Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

True/False Questions

1. Property, plant, and equipment and intangible assets are long-term, revenue producing assets.

2. Sales tax paid on equipment acquired for use in the business is not capitalized.

3. Demolition costs to remove an old building from land purchased as a site for a new building

are considered part of the cost of the new building.

4. The initial cost of property, plant, and equipment includes all the identifiable expenditures

necessary to bring the asset to its desired condition and location for use.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

5. A distinguishing characteristic of intangible assets is the degree of uncertainty about when or

if they will provide future benefits.

6. Costs incurred after discovery of a natural resource but before production begins are reported

as expenses of the period in which the expenditures are made.

7. The relative fair values are used to determine the valuation of individual assets acquired in a

lump-sum purchase.

8. The fair value of the asset, debt, or equity securities given in a noncash acquisition should

determine the value of the consideration received.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

9. Under current GAAP, fair value is used to measure the components of all nonmonetary

exchanges.

10. The interest capitalization period for a self-constructed asset ends either when the asset is

substantially complete and ready for use or when interest costs no longer are being incurred.

11. The FASB’s required accounting treatment for research and development costs often

understates both net income and assets.

12. According to International Financial Reporting Standards, all research and development

expenditures are expensed in the period incurred.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

13. A company that prepares its financial statements according to International Financial

Reporting Standards must calculate amortization of capitalized software development costs in

the same way as under U.S. GAAP.

14. A company that prepares its financial statements according to International Financial

Reporting Standards accounts for a government grant by recognizing revenue for the amount

of the grant.

15. The successful efforts method of accounting for oil and gas exploration costs allows costs

incurred in searching for oil and gas within a large geographical area to be capitalized.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

Multiple Choice Questions

16. Property, plant, and equipment and intangible assets are:

a. Created by the normal operation of the business and include accounts receivable.

b. All assets except cash and cash equivalents.

c. Current and long-term assets used in the production of either goods or services.

d. Long-term revenue-producing assets.

17. The acquisition costs of property, plant, and equipment do not include:

a. The ordinary and necessary costs to bring the asset to its desired condition and location

for use.

b. The net invoice price.

c. Legal fees, delivery charges, installation, and any applicable sales tax.

d. Maintenance costs during the first 30 days of use.

18. Goodwill is:

a. Amortized over the greater of its estimated life or 40 years.

b. Only recorded by the seller of a business.

c. The excess of the fair value of a business over the fair value of all net identifiable assets.

d. None of these answer choices are correct.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

19. Productive assets that are physically consumed in operations are:

a. Equipment.

b. Land.

c. Land improvements.

d. Natural resources.

20. An exclusive 20-year right to manufacture a product or use a process is a:

a. Patent.

b. Copyright.

c. Trademark.

d. Franchise.

21. The exclusive right to benefit from a creative work, such as a film, is a:

a. Patent.

b. Copyright.

c. Trademark.

d. Franchise.

22. The exclusive right to display a symbol of product identification is a:

a. Patent.

b. Copyright.

c. Trademark.

d. Franchise.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

23. The capitalized cost of equipment excludes:

a. Maintenance.

b. Sales tax.

c. Shipping.

d. Installation.

24. Asset retirement obligations:

a. Increase the balance in the related asset account.

b. Are measured at fair value in the balance sheet.

c. Are liabilities associated with the restoration of a long-term asset.

d. All of these answer choices are correct.

25. If a company incurs disposition obligations as a result of acquiring an asset:

a. The company recognizes the obligation at fair value when the asset is acquired.

b. The company recognizes the obligation at fair value when the asset is disposed.

c. The company records the difference between the fair value of the asset and the obligation

when the asset is acquired.

d. None of these answer choices are correct.

26. When selling property, plant, and equipment for cash:

a. The seller recognizes a gain or loss for the difference between the cash received and the

fair value of the asset sold.

b. The seller recognizes a gain or loss for the difference between the cash received and the

book value of the asset sold.

c. The seller recognizes losses, but not gains.

d. None of these answer choices are correct.

27. Which of the following does not pertain to accounting for asset retirement obligations?

a. They accrete (increase over time) at the company’s credit-adjusted risk-free rate.

b. They must be recognized according to GAAP.

c. Statement of Financial Accounting Concepts No. 7 is applied when adjusting cash flow

obligations for uncertainty.

d. All of these answer choices pertain to accounting for asset retirement obligations.

