CHAPTER 6

TIME VALUE OF MONEY CONCEPTS

Overview

Time value of money concepts, specifically future value and present value, are essential in a

variety of accounting situations. These concepts and the related computational procedures are the

subjects of this chapter. Present values and future values of single amounts and present values and

future values of annuities (series of equal periodic payments) are described separately but shown to

be interrelated.

Learning Objectives

LO6-1 Explain the difference between simple and compound interest.

LO6-2 Compute the future value of a single amount.

LO6-3 Compute the present value of a single amount.

LO6-4 Solve for either the interest rate or the number of compounding periods when present value

and future value of a single amount are known.

LO6-5 Explain the difference between an ordinary annuity and an annuity due situation.

LO6-6 Compute the future value of both an ordinary annuity and an annuity due.

LO6-7 Compute the present value of an ordinary annuity, an annuity due, and a deferred annuity.

LO6-8 Solve for unknown values in annuity situations involving present value.

LO6-9 Briefly describe how the concept of the time value of money is incorporated into the

valuation of bonds, long-term leases, and pension obligations.

Lecture Outline

Part A: Basic Concepts

I. Time Value of Money (T6-1)

A. The time value of money means that money can be invested today to earn interest and

grow to a larger dollar amount in the future.

B. Interest is the amount of money paid or received in excess of the amount borrowed or

lent.

1. Simple interest is computed by multiplying an initial investment times both the

applicable interest rate and the period of time for which the money is used.

2. Compound interest includes interest not only on the initial investment but also on the

accumulated interest in previous periods. (T6-2)

6-2 Intermediate Accounting, 8/e

II. Valuing a Single Cash Flow Amount

A. The future value of a single amount (FV) is the amount of money that a dollar will grow to

at some point in the future.

1. The future value of a single amount can be calculated by multiplying the initial

investment (I) times (1 + i)n

where: i = interest rate

n = number of compounding periods (T6-3)

2. The future value also can be determined by using Table 1, Future Value of $1. (T6-4)

B. The present value of a single amount (PV) is today’s equivalent of a particular amount in

the future.

1. The present value of a single amount can be calculated by dividing the future value by

(1 + i)n. (T6-5)

2. As with future value, we can use a table, Table 2, Present Value of $1, to determine

present value. (T6-6)

C. Solving for other values when PV and FV are known

1. There are four variables in the process of adjusting single cash flow amounts for the

time value of money: the present value (PV), the future value (FV), the number of

compounding periods (n), and the interest rate (i).

2. If you know any three of these, the fourth can be determined. (T6-7) (T6–8)

III. Accounting Applications of Present Value Techniques – Single Cash Amount

A. Most receivables and payables are valued at the present value of future cash flows,

reflecting an appropriate time value of money.

B. While most notes, loans, and mortgages explicitly state an interest rate that will properly

reflect the time value of money, there can be exceptions. (T6-9)

IV. Expected Cash Flow Approach

A. SFAC No. 7 provides a framework for using future cash flows as the basis for accounting

measurement and asserts that the objective in valuing an asset or liability using present

value is to approximate the fair value of that asset or liability.

B. Traditionally, the way uncertainty has been considered in present value calculations has

been by discounting the best estimate of future cash flows applying a discount rate that has

been adjusted to reflect the uncertainty or risk of those cash flows. SFAC No. 7 offers an

alternative method called the expected cash flow approach. This approach adjusts for

uncertainty or risk of cash flows by incorporating specific probabilities of cash flows into

the analysis. (T6-10)

Part B: Basic Annuities

I. Ordinary Annuity and Annuity Due (T6-11)

A. An annuity is a series of equal-sized cash flows occurring over equal intervals of time.

B. In an ordinary annuity cash flows occur at the end of each period.

C. In an annuity due cash flows occur at the beginning of each period.

II. Future Value of an Annuity

A. The future value of an annuity can be determined by summing the future value of each of

III. Present Value of an Annuity

A. The present value of an annuity can be determined by summing the present value of each

of the individual cash payments or by using the appropriate annuity table, Table 5, Present

IV. Financial Calculators and Excel

Financial calculators can be used to solve future and present value problems. Also, many

professionals choose to use spreadsheet software, such as Excel, to solve time value of money

problems. These spreadsheets can be used in a variety of ways. A template can be created

using the formulas or you can use the software’s built-in financial functions.

V. Solving for Unknown Values in Present Value Situations

A. In present value problems involving annuities, there are four variables: present value of an

annuity (PVA or PVAD), the amount of each annuity payment, the number of periods (n),

and the interest rate (i).

