RETAINED EARNINGS

The stock dividend caused a $13 million reduction of retained

earnings.

Net income increased retained earnings by $12 million.

T21–30

21-42 Intermediate Accounting, 8/e

COMPLETING THE SPREADSHEET

The spreadsheet now shows that net cash flows from

operating, investing, and financing activities are: $22 million;

($19 million); and $6 million, respectively. Together these

activities provide a net increase in cash of $9 million.

($ in millions)

Entry (19) Cash ……………………………………………… 9

Net increase in cash

[from statement of cash flows activities] ……… 9

As a final check of accuracy, we can confirm that the total

of the debits is equal to the total of the credits in the

United Brands Corporation

Spreadsheet for the Statement of Cash Flows

Dec. 31 Changes Dec. 31

2015 Debits Credits 2016

Balance Sheet

Assets:

Cash 20 (19) 9 29

Liabilities:

Accounts payable 20 (4) 6 26

Salaries payable 1 (5) 2 3

Shareholders’ Equity:

Common stock 100 (16) 10

(17) 20 130

T21–32

21-44 Intermediate Accounting, 8/e

(continued)

Dec. 31 Changes Dec. 31

2015 Debits Credits 2016

Income Statement

Revenues:

Sales revenue (1) 100 100

Investment revenue (2) 3 3

T21–32 (continued)

Dec. 31 Changes Dec. 31

2015 Debits Credits 2016

Statement of Cash Flows

Operating activities:

Cash inflows:

From customers (1) 98

From investment revenue (2) 3

Net cash flows 22

Investing activities:

Sale of land (3) 18

Net cash flows (19)

Financing activities:

T21–32 (continued)

21-46 Intermediate Accounting, 8/e

INDIRECT METHOD

By the indirect method, the net cash increase or decrease

Cash Flows from Operating Activities – Indirect Method

and

Reconciliation of Net Income to

Net Cash Flows from Operating Activities

Net income $12

Adjustments for noncash effects:

COMPARISON OF DIRECT AND

INDIRECT METHODS

Cash Flows from Operating Activities

INCOME STATEMENT INDIRECT METHOD DIRECT METHOD

Net income $12

Adjustments :

