Question 8–1

Question 8–2

Question 8–3

Perpetual System Periodic System

(1) Purchase of merchandise debit inventory debit purchases

Chapter 8 Inventories: Measurement

QUESTIONS FOR REVIEW OF KEY TOPICS

Inventory for a manufacturing company consists of (1) raw materials, (2) work in

process, and (3) finished goods. Raw materials represent the cost, primarily purchase

Beginning inventory plus net purchases for the period equals cost of goods

8–2 Intermediate Accounting, 8/e

Answers to Questions (continued)

Question 8–4

Question 8–5

Question 8–6

Question 8–7

Inventory shipped f.o.b. shipping point is included in the inventory of the

purchaser when the merchandise reaches the common carrier. Laetner Corporation

A consignment is an arrangement under which goods are physically transferred to

By the gross method, purchase discounts not taken are viewed as part of

1. Beginning inventory — increase

Answers to Questions (continued)

Question 8–8

Question 8–9

Question 8–10

Four methods of assigning cost to ending inventory and cost of goods sold are (1)

specific identification, (2) first-in, first-out (FIFO), (3) last-in, first-out (LIFO), and

(4) average cost. The specific identification method requires each unit sold during the

When costs are declining, LIFO will result in a lower cost of goods sold and

Proponents of LIFO argue that it provides a better match of revenues and

expenses because cost of goods sold includes the costs of the most recent purchases.

8–4 Intermediate Accounting, 8/e

Question 8–11

Question 8–12

Question 8–13

Question 8–14

Many companies choose the LIFO inventory method to reduce income taxes in

periods when prices are rising. In periods of rising prices, LIFO results in a higher

The gross profit, inventory turnover, and average days in inventory ratios are

A LIFO inventory pool groups inventory units into pools based on physical

The dollar-value LIFO method has important advantages. First, it simplifies the

Answers to Questions (concluded)

Question 8–15

After determining ending inventory at year-end cost, the following steps remain:

1. Convert ending inventory valued at year-end cost to base year cost.

3. Convert each layer’s base year cost measurement to layer year cost

measurement using the layer year’s cost index and then sum the layers.

