Exercise 4–3

Requirement 1

GENERAL LIGHTING CORPORATION

Income Statement

For the Year Ended December 31, 2016

Revenues and gains:

Sales ………………………………………………………..

$2,350,000

Interest ……………………………………………………..

Expenses and losses:

Cost of goods sold ……………………………………..

$1,200,300

Selling ……………………………………………………..

300,000

General and administrative ………………………….

Interest ………………………………………………………

Loss on sale of investments ………………………..

Loss from inventory write-down …………………

1,962,800

$ 280,320

4–22 Intermediate Accounting, 8/e

Exercise 4–3 (concluded)

Requirement 2

GENERAL LIGHTING CORPORATION

Income Statement

For the Year Ended December 31, 2016

Sales revenue ……………………………………………….

$2,350,000

Operating expenses:

Selling ………………………………………………………

$300,000

General and administrative ………………………….

Other income (expense):

Interest revenue ………………………………………….

80,000

Loss on sale of investments …………………………

(22,500)

Interest expense …………………………………………

(90,000)

Exercise 4–4

LINDOR CORPORATION

Statement of Comprehensive Income

For the Year Ended December 31, 2016

Sales revenue ………………………………………………

$2,300,000

Cost of goods sold ……………………………………….

Gross profit …………………………………………………

Operating expenses:

Selling and administrative …………………………...

420,000

Operating income ………………………………………..

Other income (expense):

Interest expense …………………………………………..

(40,000)

Income before income taxes …………………………..

440,000

Income tax expense * ……………………………………

4–24 Intermediate Accounting, 8/e

Exercise 4–5

AXEL CORPORATION

Income Statement

For the Year Ended December 31, 2016

Sales revenue ……………………………………………….

$ 592,000

Cost of goods sold ………………………………………..

Gross profit ………………………………………………….

267,000

Operating expenses:

Selling ……………………………………………………..

$67,000

Administrative ………………………………………….

Restructuring costs …………………………..………..

Operating income …………………………..…………….

Other income (expense):

Interest and dividends …………………………………

32,000

Income before income taxes …………………………..

Income tax expense* …………………………………….

Net income ………………………………………………….

Interest expense …………………………………………

(26,000)

Exercise 4–6

CHANCE COMPANY

Partial Income Statement

For the Year Ended December 31, 2016

Income from continuing operations ………………………………

$ 350,000

Discontinued operations:

Loss from operations of discontinued component

Loss on discontinued operations …………………………………..

Net income ……………………………………………………….………..

Earnings per share:

Income from continuing operations ………………………………

Loss on discontinued operations ………………………………….

Net income ……………………………………………………….……….

* Loss on discontinued operations:

Loss on sale of assets $(400,000)

4–26 Intermediate Accounting, 8/e

Exercise 4–7

ESQUIRE COMIC BOOK COMPANY

Partial Income Statement

For the Year Ended December 31, 2016

Income from continuing operations * …………………………….

$ 552,000

Discontinued operations:

Income from operations of discontinued component

Income on discontinued operations ………………………………..

Net income ………………………………………………………………….

* Income from continuing operations:

Income before considering additional items $1,000,000

Exercise 4–8

Requirement 1

KANDON ENTERPRISES, INC.

Partial Income Statement

For the Year Ended December 31, 2016

Income from continuing operations ………………………………

$ 400,000

Discontinued operations:

Loss on discontinued operations ………………………………….

Net income ……………………………………………………….……….

$ 286,000

* Loss on discontinued operations:

Loss from operations $(140,000)

4–28 Intermediate Accounting, 8/e

Exercise 4–8 (concluded)

Requirement 2

KANDON ENTERPRISES, INC.

Partial Income Statement

For the Year Ended December 31, 2016

Income from continuing operations ……………………………..

$ 400,000

Discontinued operations:

Loss on discontinued operations ………………………………….

Net income ……………………………………………………………….