Use the following to answer questions 28 and 29:

Montana Mining Co. (MMC) paid $200 million for the right to explore and extract rare metals from

land owned by the state of Montana. To obtain the rights, MMC agreed to restore the land to a

suitable condition for other uses after its exploration and extraction activities. MMC incurred

exploration and development costs of $60 million on the project.

MMC has a credit-adjusted risk free interest rate is 7%. It estimates the possible cash flows for

restoring the land, three years after its extraction activities begin, as follows:

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

Cash Outflow

Probability

$10 million

60%

$30 million

40%

28. The asset retirement obligation (rounded) that should be recognized by MMC at the beginning

of the extraction activities is:

a. $ 8.2 million.

b. $14.7 million.

c. $ 18 million.

d. $ 30 million.

29. The asset retirement obligation (rounded) that should be reported on MMC’s balance sheet

one year after the extraction activities begin is:

a. $0.

b. $14.7 million.

c. $15.7 million.

d. $19.3 million.

30. Grab Manufacturing Co. purchased a 10-ton draw press at a cost of $180,000 with terms of

5/15, n/45. Payment was made within the discount period. Shipping costs were $4,600, which

included $200 for insurance in transit. Installation costs totaled $12,000, which included

$4,000 for taking out a section of a wall and rebuilding it because the press was too large for

the doorway. The capitalized cost of the 10-ton draw press is:

a. $171,000.

b. $183,600.

c. $187,600.

d. $185,760.

31. Holiday Laboratories purchased a high-speed industrial centrifuge at a cost of $420,000.

Shipping costs totaled $15,000. Foundation work to house the centrifuge cost $8,000. An

additional water line had to be run to the equipment at a cost of $3,000. Labor and testing

costs totaled $6,000. Materials used up in testing cost $3,000. The capitalized cost is:

a. $455,000.

b. $446,000.

c. $437,000.

d. $435,000.

