Exercise 14–34

Analysis: Book value: $12 million + 1.2 million = $13,200,000

1. January 1, 2016

Interest payable (10% x $12,000,000) ……………………. 1,200,000

2. December 31, 2017

Notes payable …………………………………………………. 1,000,000

3. December 31, 2018

Notes payable …………………………………………………. 1,000,000

14–62 Intermediate Accounting, 8/e

Exercise 14–35

Analysis: Book value: $240,000 + (10% x $240,000) = $264,000

1. January 1, 2016

No entry needed.

2. December 31, 2016

3. December 31, 2017

Interest expense (2% x [$264,000 + 5,280]) ……………… 5,385*

Exercise 14–36

Requirement 2

The specific citation that specifies the accounting treatment of legal fees and other

Requirement 3

14–64 Intermediate Accounting, 8/e

CPA / CMA REVIEW QUESTIONS

CPA Exam Questions

1. c. At issuance, a bond is valued at the present value of the principal and interest

2. d. The interest expense is for the time the bonds were outstanding during the

3. d. Six months interest revenue at stated rate.

8% x ½ x $500,000 = $20,000

4. b. Present value of payments:

5. a. A bond issued at a discount reflects that the market rate is greater than the

contract rate.

CPA Exam Questions (continued)

6. a. The interest payable at September 30, 2016, will be for the three month’s

7. a. Must determine book value at time of extinguishment:

Bond premium at issue $ 40,000

Amortization of premium 1/1/2011 through 7/1/2016:

8. a. Using the book value method, no gain or loss is recognized. The journal

entry for the conversion would be:

Bonds payable 1,000,000

14–66 Intermediate Accounting, 8/e

CPA Exam Questions (concluded)

9. b. Book value of bonds at 6/30/2016 is $4,980,000 ($5,000,000 + 30,000 –

50,000).

10. b. The discount on the bonds is $800:

Market value of the bonds $196,000

11. c. Under US GAAP, the entire issue price is recorded as debt. Under IFRS,

convertible debt is divided into its liability and equity elements.

CMA Exam Questions

1. a. Because the bonds sold for more than their face value, they were sold at a

2. d. The annual interest cash outlay is $70,000 (7% nominal rate x $1,000,000),

or $35,000 each semiannual period. Interest expense is less than $35,000,

3. b. A bond liability is shown at its face value (maturity value), minus any

14–68 Intermediate Accounting, 8/e

PROBLEMS

Problem 14–1

Requirement 1

Interest $2,500,000¥ x 15.04630 * = $37,615,750

Requirement 2

Interest $ 2,500,000 x 18.40158 * = $46,003,950

Requirement 3

Investment in bonds (face amount) ……………………………. 50,000,000

Problem 14–2

1. Liabilities at September 30, 2016

Bonds payable (face amount) ………………………………. $160,000,000

2. Interest expense for year ended September 30, 2016

3. Statement of cash flows for year ended September 30, 2016

Baddour would report the cash inflow of $140,000,000*** from the sale of the

14–70 Intermediate Accounting, 8/e

Problem 14–2 (concluded)

Calculations:

January 1, 2016***

Cash (price: given) ……………………………………………… 140,000,000

June 30, 2016*

Interest expense (6% x $140,000,000) ………………………… 8,400,000

September 30, 2016**

Interest expense (6% x [$140,000,000 + 400,000] x 3/6) .. 4,212,000

Problem 14–3

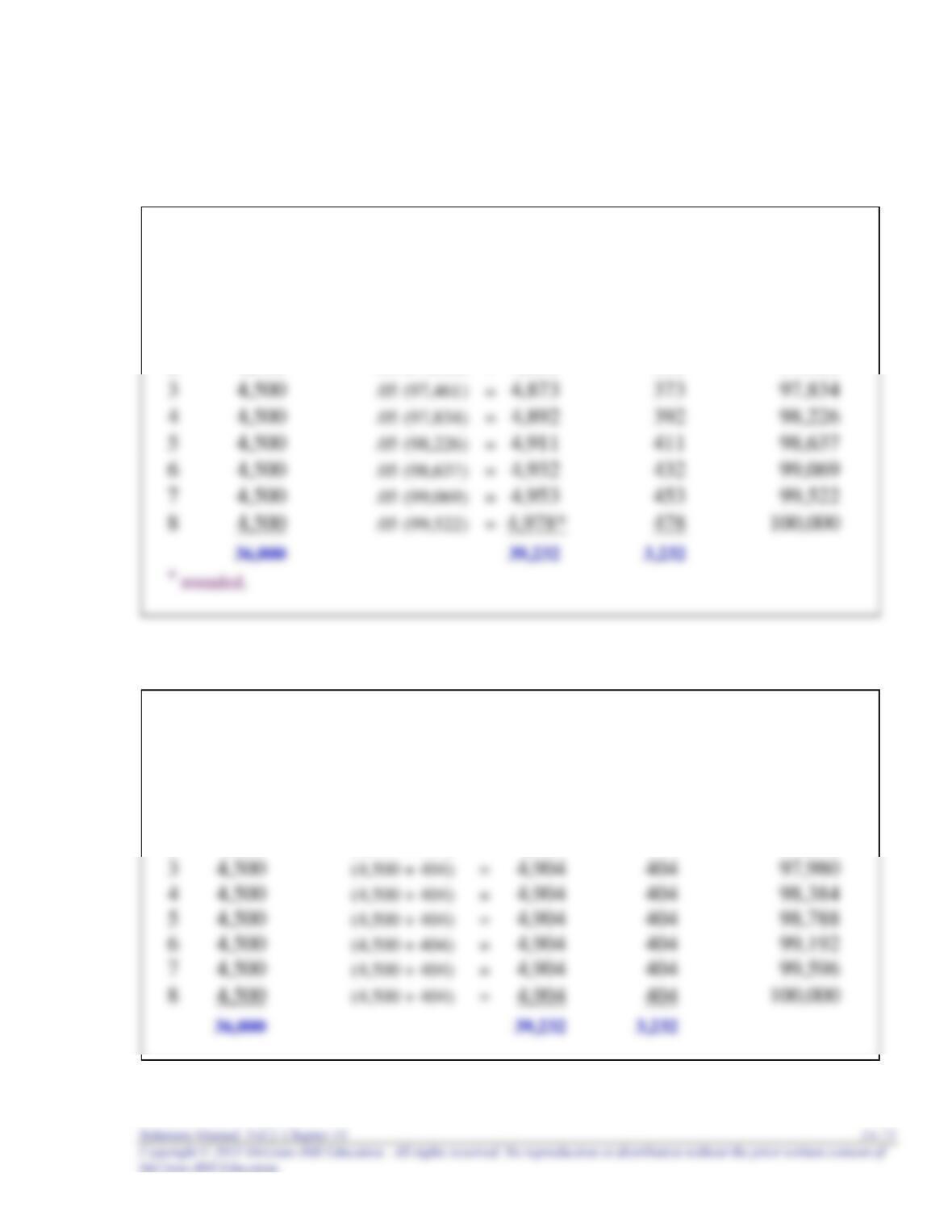

Requirement 1

Cash Effective Increase in Outstanding

Payment Interest Balance Balance

4.5% x Face Amount 5% x Outstanding Balance

96,768

1 4,500 .05 (96,768) = 4,838 338 97,106

2 4,500 .05 (97,106) = 4,855 355 97,461

Requirement 2

Cash Recorded Increase in Outstanding

Payment Interest Balance Balance

4.5% x Face Amount Cash plus Discount Reduction $3,232 ÷ 8

96,768

1 4,500 (4,500 + 404) = 4,904 404 97,172

2 4,500 (4,500 + 404) = 4,904 404 97,576

14–72 Intermediate Accounting, 8/e

Problem 14–3 (continued)

Requirement 3

(effective interest)

Interest expense (5% x $98,226) ………………………………… 4,911

Discount on bonds payable (difference) …………….. 411

Requirement 4

By the straight-line method, a company determines interest indirectly by

allocating a discount or a premium equally to each period over the term to maturity.

This is allowed if doing so produces results that are not materially different from the

interest method. The decision should be guided by whether the straight-line method

Problem 14–3 (concluded)

Requirement 5

The amortization schedule in requirement 1 gives us the present value, which

represents fair value since the market rate still is 10%. The outstanding debt balance

after the June 30, 2018, interest payment (line 5) is the present value at that time

14–74 Intermediate Accounting, 8/e

Problem 14–4

Requirement 1

$8,000,000 (outstanding balance at maturity)

Requirement 2

Problem 14–5

Requirement 1

Interest $3,600,000¥ x 6.46321 * = $23,267,556

Requirement 2

(a) Cromley

Cash Effective Increase in Outstanding

Payment Interest Balance Balance

4.5% x Face Amount 5% x Outstanding Balance Discount Reduction

77,414,756

1 3,600,000 .05 (77,414,756) = 3,870,738 270,738 77,685,494

14–76 Intermediate Accounting, 8/e

Problem 14–5 (continued)

(b) Barnwell

Cash Effective Increase in Outstanding

Payment Interest Balance Balance

4.5% x Face Amount 5% x Outstanding Balance Discount Reduction

77,415

1 3,600 .05 (77,415) = 3,871 271 77,686

2 3,600 .05 (77,686) = 3,884 284 77,970

Requirement 3

February 1, 2016 (Cromley)

Cash (price determined above) …………………………... 77,414,756

Problem 14–5 (continued)

Requirement 4

July 31, 2016 (Cromley)

Interest expense (from schedule) ………………………….. 3,870,738

Discount on bonds payable (from schedule) ….. 270,738

14–78 Intermediate Accounting, 8/e

Problem 14–5 (concluded)

July 31, 2017 (Cromley)

Interest expense (from schedule) ………………………….. 3,898,488

Discount on bonds payable (from schedule) …… 298,488

Problem 14–6

Requirement 1

April 1, 2016 (Western)

Cash ($29,300,000 + [1/12 x 12% x $30,000,000]) …….. 29,600,000

Discount on bonds payable ($30 million – 29.3 million) 700,000

Problem 14–6 (continued)

Requirement 2

The original maturity of the bonds was three years, or 36 months. But since

the bonds weren’t sold until one month after they were dated, they are

outstanding for only 35 months. Straight-line amortization, then, is $700,000 ÷