14-36 Intermediate Accounting, 8/e

DEBT CONTINUED, WITH MODIFIED TERMS

WHEN TOTAL CASH PAYMENTS

EXCEED THE BOOK VALUE OF THE DEBT

If the payments exceed the amount owed, the restructured debt

agreement still provides interest on the debt – but less than before

the agreement was revised. No longer is the effective rate 10%.

The accounting objective now is to determine what the new

effective rate is and record interest for the remaining term of the

loan at that new, lower rate.

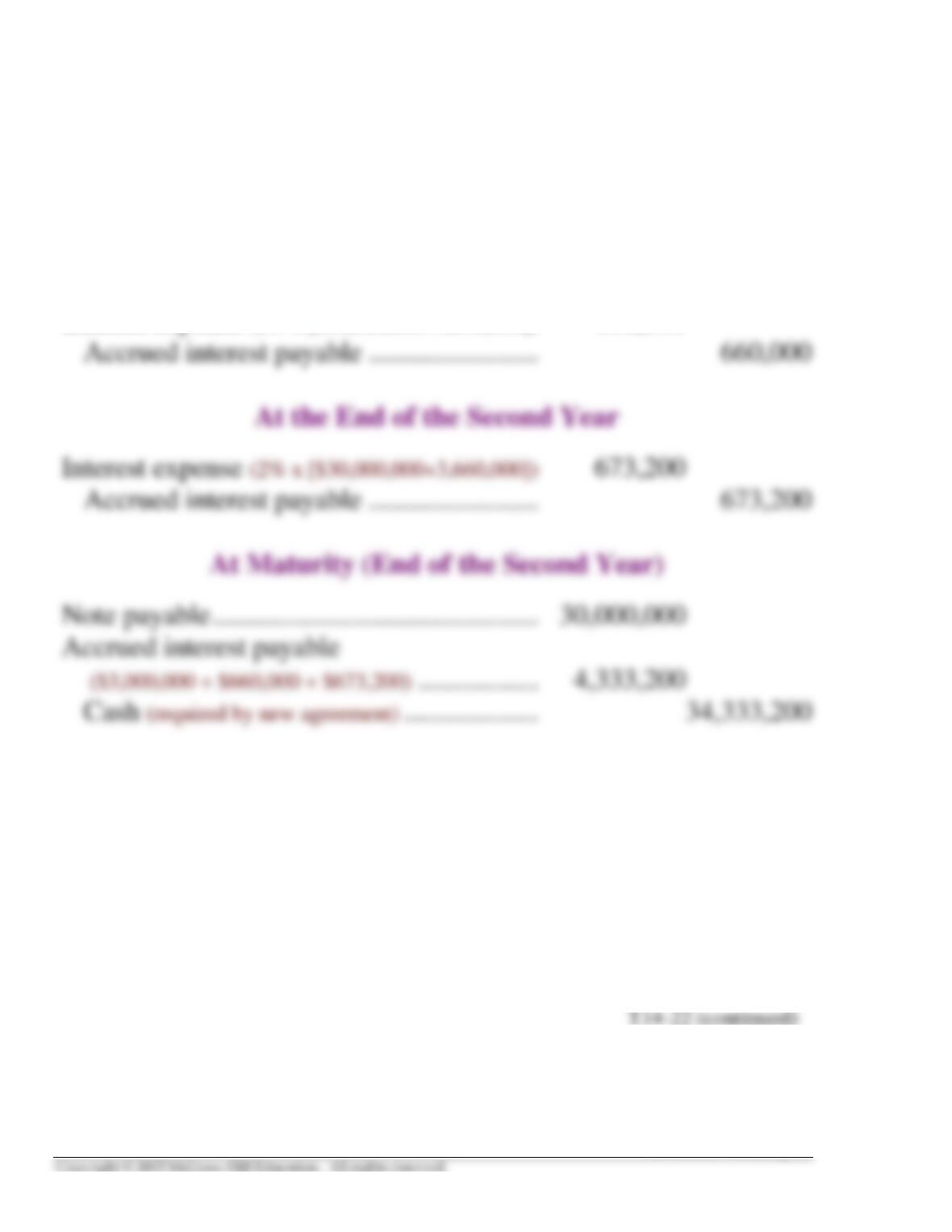

Illustration – Brillard Properties owes First Prudent Bank $30

million, under a 10% note with 2 years remaining to maturity.

Due to Brillard’s financial difficulties, the previous year’s

interest ($3 million) was not paid. First Prudent Bank agrees to:

(1) delay the due date for all cash payments until maturity, and

(2) accept $34,333,200 at that time in full settlement of the debt.