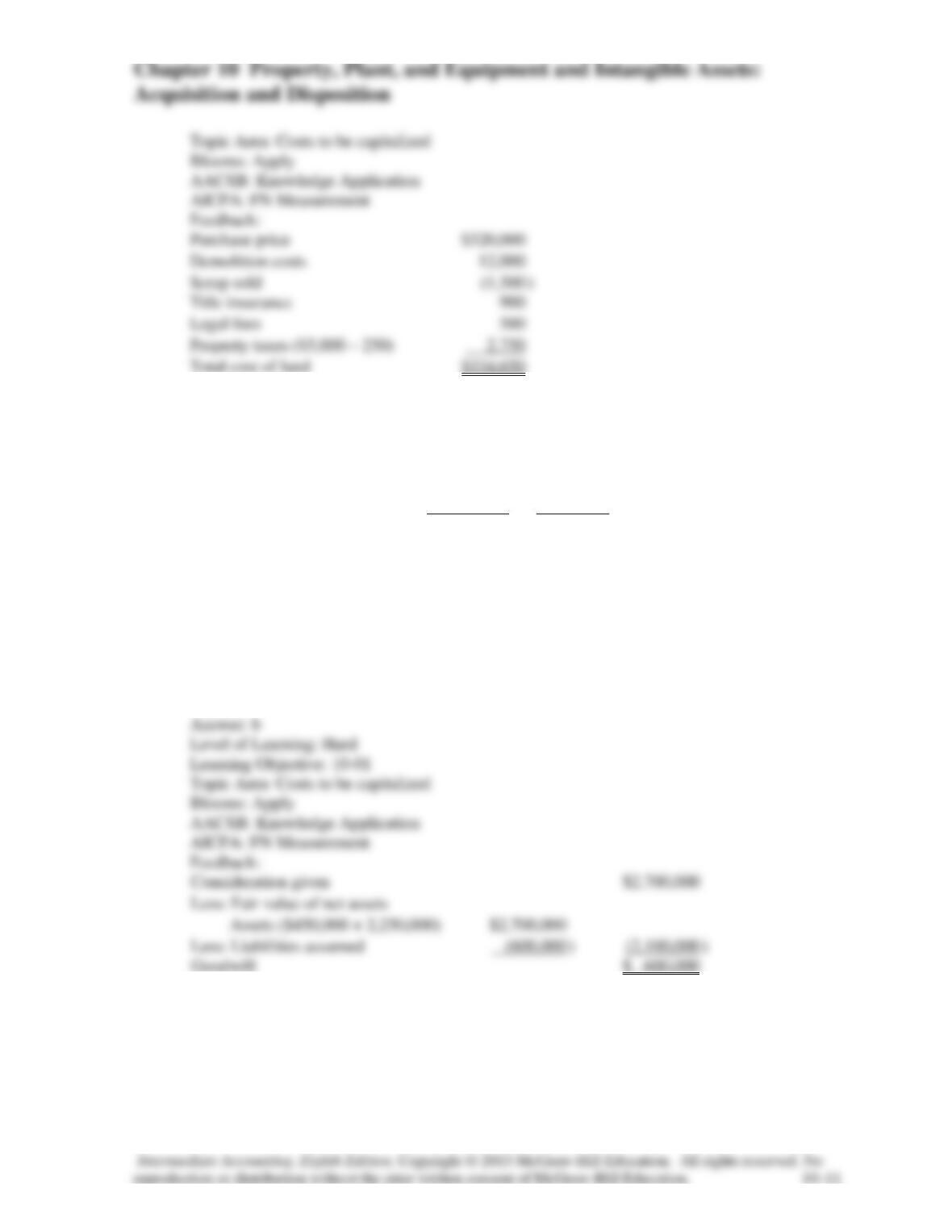

32. Vijay Inc. purchased a three-acre tract of land for a building site for $320,000. On the land

was a building with an appraised value of $120,000. The company demolished the old

building at a cost of $12,000, but was able to sell scrap from the building for $1,500. The cost

of title insurance was $900 and attorney fees for reviewing the contract were $500. Property

taxes paid were $3,000, of which $250 covered the period subsequent to the purchase date.

The capitalized cost of the land is:

a. $336,400.

b. $336,150.

c. $334,650.

d. $201,150.

33. Juliana Corporation purchased all of the outstanding stock of Caldwell Inc., paying

$2,700,000 cash. Juliana assumed all of the liabilities of Caldwell. Book values and fair

values of acquired assets and liabilities were:

Book Value

Fair Value

Current assets (net)

$420,000

$450,000

Property, plant, & equip. (net)

1,600,000

2,250,000

Liabilities

500,000

600,000

Juliana would record goodwill of:

a. $1,180,000.

b. $ 600,000.

c. $ 880,000.

d. $ 100,000.

34. Lake Incorporated purchased all of the outstanding stock of Huron Company paying $950,000

cash. Lake assumed all of the liabilities of Huron. Book values and fair values of acquired

assets and liabilities were:

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

Book Value

Fair Value

Current assets (net)

$130,000

$125,000

Property, plant, equip. (net)

600,000

750,000

Liabilities

150,000

175,000

Lake would record goodwill of:

a. $ 0.

b. $ 75,000.

c. $445,000.

d. $250,000.

35. On July 1, 2016, Larkin Co. purchased a $400,000 tract of land that is intended to be the site

of a new office complex. Larkin incurred additional costs and realized salvage proceeds

during 2016 as follows:

Demolition of existing building on site

$75,000

Legal and other fees to close escrow

12,000

Proceeds from sale of demolition scrap

10,000

What would be the balance in the land account as of December 31, 2016?

a. $400,000.

b. $475,000.

c. $477,000.

d. $487,000.

36. Assets acquired in a lump-sum purchase are valued based on:

a. Their assessed valuation.

b. Their relative fair values.

c. The present value of their future cash flows.

d. Their cost plus the difference between their cost and fair values.

