Student Name:

Class:

2016 2017 2018 2019

60,000$ 80,000$ 70,000$ 70,000$

(39,600) (52,800) (18,000) (9,600)

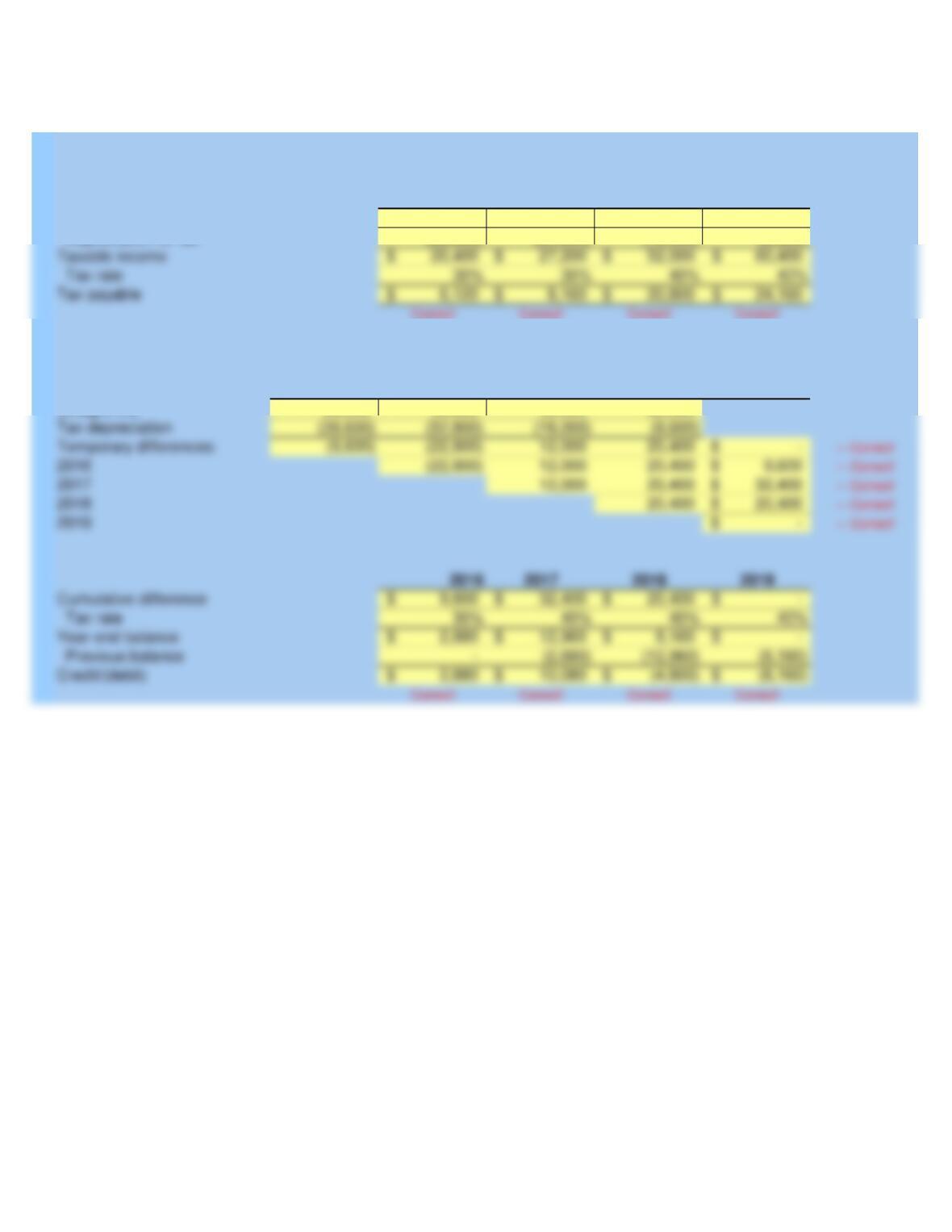

Cumulative

Temporary

2016 2017 2018 2019 Difference

Previous balance

Credit/(debit)

