Exercise 7–8

Requirement 1

Estimated returns = 4% x $11,500,000 = $460,000

To record the actual sales returns

Sales returns ………………………………………………………….. 450,000

December 31, 2016 To record the estimated sales returns

Sales returns ………………………………………………………….. 10,000

7–22 Intermediate Accounting, 8/e

Exercise 7–8 (continued)

Note: another series of journal entries that produce the same end result would be:

To record the actual sales returns

Allowance for sales returns ……………………………………… 450,000

December 31, 2016 To record the estimated sales returns

Sales returns (4% x $11,500,000) …………………………………. 460,000

Requirement 2

Beginning balance in allowance account $300,000

Exercise 7–9

Requirement 1

and Doubtful Accounts.”

Requirement 2

FASB ACS 310–10–50–9 reads as follows:

“In addition to disclosures required by this Subsection and Subtopic 450-20, an entity

7–24 Intermediate Accounting, 8/e

Exercise 7–10

Requirement 1

Requirement 2

Allowance for uncollectible accounts

Balance, beginning of year $42,000

Requirement 3

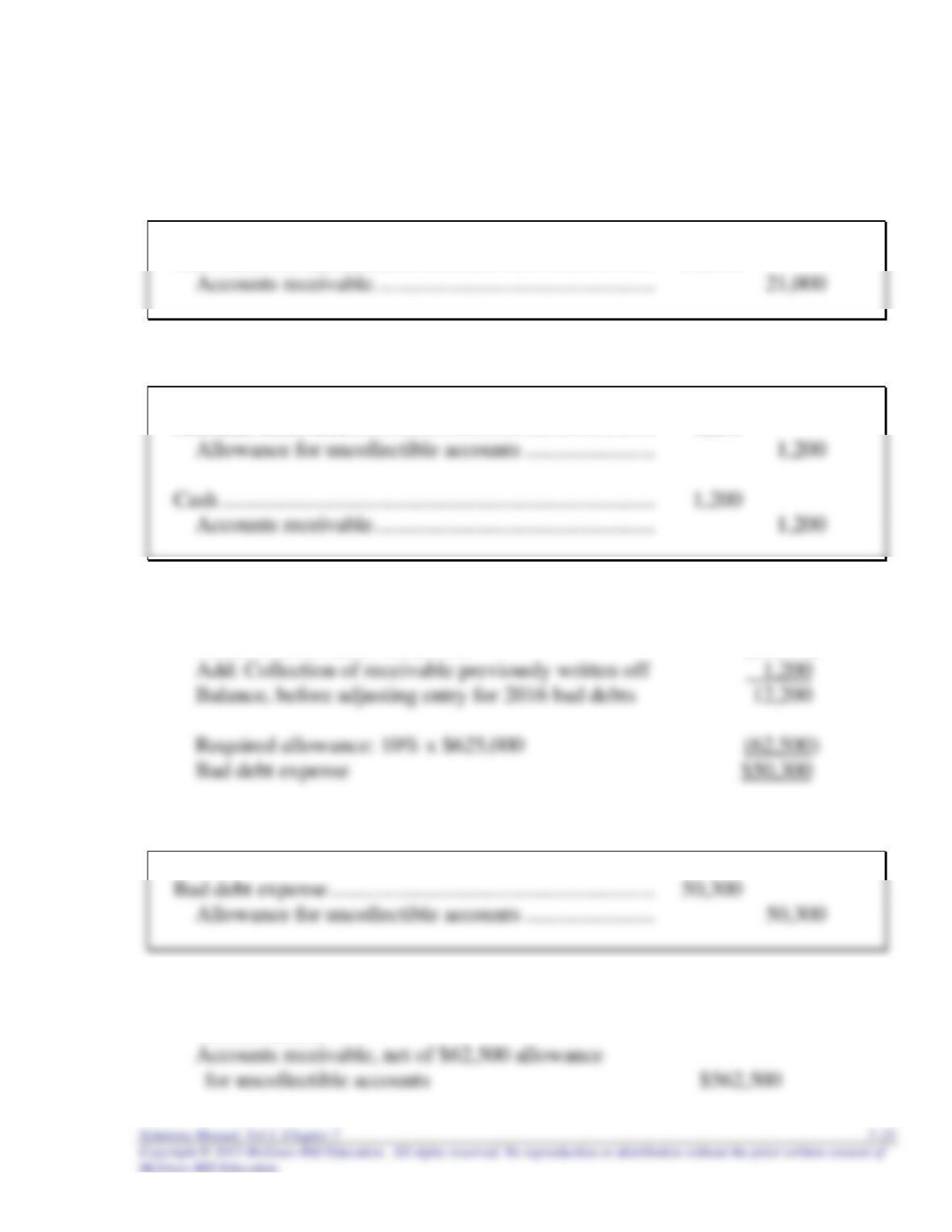

Exercise 7–11

Requirement 1

To record the write-off of receivables:

Allowance for uncollectible accounts ………………………. 21,000

To reinstate an account previously written off and to record the collection:

Accounts receivable ……………………………………………….. 1,200

Allowance for uncollectible accounts:

Balance, beginning of year $32,000

Deduct: Receivables written off (21,000)

To record bad debt expense for the year:

Requirement 2

Current assets:

7–26 Intermediate Accounting, 8/e

Exercise 7–12

Using the direct write-off method, bad debt expense is equal to actual write-offs.

Collections of previously written-off receivables are recorded as revenue.

Allowance for uncollectible accounts:

Balance, beginning of year $17,280

Exercise 7–13

($ in millions)

Allowance for uncollectible accounts:

Balance, beginning of year $21.7

12.0

19.9

Accounts receivable analysis:

Balance, beginning of year $ 1,345.3

($1,323.6 + 21.7)

17,774.1

13.8

1,466.3

Allowance

21.7

Gross A/R

1,345.3

Exercise 7–14

Requirement 1

June 30, 2016

Note receivable ……………………………………………………… 30,000

Sales revenue …………………………………………………….. 30,000

December 31, 2016

Requirement 2

2016 income before income taxes would be understated by $900

7–28 Intermediate Accounting, 8/e

Exercise 7–15

Requirement 1

June 30, 2016

December 31, 2016

March 31, 2017

Discount on note receivable ……………………………………. 600

Requirement 2

$ 1,800 interest for 9 months

Exercise 7–16

Requirement 1

Sales revenue = present value of the note receivable

Requirement 2

January 1, 2016

Note receivable …………………………………………..

515,000

Discount on note receivable………………………

Sales revenue* ………………………………………..

December 31, 2016

Discount on note receivable………………………….

Interest revenue ($408,822 × 8%) …………………

December 31, 2017

Discount on note receivable …………………………...

35,322

December 31, 2018

Cash …………………………………………………………….

515,000

Discount on note receivable …………………………...

7–30 Intermediate Accounting, 8/e

Exercise 7–17

Requirement 1

Book (carrying) value of stock $16,000

Plus gain on sale of stock 6,000

Requirement 2

January 1, 2016

To accrue interest on note receivable for twelve months:

December 31, 2016

Exercise 7–18

Exercise 7–19

Cash (90% x $60,000) ……………………………………………….. 54,000

Exercise 7–20

Cash ([90% – 2%] x $60,000) ………………………………………. 52,800

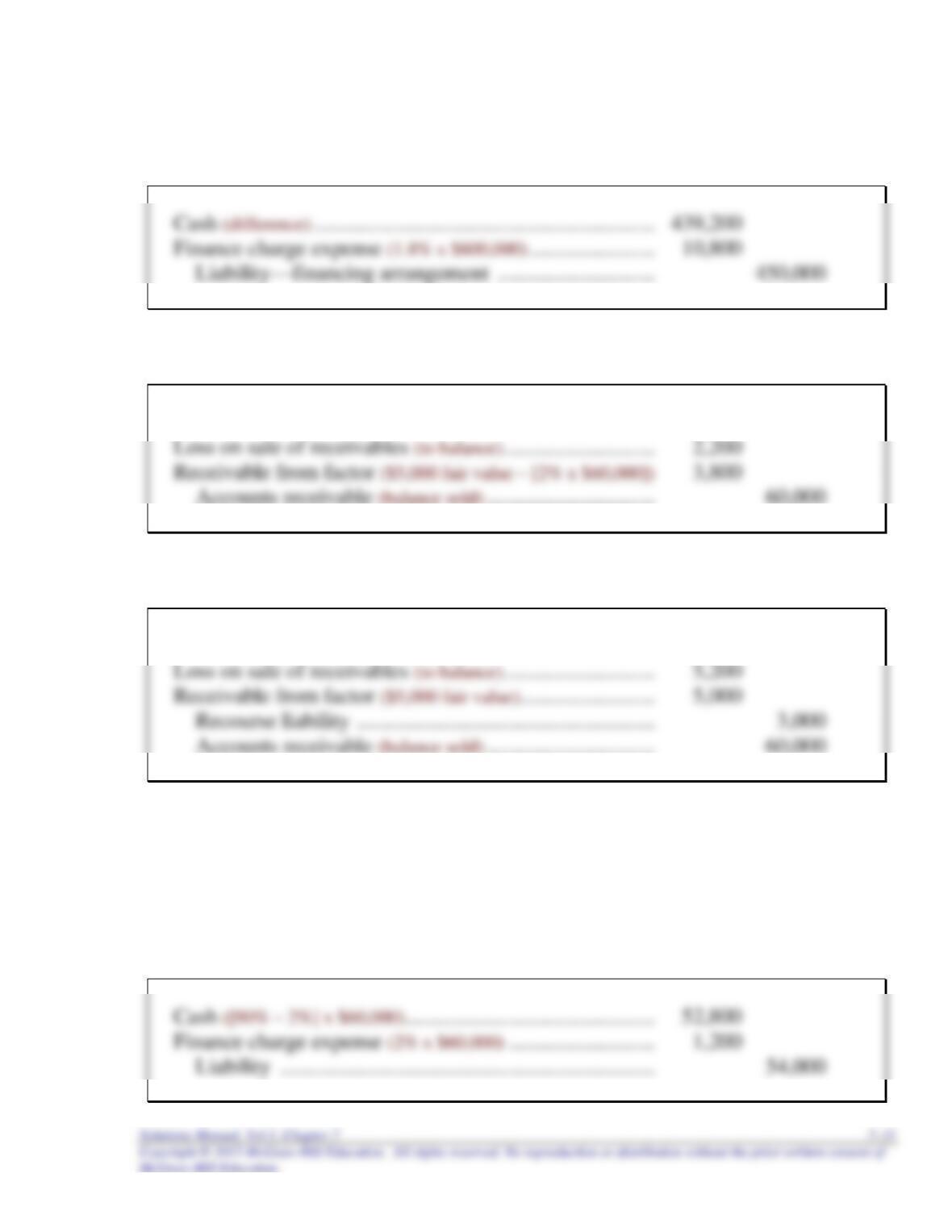

Exercise 7–21

Mountain High retains significant risks and rewards and therefore must treat the

transfer as a secured borrowing. The accounts receivable stay on the balance sheet of

Mountain High, and they must record a liability.

