Exercise 10–9

Requirement 1

Tractor ($5,000 cash + 18,783† present value of note) …………. 23,783

Requirement 2

Requirement 3

10–22 Intermediate Accounting, 8/e

Exercise 10–10

Land:

Purchase price $1,200,000

Building:

Architect’s fees $ 50,000

Equipment:

Purchase price $860,000

Land improvements:

Landscaping $45,000

Fork lifts:

Exercise 10–11

Requirement 1

To record the acquisition of land in exchange for common stock.

February 1, 2016

Land ……………………………………………………………………. 900,000

To record the acquisition of a building through purchase and donation.

November 2, 2016

Building ……………………………………………………………….. 6,000,000

Requirement 2

As with U.S. GAAP, the building would be valued at fair value. However, the

amount donated ($2,000,000) would not be recorded as revenue. Instead, IFRS

Exercise 10–12

Requirement 1

IFRS requires that government grants be recognized in income over the periods

necessary to match them on a systematic basis with the related costs that they are

Requirement 2

Alternative 1:

A correcting entry is necessary to eliminate the revenue recognized and reduce

the cost of the equipment:

Alternative 2:

A correcting entry is necessary to eliminate the revenue recognized and record

deferred income.

Exercise 10–13

Requirement 1

($ in thousands)

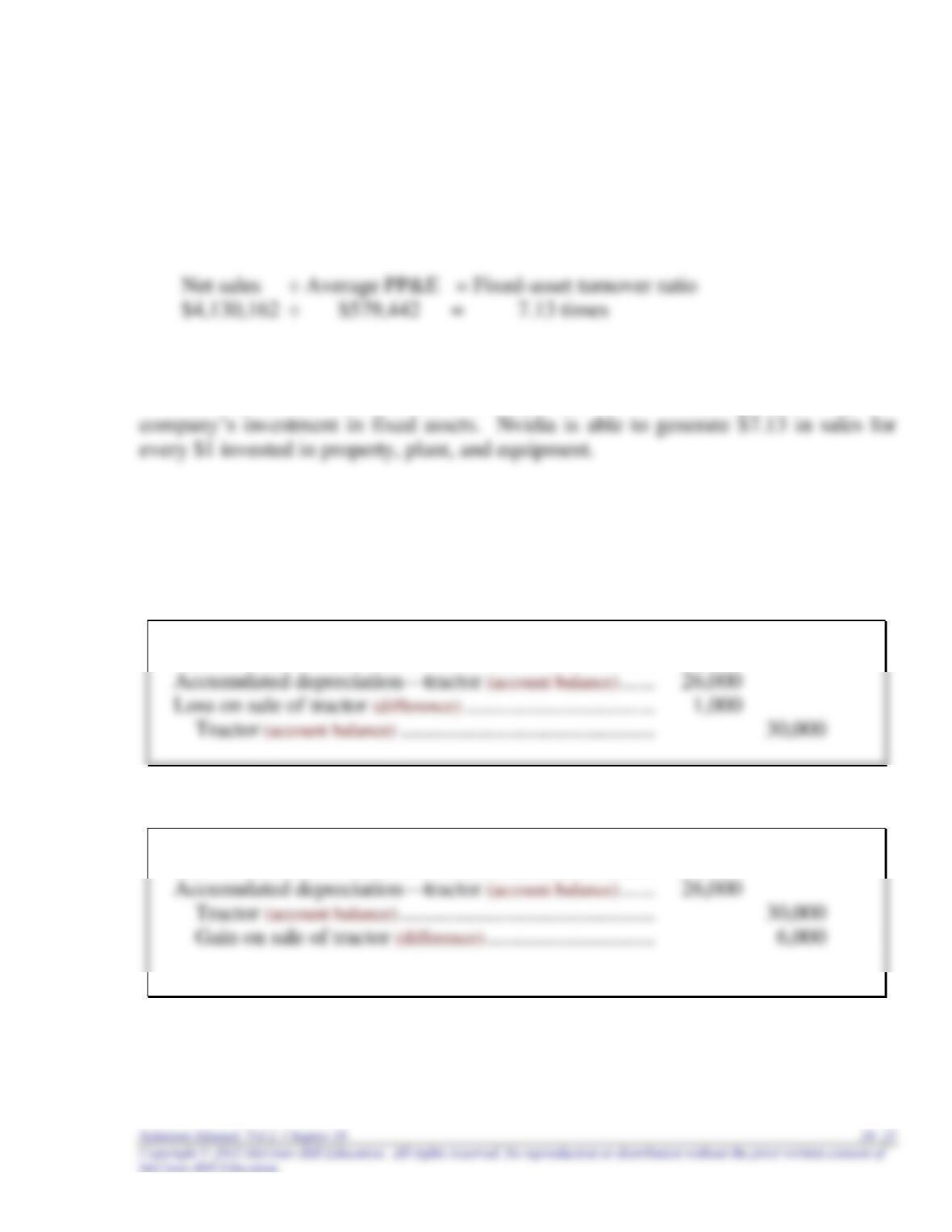

Average PP&E for 2014 = ($582,740 + 576,144) ÷ 2 = $579,442

Requirement 2

The fixed-asset turnover ratio indicates the level of sales generated by the

Exercise 10–14

Requirement 1

Cash …………………………………………………………………….. 3,000

Requirement 2

Cash …………………………………………………………………….. 10,000

10–26 Intermediate Accounting, 8/e

Exercise 10–15

Requirement 1

To record the sale of the patent.