Question 8–16

The primary difference between U.S. GAAP and IFRS in the methods

8–6 Intermediate Accounting, 8/e

Brief Exercise 8–1

Brief Exercise 8–2

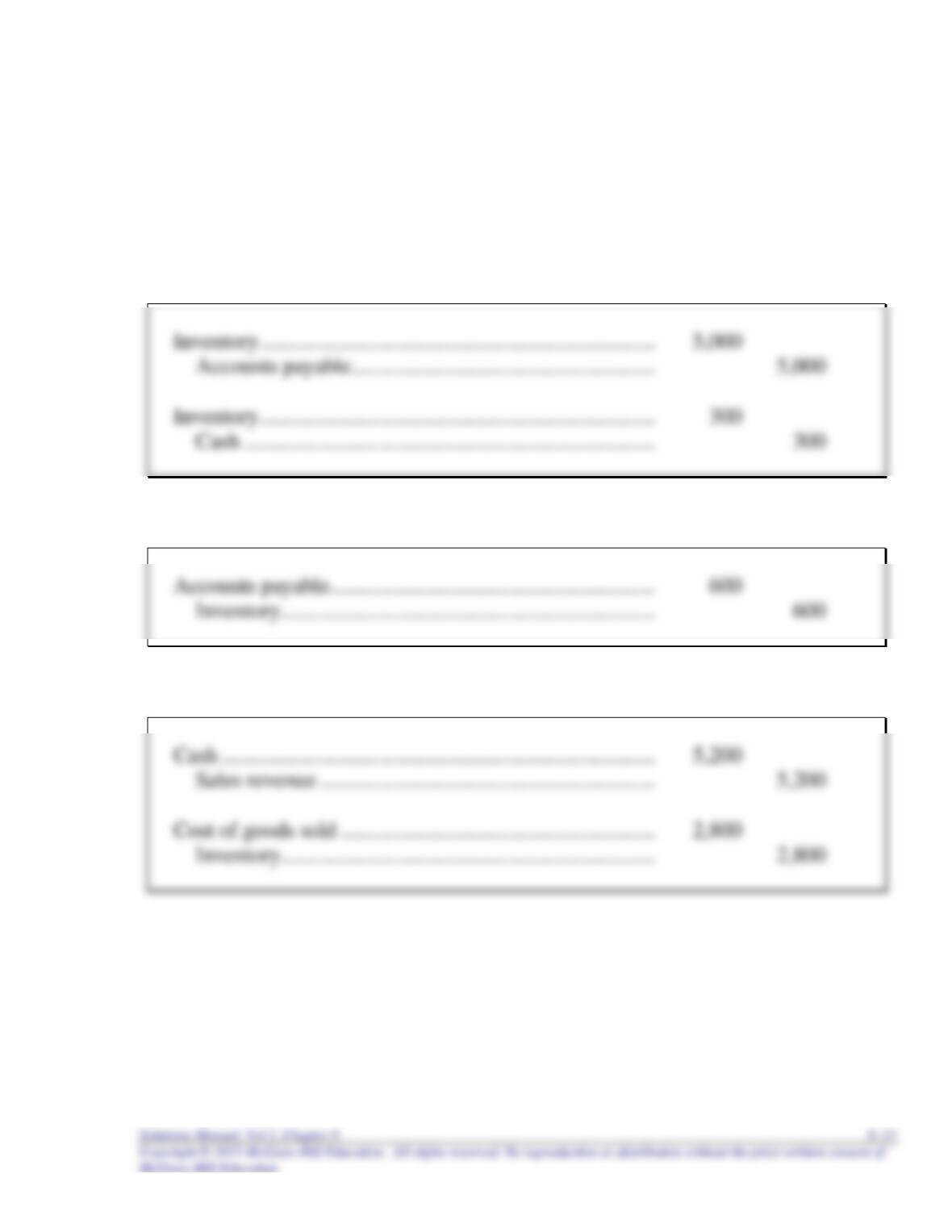

To record the purchase of inventory on account.

To record sales on account and cost of goods sold.