Sales $100 Increase in A/R (2) Cash from customers $98

Investment rev. 3 [No adjustment – no

T21–34

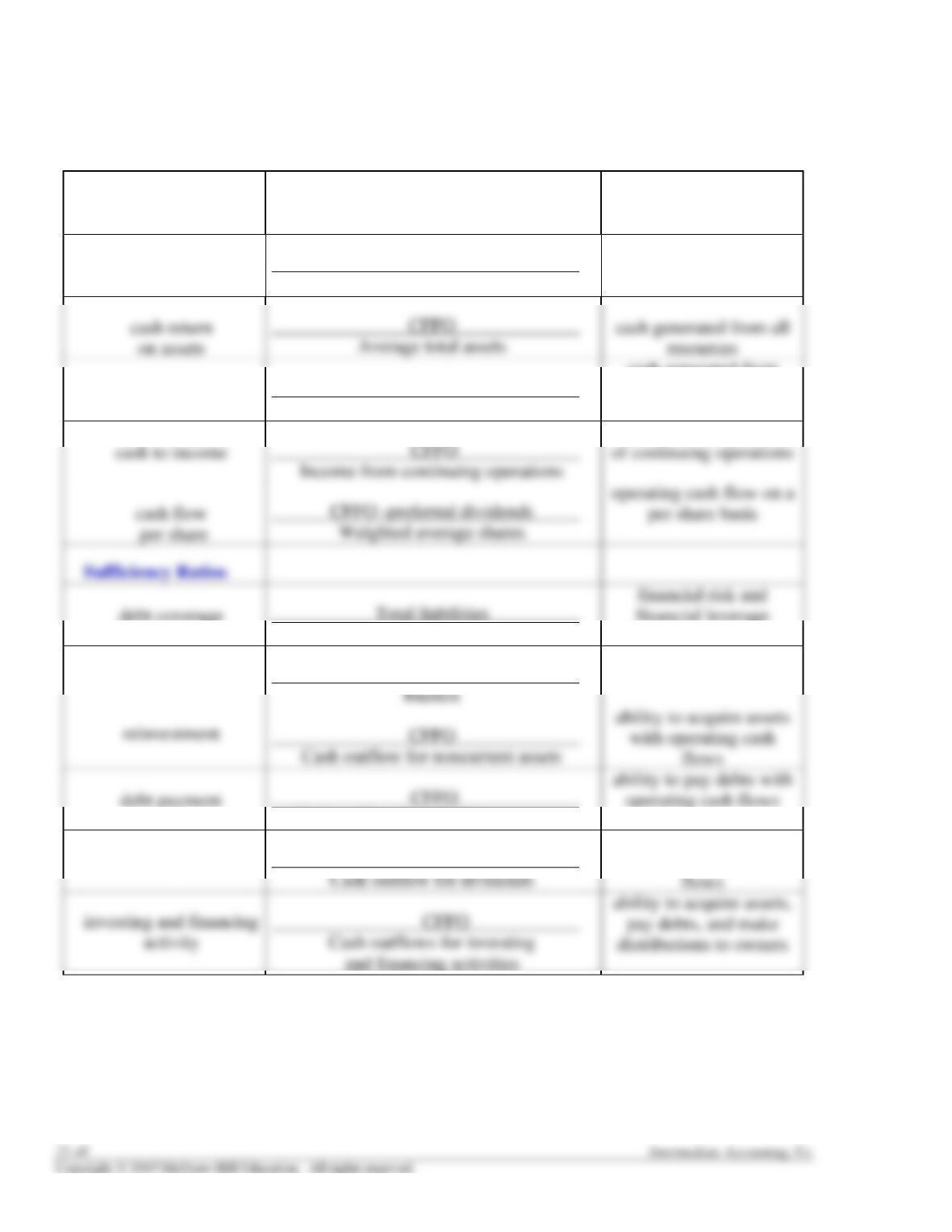

CASH FLOW RATIOS

RATIO

CALCULATION

MEASURES:

Performance Ratios

cash flow to sales

CFFO

Net sales

cash generated by each

sales dollar

CFFO

cash return on

shareholders’ equity

CFFO

Average shareholders’ equity

cash generated from

owner-provided

resources

CFFO

CFFO -preferred dividends

Total liabilities

cash-generating ability

debt coverage

CFFO

financial leverage

interest coverage

CFFO

CFFO

CFFO+interest+taxes

ability to satisfy its fixed

obligations

Cash outflow for LT debt repayment

dividend payment

CFFO

ability to pay dividends

with operating cash

T21–35

S

Su

ug

gg

ge

es

st

ti

io

on

ns

s

f

fo

or

r

C

Cl

la

as

ss

s

A

Ac

ct

ti

iv

vi

it

ti

ie

es

s

1. Critical Thought Activity

Students often are lulled into believing that there is only one “right” way to report a transaction.

Accounting for cash flows provides and opportunity to consider supportable alternatives.

Suggestions:

Ask your students to consider the appropriate way to report cash payments for dividends in a

statement of cash flows.

Next, ask them to consider the appropriate way to report cash dividends received in a statement of

cash flows.

21-50 Intermediate Accounting, 8/e

2. Real World Scenario

Students learn in the text that footnote disclosure provides useful information related to the

statement of cash flows, often in the form of non-cash information. The following disclosure from

HP offers a fairly complete example of that type of disclosure.

HEWLETT PACKARD COMPANY

CONSOLIDATED STATEMENT OF CASH FLOWS (in part)

Note 5: Supplemental Cash Flow Information

Supplemental cash flow information to the Consolidated Statements of Cash Flows was as follows for the following

fiscal years ended October 31:

In millions

Cash paid for income taxes, net

$

1,293

$

643

$

1,136

Cash paid for interest

$

384

$

572

$

426

Non-cash investing and financing activities:

Issuance of common stock and stock awards assumed in business acquisitions

$

$

$

316

Purchase of assets under financing arrangements

$

$

283

$

Acquisition of asset use under lease agreements

$

122

$

131

$

Suggestions:

Have your students find this information on the Internet or provide it to them. Would the

information about cash for interest and taxes be needed if HP reported operating activities by the

direct method?