$ 316,000

Exercise 4–9

Pretax income from continuing operations $14,000,000

Income tax expense (5,600,000)

*1 – tax rate of 40% = 60%

Pretax income of division $4,000,000

Exercise 4–10

Earnings per share:

Income from continuing operations $5.00

4–30 Intermediate Accounting, 8/e

Exercise 4–11

THE MASSOUD CONSULTING GROUP

Statement of Comprehensive Income

For the Year Ended December 31, 2016

Net income ………………………………………………….

$1,354,000

Other comprehensive income (loss):

Total other comprehensive income …………………

Comprehensive income …………………………………

Exercise 4–12

1. b Purchase of equipment for cash.

Exercise 4–13

Bluebonnet Bakers

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash flows from operating activities:

Collections from customers $ 380,000

Interest on note receivable 6,000

Cash flows from investing activities:

Collection of note receivable 50,000

Cash flows from financing activities:

Proceeds from note payable 100,000

4–32 Intermediate Accounting, 8/e

Exercise 4–14

Cash collected for interest, considered an operating cash flow by U.S. GAAP,

could be classified as either an operating cash flow or an investing cash flow

according to International Accounting Standards.

Cash paid for interest, considered an operating cash flow by U.S. GAAP, could

BLUEBONNET BAKERS

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash flows from operating activities:

Collections from customers $ 380,000

Purchase of inventory (160,000)

Cash flows from investing activities:

Collection of note receivable 50,000

Interest on note receivable 6,000

Cash flows from financing activities:

Proceeds from note payable 100,000

Payment of note payable (25,000)

Exercise 4–15

Cash flows from operating activities:

Net income $17,300

Adjustments for noncash effects:

Exercise 4–16

Requirement 1

Operating Investing Financing

1. $300,000

2. $(10,000) ✓

4–34 Intermediate Accounting, 8/e

Exercise 4–16 (concluded)

Requirement 2

WAINWRIGHT CORPORATION

Statement of Cash Flows

For the Month Ended March 31, 2016

Cash flows from operating activities:

Collections from customers $ 55,000

Payment of rent (5,000)

Noncash investing and financing activities:

Acquired $40,000 of equipment by paying cash and issuing a note as follows:

Cost of equipment $40,000

Exercise 4–17

Cash flows from operating activities:

Net income $624,000

Adjustments for noncash effects:

Depreciation and amortization expense 87,000

Changes in operating assets and liabilities:

Exercise 4–18

Cash flows from operating activities:

Net income $1,250,000

Adjustments for noncash effects:

Depreciation expense 140,000

Exercise 4–19

Consistent with U.S. GAAP, international standards also require a statement of

cash flows. Consistent with U.S. GAAP, cash flows are classified as operating,

4–38 Intermediate Accounting, 8/e

Exercise 4–19 (concluded)

Accordingly, the statement of cash flows prepared according to IFRS mostly

likely would be presented as follows (differences from U.S. GAAP in italics):

BRONCO METALS

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash flows from operating activities:

Collections from customers $ 353,000

Purchase of inventory (186,000)

Exercise 4–20

TIGER ENTERPRISES

Statement of Cash Flows

For the Year Ended December 31, 2016

($ in thousands)

Cash flows from operating activities:

Net income $ 900

Adjustments for noncash effects:

Depreciation expense 240

Changes in operating assets and liabilities:

Decrease in accounts receivable 80

Increase in inventory (40)