BRIEF EXERCISES

Brief Exercise 8–3

Both shipments should be included in inventory. The goods shipped to a

Brief Exercise 8–4

8–8 Intermediate Accounting, 8/e

Brief Exercise 8–5

December 28, 2016

Brief Exercise 8–6

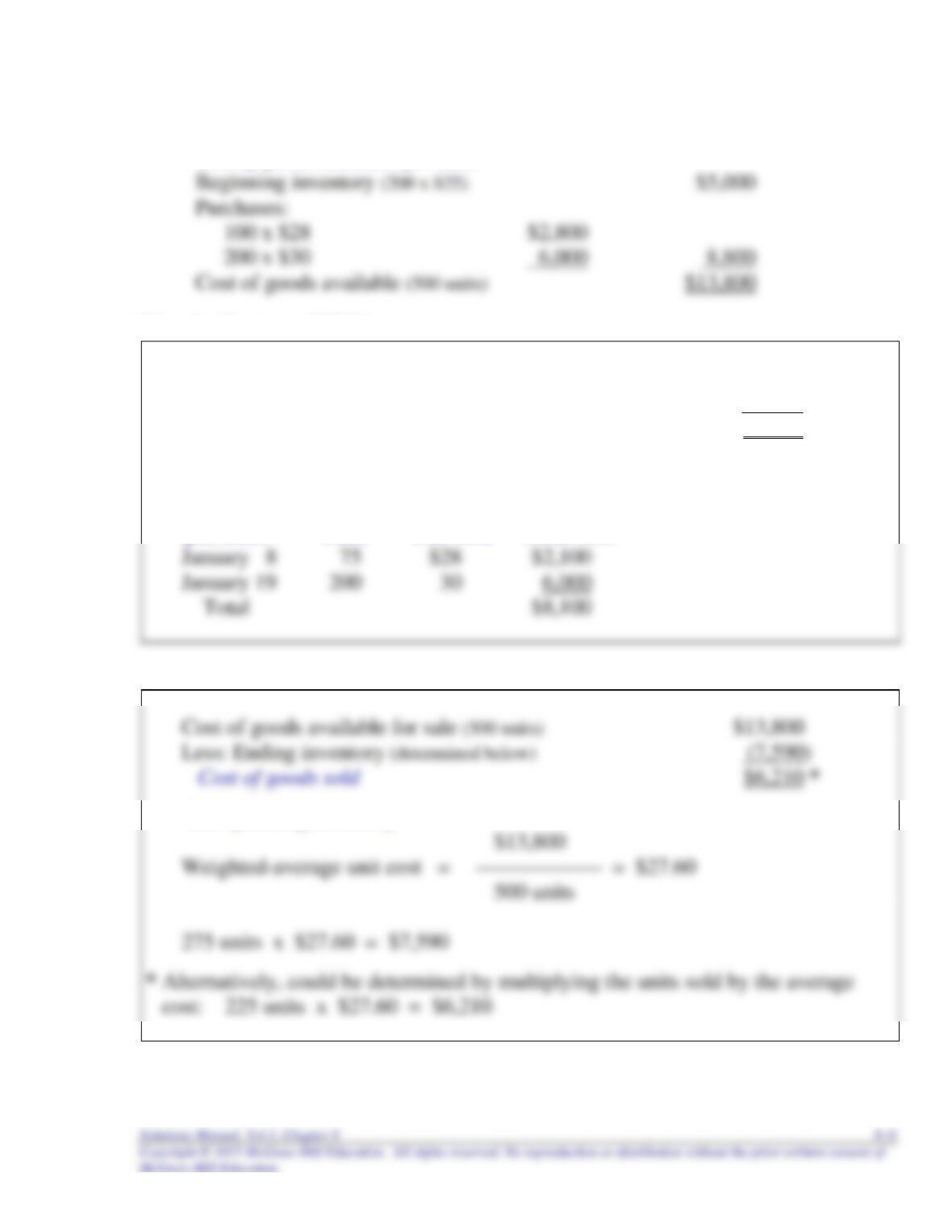

Cost of goods available for sale:

First-in, first-out (FIFO)

Cost of goods available for sale (500 units) $13,800

Less: Ending inventory (determined below) (8,100)

Cost of goods sold $5,700

Cost of ending inventory:

Date of

purchase Units Unit cost Total cost

Average cost

Cost of ending inventory:

Brief Exercise 8–7

8–10 Intermediate Accounting, 8/e

First-in, first-out (FIFO)

Cost of goods sold:

Date of Cost of

Sale Units Sold Units Sold Total Cost

Ending inventory:

Date of

Purchase Units Unit Cost Total Cost

Brief Exercise 8–7 (concluded)

Average cost

Date

Purchased

Sold

Balance

Beginning

inventory

200 @ $25 = $5,000

200 @ $25 $5,000

January 10

125 @ $26 = $3,250

175 @ $26 $4,550

8–12 Intermediate Accounting, 8/e

Brief Exercise 8–8

Cost of goods available for sale:

Brief Exercise 8–9

64,000 units were sold.

Cost of goods sold without year-end purchase:

If FIFO were used instead of LIFO, the year-end purchase would have no effect

on income before income taxes. FIFO cost of goods sold with or without the purchase

would consist of the 10,000 units from beginning inventory and 54,000 units

purchased during the year at $18:

Brief Exercise 8–10

Brief Exercise 8–11

Cost of goods sold for the six months ended February 28, 2014, would have been

$100 million lower had Walgreen used FIFO for its LIFO inventory. While

beginning inventory would have been $2,100 million higher, ending inventory also

8–14 Intermediate Accounting, 8/e

Brief Exercise 8–12

Average inventory = ($60,000 + 48,000) 2 = $54,000

Brief Exercise 8–13

Ending Inventory Inventory Layers Inventory Layers Inventory

Date at Base Year Cost at Base Year Cost Converted to Cost DVL Cost

Exercise 8–1

1. To record the purchase of inventory on account and the payment of freight

charges.

2. To record purchase returns.

3. To record cash sales and cost of goods sold.

EXERCISES

Exercise 8–2

1. To record the purchase of inventory on account and the payment of freight

charges.

2. To record purchase returns.

3. To record cash sales.

Exercise 8–3

Requirement 1

Beginning inventory $ 32,000

Requirement 2

Cost of goods sold (above) ………………………………………. 233,000

8–18 Intermediate Accounting, 8/e

Exercise 8–4

PERPETUAL SYSTEM PERIODIC SYSTEM

($ in 000s)

Purchases

Inventory 155 Purchases 155

Accounts payable 155 Accounts payable 155

Freight

Sales

Accounts receivable 250 Accounts receivable 250

Sales revenue 250 Sales revenue 250

Cost of goods sold 148 No entry

Inventory 148

End of period

Exercise 8–5

2016 2017 2018

Beginning inventory 275 (1) 249 (3) 225

Cost of goods sold 627 621 584 (6)

2016:

(1) Cost of goods available for sale – Net purchases = Beginning inventory

2017:

(3) 2017 beginning inventory = 2016 ending inventory = 249

2018:

(6) Cost of goods available for sale – Ending inventory = Cost of goods sold

8–20 Intermediate Accounting, 8/e

Exercise 8–5 (concluded)

(7) Cost of goods available for sale – Beginning inventory = Net purchases