Exercise 8–25

Set the base year, 1/1/16, equal to 1.00.

Cost index in layer year: 264 ÷ 240 = 1.10

Ending Inventory Inventory Layers Inventory Layers Inventory

Date at Base Year Cost at Base Year Cost Converted to Cost DVL Cost

8–42 Intermediate Accounting, 8/e

Exercise 8–26

List A List B

i 1. Perpetual inventory a. Legal title passes when goods are

system delivered to common carrier.

CPA / CMA REVIEW QUESTIONS

CPA Exam Questions

1. d.

CMA Exam Questions

1. c. The company began March with 3,200 units in inventory at $64.30 each.

The March 4 purchase added 3,400 additional units at $64.75 each. Under

FIFO, the 3,600 units sold on March 14 were the oldest units. That sale

Problem 8–1

Requirement 1

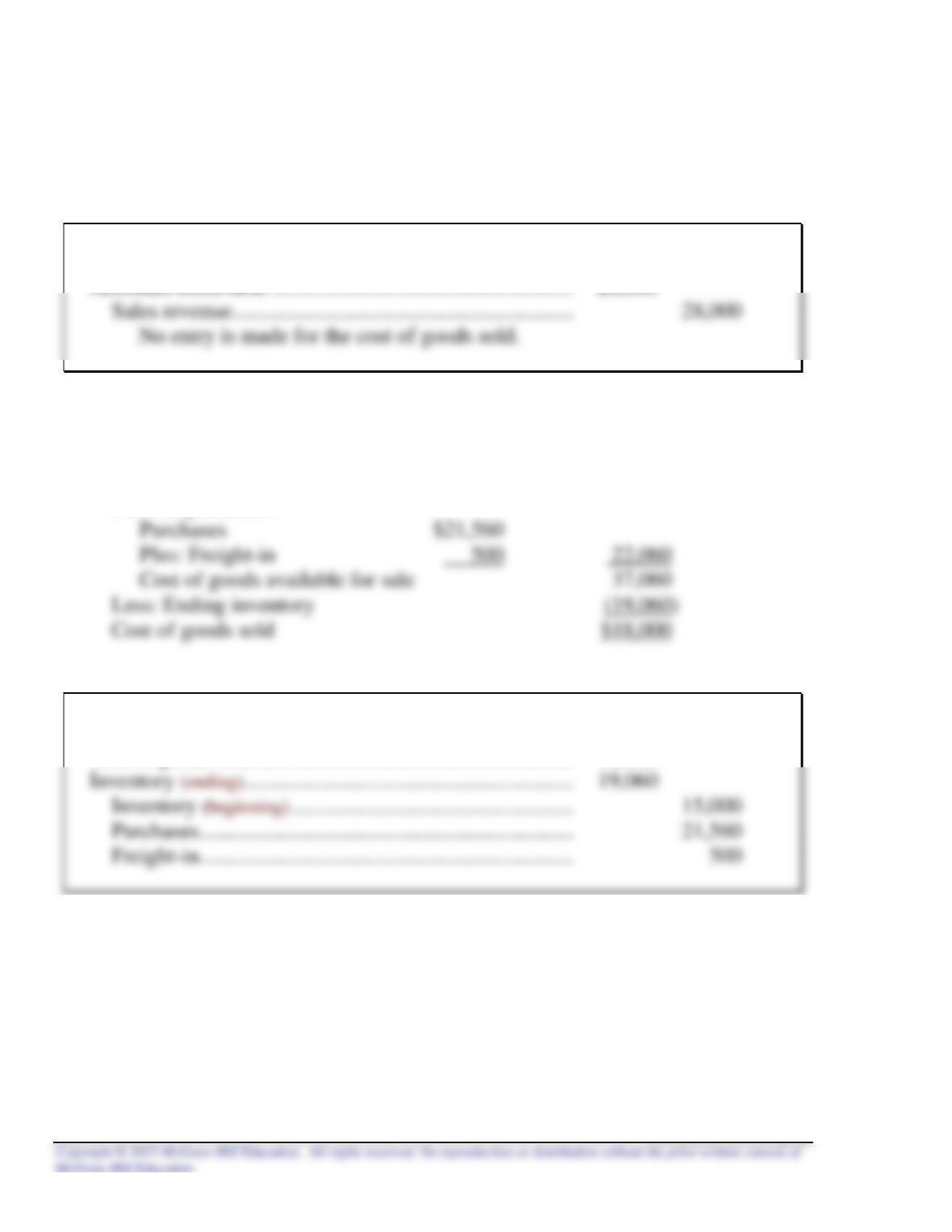

a. To record the purchase of inventory on account and the payment of freight

charges.

October 12, 2016

Purchases (98% x $22,000) ………………………………………… 21,560

b. To record payment of accounts payable.

October 31, 2016

PROBLEMS

8–46 Intermediate Accounting, 8/e

Problem 8–1 (continued)

c. To record sales on account.