You might ask them to reconstruct the journal entries for the acquisitions and sales reported. Why

is this information reported?

Points to note:

If HP reported operating activities by the direct method, the information about cash for interest

3. Spreadsheet Activity

Have students create a functional spreadsheet in Excel or some other spreadsheet program capable of

being used to help prepare a statement of cash flows. Suggest that the spreadsheet:

2. Automatically and continually verify that total debits equal total credits.

4. Professional Skills Development Activities

The following are suggested assignments from the end-of-chapter material that will help your

students develop their communication, research, analysis, and judgment skills.

Communication Skills. In addition to Communication Case 21-1, Judgment Case 21-2 can be

adapted to ask students to prepare a report outlining the findings of the research for

presentation at the meeting. Judgment Case 21-2, Real World Case 21-8, and Analysis Cases

Research Skills. In their professional lives, our graduates will be required to locate and extract

relevant information from available resource material to determine the correct accounting

practice, perhaps identifying the appropriate authoritative literature to support a decision.

Research Cases 21-3, 21-9, and 21-11 provide opportunities to develop research skills.

21-52 Intermediate Accounting, 8/e

5. Ethical Dilemma

The chapter includes the following ethical dilemma.

ETHICAL DILEMMA

“We must get it,” Courtney Lowell, president of Industrial Fasteners, roared. “Without it

we’re in big trouble.” The “it” Mr. Lowell referred to is the renewal of a $14 million loan with

Community First Bank. The “big trouble” he fears is the lack of funds necessary to repay the

existing debt and few, if any, prospects for raising the funds elsewhere.

Mr. Lowell had just hung up the phone after a conversation with a bank vice-president in

which it was made clear that this year‘s statement of cash flows must look better than last year‘s.

Mr. Lowell knows that improvements are not on course to happen. In fact, cash flow projections

were dismal.

Later that day, Tim Cratchet, assistant controller, was summoned to Mr. Lowell’s office.

“Cratchet,” Lowell barked, “I’ve looked at our accounts receivable. I think we can generate quite

a bit of cash by selling or factoring most of those receivables. I know it will cost us more than if

we collect them ourselves, but it sure will make our cash flow picture look better.”

Is there an ethical question facing Cratchet?

You may wish to discuss this in class. If so, discussion should include these elements.

Step 1 – The Facts:

Industrial Fasteners needs the renewal of a $14 million loan with Community First Bank.

Prospects for currently repaying the debt are poor. The bank has required an improved statement of

Step 2 – The Ethical Issue and the Stakeholders:

The ethical issue or dilemma is whether the assistant controller’s obligation to the president and

the company is greater than an obligation to appropriately advise the president in making a sound

Step 4 – Alternatives:

2. Refuse to factor the accounts receivable.

4. Resign from the company and seek employment elsewhere.

Step 5 – Evaluation of Alternatives in Terms of Values:

2. Alternative 2 exhibits the values of competence, honesty, integrity, objectivity, and

responsibility to users of the financial statements.

3. Alternative 3 also illustrates loyalty to the employer at a level higher than that of the

4. Alternative 4 supports the values of honesty and integrity, but does not reflect competence,

objectivity, or responsibility to financial statement users.

Step 6 – Consequences:

Alternative 1

Positive consequences: The assistant controller keeps the job and pleases the president. The

company will obtain the renewal and may avoid loan payment default and possible bankruptcy.

Alternative 2

Positive consequences: The bank receives a cash flow statement that is more relevant and

Alternative 3

Positive consequences: The assistant controller would maintain integrity. The bank receives

a more relevant and reliable reflection of the company’s operating cash position if the board of

21-54 Intermediate Accounting, 8/e

Alternative 4

Positive consequences: The assistant controller maintains integrity and avoids conflict with

A

As

ss

si

ig

gn

nm

me

en

nt

t

C

Ch

ha

ar

rt

t

Learning Est. time

Questions Objective(s) Topic (min.)