Analysis:

T14-22 (continued)

WHEN TOTAL CASH PAYMENTS

EXCEED THE BOOK VALUE OF THE DEBT

(continued)

The discount rate that “equates” the present value of the debt

($33 million) and its future value ($34,333,200) is the effective

rate of interest.

CALCULATION OF THE NEW EFFECTIVE INTEREST RATE:

• $33,000,000÷ $34,333,200= .9612 – the Table 2 value for n = 2, i = ?

• In row 2 of Table 2, the number .9612 is in the 2% column. So, this is the

T14-22 (continued)

14-38 Intermediate Accounting, 8/e

WHEN TOTAL CASH PAYMENTS

EXCEED THE BOOK VALUE OF THE DEBT

(continued)

At the End of the First Year

Interest expense (2% x [$30,000,000+3,000,000]) 660,000

Suggestions for Class Activities

1. Real World Scenario

An article in BARRON’S, entitled “Wall Street’s Latest Illusion,” reported that “Goldman Sachs,

Morgan Stanley and other firms are booking profits from the falling value of their own debt.” The

article asserts that when a company’s credit weakens, it reports a gain.

Suggestions:

Have the students consider this assertion and explain how it occurs.

Points to note:

A company is not required to, but has the option to, value some or all of its financial assets and

2. Real World Scenario

Texas Eastern Transmission Corporation is a unit of PanEnergy Corporation. In a press release,

the company announced the retirement of some of its bonds. Excerpts from the press release follow:

…. $100 million face value of outstanding of 10 1/8% debentures and $150 million outstanding

of the 10% debentures are outstanding. The 10 1/8% debentures are due Sept. 1, 2015 and the

10% debentures are due Oct. 1, 2015. The redemption price for the 10 1/8% debentures is

105.062% of the principal amount to be redeemed, together with interest accrued to the Oct. 1

redemption date.

Suggestions:

Have the students consider how they would account for the retirement of the 10 1/8 bonds. Ask

them to assume they were issued at face value.

Points to note:

14-40 Intermediate Accounting, 8/e

3. Spreadsheet Activity

Have students create a functional debt amortization schedule in Excel. Suggest that the spreadsheet:

1. Include cells for the number of periods, the stated interest rate, the effective interest rate, the

principal, the present value of cash flows, and periodic cash payment. The cells should be

“defined” as the respective variables so that formulas in the schedule that refer to the variable

names will pick up the values entered in the cells.

2. The initial balance can be made to calculate the bond price if a principal is provided by the user

in the principal cell, or to assume an installment note and calculate the PV of cash payments if

the principal is not provided by the user in the principal cell.

3. In addition, the cash payments cell can be made to calculate installment payments if the PV is

provided by the user in a PV cell. Thus, if “PV” is blank, the calculation will default to a bond or

note with the principal paid at maturity.

Provide students with various variable values to conduct several “what if?“ exercises.

4. Spreadsheet Activity

Ask students to use the spreadsheet they created in Activity 2. or the spreadsheet available to them

5. Bond Valuation Activity

This is to reinforce students’ understanding of bond valuation concepts:

Have students determine the price of the bonds at January 1, 2016, under each of the following

independent assumptions, one at a time. Have students volunteer solutions out loud. After each

response, ask the class why the chosen number of periods and discount rate were used and why the

price is more or less than $200 million.

Bond offerings:

On January 1, 2016, Ross-Finn Fabrication issued $200 million of 12% bonds, dated January 1.

(a) The bonds mature in 2036 (20 years). The market yield for bonds of similar risk and maturity

Calculations:

(a)

Interest $24,000,000 ¥ x 6.62313 * = $158,955,120

(b)

Interest $12,000,000 ¥ x 13.33171 * = $159,980,520

(c)

Interest $12,000,000 ¥ x 16.04612 * = $192,553,440

(d)

Interest $12,000,000 ¥ x 17.44985 * = $209,398,200

(e)

Interest $12,000,000 ¥ x 16.16143 * = $193,937,160

6. Professional Skills Development Activities

The following are suggested assignments from the end-of-chapter material that will help your

students develop their communication, research, analysis, and judgment skills.

Communication Skills. In addition to Communication Cases 14-1, 14-3 and 14-7, Judgment Case

14-5 can be adapted to ask students to write a memo to Mr. Wilde, and Judgment Case 14-6

can be adapted to ask students to write a memo to Jaecke’s chief accountant defending their

positions. Judgment Case 14-5 is suitable for student presentation(s). Communication Case

14-3 requires group interaction. In addition, Ethics Case 14-8 and Judgment Case 14-9 do well

as group assignments. Questions 14-11 and 14-20 and Exercise 14-22 create good class

discussions.