B. If you know any three of these, the fourth can be determined. (T6-17) (T6-18)

6-4 Intermediate Accounting, 8/e

VI. Accounting Applications of Present Value Techniques – Annuities

A. Because financial instruments typically specify equal periodic payments, accounting

applications incorporating the time value of money concept quite often involve annuity

situations.

B. Three examples are:

1. The valuation of long-term bonds. (T6-19)

VII. Summary of Time Value of Money Concepts (T6-22)

PowerPoint Slides

A PowerPoint presentation of the chapter is available at the textbook website.

Teaching Transparency Masters

The following can be reproduced on transparency film as they appear here, or

TIME VALUE OF MONEY

➢ Time value of money ⎯ Money can be invested today to

earn interest and grow to a larger dollar amount in the

future.

➢ Interest ⎯ The rent paid for the use of money for some

T6-1

6-6 Intermediate Accounting, 8/e

COMPOUND INTEREST

Compound interest includes interest not only on the initial

investment but also on the accumulated interest in previous

periods.

Example:

Cindy Johnson invested $1,000 in a savings account paying

10% interest compounded annually.

Interest

(Interest rate x

Date Outstanding balance) Balance

Initial deposit $1,000

If interest is compounded twice a year:

Interest

(Interest rate x

Date Outstanding balance) Balance

FUTURE VALUE OF A SINGLE AMOUNT

Future

Value

$1,000 ——————————————-> $1,331

End of End of End of

FV = I (1 + i)n

T6-3

6-8 Intermediate Accounting, 8/e

USING A TABLE

The future value also can be determined using

Table 1. The table contains the future value of

$1 invested for various periods of time, n, at

various interest rates, i.

Interest Rates (i)

7%

8%

9%

10%

11%

12%

Periods (n)

1

1.07000

1.08000

1.09000

1.10000

1.11000

1.12000

2

1.14490

1.16640

1.18810

1.21000

1.23210

1.25440

3

1.22504

1.25971

1.29503

1.33100

1.36763

1.40493

4

1.31080

1.36049

1.41158

1.46410

1.51807

1.57352

5

1.40255

1.46933

1.53862

1.61051

1.68506

1.76234

Illustration 6-1

FV = I x FV factor

T6-4

PRESENT VALUE OF A SINGLE AMOUNT

The previous example reveals that $1,000 invested today is

Thus, $1,000 is the present value (PV) of the single sum of

$1,331 to be received at the end of three years.

FV = PV (1 + i)n

T6-5

6-10 Intermediate Accounting, 8/e

USING A TABLE

The present value also can be determined

using Table 2. The table contains the present

Interest Rates (i)

7%

8%

9%

10%

11%

12%

Periods (n)

1

.93458

.92593

.91743

.90909

.90090

.89286

2

.87344

.85734

.84168

.82645

.81162

.79719

3

.81630

.79383

.77218

.73119

.71178

4

.76290

.73503

.70843

.68301

.65873

.63552

5

.71299

.68058

.64993

.62092

.59345

.56743

Illustration 6-2

PV = FV x PV factor

SOLVING FOR OTHER VALUES WHEN FV AND PV ARE KNOWN

There are four variables in the process of adjusting single cash flow

If you know any three of these, the fourth can be determined.

Suppose a friend asks to borrow $500 today and promises to repay

you $605 two years from now. What is the annual interest rate you

would be agreeing to?

Illustration 6-3

Present Future

Value Value

$500 <————————> $605

End of End of

$500 = $605 x ? *

present future

When you consult the present value table, Table 2, you search row 2 (n=2) for

this value and find it in the 10% column. So the effective interest rate is 10%.

T6-7

6-12 Intermediate Accounting, 8/e

DETERMINING n WHEN PV, FV, AND i ARE KNOWN

You want to invest $10,000 today to accumulate $16,000 for graduate

Illustration 6-4

Present Future

Value Value

$10,000 <——————————————————-> $16,000

End of End of End of End of

$10,000 = $16,000 x ? *

present future

value value

When you consult the present value table, Table 2, you search the

T6-8

VALUING A NOTE ⎯ ONE PAYMENT ⎯ NO EXPLICIT INTEREST

The Stridewell Wholesale Shoe Company recently sold a large order

of shoes to the Harmon Sporting Goods. Terms of the sale require

Harmon to sign a noninterest-bearing note of $60,500 with payment

due in two years.

Illustration 6-6

Present Future

Value Value

? <————————– $60,500

End of End of

0 year 1 year 2

____________________________

n = 2, i = 10%

Using the present value of $1 table,

$60,500 x .82645* = $50,000

future present

Both the note receivable for Stridewell and the note payable for

T6-9

6-14 Intermediate Accounting, 8/e

EXPECTED CASH FLOW APPROACH

➢ Present value measurement has long been integrated with accounting valuation.