21-1

1, 2

Need for financial statement that reports cash

flows

5

21-2

3

Evolution of statement of cash flows

5

21-3

4

Cash equivalent

5

21-4

4

Cash equivalent

5

21-5

5

Cash flows from operating activities

5

21-6

5

Cash flows from operating activities

5

21-7

5

Cash flows from investing activities

5

21-8

5

Cash flows from financing activities

5

21-9

6

Noncash investing and financing activities

5

21-10

6

Transaction partly in cash

5

21-11

7

Most noteworthy item on a statement of cash

flows

5

21-12

7

Spreadsheet

5

21-13

7

Cash received from customers

5

21-14

7

When an asset is sold at a gain

5

21-15

7

Ordinary losses and extraordinary losses

5

21-16

7

Increase in the deferred income tax liability

5

21-17

8

Indirect method

5

21-18

8

Direct method

5

21-19

8

Indirect method

5

21-20

8

Indirect method

5

21-21

9

IFRS

5

21-22

9

IFRS

5

Brief Learning Est. time

Exercises Objective(s) Topic (min.)

21-1

3

Determine cash received from customers

5

21-2

3

Determine cash received from customers

5

21-3

3

Determine cash paid to suppliers

5

21-4

3

Determine cash paid to employees

5

21-5

3, 6

Bond interest and discount

5

21-6

4, 6

Bond interest and discount

5

21-7

3, 6

Installment note

5

21-8

3, 4, 5

Sale of land

5

21-9

5

Investing activities

5

21-10

6

Financing activities

5

21-11

4

Indirect method

5

21-12

4

Indirect method

5

21-56 Intermediate Accounting, 8/e

Learning Est. time

Exercises Objective(s) Topic (min.)

21-1

3-6

Classification of cash flows

20

21-2

3, 8

Determine cash paid to suppliers of merchandise

15

21-3

3

Determine cash received from customers

20

21-4

3

Summary entries for cash received from

customers

20

21-5

3

Determine cash paid to suppliers of merchandise

25

21-6

3

Summary entries for cash paid to suppliers of

merchandise

25

21-7

3

Determine cash paid for bond interest

20

21-8

3

Determine cash paid for bond interest

20

21-9

3

Determine cash paid for income taxes

25

21-10

3

Summary entries for cash paid for income taxes

25

21-11

3

Bonds; statement of cash flows effects

20

21-12

3, 6

Installment note; statement of cash flows effects

20

21-13

5, 6

Identifying cash flows from investing activities

and financing activities

20

21-14

5, 6

Identifying cash flows from investing activities

and financing activities

20

21-15

3, 5, 6

Lease; statement of cash flows effects

20

21-16

3, 5

Equity method investment; statement of cash

flows effects

20

21-17

4

Indirect method; reconciliation of net income to

net cash flows from operating activities

15

21-18

3 – 8

Summary entries from statement of retained

earnings

20

21-19

3, 4

Relationship among the income statement, cash

flows from operating activities (direct method),

and cash flows from operating activities

(indirect method)

30

21-20

3, 4

Reconciliation of net cash flows from operating

activities to net income

30

21-21

3, 4

Cash flows from operating activities (direct

method) derived from an income statement and

cash flows from operating activities (indirect

method)

30

21-22

4

Indirect method; reconciliation of net income to

net cash flows from operating

15

21-23

3

Cash flows from operating activities (direct

method) – includes loss on sale of cash

equivalents and extraordinary loss

30

21-24

4

Cash flows from operating activities (indirect

method) includes loss on sale of cash

equivalents and extraordinary loss

20

21-25

3

Cash flows from operating activities (direct

method) – includes loss on sale of cash

equivalents and extraordinary gain

30

21-26

4

Cash flows from operating activities (indirect

method) – includes loss on sale of cash

equivalents and extraordinary gain

20

21-27

3, 5, 6, 8

Statement of cash flows; direct method

60

21-28

3

Pension plan funding

15

21-29

2

FASB codification research

15

21-30

1, 4, 7

FASB codification research

25

21-31

4, 5, 6, 8

Statement of cash flows; indirect method [based

on appendix 21-A]

45

21-32

8

Statement of cash flows; T-account method

[based on appendix 21-B]

50

21-58 Intermediate Accounting, 8/e

CPA/CMA Learning Est. time

Exam Questions Objective(s) Topic (min.)