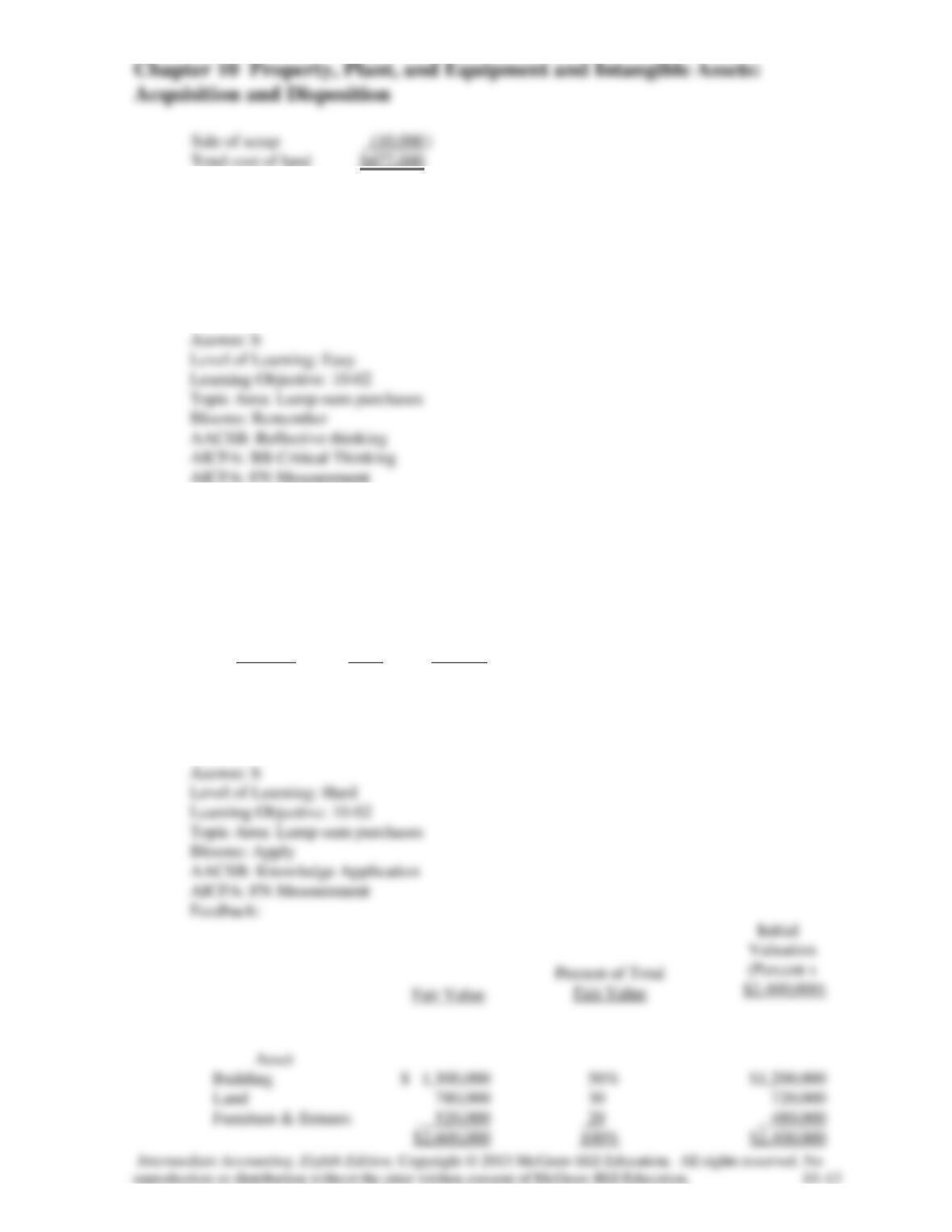

37. Simpson and Homer Corporation acquired an office building on three acres of land for a lump–

sum price of $2,400,000. The building was completely furnished. According to independent

appraisals, the fair values were $1,300,000, $780,000, and $520,000 for the building, land, and

furniture and fixtures, respectively. The initial values of the building, land, and furniture and

fixtures would be:

Building

Land

Fixtures

a. $1,300,000 $ 780,000 $520,000

b. $1,200,000 $ 720,000 $480,000

c. $ 720,000 $1,200,000 $480,000

d. None of these answer choices are correct.

38. Cantor Corporation acquired a manufacturing facility on four acres of land for a lump-sum

price of $8,000,000. The building included used but functional equipment. According to

independent appraisals, the fair values were $4,500,000, $3,000,000, and $2,500,000 for the

building, land, and equipment, respectively. The initial values of the building, land, and

equipment would be:

Building

Land

Equipment

a. $4,500,000 $3,000,000 $2,500,000

b. $4,500,000 $3,000,000 $ 500,000

c. $3,600,000 $2,400,000 $2,000,000

d. None of these answer choices are correct.

39. Assets acquired under multi-year deferred payment contracts are:

a. Valued at their fair value on the date of the final payment.

b. Valued at the present value of the payments required by the contract.

c. Valued at the sum of the payments required by the contract.

d. None of these answer choices are correct.

40. Assets acquired by the issuance of equity securities are valued based on:

a. Their fair values.

b. The fair value of the equity securities.

c. A or B, whichever is more reasonably determinable.

d. A or B, whichever is smaller.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

41. Donated assets are recorded at:

a. Zero (memo entry only).

b. The donor’s book value.

c. The donee’s stated value.

d. Fair value.