➢ Traditionally, the way uncertainty has been considered in present value

calculations has been by discounting the best estimate of future cash flows

applying a discount rate that has been adjusted to reflect the uncertainty or risk

of those cash flows.

LDD Corporation faces the likelihood of having to pay an uncertain amount in five years in

connection with an environmental cleanup. The future cash flow estimate is in the range of $100

million to $300 million with the following estimated probabilities:

Loss amount Probability

$100 million 10%

$200 million 60%

$300 million 30%

The expected cash flow, then, is $220 million:

$100 x 10% = $10 million

If the risk-free rate of interest is 5%, LDD will report a liability of $172,376,600, the present value

of the expected cash outflow:

$220,000,000

Illustration 6-7

T6–10

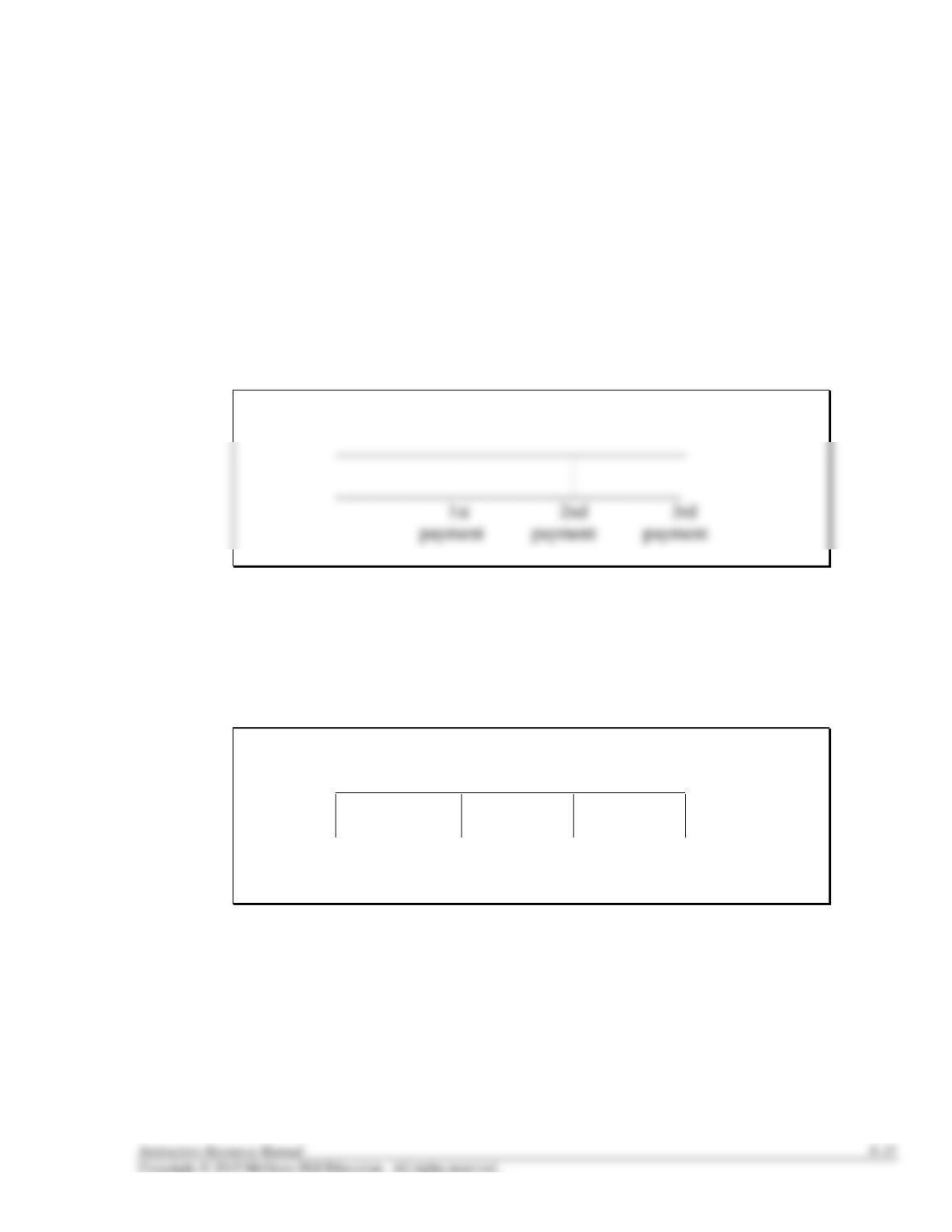

ANNUITIES

An annuity is a series of equal-sized cash flows occurring

over equal intervals of time.

➢ In an ordinary annuity cash flows occur at the end of

each period.

