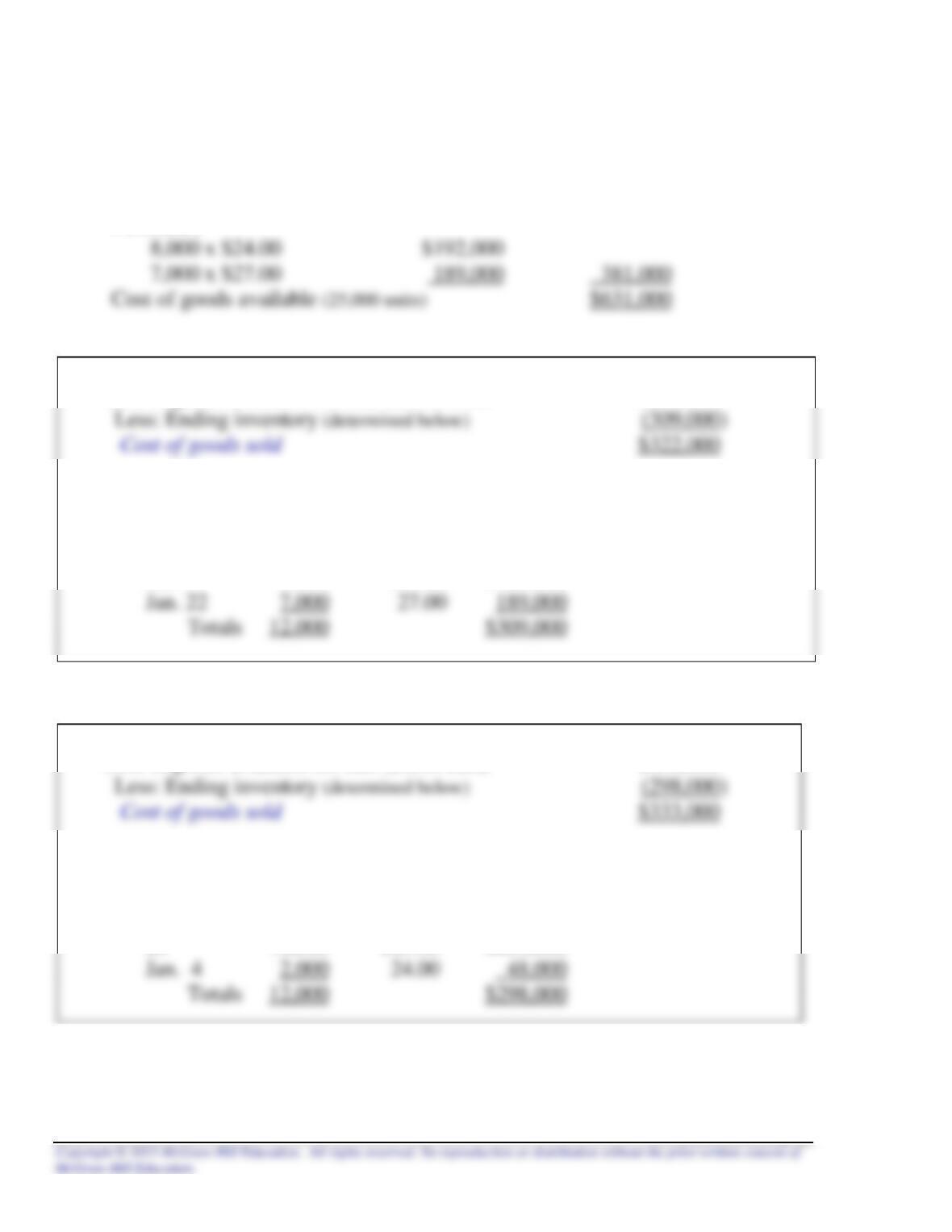

Cost of goods available for sale:

Beginning inventory (7,000 x $22.00) $154,000

Purchases:

Cost of ending inventory:

Alternate Exercises and Problems 8–9

Exercise 8-5 (concluded)

Requirement 2

Date

Purchased

Sold

Balance

Beginning

inventory

7,000 @ $22.00 = $154,000

7,000 @ $22.00 $154,000

April 11

5,000 @ $22.30 = $111,500

8,000 @ $22.20 $178,400

8–10 Intermediate Accounting, 8/e

Exercise 8-6

Ending

Ending Inventory Inventory Layers Inventory Layers Inventory

Date at Base Year Cost at Base Year Cost Converted to Cost DVL Cost

1/1/16 $832,000

Alternate Exercises and Problems 8–11

PROBLEMS

Problem 8-1

Requirement 1

Beginning inventory (8,000 x $10.00) $ 80,000

Net purchases:

Cost of ending inventory:

Date of

purchase Units Unit cost Total cost

8–12 Intermediate Accounting, 8/e

Problem 8-2

Cost of goods available for sale for periodic system:

Beginning inventory (10,000 x $25.00) $250,000

Purchases:

1. FIFO, periodic system

Cost of goods available for sale (25,000 units) $631,000

Cost of ending inventory:

Date of

purchase Units Unit cost Total cost

Jan. 4 5,000 $24.00 $120,000

2. LIFO, periodic system

Cost of goods available for sale (25,000 units) $631,000

Cost of ending inventory:

Date of

purchase Units Unit cost Total cost

BI 10,000 $25.00 $250,000

Alternate Exercises and Problems 8–13

Problem 8-2 (concluded)

3. Average cost, periodic system

Cost of goods available for sale (25,000 units) $631,000

Cost of ending inventory:

$631,000

Weighted-average unit cost = = $25.24