Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 019 Share-Based Compensation and Earnings per Share

175. The tax code differentiates between qualified and nonqualified incentive plans. What are the major

differences in tax treatment between the two?

176. Blair Systems offers its employees a variety of share-based compensation plans including stock

options, stock appreciation rights, and restricted stock. The following is an excerpt from a disclosure

note from Blair's 2016 financial statements:

Note 11 Employee Benefit Plans (in part)

The Company adopted SFAS 123(R) [ASC Topic 718], which requires the measurement and

recognition of compensation expense for all share-based payment awards made to the

Company’s employees and directors including employee stock options and employee stock

purchase rights, based on estimated fair values. Employee share-based compensation expense

under SFAS 124 (R) was as follows (in millions):

Years Ended

2016

2015

2014

Total employee share-based compensation expense

$455

$870

$760

Required:

1. Blair's share-based compensation includes stock options, stock appreciation rights, and restricted

stock awards. What is the general financial reporting objective when recording compensation

expense for these forms of compensation?

2. Blair reported share-based expense of $455 million in 2016. Without referring to specific numbers

and ignoring other forms of share-based compensation, describe how this amount reflects the value

of stock options.

Answer:

177. Reacting to opposition to the FASB's "Share-Based Payment" Exposure Draft, Senator Carl Levin

stated, "Stock options are the 800-pound gorilla that has yet to be caged by corporate reform." In

reference to a bill that would thwart the FASB's position, Senator John McCain said, "This legislation

blocking stock option expensing not only undermines FASB's independence, but undermines the effort

to restore confidence in our financial markets as well." Discuss what these two senators meant by their

statements.

Chapter 019 Share-Based Compensation and Earnings per Share

178. Stock option plans give employees the option to purchase (a) a specified number of shares of the

firm's stock, (b) at a specified price, (c) during a specified period of time. One of the most heated

controversies in standard-setting history has been the debate over the amount of compensation to be

recognized as expense for stock options. At issue is how the value of stock options is measured, which

for most options determines whether any expense at all is recognized. The opposition included

corporate executives, auditors, members of Congress, and the SEC.

Required:

Describe the primary objections of critics of the FASB's eventually successful attempt to require

expensing of the fair value of the options.

179. Pastner Brands is a calendar-year firm with operations in several countries. As part of its

executive compensation plan, at January 1, 2016, the company had issued 20 million executive stock

options permitting executives to buy 20 million shares of stock for $25. The vesting schedule is 20%

the first year, 30% the second year, and 50% the third year (graded-vesting). The fair value of the

options is estimated as follows:

Vesting Amount Fair Value

Date Vesting per Option

Dec. 31, 2016 20% $3.50

Dec. 31, 2017 30% $4.00

Chapter 019 Share-Based Compensation and Earnings per Share

Dec. 31, 2018 50% $6.00

Required:

1. Determine the compensation expense related to the options to be recorded each year for 2016–2018,

assuming Pastner accounts for each vesting date as a separate award.

2. Determine the compensation expense related to the options to be recorded each year for 2016–2018,

assuming Pastner uses the straight-line method over the three-year vesting period.

Answer:

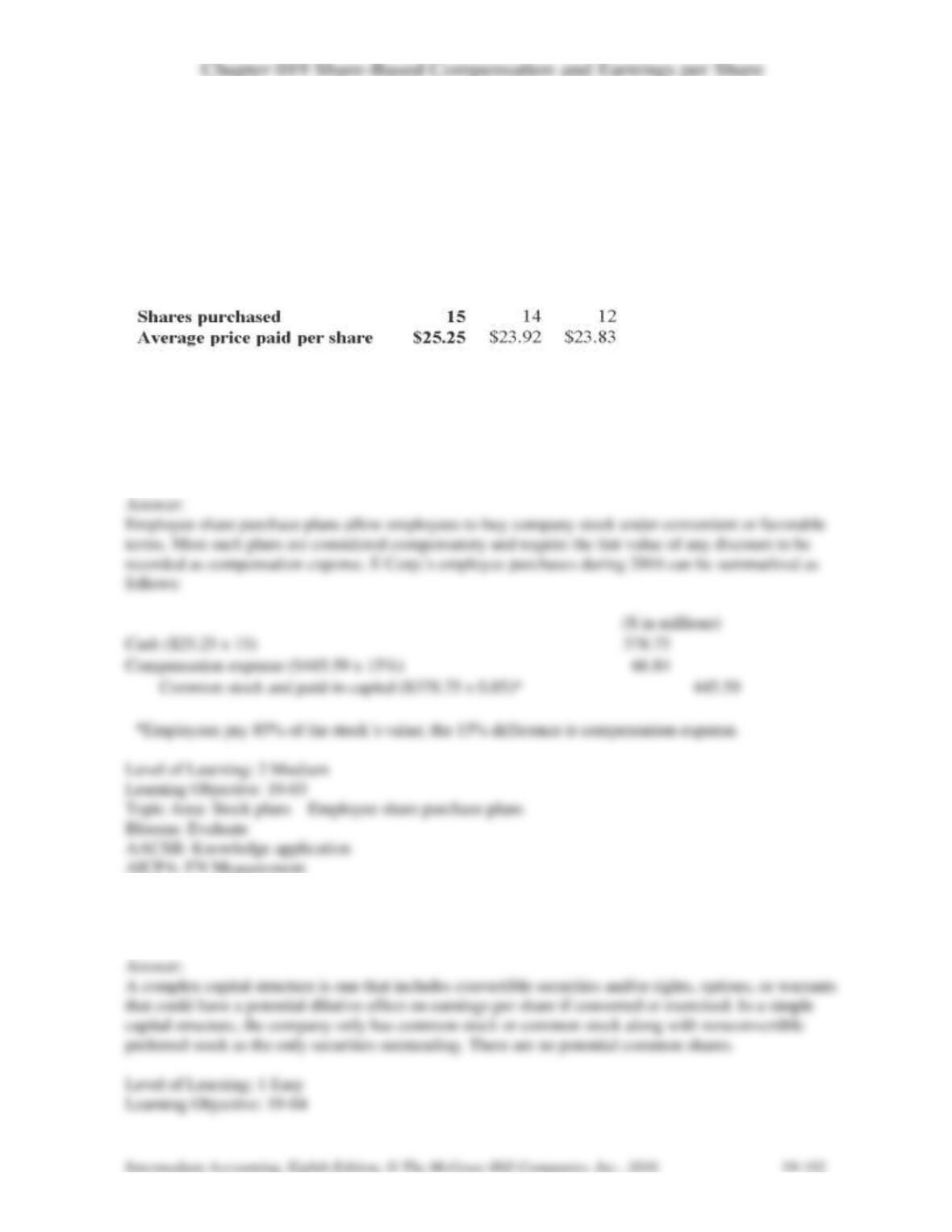

180. A disclosure note from E Corp.'s 2016 annual report is shown below:

Employee Stock Purchase Plan. We have an employee stock purchase plan for all eligible employees.

Compensation expense for the employee stock purchase plan is recognized in accordance with GAAP.

Shares of our common stock may be purchased by employees at three-month intervals at 85% of the

fair value on the last day of each three-month period. Employees may purchase shares having a value

not exceeding 10% of their gross compensation during an offering period. Employees purchased the

following shares:

2016 2015 2014

At June 30, 2016, 150 million shares were reserved for future issuance.

Required:

Describe the way "Compensation expense for the employee stock purchase plan” is recognized in

accordance with GAAP by E Corp. Include in your explanation the journal entry that summarizes

employee share purchases during 2016.

181. How is a complex capital structure different from a simple capital structure?

182. What is the treasury stock method of accounting for stock options, warrants, and rights?

Use the following to answer questions 183 and 184:

In its 2016 Annual Report to shareholders, V Co. had the following disclosure note about its EPS:

NOTE 9 – EARNINGS PER SHARE:

The following represents the reconciliation from basic earnings per share to diluted earnings per share.

Options to purchase 8.3 million and 9.7 million shares of common stock were outstanding at May 31,

2016 and May 31, 2015, respectively, but were not included in the computation of diluted earnings per

share because the options' exercise prices were greater than the average market price of the common

shares and, therefore, the effect would be antidilutive. No such antidilutive options were outstanding at

May 31, 2014.

Year ended May 31,

2016 2015 2014

183. How are outstanding stock options and awards taken into account in computing diluted EPS for V

Co.?

184. At the end of 2016, what is the maximum number of shares that could possibly be issued if all

stock options and awards are exercised? Explain why V Co. used only 3.3 million in its computation for

2016.