July 15, 2016

Cash …………………………………………………………………….. 750,000

Exercise 10–16

Equipment—new ($200,000 + 60,000) …………………………. 260,000

Exercise 10–17

Equipment—new ($170,000 + 60,000) …………………………. 230,000

10–28 Intermediate Accounting, 8/e

Exercise 10–18

Requirement 1

Fair value of land + Cash given = Fair value of equipment

Requirement 2

Equipment ($150,000 + 10,000) …………………………………… 160,000

Exercise 10–19

Requirement 1

Fair value of land – Cash received = Fair value of equipment

Requirement 2

Equipment ($150,000 – 10,000) …………………………………… 140,000

Exercise 10–20

Requirement 1

Fair value of old land + Cash given = Fair value of new land

Requirement 2

Land—new ($72,000 + 14,000) …………………………………… 86,000

Requirement 3

Land—new ($30,000 + 14,000) …………………………………… 44,000

10–30 Intermediate Accounting, 8/e

Exercise 10–21

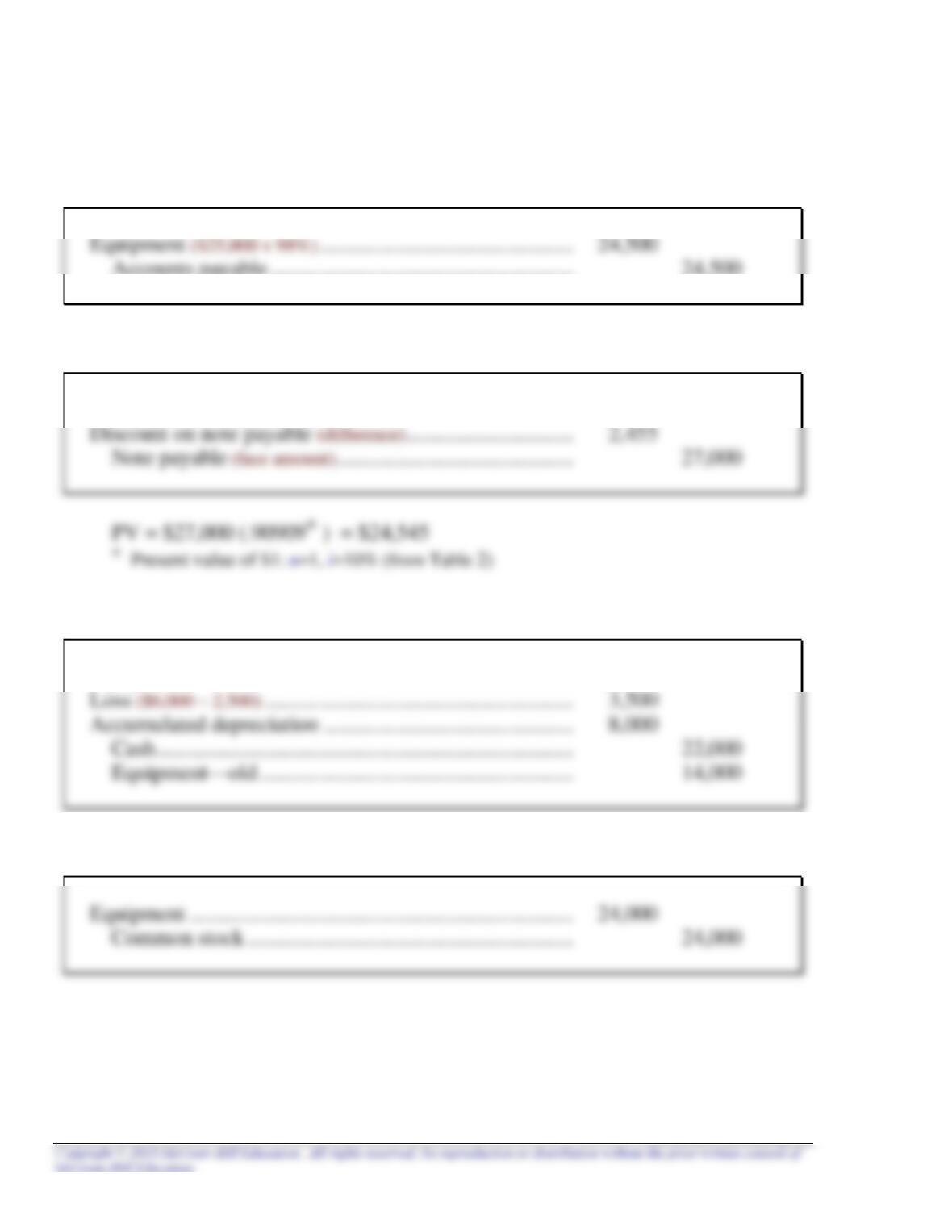

1. To record the purchase of equipment on account.

2. To record the acquisition of equipment in exchange for a note.

Equipment (determined below) ……………………………………. 24,545

3. To record the exchange of old equipment for new equipment.

Equipment—new ($2,500 + 22,000) …………………………….. 24,500

4. To record the acquisition of equipment by the issuance of stock.

Exercise 10–22

Requirement 1

The Codification topic number for nonmonetary transactions is FASB ASC 845:

Requirement 2

The specific citations that describe the required disclosures for nonmonetary

Requirement 3

An entity that engages in one or more nonmonetary transactions during a period shall

disclose in financial statements for the period all of the following:

a. The nature of the transactions

10–32 Intermediate Accounting, 8/e

Exercise 10–23

The FASB Accounting Standards Codification® represents the single source of

authoritative U.S. generally accepted accounting principles. The specific citation for

each of the following items is:

1. The disclosure requirements in the notes to the financial statements for

depreciation on property, plant, and equipment:

FASB ASC 360–10–50–1: “Property, Plant, and Equipment–Overall–Disclosure.”

Because of the significant effects on financial position and results of operations of

Exercise 10–23 (continued)

2. The criteria for determining commercial substance in a nonmonetary

exchange:

FASB ASC 845–10–30–4: “Nonmonetary Transactions–Overall–Initial

Measurement.”

