Problem 15-9 (continued)

Requirement 2

The lessee’s incremental borrowing rate (12%) is more than the lessor’s implicit

rate (10%). So, both parties’ calculations should be made using a 10% discount rate:

Application of Classification Criteria

1 Does the agreement specify that

ownership of the asset transfers

to the lessee? NO

Present Value of Minimum Lease Payments

Present value of periodic lease payments excluding

15–102 Intermediate Accounting, 8/e

Problem 15-9 (continued)

(a) by Western Soya Co. (the lessee)

Since at least one criterion is met, this is a capital lease to the lessee. Western

(b) by Rhone-Metro (the lessor)

Since the fair value exceeds the lessor’s book value, the equipment is being “sold”

at a profit, making this a sales-type lease:

Fair value $365,760

Requirement 3

December 31, 2016

Western Soya Co. (Lessee)

Leased equipment (calculated above) …………………………... 348,685

Lease payable (calculated above) ……………………………… 348,685

Rhone-Metro (Lessor)

Lease receivable (fair value)………………………………………. 365,760

Problem 15-9 (continued)

Requirement 4

Lessee (unguaranteed residual value excluded):

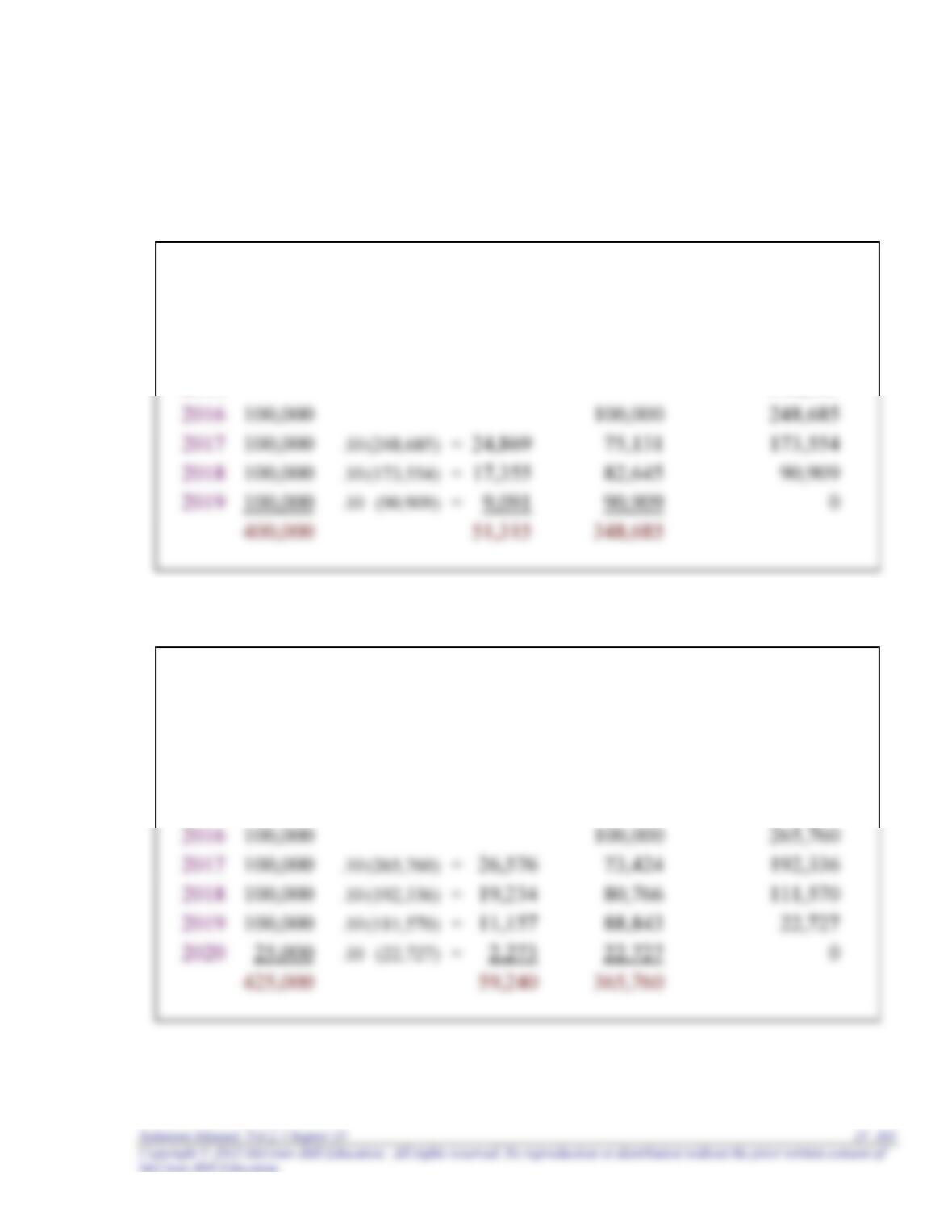

Lease Amortization Schedule

Effective Decrease Outstanding

Dec. Payments Interest in Balance Balance

31 10% x Outstanding Balance

2016 348,685

Lessor (unguaranteed residual value included):

Lease Amortization Schedule

Effective Decrease Outstanding

Dec. Payments Interest in Balance Balance

31 10% x Outstanding Balance

2016 365,760

Problem 15-9 (continued)

Requirement 5

December 31, 2017

Western Soya Co. (Lessee)

Depreciation expense ([$348,685] ÷ 4 years) …………………….. 87,171

Problem 15-9 (concluded)

Requirement 6

December 31, 2020

Western Soya Co. (Lessee)