12/31/16 12/31/17 12/31/18 12/31/19

➢ In an annuity due cash flows occur at the beginning of

each period.

12/31/16 12/31/17 12/31/18 12/31/19

_____________________________________

1st 2nd 3rd

payment payment payment

T6–11

6-16 Intermediate Accounting, 8/e

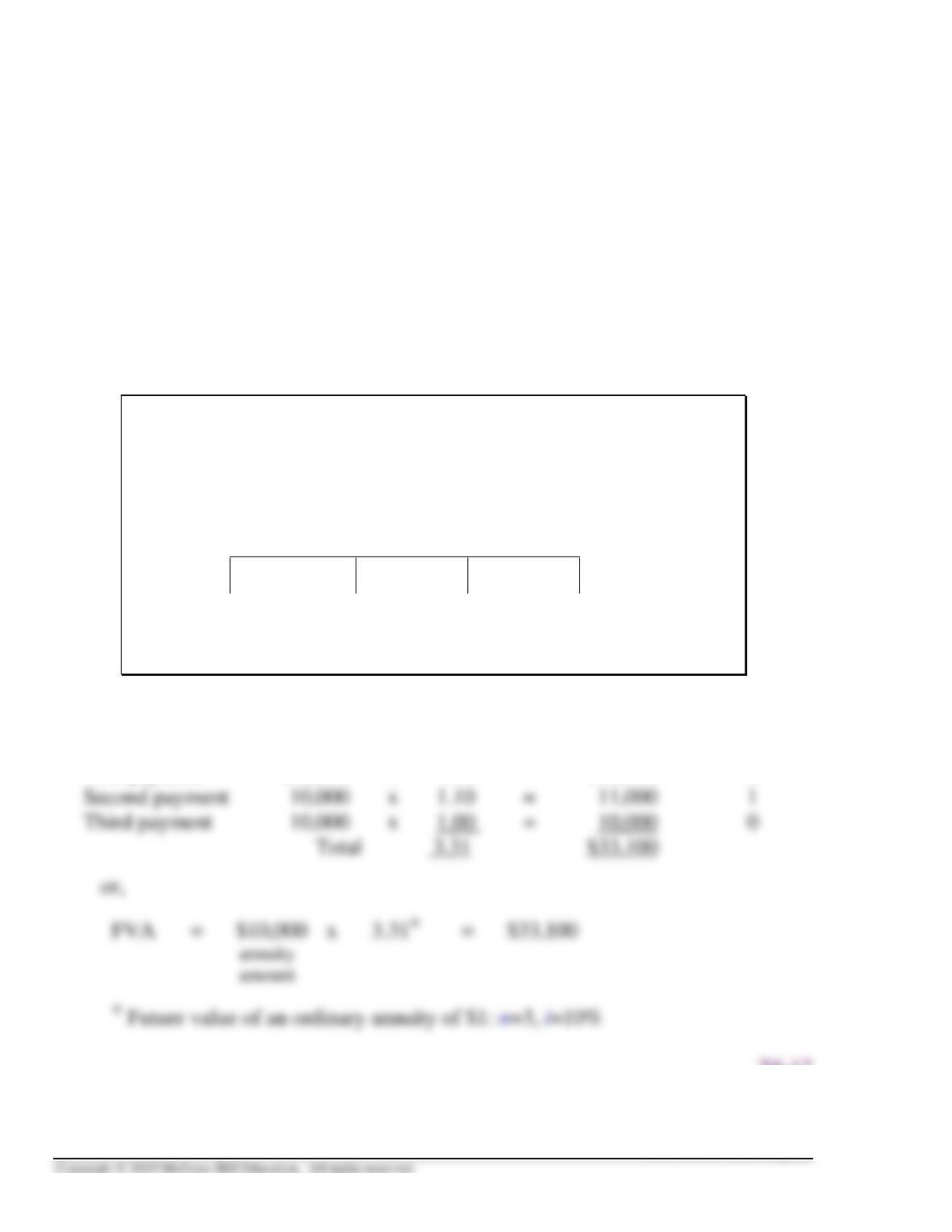

FUTURE VALUE OF AN ORDINARY ANNUITY

Sally Rogers wants to accumulate a sum of money to pay for graduate

school. Rather than investing a single amount today that will grow to

a future value, she decides to invest $10,000 a year over the next

three years in a savings account paying 10% interest compounded

annually. She decides to make the first payment to the bank one year

from today.

Illustration 6-8

Future

Value

?

End of End of End of

0 year 1 year 2 year 3

____________________________________________

$10,000 $10,000 $10,000

n = 3, i= 10%

FV of $1 Future Value

Payment i=10% (at the end of year 3) n

First payment $10,000 x 1.21 = $12,100 2

T6–12