Cumulative difference

Tax depreciation

Temporary differences:

Tax rate

Year-end balance

30,000 30,000 30,000 30,000

Straight-line

Instructor

Calculations

ZEKANY CORPORATION

Problem 16-04

McGraw-Hill/Irwin

Pretax accounting income

Depreciation for tax

Taxable income

Tax rate

Tax payable

Student Name:

Class:

Instructor

Problem 16-04

McGraw-Hill/Irwin

Debit Credit

9,000 «- Correct!

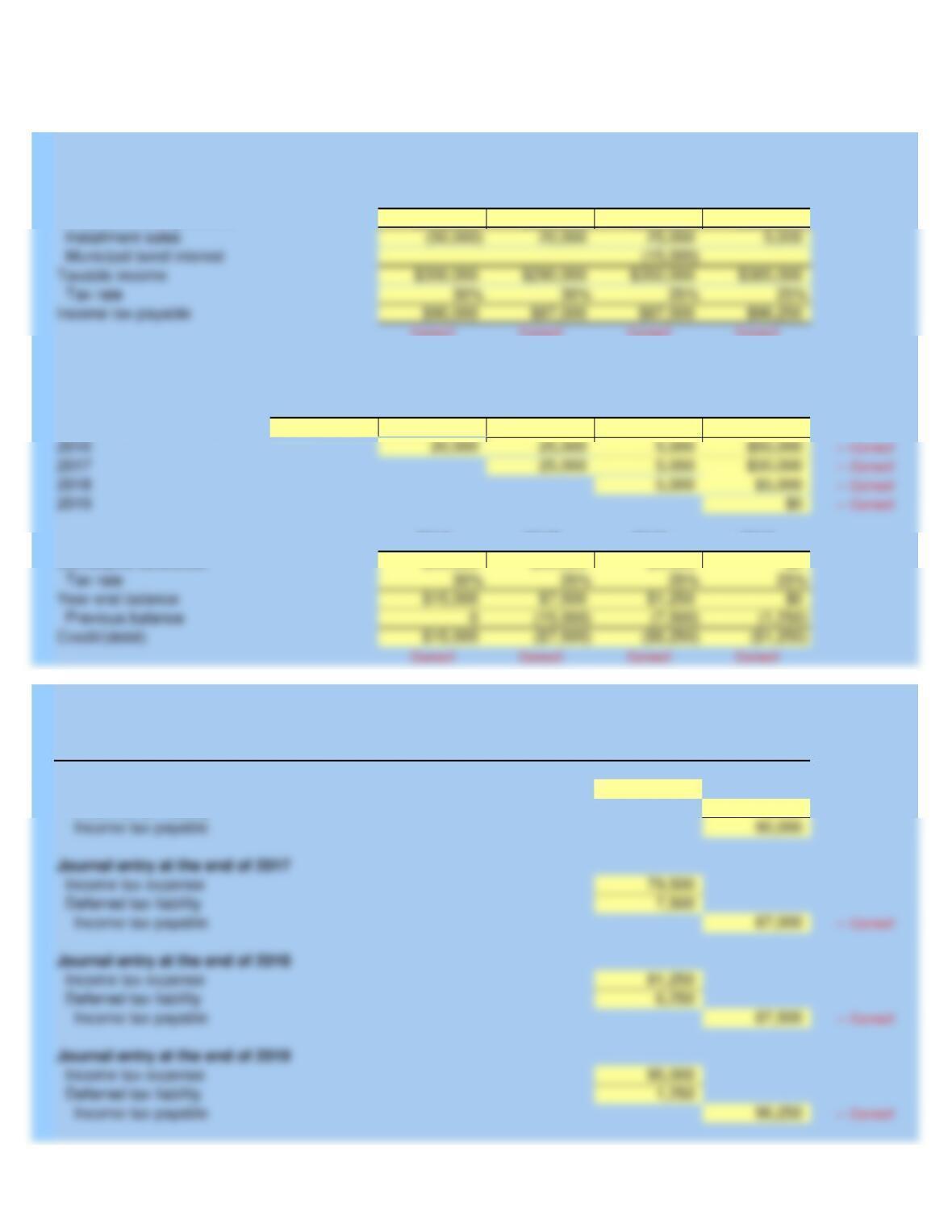

Income tax expense

Journal entry at the end of 2016

Account

ZEKANY CORPORATION

General Journal

Income tax payable

Income tax expense

Deferred tax liability

Income tax payable

Income tax expense

Deferred tax liability

Deferred tax liability

Journal entry at the end of 2019

Journal entry at the end of 2018

Journal entry at the end of 2017

Income tax payable

Income tax expense

Deferred tax liability

Income tax payable

$120,000

2016 2017 2018 2019

$39,600 $52,800 $18,000 $9,600

Depreciation

Given Data P16-04:

ZEKANY CORPORATION

Asset cost

Accounting income before tax and depr.

Average and marginal income tax rate

Student Name:

Class:

2016 2017 2018 2019

$350,000 $270,000 $340,000 $380,000

Correct! Correct! Correct! Correct!

Cumulative