CPA-1

3

Operating activities

3

CPA-2

6

Financing activities

3

CPA-3

4

Operating activities

3

CPA-4

3

Operating activities

3

CPA-5

5

Investing activities

3

CPA-6

4

Operating activities

3

CPA-7

3

IFRS

3

CPA-8

5

IFRS

3

CPA-9

4

IFRS

3

CMA-1

3

Operating activities

3

CMA-2

5, 6

Investing and financing activities

3

CMA-3

4

Operating activities

3

Learning Est. time

Problems Objective(s) Topic (min.)

21-1

2 , 5-7

Classifications of cash flows from investing

and financing activities

25

21-2

3, 8

Statement of cash flows; direct method

60

21-3

3, 8

Statement of cash flows; direct method

75

21-4

3, 8

Statement of cash flows; direct method

75

21-5

3, 8

Statement of cash flows; direct method

60

21-6

3, 4

Cash flows from operating activities (direct

method) derived from an income statement

and cash flows from operating activities

(indirect method)

35

21-7

3, 4

Cash flows from operating activities (direct

method) derived from an income statement

and cash flows from operating activities

(indirect method)

40

21-8

3, 4

Cash flows from operating activities (direct

method and indirect method) – deferred

income tax liability and amortization of

bond discount

45

21-9

3, 4

Cash flows from operating activities (direct

method) and indirect method) – gain on sale

of cash equivalents and extraordinary loss

45

21-10

3, 4

Relationship among the income statement,

cash flows from operating activities (direct

method), and cash flows from operating

activities (indirect method)

25

21-11

3, 8

Statement of cash flows; direct method

75

21-12

5, 6, 8

Transactions affecting retained earnings

20

21-13

5

Various cash flows

25

21-14

4, 8

Statement of cash flows; indirect method;

limited information

40

21-15

3, 5, 6

Integrating problem; bonds; lease

transactions; lessee and lessor; statement of

cash flow effects

40

21-16

4, 8

Statement of cash flows; indirect method

60

21-17

4, 8

Statement of cash flows; indirect method

45

21-18

4, 8

Statement of cash flows; indirect method

60

21-19

3, 8

Statement of cash flows; T-account method

60

21-20

3, 8

Statement of cash flows; T-account method

45

21-21

3, 8

Statement of cash flows; T-account method

60

Star Problems

21-60 Intermediate Accounting, 8/e

Learning Est. time

Cases Objective(s) Topic (min.)

Communication Case 21-1

1, 3, 4

Distinguish income and cash flows

45

Judgment Case 21-2

3, 8

Distinguish income and cash flows

30

Research Case 21-3

3 – 8

Information from cash flow activities;

codification; FedEx

25

Trueblood Accounting Case

21-4

4

Presenting borrowings and payments under a

revolving line of credit in a statement of cash

flows

40

Analysis Case 21-5

3, 4

Postretirement benefits and accounting for

income taxes

20

Real World Case 21-6

1 – 8

Analyze cash flow activities; Staples

40

Ethics Case 21-7

1, 3

Where’s the cash?

25

Real World Case 21-8

3, 4

Cash flow different from earnings; PetSmart,

Inc.

35

Research Case 21-9

3 – 8

Researching the way cash flows are reported;

retrieving information from the Internet

50

Analysis Case 21-10

3 – 8

Information from cash flow activities; PetSmart,

Inc.

25

Research Case 21-11

4 – 6

FASB codification; locate and extract relevant

information and cite authoritative support for a

financial reporting issue; cash flow classification

25

IFRS Case 21-12

3 – 6, 9

Statement of cash flows presentation, British

Telecommunications

25

Air France/KLM Case

9

IFRS; statement of cash flows; Air

France/KLM

30

CPA Simulation 21-1 Judgment; calculating cash flows; analyzing

accrual transactions; communication;

research