Research Skills. In their careers, our graduates will be required to locate and extract relevant

information from available resource material to determine the correct accounting practice,

perhaps identifying the appropriate authoritative literature to support a decision. Real World

Case 14-2 and Research Case 14-10 provide an excellent opportunity to help students develop

this skill.

Here’s another research activity that may add to your students’ research skills:

Very frequently, the Wall Street Journal lists new security issues in a boxed section

toward the end of the “Money and Investing” section by the “NEW SECURITY ISSUES”

that includes corporate debt issues and stock issues. Ask students to locate that section

of a recent issue of the Journal and list the corporate debt issues described. For each, ask

them to determine:

1. Whether it is secured or unsecured

2. The face amount and the issue price

3. The stated rate and yield

5. Whether it is callable

Analysis Skills. The “Broaden Your Perspective” section includes Analysis Cases that direct

students to gather, assemble, organize, process, or interpret date to provide options for making

business and investment decisions. In addition to Analysis Cases 14-4 and 14-11, Exercise 14–

6, Problems 14-2 and 14-4, and Real World Case 14-2 also provide opportunities to develop

analysis skills.

Judgment Skills. The “Broaden Your Perspective” section includes Judgment Cases that require

14-44 Intermediate Accounting, 8/e

Assignment Chart

Learning Est. time

Questions Objective(s) Topic (min.)

14-1

1

Periodic interest

5

14-2

1

Reporting long-term liabilities on a balance

sheet

5

14-3

1

How are bonds and notes the same?

5

14-4

2

Bond indenture

5

14-5

2

Bond pricing

5

14-6

2

Bond pricing

5

14-7

2

Zero-coupon bond

5

14-8

2

Bonds issued at a premium

5

14-9

2

Methods of determining interest on bonds

5

14-10

2

Debt issue costs

5

14-11

3

When a note’s stated rate of interest is

unrealistic relative to the “market rate”

5

14-12

3

Notes

5

14-13

4

Disclosures

5

14-14

5

Early extinguishment of debt

5

14-15

5

Early extinguishment of debt

5

14-16

5

Convertible bonds and bonds issued with

detachable warrants

5

14-17

5

Voluntary conversion

5

14-18

5, 7

IFRS; convertible bonds

5

14-19

6

Fair value option

5

14-20

A

Pricing bonds at price plus accrued interest

5

14-21

B

Troubled debt restructuring

5

14-22

B

Troubled debt restructuring

5

14-23

B

Troubled debt restructuring

5

Brief Learning Est. time

Exercises Objective(s) Topic (min.)

14-1

1

Bond interest

5

14-2

2

Determining the price of bonds

5

14-3

2

Determining the price of bonds

5

14-4

2

Determining the price of bonds

5

14-5

2

Effective interest on bonds

5

14-6

2

Effective interest on bonds

5

14-7

2

Straight-line interest on bonds

5

14-8

2

Investment in bonds

5

14-9

3

Note with unrealistic interest rate

5

14-10

3

Installment note

5

14-11

5

Early extinguishment

5

14-12

5

Bonds with detachable warrants

5

14-13

5

Convertible bonds

5

14-14

6

Reporting bonds at fair value

5

14-46 Intermediate Accounting, 8/e

Learning Est. time

Exercises Objective(s) Topic (min.)

14-1

2

Bond valuation

25

14-2

2

Determining the price of bonds

35

14-3

2

Determine the price of bonds; issuance;

effective interest

15

14-4

2

Investor; effective interest

15

14-5

2

Determine the price of bonds; issuance;

effective interest; financial statement effects

15

14-6

2

Determine the price of bonds; issuance;

effective interest

15

14-7

2

Determine the price of bonds; issuance;

straight-line method

15

14-8

2

Investor; straight-line method

15

14-9

2

Issuance of bonds; effective interest; amort-

ization schedule; financial statement effects

15

14-10

2

Issuance of bonds; effective interest;

