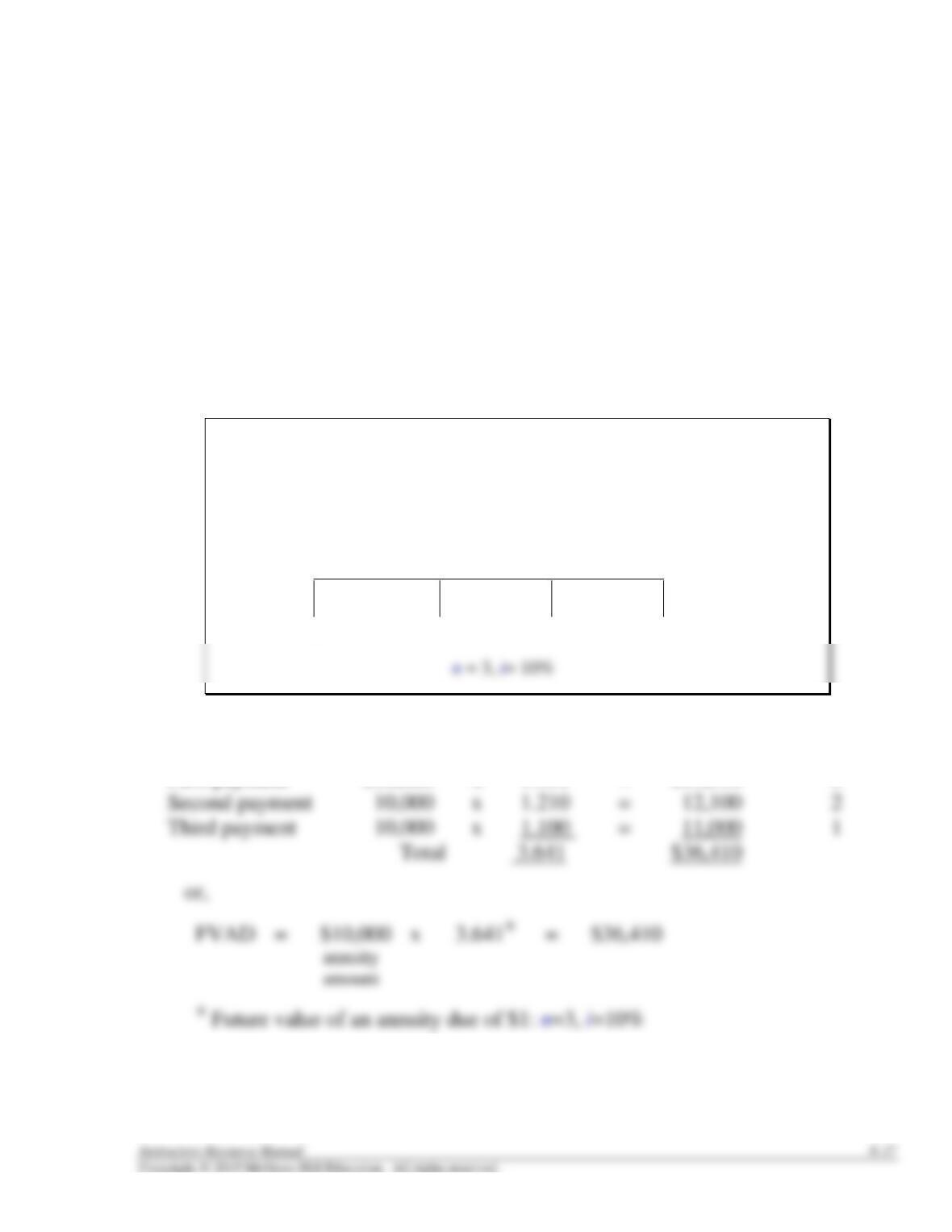

FUTURE VALUE OF AN ANNUITY DUE

Sally Rogers wants to accumulate a sum of money to pay for graduate

school. Rather than investing a single amount today that will grow to

a future value, she decides to invest $10,000 a year over the next

three years in a savings account paying 10% interest compounded

annually. She decides to make the first payment to the bank

immediately. How much will Sally have available in her account at

the end of three years?

Illustration 6-10

Future

Value

?