185. Why are earnings per share figures for prior years adjusted for stock splits and stock dividends

when data from prior years is presented in comparative financial statements?

Chapter 019 Share-Based Compensation and Earnings per Share

186. Why are preferred dividends deducted from net income when calculating EPS?

187. The D Company develops, manufactures, distributes, and markets branded health care products as

well as private-label vitamin products in the United States and more than 50 other countries. A

disclosure note from D's 2014 annual report is shown below:

Weighted Average Shares Outstanding

The following table provides information about basic and diluted weighted average shares

outstanding:

(shares in thousands)

2016

2015

2014

Basic weighted average shares outstanding

5,896

2,426

1,451

Effect of dilutive securities

Assumed exercise of stock options

443

110

252

Assumed vesting of restricted stock

37

99

77

Diluted weighted average shares outstanding

6,376

2,635

1,780

The computations of diluted weighted average shares outstanding exclude 4 million shares in

fiscal year 2016, 2 million shares in fiscal year 2015 and 1 million shares in fiscal year 2014 since the

options were antidilutive.

Required:

1. The disclosure note shows adjustments for "assumed exercise of stock options and assumed vesting

of restricted stock." What other adjustments might be needed? Explain why and how these

adjustments are made to the weighted-average shares outstanding.

2. The disclosure note indicates that the effect of some of the stock options were not included because

they would be antidilutive. What does that mean? Why not include antidilutive securities?

Chapter 019 Share-Based Compensation and Earnings per Share

Chapter 019 Share-Based Compensation and Earnings per Share

188. What is meant by dilution of earnings per share?

189. What is the "if converted method"?

190. What is an antidilutive security?

191. M, Inc., supplies consumer products used in the United States and other markets. In its 2016

Annual Report to Shareholders, M, Inc., disclosed the following note about its EPS:

Basic earnings per share are computed using the weighted average number of common shares

outstanding during the period. Diluted earnings per common share incorporate the incremental

shares issuable upon the assumed exercise of stock options and upon the assumed conversion of

the Company's Convertible Notes in fiscal 2016 as if conversion to common shares had

occurred at the beginning of the fiscal year. Earnings have also been adjusted for interest

expense on the Convertible Notes in fiscal 2016.

Explain why M mentioned the adjustment in the last sentence of the disclosure note.

Chapter 019 Share-Based Compensation and Earnings per Share

192. Zeba Company granted 27 million of its no par common shares to executives, subject to forfeiture

if employment is terminated within three years. Zeba’s common shares have a market price of $10 per

share on January 1, 2015, the grant date.

Required:

When calculating diluted EPS at December 31, 2016, what will be the net increase in the denominator

of the EPS fraction if the market price of the common shares averaged $10 during 2016?

193. Salle Services issued $300 million of 6% bonds in 2014. The bonds are convertible into 60 million

shares of its no par common stock. Salle elected the option to report the bonds at fair value, with

changes in fair value reported in earnings. As a result the bonds are reported at $312 million in the

December 31, 2016, balance sheet.

Required:

When calculating diluted EPS at December 31, 2016, what will be the net increase in the denominator

of the EPS fraction? Explain.

Answer:

194. If executive stock options or restricted stock are outstanding when calculating diluted EPS, what

are the components of the “proceeds” assumed available for the repurchase of shares under the treasury

stock method?

195. When the income statement includes discontinued operations, which amounts require per share

presentation?

196. Compare the concepts of basic and diluted earnings per share with respect to their calculation.

Chapter 019 Share-Based Compensation and Earnings per Share

197. What is the advantage of stock appreciation rights over stock options?

198. Pastner Brands is a calendar-year firm with operations in several countries. As part of its

executive compensation plan, at January 1, 2016, the company had issued 20 million executive stock

options permitting executives to buy 20 million shares of stock for $25. The vesting schedule is 20%

the first year, 30% the second year, and 50% the third year (graded-vesting). The fair value of the

options is estimated as follows:

Vesting Amount Fair Value

Date Vesting per Option

Dec. 31, 2016 20% $3.50

Dec. 31, 2017 30% $4.00

Dec. 31, 2018 50% $6.00

Required:

Determine the compensation expense related to the options to be recorded each year for 2016–2018,

assuming Pastner prepares its financial statements in accordance with International Financial Reporting

Standards (IFRS).

Answer:

Chapter 019 Share-Based Compensation and Earnings per Share