4–40 Intermediate Accounting, 8/e

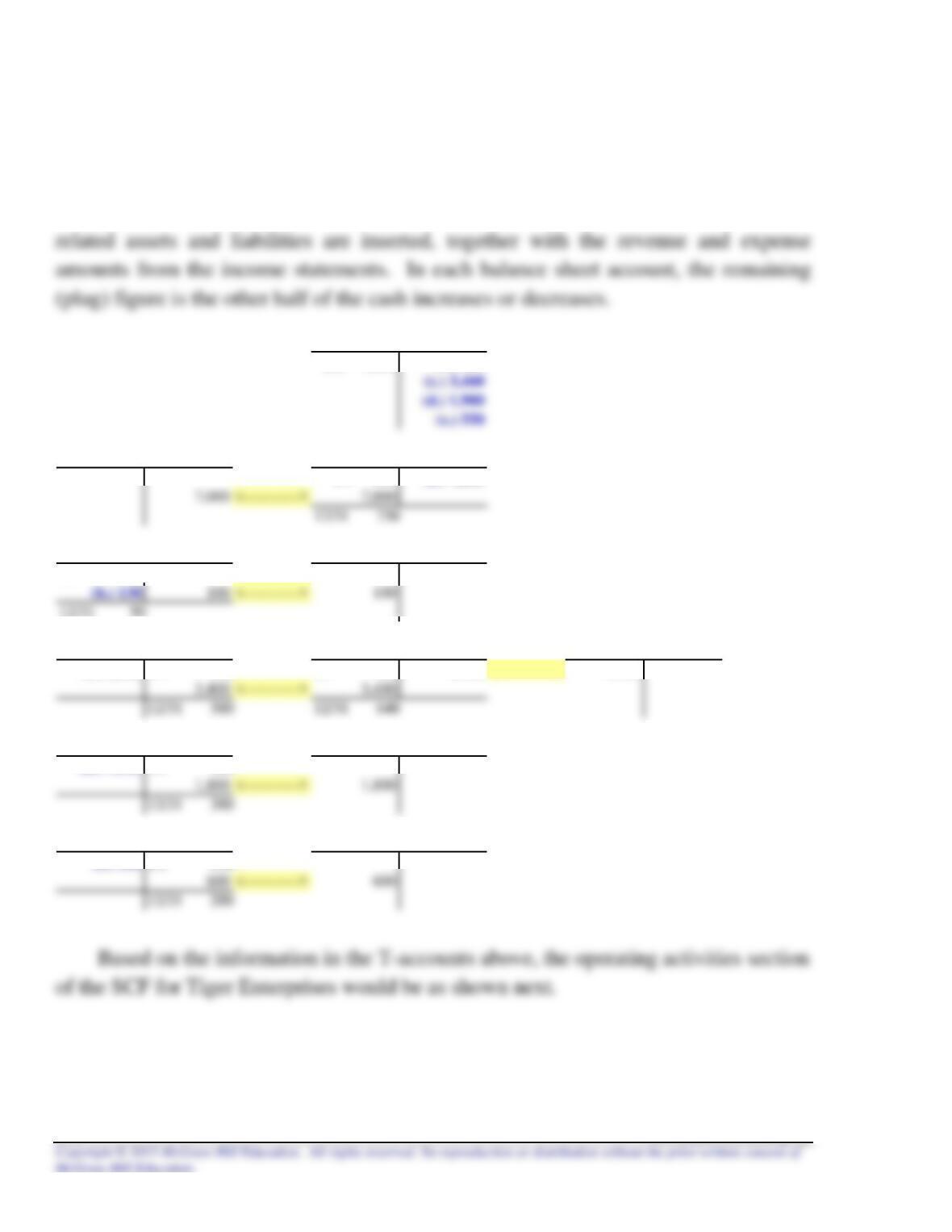

Exercise 4–21

The T-account analysis of the transactions related to operating cash flows is

shown below. To derive the cash flows, the beginning and ending balances in the

Cash Flows (Operating)

(a.) 7,080 (b.) 130

Sales Revenue Accounts Receivable

1/1 830 (a.) 7,080

Prepaid Insurance Insurance Expense

1/1 20

12/31 50

Accounts Payable Inventory Cost of Goods Sold

(c.) 3,460 1/1 360

1/1 600

3,360 <———–> 3,360

Admin. & Other Payables Admin. & Other Expense

(d.) 1,900 1/1 400

Income Taxes Payable Income Tax Expense

(e.) 550 1/1 150