Temporary

2016 2017 2018 2019 Difference

(50,000) 20,000 25,000 5,000 $0 «- Correct!

2016 2017 2018 2019

Previous balance

Tax rate

Year-end balance

$50,000 $30,000 $5,000 $0

Debit Credit

Income tax expense

Deferred tax liability

Income tax payable

Journal entry at the end of 2019

Income tax payable

Income tax payable

Income tax expense

Journal entry at the end of 2018

Journal entry at the end of 2017

Income tax payable

Income tax expense

Deferred tax liability

105,000 «- Correct!

15,000

Income tax expense

Deferred tax liability

Journal entry at the end of 2016

Account

Temporary differences:

Cumulative difference

Instructor

Calculations

DEVILLE COMPANY

General Journal

DEVILLE COMPANY

Problem 16-05

McGraw-Hill/Irwin

Pretax accounting income

Installment sales

Municipal bond interest

Taxable income

Tax rate

Income tax payable

2016 2017 2018 2019

$350,000 $270,000 $340,000 $380,000

$50,000

2016 Installment sale

Given Data P16-05:

DEVILLE COMPANY

Pretax accounting income

2016 2017 2018 2019

Enacted tax rate

Cash collected on installment

2018 Interest from investments

Student Name:

Class:

Current Future

Year Deductible

2014 2015 2016 Amounts

(135)