End of End of End of

0 year 1 year 2 year 3

____________________________________________

$10,000 $10,000 $10,000

FV of $1 Future Value

Payment i=10% (at the end of year 3) n

First payment $10,000 x 1.331 = $13,310 3

T6–13

6-18 Intermediate Accounting, 8/e

PRESENT VALUE OF AN ORDINARY ANNUITY

Sally Rogers wants to accumulate a sum of money to pay for graduate

school. She wants to invest a single amount today in a savings

account earning 10% interest compounded annually that is equivalent

to investing $10,000 at the end of each of the next three years.

Illustration 6-11

Present Value

PV of $1 (at the beginning n

Payment i=10% of year 1)

First payment $10,000 x .90909 = $9,091 1

* Present value of an ordinary annuity of $1: n=3, i=10%

Present Future

Value Value

$24,868 $33,100

End of End of End of

0 year 1 year 2 year 3

____________________________________________

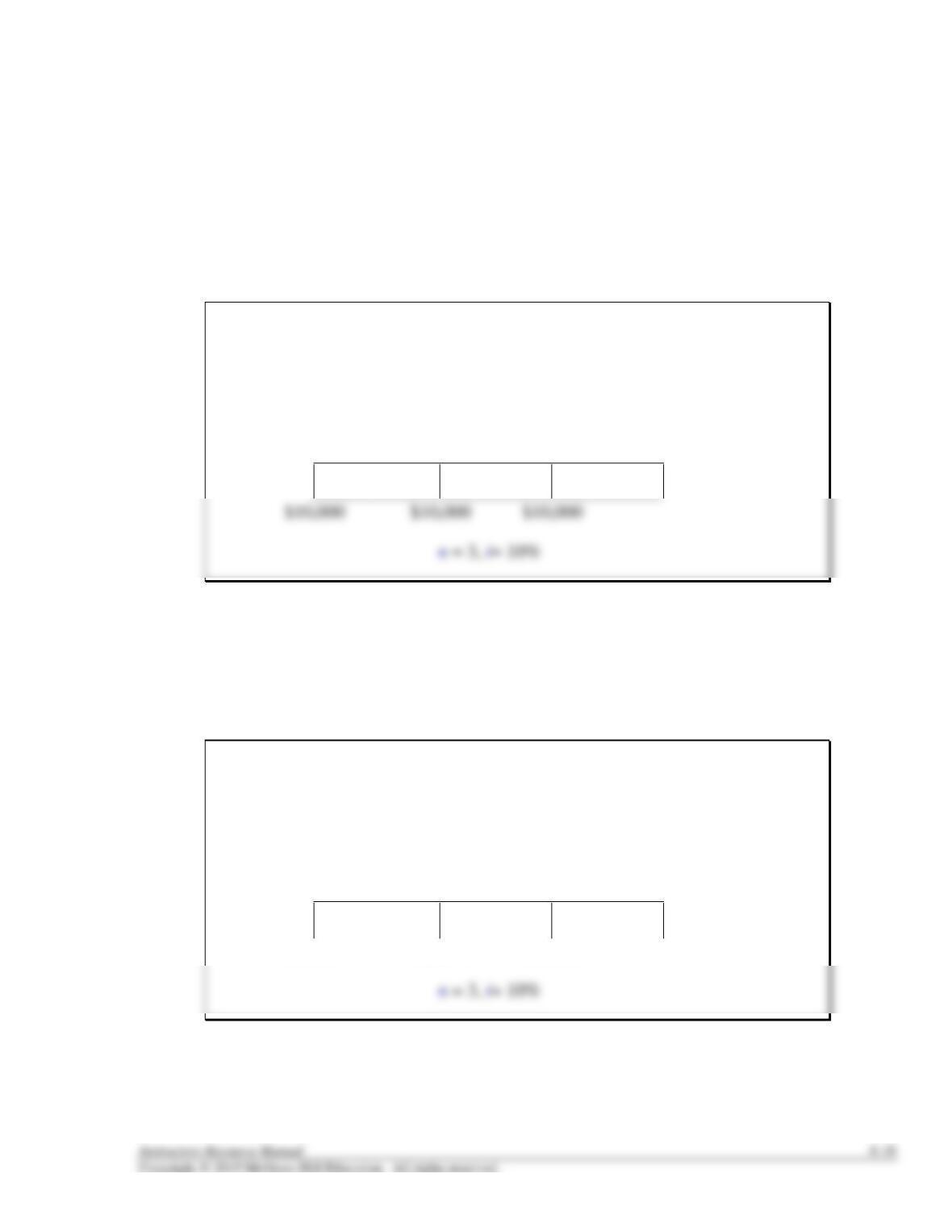

PRESENT VALUE OF AN ANNUITY DUE

In the previous illustration, suppose that the three equal payments of

$10,000 are to be made at the beginning of each of the three years.