42. The fixed-asset turnover ratio provides:

a. The rate of decline in asset lives.

b. The rate of replacement of fixed assets.

c. The amount of sales generated per dollar of fixed assets.

d. The decline in book value of fixed assets compared to capital expenditures.

43. The balance sheets of Davidson Corporation reported net fixed assets of $320,000 at the end

of 2016. The fixed-asset turnover ratio for 2016 was 4.0, and sales for the year totaled

$1,480,000. Net fixed assets at the end of 2015 were:

a. $470,000.

b. $370,000.

c. $420,000.

d. None of these answer choices are correct.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

44. The basic principle used to value an asset acquired in a nonmonetary exchange is to value it at:

a. Fair value of the asset(s) given up.

b. The book value of the asset given plus any cash or other monetary consideration received.

c. Fair value or book value, whichever is smaller.

d. Book value of the asset given.

45. In a nonmonetary exchange of equipment, if the exchange has commercial substance, a gain is

recognized if:

a. The fair value of the equipment received exceeds the book value of the equipment

received.

b. The book value of the equipment received exceeds the fair value of the equipment given

up.

c. The fair value of the equipment surrendered exceeds the book value of the equipment

given up.

d. None of these answer choices are correct.

Use the following to answer questions 46 and 47:

Alamos Co. exchanged equipment and $18,000 cash for similar equipment. The book value and the

fair value of the old equipment were $82,000 and $90,000, respectively.

46. Assuming that the exchange has commercial substance, Alamos would record a gain/(loss) of:

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

a. $26,000.

b. $ 8,000.

c. $(8,000).

d. $ 0.

47. Assuming that the exchange lacks commercial substance, Alamos would record a gain/(loss)

of:

a. $26,000.

b. $ 8,000.

c. $(8,000).

d. $ 0.

Use the following to answer questions 48 and 49:

Horton Stores exchanged land and cash of $5,000 for similar land. The book value and the fair

value of the land were $90,000 and $100,000, respectively.

48. Assuming that the exchange has commercial substance, Horton would record land-new and a

gain/(loss) of:

Land Gain/(loss)

a. $105,000 $ 0.

b. $105,000 $10,000.

c. $ 95,000 $ 0.

d. $ 95,000 $10,000.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

49. Assuming that the exchange lacks commercial substance, Horton would record land-new and a

gain/(loss) of:

Land Gain/(loss)

a. $105,000 $ 0.

b. $105,000 $10,000.

c. $ 95,000 $ 0.

d. $ 95,000 $10,000.

50. Bloomington Inc. exchanged land for equipment and $3,000 in cash. The book value and the

fair value of the land were $104,000 and $90,000, respectively.

Bloomington would record equipment and a gain/(loss) of:

Equipment Gain/(loss)

a. $ 87,000 $ 3,000.

b. $104,000 $ (5,000).

c. $ 87,000 $(14,000).

d. All of these answer choices are incorrect.

51. P. Chang & Co. exchanged land and $9,000 cash for equipment. The book value and the fair

value of the land were $106,000 and $90,000, respectively.

Chang would record equipment and a gain/(loss) of:

Equipment Gain/(loss)

a. $ 99,000 $ (16,000).

b. $ 90,000 $ (25,000).

c. $108,000 $ 16,000.

d. $106,000 $ (9,000).

Use the following to answer questions 52 and 53:

Below is information relative to an exchange of similar assets by Grand Forks Corp. Assume the

exchange has commercial substance.

Old Equipment

Cash

Book Value

Fair Value

Paid

Case A

$50,000

$60,000

$15,000

Case B

$40,000

$35,000

$ 8,000

52. In Case A, Grand Forks would record the new equipment at:

a. $65,000.

b. $75,000.

c. $50,000.

d. $60,000.

Equipment (FV of land – $3,000)

Loss ($104,000 – 90,000)

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

53. In Case B, Grand Forks would record a gain/(loss) of:

a. $ 5,000.

b. $ 3,000.

c. $(5,000).

d. $(3,000).

Equipment ($35,000 + 8,000)

Loss ($40,000 – 35,000)

Use the following to answer questions 54 and 55:

Below is information relative to an exchange of equipment by Pensacola Inc. Assume the exchange

has commercial substance.

Old Equipment

Cash

Book Value

Fair Value

Received

Case A

$75,000

$80,000

$12,000

Case B

$60,000

$56,000

$10,000

54. In Case A, Pensacola would record the new equipment at:

a. $68,000.

b. $63,750.

c. $67,250.

d. $80,000.

Equipment ($60,000 + 15,000)