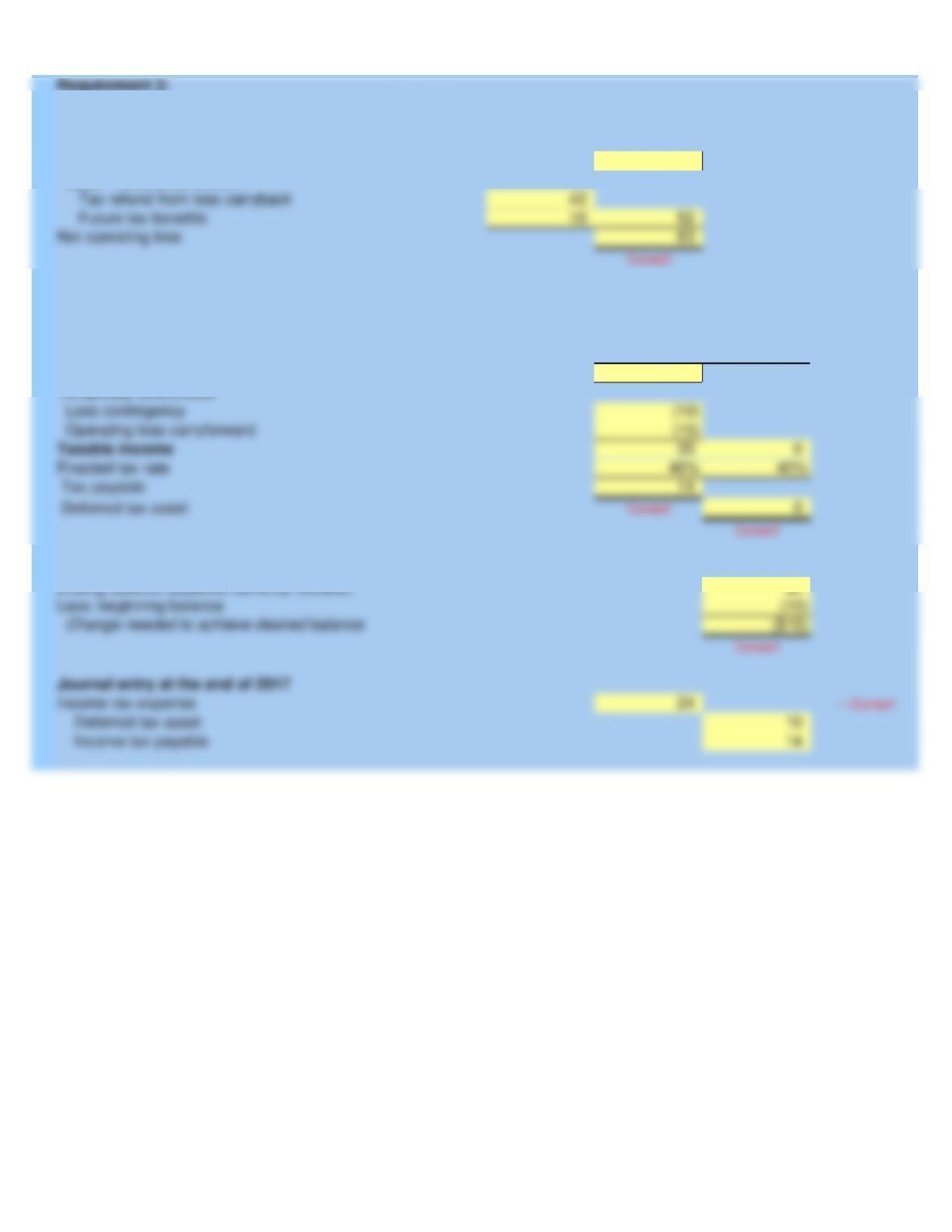

Receivable – income tax refund

Deferred tax asset

Income tax benefit

Less: beginning balance

Journal entry at the end of 2016

$10

Ending balance (balance currently needed)

(in millions)

Prior Years

Deferred tax asset:

Accounting Loss

Permanent difference:

Problem 16-10

McGraw-Hill/Irwin

Intructor

FORES CONSTRUCTION COMPANY

Calculations

Requirement 1:

(120)

Loss carryforward

Enacted tax rate

Deferred tax asset

Loss carryback

Temporary differences:

Fine paid

Loss contingency

Taxable loss

135

Current Future

Year Deductible

2017 Amounts

60

Loss contingency

Operating loss carryforward

Taxable income

Enacted tax rate

Deferred tax asset

Income tax payable

Income tax expense

Journal entry at the end of 2017

Ending balance (balance currently needed)

Less: beginning balance

Deferred tax asset:

Pretax accounting Income

Operating loss before income taxes

Requirement 2:

(in millions)

Less: Income tax benefit

Requirement 3:

Calculations

Future tax benefits

Tax refund from loss carryback

2014 2015

$75,000,000 $30,000,000

Additional Information:

Taxable Income

FORES CONSTRUCTION COMPANY

Given Data P16-10:

2016 pretax operating loss

EPA penalty included in 2016 loss

Accrued loss contingency included in 2016 loss

Enacted tax rate