What is the present value?

Illustration 6-13

Present

Value

?

End of End of End of

0 year 1 year 2 year 3

_____________________________________________

PVAD = $10,000 x 2.73554* = $27,355 (rounded)

annuity

amount

* Present value of an annuity due of $1: n=3, i=10%

Present Future

Value Value

$27,355 $36,410

End of End of End of

0 year 1 year 2 year 3

____________________________________________

$10,000 $10,000 $10,000

T6–15

6-20 Intermediate Accounting, 8/e

PRESENT VALUE OF A DEFERRED ANNUITY

At January 1, 2016, you are considering acquiring an investment that

will provide three equal payments of $10,000 each to be received at

the end of three consecutive years. However, the first payment is not

expected until December 31, 2018. The time value of money is 10%.

How much would you be willing to pay for this investment?

Illustration 6-14

Present

Value i = 10%

?

1/1/16 12/31/16 12/31/17 12/31/18 12/31/19 12/31/20

$10,000 $10,000 $10,000

Present Value

PV of $1 (at the beginning n

Payment i=10% of year 1)

First payment $10,000 x .75131 = $ 7,513 3

T6–16

PRESENT VALUE OF A DEFERRED ANNUITY

(continued)

or,

1. Calculate the PV of the annuity as of the beginning of the annuity

period.

PVA = $10,000 x 2.48685* = $24,868

2. Discount the single amount calculated in 1 to its present value as of

today.

PV = $24,868 x .82645* = $20,552

future

amount

Present Present Value

Value at beginning of i = 10%

the annuity period

$20,552 $24,868

1/1/16 12/31/16 12/31/17 12/31/18 12/31/19 12/31/20

$10,000 $10,000 $10,000

T6-16 (continued)