A nonmonetary exchange has commercial substance if the entity’s future cash

10–34 Intermediate Accounting, 8/e

Exercise 10–23 (continued)

3. The disclosure requirements for interest capitalization:

FASB ASC 835–20–50–1: “Interest Capitalization–Overall–Disclosure.”

An entity shall disclose the following information with respect to interest cost in

Exercise 10–23 (concluded)

4. The elements of costs to be included as R&D activities:

FASB ASC 730–10–25–2: “Research & Development–Overall–Recognition.”

Elements of costs shall be identified with research and development activities as follows:

a. Materials, equipment, and facilities. The costs of materials (whether from the entity‘s

normal inventory or acquired specially for research and development activities) and

b. Personnel. Salaries, wages, and other related costs of personnel engaged in research

and development activities shall be included in research and development costs.

c. Intangible assets purchased from others. The costs of intangible assets that are

purchased from others for use in research and development activities and that have

alternative future uses (in research and development projects or otherwise) shall be

10–36 Intermediate Accounting, 8/e

Exercise 10–24

Average accumulated expenditures:

Interest capitalized:

$3,000,000

* Weighted-average rate of all other debt:

$2,000,000 x 9% = $180,000

Exercise 10–25

Average accumulated expenditures for 2016:

January 1, 2016 $500,000 x 12/12 = $ 500,000

Interest capitalized:

Exercise 10–26

Average accumulated expenditures for 2016:

January 1, 2016 $ 600,000 x 12/12 = $ 600,000

Interest capitalized:

$2,050,000

* Weighted-average rate of all other debt:

$5,000,000 x 12% = $600,000

Exercise 10–27

Average accumulated expenditures for 2016:

10–38 Intermediate Accounting, 8/e

July 1, 2016 $ 400,000 x 6/6 = $ 400,000

Interest capitalized in 2016:

Average accumulated expenditures for 2017:

January 1, 2017 ($1,600,000 + 19,200) $1,619,200 x 3/3 = $1,619,200

Interest capitalized in 2017:

Exercise 10–28

To expense R&D costs incorrectly capitalized.

Research and development expenditures:

Basic research to develop the technology $2,000,000

Engineering design work 680,000

10–40 Intermediate Accounting, 8/e

Exercise 10–29

Research and development expense:

Salaries and wages for lab research $ 400,000