7–32 Intermediate Accounting, 8/e

Exercise 7–22

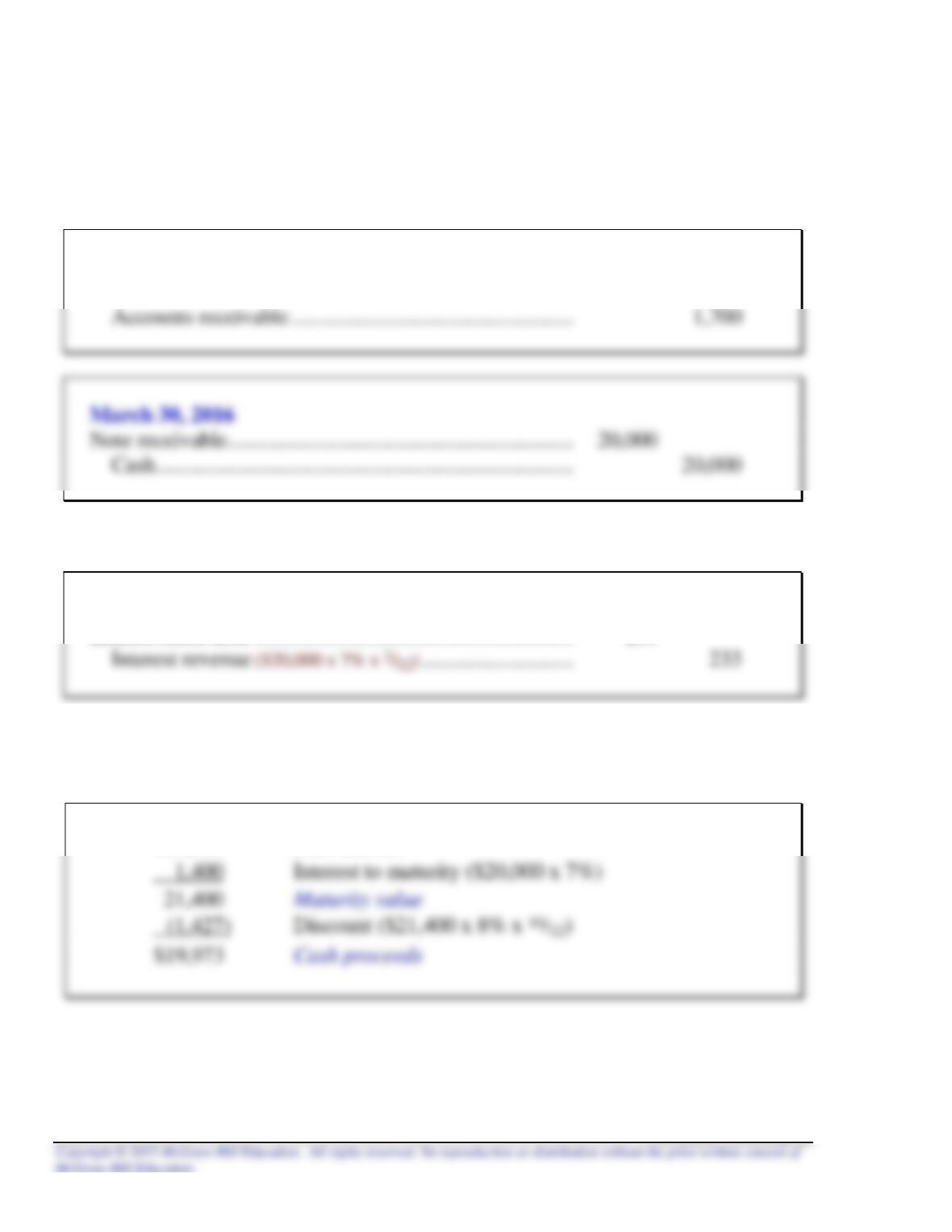

Step 1: Accrue interest earned.

February 28, 2016

Step 2: Add interest to maturity to calculate maturity value.

Step 3: Deduct discount to calculate cash proceeds.

$15,000 Face amount

Step 4: Record a loss for the difference between the cash proceeds and the

note’s book value.

February 28, 2016

Cash (proceeds determined above) …………………………………. 15,120

Exercise 7–23

List A List B

c 1. Internal control a. Restriction on cash.

7–34 Intermediate Accounting, 8/e

Exercise 7–24

Requirement 1

March 17, 2016

Allowance for uncollectible accounts ……………………….. 1,700

Step 1: Accrue interest earned for two months on note receivable.

May 30, 2016

Interest receivable ………………………………………………….. 233

Step 2: Add interest to maturity to calculate maturity value.

Step 3: Deduct discount to calculate cash proceeds.

$20,000 Face amount

Exercise 7–24 (continued)