amortization schedule

25

14-11

2

Bonds; effective interest; adjusting entry

15

14-12

2

Bonds; straight line method; adjusting entry

15

14-13

2

Issuance of bonds; effective interest

15

14-14

2

New debt issues; offerings announcements

15

14-15

2

Error correction; accrued interest on bonds

15

14-16

3

Error in amortization schedule

20

14-17

3

Note with unrealistic interest rate

25

14-18

3

Installment note

20

14-19

3

Installment note

20

14-20

2, 3, 4

FASB codification research

25

14-21

5

Early extinguishment

10

14-22

5

Convertible bonds

20

14-23

5

IFRS; convertible bonds

10

14-24

5

Convertible bonds; induced conversion

20

14-25

5, 7

IFRS; convertible bonds

20

14-26

5

Bonds with detachable warrants

20

14-27

6

Reporting bonds at fair value

20

14-28

6

Reporting bonds at fair value

25

14-29

6

Reporting bonds at fair value

30

14-30

A

Accrued interest

5

14-31

B

Troubled debt restructuring; debt settled

10

14-32

B

Troubled debt restructuring; modification of

terms

15

14-33

B

Troubled debt restructuring; modification of

terms; unknown effective rate

20

14-34

B

FASB codification research; legal fees in a

troubled debt restructuring

20

CPA/CMA Learning Est. time

Exam Questions Objective(s) Topic (min.)

CPA-1

1

Bond pricing

3

CPA-2

2

Bond interest

3

CPA-3

2

Bond interest

3

CPA-4

2

Bond interest

3

CPA-5

2

Bond interest

3

CPA-6

2

Bond interest

3

CPA-7

5

Bond redemption

3

CPA-8

5

Bond conversion

3

CPA-9

5

Bond redemption

3

CPA-10

5

Bonds with warrants

3

CPA-11

5

IFRS

3

CPA-12

5

IFRS

3

CMA-1

1

Bond pricing

3

CMA-2

2

Bond interest

3

CMA-3

4

Bond reporting

3

14-48 Intermediate Accounting, 8/e

Learning Est. time

Problems Objective(s) Topic (min.)

14-1

2

Determining the price of bonds – discount and

premium – issuer and investor

20

14-2

2

Accrued interest; effective interest; financial

statement effects

30

14-3

2

Straight-line and effective interest compared

30

14-4

2

Bond amortization schedule

20

14-5

2

Issuer and investor; effective interest;

amortization schedule; adjusting entries

50

14-6

2, A

Issuer and investor; straight-line method;

adjusting entries

50

14-7

2

Issuer and investor; effective interest; no

amortization schedule

25

14-8

2

Bonds; effective interest; partial period interest;

financial statement effects

60

14-9

2

Zero-coupon bonds

20

14-10

3

Notes exchanged for assets

25

14-11

3

Note with unrealistic interest rate

15

14-12

3

Noninterest-bearing installment note

20

14-13

3

Note and installment note with unrealistic interest

rate

25

14-14

5

Early extinguishment of debt

15

14-15

5

Early extinguishment; effective interest

15

14-16

2, 5

Debt issue costs; issuance; expensing; early

extinguishment

20

14-17

5

IFRS; transaction costs

15

14-18

5

Early extinguishment

15

14-19

5

Convertible bonds; induced conversion; bonds

with detachable warrants

35

14-20

5

Convertible bonds; zero coupon; potentially

convertible into cash; FASB codification research;

Microsoft

45

14-21

1, 2, 3, 4, 5

Concepts; terminology

20

14-22

6

Determine bond price; record interest; reporting

bonds at fair value

60

14-23

6

Reporting bonds at fair value; quarterly reporting

60

14-24

2, A

Investments in bonds; accrued interest; sale

60

14-25

2, A

Accrued interest; effective interest; financial

statement effects

60

14-26

B

Troubled debt restructuring

30

Star Problems

Learning Est. time

Cases Objective(s) Topic (min.)

Communication Case 14-1

5

Convertible securities and warrants; concepts

45

Real World Case 14-2

2

Zero-coupon debt; Hewlett-Packard Company

35

Communication Case 14-3

5

Is convertible debt a liability or is it

shareholders’ equity?

30

Analysis Case 14-4

2

Issuance of notes

20

Judgment Case 14-5

3

Noninterest bearing debt

15

Judgment Case 14-6

3

Noninterest bearing note exchanged for cash and

other privileges

15

Communication 14-7

3

Note receivable exchanged for cash and other

services

25

Ethics Case14-8

5

Debt for equity swaps; have your cake and eat it

too

20

Judgment Case 14-9

1, 4

Analyzing financial statements; financial

leverage; interest coverage

25

Research Case 14-10

1 – 4

Researching the way long-term debt is reported;

retrieving information from the Internet: Macy’s

45

Analysis Case 14-11

5

Bonds; conversion; extinguishment

30

Analysis Case 14-12

5

Analyzing financial statements; debt-to-equity;

interest coverage; PetSmart

30

Air France/KLM Case

7

IFRS; accounting for bonds and long-term

notes; Air France

30

CPA Simulation 14-1 Early extinguishment