October 2016

Cost of goods sold:

Beginning inventory $15,000

Plus net purchases:

Adjusting entry:

October 31, 2016

Cost of goods sold (above) ……………………………………….. 18,000

Problem 8–1 (concluded)

Requirement 2

a. To record the purchase of inventory on account and the payment of freight

charges.

October 12, 2016

Inventory (98% x $22,000) ………………………………………… 21,560

b. To record payment of accounts payable.

October 31, 2016

c. To record sales on account.

October 2016

8–48 Intermediate Accounting, 8/e

Problem 8–2

1. The transaction is not correctly accounted for. Inventory held on consignment by

2. The transaction is not correctly accounted for. Legal title to merchandise shipped

3. The transaction is not correctly accounted for. Since the merchandise was shipped

2017.

4. The transaction is correctly accounted for. Merchandise held on consignment from

5. The transaction is correctly accounted for. Since the merchandise was shipped

Problem 8–3

Accounts

Inventory Payable Sales

Initial amounts $1,250,000 $1,000,000 $9,000,000

Adjustments – increase (decrease):

1. (155,000) (155,000) NONE

Problem 8–4

Requirement 1

Beginning inventory (10,000 x $8.00) $ 80,000

Net purchases:

Purchases (50,000* units x $10.00) $500,000

Requirement 2

Sales (45,000 units x $18.00) $810,000

Problem 8–5

Cost of goods available for sale for periodic system:

Beginning inventory (6,000 x $8.00) $ 48,000

Purchases:

1. FIFO, periodic system

Cost of goods available for sale (17,000 units) $153,000

Cost of ending inventory:

Date of

purchase Units Unit cost Total cost

Jan. 10 2,000 $ 9.00 $18,000

Problem 8–5 (continued)

2. LIFO, periodic system

Cost of goods available for sale (17,000 units) $153,000

Less: Ending inventory (determined below) (66,000)

Cost of goods sold $ 87,000

Cost of ending inventory:

Date of

purchase Units Unit cost Total cost

Beg. Inv. 6,000 $8.00 $48,000

8–52 Intermediate Accounting, 8/e

Problem 8–5 (continued)

3. LIFO, perpetual system

Date

Purchased

Sold

Balance

Beginning

inventory

6,000 @ $8.00 = $48,000

6,000 @ $8.00 $48,000

January 5

3,000 @ $8.00 = $24,000

3,000 @ $8.00 $24,000

4. Average cost, periodic system

Cost of goods available for sale (17,000 units) $153,000

Less: Ending inventory (below) (72,000)

Problem 8–5 (concluded)

5. Average cost, perpetual system

Date

Purchased

Sold

Balance

Beginning

inventory

6,000 @ $8.00 = $48,000

6,000 @ $8.00 $48,000

January 5

3,000 @ $8.00 $24,000

January 12

6,000 @ $8.625 $51,750

8–54 Intermediate Accounting, 8/e

Problem 8–6

Requirement 1

Cost of goods available for sale for periodic system:

Purchases:

5,000 x $4.00 $20,000

a. FIFO

Cost of goods available for sale (34,000 units) $159,000

b. LIFO

Cost of goods available for sale (34,000 units) $159,000

Problem 8–6 (concluded)

c. Average cost

Cost of goods available for sale (34,000 units) $159,000

Less: Ending inventory (below) (65,471)

Cost of goods sold $ 93,529*

Cost of ending inventory:

Gross Profit ratio:

FIFO: $51,000* ÷ $140,000** = 36%

Requirement 2

In situations when costs are rising, LIFO results in a higher cost of goods sold

8–56 Intermediate Accounting, 8/e

Problem 8–7

Requirement 1

Beginning inventory ($60,000 + 60,000 + 63,000) $183,000

Purchases:

211 $63,000

212 63,000

Requirement 2

Cost of goods available for sale $798,300

Cost of ending inventory (3 autos):

Car ID Cost

219 $ 75,000

Problem 8–7 (concluded)

Requirement 3

Cost of goods available for sale $798,300

Cost of ending inventory (3 autos):

Car ID Cost

203 $ 60,000

Requirement 4

Cost of goods available for sale (12 units) $798,300

Cost of ending inventory:

$798,300

8–58 Intermediate Accounting, 8/e

Problem 8–8

Requirement 1

The note indicates that if the company had used FIFO, inventory would have

been higher by $2,504 million and $2,750 million at the end of 2013 and 2012,

Requirement 2

Requirement 3

Problem 8–9

Requirement 1

Beginning inventory $ 450,000

Purchases:

Requirement 2

Cost of goods sold assuming all units purchased at the year 2016 price:

40,000 units x $25.00 = $1,000,000

Problem 8–10

Requirement 1

Cost of goods sold:

2016: 1,000 x $16 = $ 16,000

Requirement 2

LIFO liquidation before-tax profit or loss:

2016: 1,000 units x $2 ($18 – 16) = $2,000 profit

Requirement 3

Disclosure note:

During fiscal 2018, 2017, and 2016, inventory quantities in certain LIFO layers were