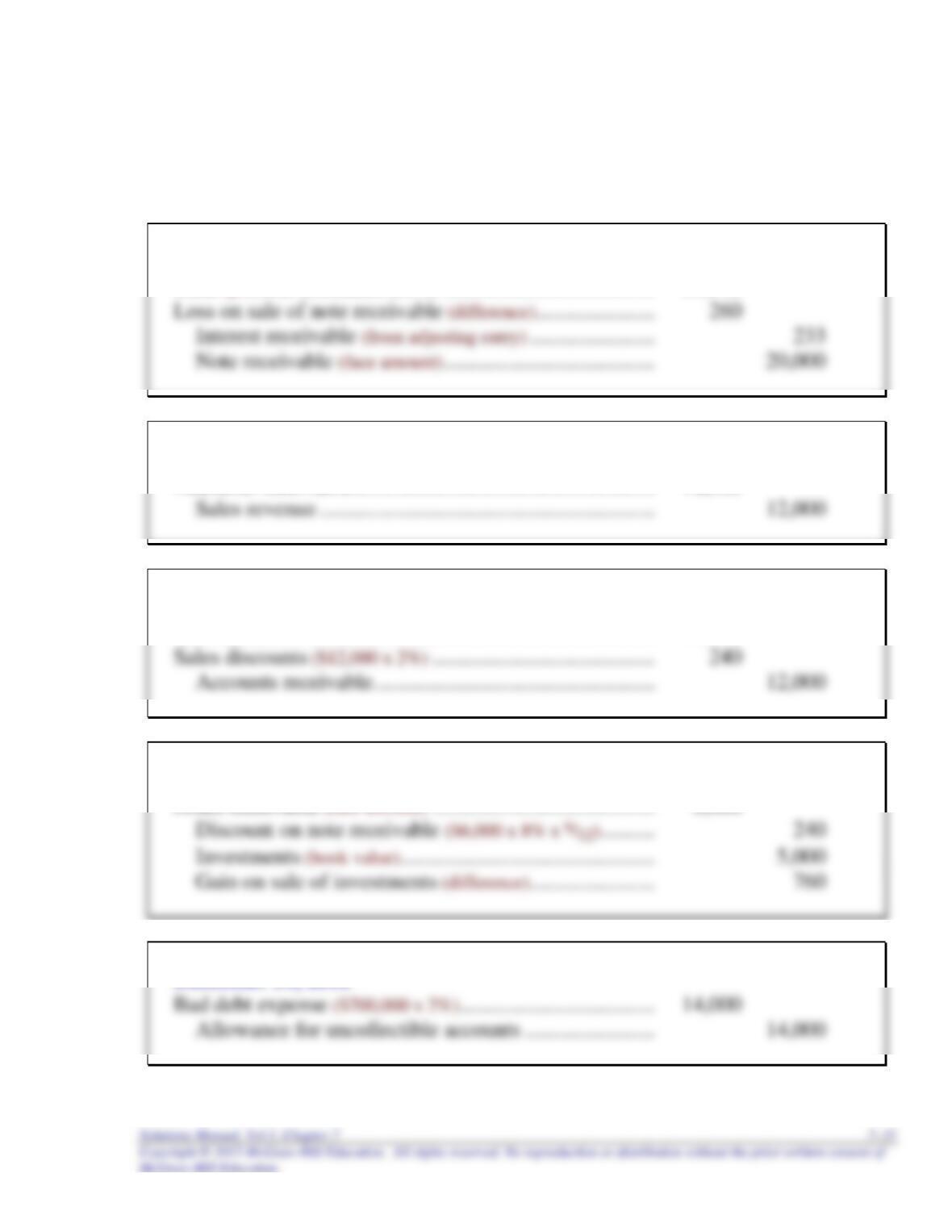

Step 4: Record a loss for the difference between the cash proceeds and the note’s book value.

May 30, 2016

Cash (proceeds determined above) ………………………………… 19,973

June 30, 2016

Accounts receivable ……………………………………………….. 12,000

July 8, 2016

Cash ($12,000 x 98%) ……………………………………………….. 11,760

August 31, 2016

December 31, 2016

7–36 Intermediate Accounting, 8/e

Exercise 7–24 (concluded)

Requirement 2

To accrue interest earned on note receivable:

December 31, 2016

Exercise 7–25

Second quarter:

Receivables turnover = $24,519 = 1.817 times

Exercise 7–26

Average collection period = 365 ÷ Accounts receivable turnover = 50 days

Accounts receivable turnover = 365 ÷ 50 = 7.3

Exercise 7–27

To establish the petty cash fund:

October 2, 2016

To replenish the petty cash fund:

October 31, 2016

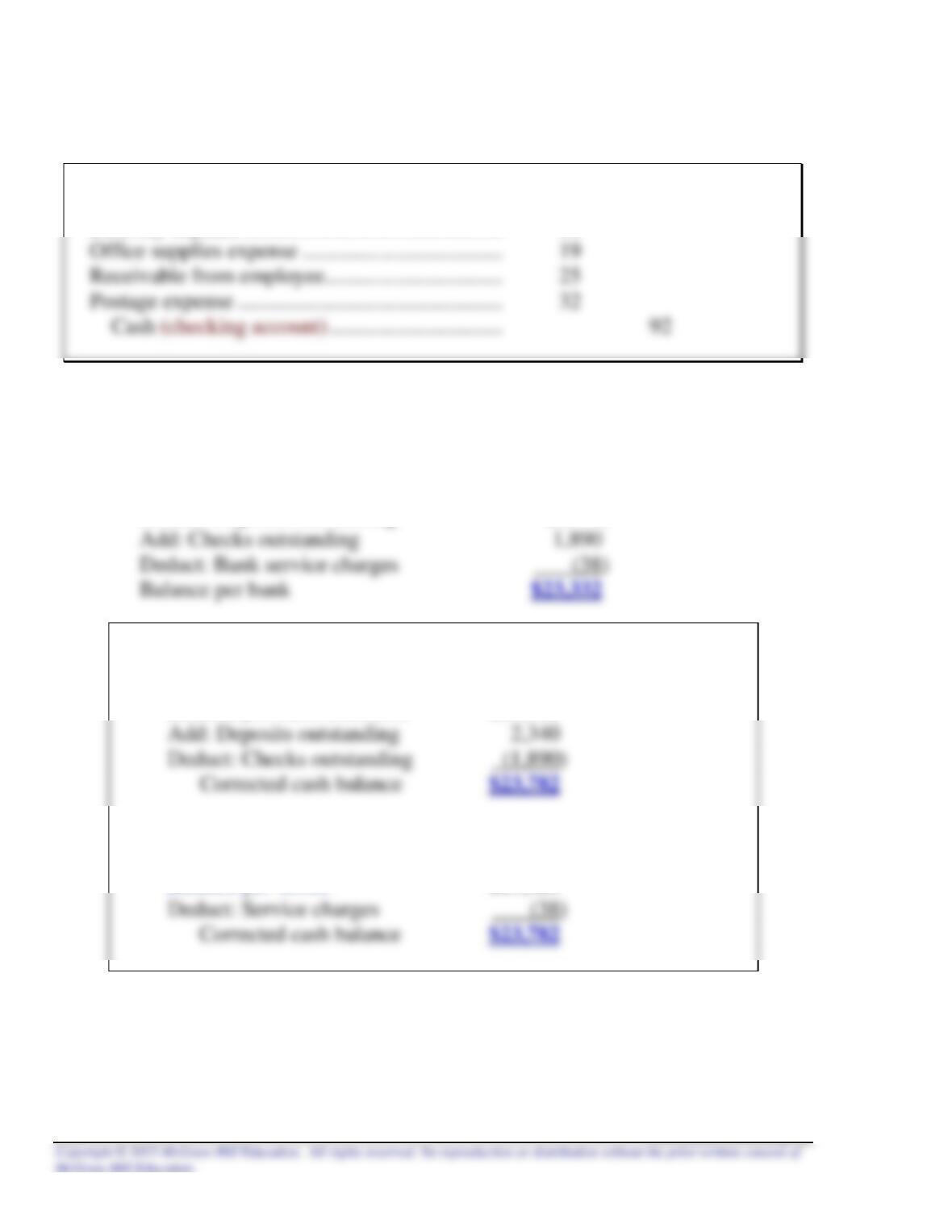

Office supplies expense …………………………..….. 76

7–38 Intermediate Accounting, 8/e

Exercise 7–28

September 30, 2016 To replenish the petty cash fund

Delivery expense ………………………………………… 16

Exercise 7–29

Compute balance per bank statement:

Balance per books $23,820

Deduct: Deposits outstanding (2,340)