6-22 Intermediate Accounting, 8/e

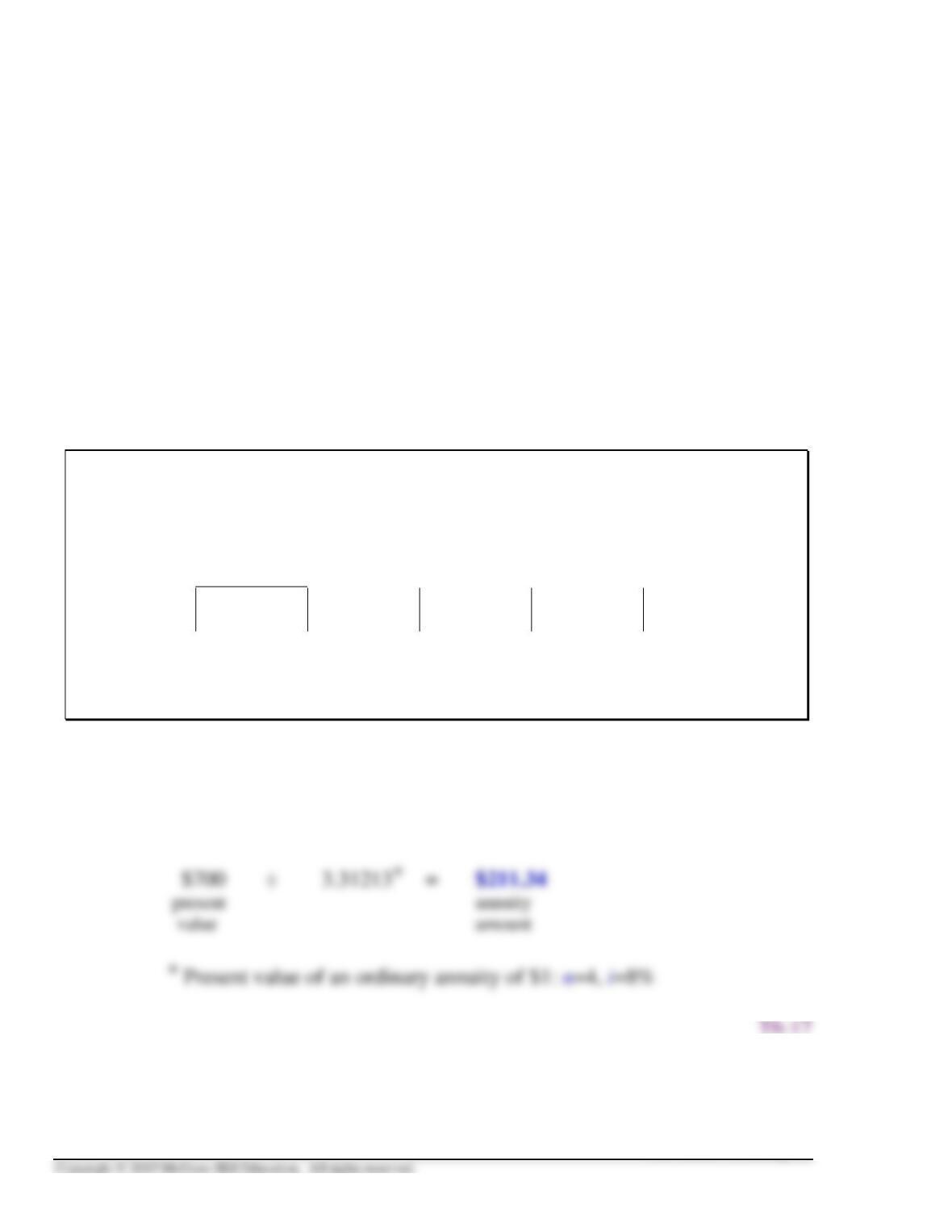

DETERMINING THE ANNUITY AMOUNT WHEN OTHER

VARIABLES ARE KNOWN

Assume that you borrow $700 from a friend and intend to repay the

amount in four equal annual installments beginning one year from

today. Your friend wishes to be reimbursed for the time value of

money at an 8% annual rate. What is the required annual payment

that must be made (the annuity amount), to repay the loan in four

years?

Illustration 6-15

Present

Value

$700 End of End of End of End of

0 year 1 year 2 year 3 year 4

____________________________________

________________________________________________

? ? ? ?

n = 4, i = 8%

$700 = 3.31213* x Annuity amount

present

value

DETERMINING n WHEN OTHER VARIABLES ARE KNOWN

Assume that you borrow $700 from a friend and intend to repay the

amount in equal installments of $100 per year over a period of years.

The payments will be made at the end of each year beginning one

year from now. Your friend wishes to be reimbursed for the time

value of money at a 7% annual rate. How many years would it take

before you repaid the loan?

Illustration 6-16

Present

Value

$700 End of End of End of End of

0 year 1 year 2 year n-1 year n

________________ ________________

____________________________ ________________

n = ?, i = 7%

$700 = $100 x ? *

present annuity

value amount

When you consult the present value of an ordinary annuity table, Table 4, you

search the 7% column (i=7%) for this value and find 7.02358 in row 10. So it

would take approximately 10 years.

T6–18

6-24 Intermediate Accounting, 8/e

VALUATION OF LONG-TERM BONDS

On June 30, 2016, Fumatsu Electric issued 10% stated rate bonds with

a face amount of $200 million. The bonds mature on June 30, 2036 (20

years). The market rate of interest for similar issues was 12%. Interest is

paid semiannually (5%) on June 30 and December 31, beginning

December 31, 2016. The interest payment is $10 million (5% X $200

million). What was the price of the bond issue? What amount of interest

expense will Fumatsu record on the bonds in 2016?

Illustration 6-19

T6–19

VALUATION OF LEASES

On January 1, 2016, the Stridewell Wholesale Shoe Company signed

a 25-year lease agreement for an office building. Terms of the lease

call for Stridewell to make annual lease payments of $10,000 at the

beginning of each year, with the first payment due on January 1,

2016. Assuming that an interest rate of 10% properly reflects the

time value of money in this situation, how should Stridewell value the

asset acquired and the corresponding lease liability?