Operating expense (2020 expenses) …………………………….. 4,000

15–106 Intermediate Accounting, 8/e

Problem 15-10

Requirement 1

Lessor’s Calculation of Lease payments

Amount to be recovered (fair value) $365,760

Problem 15-10 (continued)

Application of Classification Criteria

1 Does the agreement specify that

ownership of the asset transfers

to the lessee? NO

Present Value of Minimum Lease Payments

Present value of periodic lease payments excluding

executory costs of $4,000 ($130,960 x 2.73554**) $358,247***

Problem 15-10 (continued)

(a) by Western Soya Co. (the lessee)

(b) by Rhone-Metro (the lessor)

Since the fair value exceeds the lessor’s book value, the equipment is being “sold”

at a profit, making this a sales-type lease:

Requirement 3

December 31, 2016

Western Soya Co. (Lessee)

Leased equipment (calculated above) …………………………... 365,760

Lease payable (calculated above) ……………………………… 365,760

Problem 15-10 (continued)

Requirement 4

Lessee and lessor (BPO included):

Since both use the same discount rate and since the bargain purchase option is

included as an additional payment for both, the same amortization schedule applies to

both the lessee and lessor. The lease term ends for accounting purposes after 3 lease

payments, because the BPO becomes exercisable before the fourth:

Lease Amortization Schedule

Effective Decrease Outstanding

Dec. Payments Interest in Balance Balance

31 10% x Outstanding Balance

2016 365,760

15–110 Intermediate Accounting, 8/e

Problem 15-10 (continued)

Requirement 5

December 31, 2017

Western Soya Co. (Lessee)

Depreciation expense ($365,760 ÷ 6 years*) …………………….. 60,960

Rhone-Metro (Lessor)

Cash (lease payment) …………………………………………………. 134,960

Problem 15-10 (concluded)

Requirement 6

December 31, 2019

Western Soya Club (Lessee)

Depreciation expense ($365,760 ÷ 6 years) ………………………. 60,960

15–112 Intermediate Accounting, 8/e

Problem 15-11

Requirement 1

Lessor’s Calculation of Lease payments

Amount to be recovered (fair value) $659,805

Less: Present value of the third-party-guaranteed

Requirement 2

Since [1] title to the conveyer does not transfer to the lessee, [2] there is no BPO,

and [3] the lease term (3 years) is less than 75% of the estimated useful life (6 years),

Problem 15-11 (continued)

For the lessor, the criterion is met: The present value of minimum lease payments

($659,805) is more than 90% of the fair value ($659,805 x 90% = $593,825). Also,

since the fair value exceeds the lessor’s book value, the conveyer is being “sold” at a

profit, making this a sales-type lease:

Fair value $659,805

minus

Lessee’s Calculation of the

Present Value of Minimum Lease Payments

Present value of periodic lease payments*

15–114 Intermediate Accounting, 8/e

Problem 15-11 (continued)

Requirement 3

December 31, 2016

Poole (Lessee)

Prepaid rent (2016 payment; 2017 expense) …………………….. 200,000

Requirement 4

Since the lessee records the lease as an operating lease, interest expense is not

recorded and an amortization schedule is not applicable.

Lessor (third-party-guaranteed residual value included):

Lease Amortization Schedule

Effective Decrease Outstanding

Dec. Payments Interest in Balance Balance

31 10% x Outstanding Balance

2016 659,805

Problem 15-11 (continued)

Requirement 5

December 31, 2017

Poole (Lessee)

Rent expense …………………………………………………………. 200,000

Allied (Lessor)

Cash (lease payment)…………………………………………………. 200,000

December 31, 2018

Poole (Lessee)

Rent expense …………………………………………………………. 200,000

Allied (Lessor)

15–116 Intermediate Accounting, 8/e

Problem 15-11 (concluded)

December 31, 2019

Poole (Lessee)

Rent expense …………………………………………………………. 200,000

Problem 15-12

Situation

1 2 3 4

A. The lessor’s:

1. Minimum lease payments1 $40,000 $44,000 $44,000 $40,000

1 ($10,000 x number of payments) + Residual value guaranteed by lessee and/or by

third party.

Problem 15-13

Situation

1 2 3 4

A. The lessor’s:

1. Minimum lease payments1 $400,000 $553,000 $640,000 $510,000

Note: Since executory costs are excluded from minimum lease payments, they have no effect on

any of the calculated amounts.

1 ($100,000 x Number of payments) + Residual value guaranteed by lessee and/or by third party;

for situation 4: ($100,000 x 4) + ($60,000 + 50,000)

15–118 Intermediate Accounting, 8/e

Problem 15-14

Requirement 1

Branson Construction (Lessee)

Interest expense (10% x [$936,500 – 100,000]) ………………….. 83,650

Lease payable (difference) …………………………………………. 16,350

Requirement 2

Branson Construction (Lessee)

Interest expense (10% x [$936,500 – 100,000]) ………………….. 83,650

Lease payable (to balance) …………………………………………. 16,350

Problem 15-14 (concluded)

Branif Leasing (Lessor)

Cash (lease payment)…………………………………………………. 103,000

Requirement 3

Branson Construction (Lessee)

Interest expense (10% x [$936,500 – 100,000]) ………………….. 83,650

15–120 Intermediate Accounting, 8/e

Problem 15-15

Requirement 1

Note:

Because exercise of the option appears at the inception of the lease to be

reasonably assured, payment of the option price ($6,000) is expected to occur

Present value of quarterly lease payments ($3,000 x 7.23028**) $21,691