Student Name:

Class:

PV of retirement annuity at end of 2016

Pension benefit at end of 2016

Less: Interest cost

Projected benefit obligation

Requirement 6:

PBO at the end of 2017

PBO at the end of 2016

Change in PBO

PV of retirement annuity at end of 2017

Accumulated benefit obligation

Requirement 5:

Final year’s salary

1.2%

Correct!

80,000$

Correct!

Instructor

McGraw-Hill/Irwin

Exercise 17-12

Clark Industries

Requirement 1:

Percentage

Requirement 4:

Salary at end of 2016

Requirement 3:

Service years

Lump-sum equivalent

Final year’s salary

Annual retirement benefit payments

Present value of an ordinary annuity (n=15; i=7%)

Annual retirement benefit

Requirement 2:

Projected benefit obligation

Present value (n=25; i=7%)

PV of retirement annuity at end of 2041

1.2% X Service years X Final year’s salary

Clark Industries

Given Data E17-12:

Annual retirement benefit formula:

January 1, 1997

Stanley Mills’ hire date

Stanley Mills’ retirement date

December 31, 2041

Salary 20 years after hiring

Projected salary at retirement

Actuary‘s discount rate

Years of service

Expected retirement span – in years

Student Name:

Class:

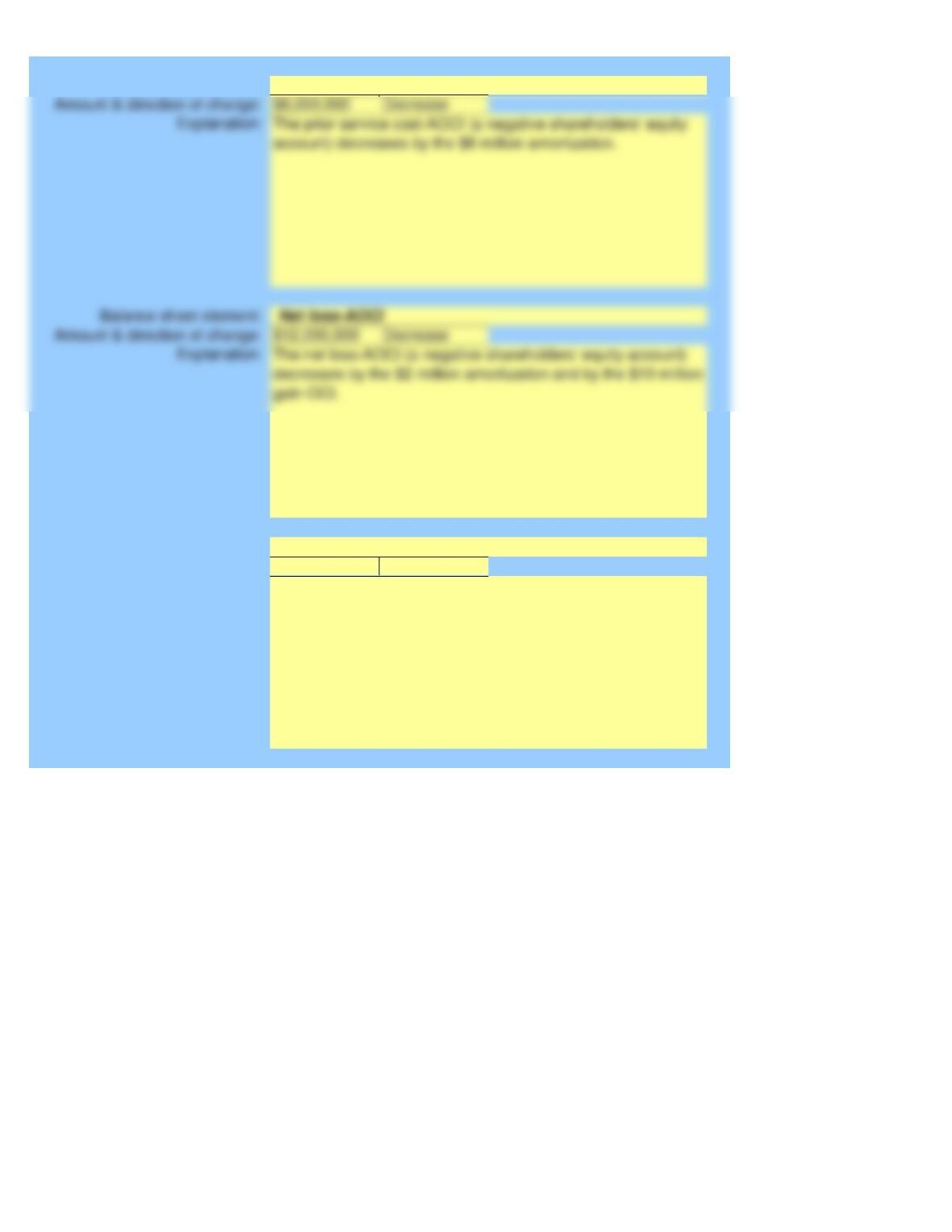

Balance sheet element:

Balance sheet element:

Shareholders’ Equity

Which elements of Warrick’s balance sheet are affected by the components of pension

expense? What are the specific changes in these accounts? NOTE: because of the free-form

nature of this exercise there is no reliable way to label your answers with “Correct” or “Try

Again”.

Instructor

McGraw-Hill/Irwin

Exercise 17-14

Balance sheet element:

Liabilities

Warrick Boards

pension liability (underfunded plan) will increase by $274

Amount & direction of change:

Explanation:

Balance sheet element:

Balance sheet element:

Prior service cost-AOCI

Amount & direction of change:

Balance sheet element:

Net loss-AOCI

Amount & direction of change:

Explanation:

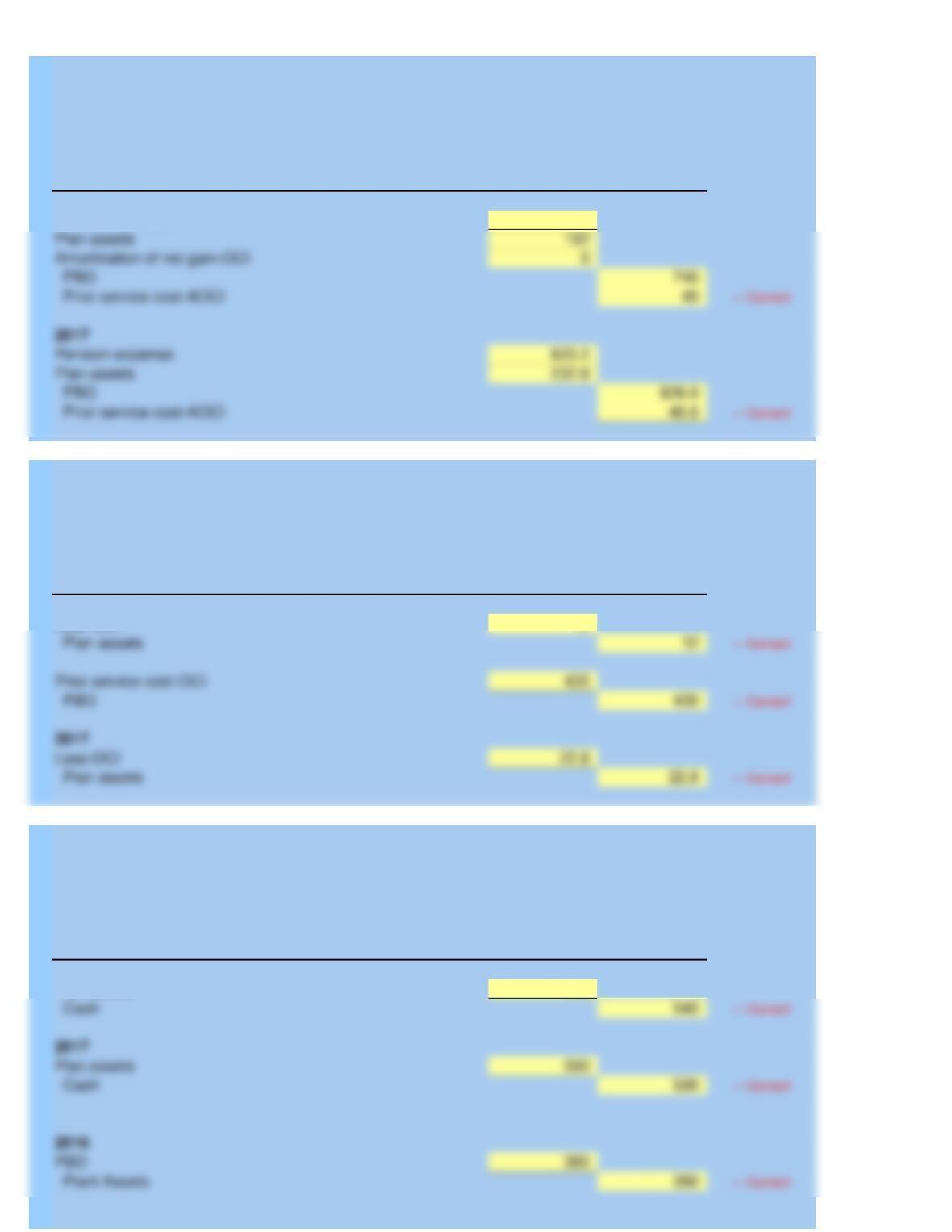

224$

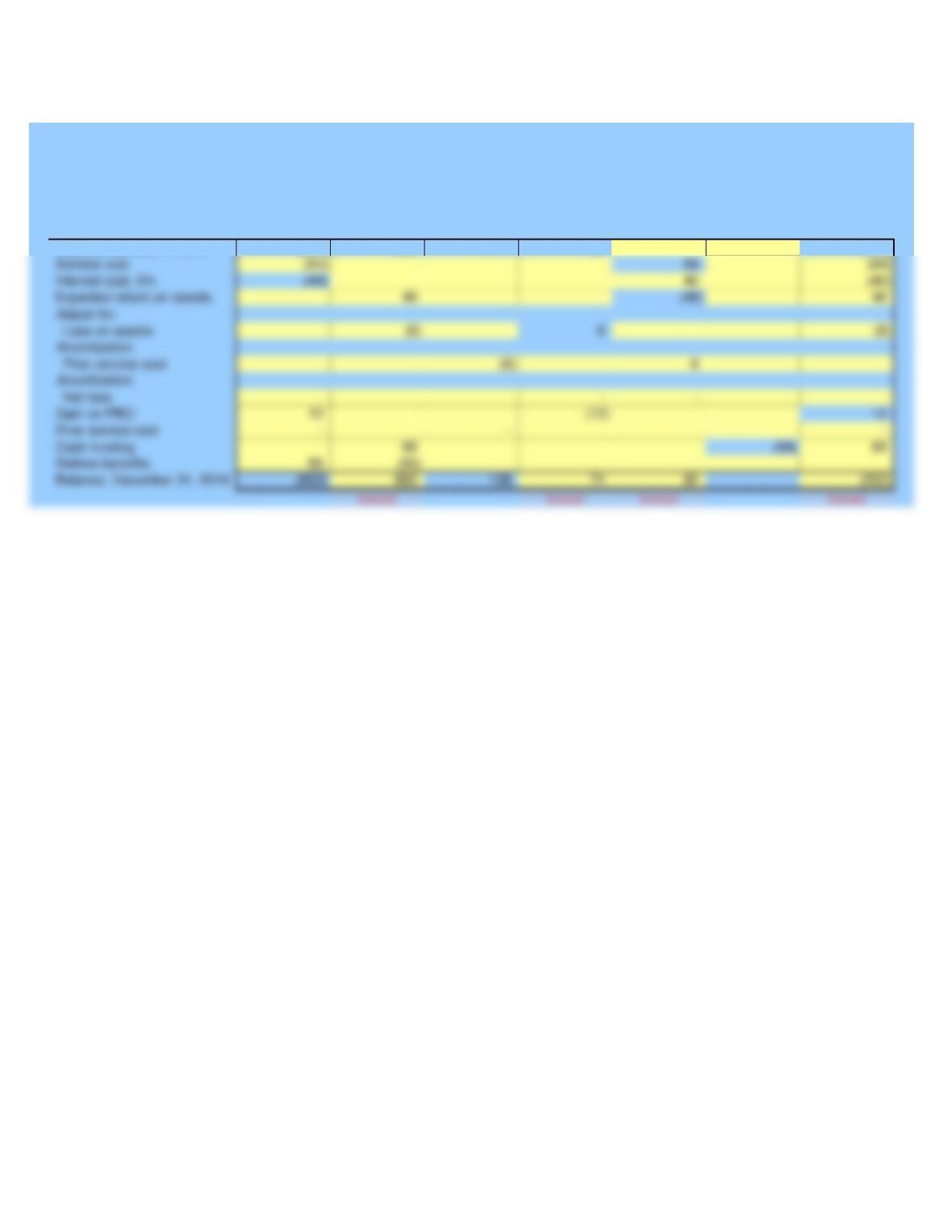

Given Data E17-14:

Service cost

Pension expense calculation (in millions):

Warrick Boards

Amortization of net loss

Amortization of prior service cost

Expected return on the plan assets ($100 actual, less $10 gain)

Interest cost

Student Name:

Class:

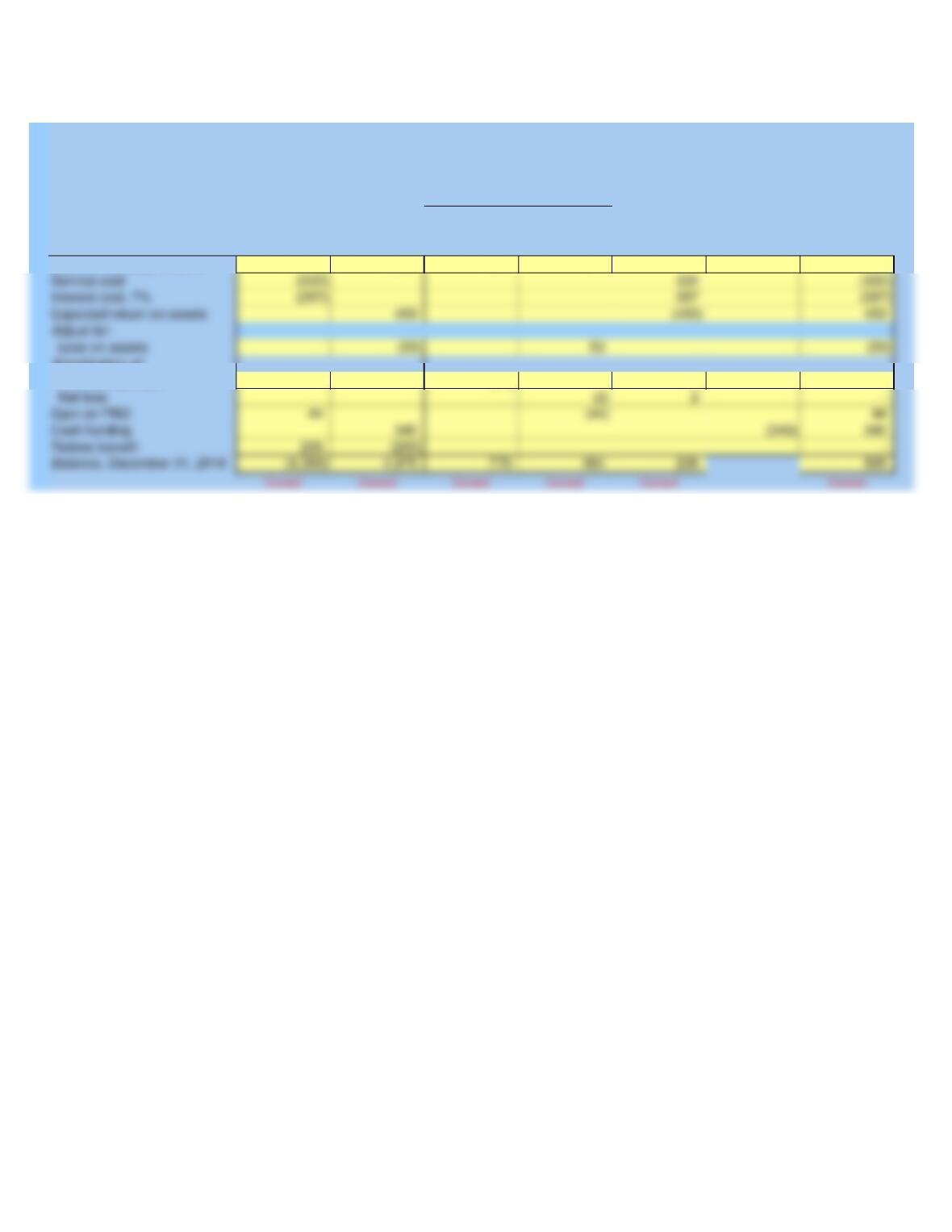

( )s indicate

Prior Net Pension

credits; debits

Plan Service Net Pension (Liability)/

otherwise

PBO Assets Cost Loss Expense Cash Asset

(800) 600 114 80 (200)

Universal Products

Pension Worksheet

Balance, January 1, 2016

Exercise 17-15

McGraw-Hill/Irwin

Instructor

($ in 000s)

Prior service cost

Prior Net Pension

Plan Service Net Pension (Liability)/

PBO Assets Cost Loss Expense Cash Asset

(800) 600 114 80 (200)

84

Partially Completed Pension Worksheet

Given Data E17-15:

Universal Products

Service cost

Balance, January 1, 2016

Average remaining service life of active employee group

Actuary’s discount rate

Prior service cost at end of 2014

Expected rate of return on assets

Interest cost, 5%

Prior service cost

Retiree benefits

Cash funding

Prior service cost

Gain on PBO

Net loss

Loss on assets

Expected return on assets

Student Name:

Class:

–$

150

Contributions 2016

Benefits paid

Actual return on plan assets

Balance, December 31, 2016

Contributions 2017

Benefits paid

–$

–

Interest cost

Expected return on the plan assets

Pension Expense – 2017

Expected return on the plan assets

Service cost

150$

–

Plan assets

PBO

150$

PBO

Balance, January 1, 2016

Actual return on plan assets

2. Plan Assets

3. Pension Expense – 2016

4. Net Pension Asset/Liability

Service cost

Interest cost

Balance, January 1, 2016

Service cost

1. Projected Benefit Obligation

Problem 17-6

McGraw-Hill/Irwin

Instructor

($ in 000s)

Calculations

STANLEY-MORGAN INDUSTRIES

Balance, December 31, 2016

Service cost

Interest cost

Benefits paid

Interest cost

Benefits paid

10% rate of return

Given Data P17-06:

STANLEY-MORGAN INDUSTRIES

Expected plan asset earnings

Year-end funding, 2017

Year-end funding, 2016

Service cost, 2017

Service cost, 2016

Recommended discount rate

Student Name:

Class:

2016 2017

520.0$ 570.0$

Payments

Balance, 12-31-2016

Interest 10%

Service cost

Payments

Prior service cost

Balance, 1-2-2016

Interest 10%

Service cost

1,800$

Payments

Payments

Balance, 12-31-2016

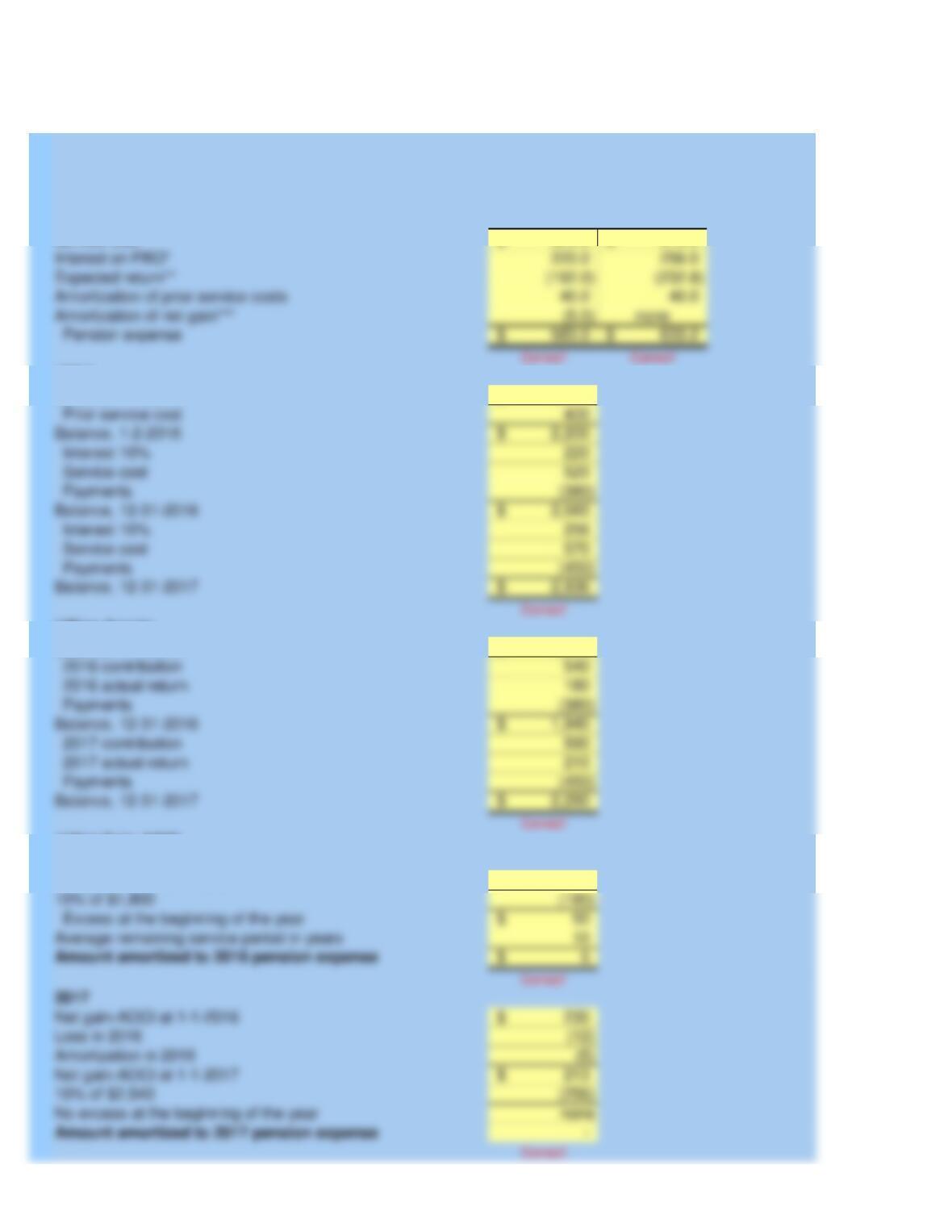

1,600$

Excess at the beginning of the year

Average remaining service period in years

Net gain-AOCI at 1-1-2016

Loss in 2016

Amortization in 2016

Net gain-AOCI at 1-1-2017

10% of $1,800

2017

10% of $2,540

No excess at the beginning of the year

Amount amortized to 2017 pension expense

230$

Service cost

Net gain-AOCI at 1-1-2016

Balance, 1-1-2016

Requirement 1:

*PBO

**Plan Assets

***Net Gain-AOCI

2016

Balance, 1-1-2016

McGraw-Hill/Irwin

Instructor

($ in millions)

Pension Expenses

KOLLAR COMPANY

Problem 17-12

Interest on PBO*

Expected return**

Amortization of prior service costs

Amortization of net gain***

Requirement 2:

Debit Credit

583

Debit Credit

Loss-OCI

Plan assets

Prior service cost-OCI

PBO

2017

12

Debit Credit

Cash

Plant Assets

2017

2016

Cash

Plan assets

540

2017

($ in millions)

General Journal

KOLLAR COMPANY

Requirement 4:

Account

Requirement 3:

Loss-OCI

2016

2016

Plan assets

Account

Account

2016

Pension expense

($ in millions)

General Journal

KOLLAR COMPANY

($ in millions)

General Journal

KOLLAR COMPANY

Prior service cost-AOCI

Pension expense

Plan assets

PBO

2017

Plan assets

Amortization of net gain-OCI

PBO

Prior service cost-AOCI

450

PBO

1,800$

400$

($ in millions)

KOLLAR COMPANY

Given Data P17-12:

Projected benefit obligation, 12/31/2014

Prior service cost, 1/2/2016

2017 actual return on plan assets

Years gains and losses amortized

Plan asset balance at fair value, 1/1/2016

2016 contribution

2017 contribution

Expected long-term rate of return on assets

2016 actual return on plan assets

Net gain-AOCI on 1/1/2016

Service cost, 2016

Service cost, 2017

Discount rate

Payments to retirees, 2016

Payments to retirees, 2017

Student Name:

Class:

2,400$

Plus: loss

prior service cost-AOCI

Interest cost

Loss (gain) on PBO

Less: Retiree benefits

End of 2016

Service cost

Interest cost

Requirement 4: Pension expense

Actual return

Service cost

2,300$

Excess

10% of $2,400

Amount amortized

330$

Net gain, Jan. 1

Requirement 5: Average remaining service life of active employees

Problem 17-14

Requirement 1: Actual return on plan assets

Plan assets

Beginning of 2016

Requirement 3: Service cost

PBO:

McGraw-Hill/Irwin

Instructor

Beginning of 2016

HILTON PANELING, INC.

($ in 000s)

Cash contributions

Less: Retiree benefits

Expected return

Requirement 2: Loss or gain on plan assets

Actual return

Actual return

2016 2016

Beginning Ending

Balances Balances

2,300$ 2,501$

Given Data P17-14:

($ in 000s)

HILTON PANELING, INC.

Projected benefit obligation

Net gain-AOCI

Paid to retirees in 2016

Employer contribution in 2016

Actuary‘s discount rate

Prior service cost-AOCI

Expected rate of return on assets

Plan assets

Funded status

Student Name:

Class:

Net

Prior Pension

Plan Service Net Pension Liability/

debits otherwise

PBO Assets Cost Loss Expense Cash Asset

Net loss

Gain on PBO

(4,100) 4,530 840 477 430

(70) 70 –

Amortization of:

Prior service cost

AOCI

Problem 17-15

McGraw-Hill/Irwin

Instructor

Pension Spreadsheet

METRO RECREATION

($ in 000s)

( )s indicate credits;

Balance, January 1, 2016

Loss on assets

Interest cost, 7%

Jan. 1 Dec. 31

Given Data P17-15:

($ in 000s)

METRO RECREATION

Pension related data:

Projected benefit obligation

Accumulated benefits obligation

Plan assets (fair value)

Interest (discount) rate

Expected return on plan assets

Prior service cost-AOCI

Net loss-AOCI

Average remaining service life, years

Gain due to changes in actuarial assumptions

Contributions to pension fund (end of year)

Pension benefits paid (end of year)