Illustration 6-20

PVAD = $10,000 x 9.98474* = $99,847

annuity

amount

T6–20

6-26 Intermediate Accounting, 8/e

VALUING A PENSION OBLIGATION

On January 1, 2016, the Stridewell Wholesale Shoe Company hired Sammy

Sossa. Sammy is expected to work for 25 years before retirement on December

31, 2040. Annual retirement payments will be paid at the end of each year

during his retirement period, expected to be 20 years. The first payment will be

on December 31, 2041. During 2016, Sammy earned an annual retirement

benefit estimated to be $2,000 per year. The company plans to contribute cash

to a pension fund that will accumulate to an amount sufficient to pay Sammy

this benefit. Assuming that Stridewell anticipates earning 6% on all funds

invested in the pension plan, how much would the company have to contribute

at the end of 2016 to pay for pension benefits earned in 2016?

Illustration 6-21

Present

Value i = 6%

?

2016 2017 2040 2041 2042 2060

____________________ _____________________________________ ______

$2,000 $2,000 $2,000

n = 24 n = 20

PVA = $2,000 x 11.46992* = $22,940

annuity

amount

T6–21

SUMMARY OF TIME VALUE OF MONEY CONCEPTS

Concept

Summary

Formula

Table

Future value (FV) of $1

The amount of money that a

dollar will grow to at some

point in the future.

FV = $1(1 + i)n

1

Present value (PV) of $1

The amount of money today

that is equivalent to a given

amount to be received or paid

in the future.

Future value of an ordinary

annuity (FVA) of $1

The future value of a series

of equal-sized cash flows

with the first payment taking

place at the end of the first

compounding period.

FVA = (1+i)n-1

i

3

Present value of an ordinary

annuity (PVA) of $1

The present value of a series

of equal-sized cash flows

with the first payment taking

place at the end of the first

compounding period.

4

Future value of an annuity

due (FVAD) of $1

The future value of a series

of equal-sized cash flows

with the first payment taking

place at the beginning of the

annuity period.

FVAD = [(1+i)n-1

i] x (1+i)

5

Present value of an annuity

due (PVAD) of $1

The present value of a series

of equal-sized cash flows

with the first payment taking

place at the beginning of the

annuity period.

6

T6–22

6-28 Intermediate Accounting, 8/e

Suggestions for Class Activities

1. Real World Scenario

An important accounting application of present value techniques illustrated in this chapter is the

valuation of bonds. Occasionally, corporations issue zero-coupon bonds or notes. These

instruments pay no stated interest over their life. For example, in 1997, Costco Wholesale

Corporation issued 20-year, zero coupons bonds with a maturity value of $900 million. The

company received $450 million upon issuance of these bonds.

Suggestions:

Have the class consider the Costco zero-coupon bonds. What is the approximate interest rate

implicit in these bonds when they were issued in 1997?

Points to note:

Students must solve for the unknown interest rate when PV and FV are known. In millions:

$450 = $900 x ? *

* Present value of $1: n =20 , i = ?

When you consult the present value table, Table 2, you search row 20 (n = 20) for this value. The

rate is approximately 3.5%. The company’s debt disclosure note reports that these notes were sold

to yield 3.5%.

2. Professional Skills Development Activities

The following are suggested assignments from the end–of-chapter material that will help your

students develop their communication, research, analysis, and judgment skills.

Communication Skills. In addition to Communication Case 6-3, Judgment Case 6-5 can be

adapted to ask students to choose one of the two alternatives and write a memo supporting their

Research Skills. In their careers, our graduates will be required to locate and extract relevant

information from available resource material to determine the correct accounting practice,

Analysis Skills. The “Broaden Your Perspective” section includes Analysis Cases that direct

students to gather, assemble, organize, process, or interpret data to provide options for making

Judgment Skills. The “Broaden Your Perspective” section includes Judgment Cases that require

6-30 Intermediate Accounting, 8/e

Assignment Chart

Learning Est. time

Questions Objective(s) Topic (min.)