Step 1: Bank Balance to Corrected Balance

Balance per bank statement $23,332

Step 2: Book Balance to Corrected Balance

Balance per books $23,820

Exercise 7–30

Requirement 1

Requirement 2

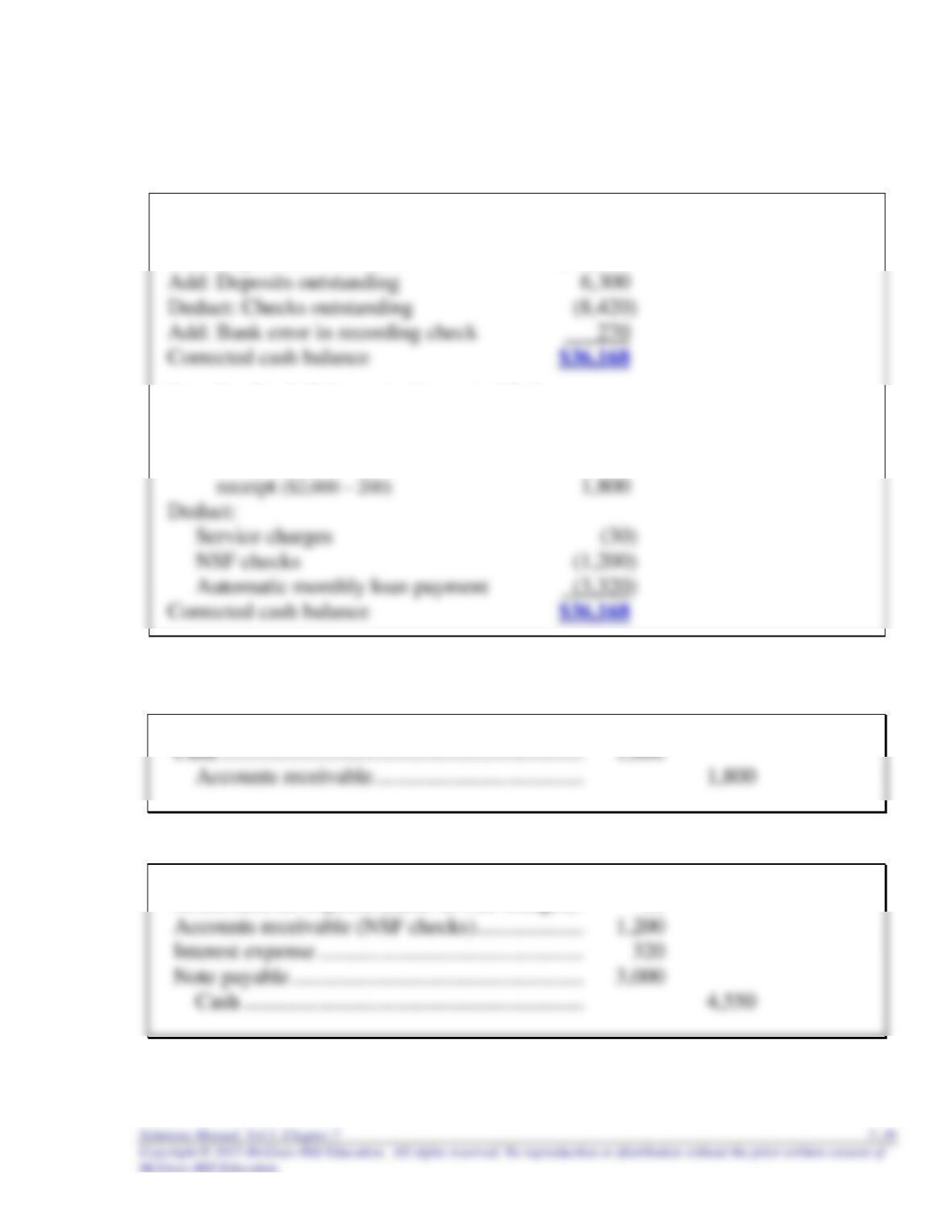

To correct error in recording cash receipt from credit customer:

To record credits to cash revealed by the bank reconciliation:

Miscellaneous expense (bank service charges) . 30

Note: Each of the adjustments to the book balance required journal entries.

None of the adjustments to the bank balance require entries.

Step 1: Bank Balance to Corrected Balance

Balance per bank statement $38,018

Step 2: Book Balance to Corrected Balance

Balance per books $38,918

Add: Error in recording cash

7–40 Intermediate Accounting, 8/e

Exercise 7–31

ANALYSIS

Previous Value:

Accrued 2015 interest (10% x $12,000,000) $ 1,200,000

Carrying amount of the receivable $13,200,000

New Value:

Interest $1 million x 1.73554 * = $1,735,540

Present value of the receivable (10,826,490)

Loss: $ 2,373,510

* present value of an ordinary annuity of $1: n = 2, i =10% (from Table 4)

JOURNAL ENTRIES

January 1, 2016

Loss on troubled debt restructuring (to balance) ……… 2,373,510

December 31, 2016

Cash (required by new agreement) …………….. ………… 1,000,000

December 31, 2017

Cash (required by new agreement) …………….. ………… 1,000,000