6-1

1

Interest

5

6-2

1

Compound interest

5

6-3

1

Effective rate or yield

5

6-4

2

Future value

5

6-5

3

Present value

5

6-6

ó

Monetary versus nonmonetary assets and

liabilities

5

6-7

5

Annuity

5

6-8

5

Ordinary annuity versus an annuity due

5

6-9

3,5

Present value table relationships

5

6-10

5

Time diagram-ordinary annuity

5

6-11

5

Time diagram-annuity due

5

6-12

7

Deferred annuity

5

6-13

8

Explain how to compute unknown annuity

payment

5

6-14

8

Compute unknown annuity payment

5

6-15

9

Long-term leases

5

Brief Learning Est. time

Exercises Objective(s) Topic (min.)

6-1

1

Simple versus compound interest

5

6-2

2

Future value; single amount

5

6-3

4

Future value; solving for unknown single amount

5

6-4

3

Present value; single amount

5

6-5

4

Present value; solving for unknown single amount

5

6-6

6

Future value; ordinary annuity

5

6-7

6

Future value; annuity due

5

6-8

7

Present value; ordinary annuity

5

6-9

7

Present value; annuity due

5

6-10

7

Deferred annuity

10

6-11

8

Solve for unknown; annuity

5

6-12

9

Price of a bond

10

6-13

9

Lease payment

10

Learning Est. time

Exercises Objective(s) Topic (min.)

6-1

2

Future value; single amounts

10

6-2

2

Future value; single amounts

10

6-3

3

Present value; single amounts

10

6-4

3

Present value; multiple, unequal amounts

10

6-5

3

Noninterest-bearing note; single payment

10

6-6

4

Solving for unknowns; single amounts

20

6-7

6

Future value; annuities

20

6-8

7

Present value; annuities

10

6-9

8

Solving for unknowns; annuities

20

6-10

4,8

Future value; solving for annuities and single

amounts

15

6-11

3,6,7

Future and present value

20

6-12

7

Deferred annuities

15

6-13

8

Solving for unknown annuity payment

10

6-14

8

Solving for unknown interest rate

10

6-15

8

Solving for unknown annuity amount

10

6-16

7,8

Deferred annuities; solving for annuity amount

15

6-17

9

Price of a bond

10

6-18

9

Price of a bond; interest expense

15

6-19

9

Lease payments

10

6-20

8,9

Lease payments; solve for unknown interest rate

10

6-21

1,2,3,5

Concepts; terminology

15

CPA/CMA Learning Est. time

Exam Questions Objective(s) Topic (min.)

CPA-1

3

Present value; single amount

3

CPA-2

7

Noninterest-bearing note

3

CPA-3

7

Present value; annuities

3

CPA-4

7

Present value; annuities

3

CPA-5

7

Present value; annuities

3

CPA-6

9

Price of a bond

3

CPA-7

8

Solving for unknowns; annuities

3

2

Future value; annuities

3

CMA-2

5,9

Lease payments

3

6-32 Intermediate Accounting, 8/e

Learning Est. time

Problems Objective(s) Topic (min.)

6-1

3,7

Analysis of alternatives

20

6-2

6,7,9

Present and future value

25

6-3

3,7

Analysis of alternatives

15

6-4

3,7

Investment analysis

20

6-5

3,7

Investment decision; varying rates

25

6-6

3,8

Solving for unknowns

20

6-7

8

Solving for unknowns

20

6-8

7

Deferred annuities

15

6-9

7

Deferred annuities

15

6-10

3,7

Noninterest-bearing note; annuity and lump-sum

payment

10

6-11

8,9

Solving for unknown lease payment

20

6-12

8,9

Lease payment; various compounding periods

20

6-13

3,7,9

Lease vs. buy alternatives

15

6-14

7,9

Deferred annuities; pension obligation

25

6-15

3,7,9

Bonds and leases; deferred annuities

30

Star Problems

Learning Est. time

Cases Objective(s) Topic (min.)

Ethics Case 6-1

1

Return on investment

20

Analysis Case 6-2

3,7

Bonus alternatives; present value analysis

15

Communication Case 6-3

7

Present value of annuities

60

Analysis Case 6-4

7

Present value of an annuity

15

Judgment Case 6-5

3,7

Replacement decision

15

Real World Case 6-6

3,9

20

Real World Case 6-7

3,9

Leases, Southwest Airlines

20