Question 10–1

Question 10–2

The cost of property, plant, and equipment and intangible assets includes the

Question 10–3

Question 10–4

Purchased intangibles are valued at their original cost to include the purchase

Chapter 10 Property, Plant, and Equipment and Intangible

Assets: Acquisition and Disposition

QUESTIONS FOR REVIEW OF KEY TOPICS

10–2 Intermediate Accounting, 8/e

Answers to Questions (continued)

Question 10–5

Goodwill represents the unique value of the company as a whole over and above

all identifiable tangible and intangible assets. This value results from a company’s

Question 10–6

A lump-sum purchase price generally is allocated based on the relative fair values

Question 10–7

Question 10–8

Answers to Questions (continued)

Question 10–10

When an item of property, plant, and equipment is sold, a gain or loss is

Question 10–11

Question 10–12

Question 10–13

GAAP require the capitalization of interest incurred during the construction of

Answers to Questions (continued)

Question 10–14

Average accumulated expenditures for a period is an approximation of the

average amount of debt the company would have had outstanding if it borrowed all of

Question 10–15

Applying the specific interest method, the interest rate on any construction-

Question 10–16

GAAP defines research and development as follows:

Research is planned search or critical investigation aimed at discovery of new

Question 10–17

GAAP specifically excludes from current R&D expense the cost of property,

Answers to Questions (continued)

Question 10–18

GAAP requires the capitalization of software development costs incurred after

technological feasibility is established. Technological feasibility is established “when

Question 10–19

The cost of developed technology is capitalized and expensed over its expected

useful life. Developed technology relates to those projects that have reached

Question 10–20

Under U.S. GAAP, donated assets are recorded as revenue. However, IAS No. 20

requires that government grants be recognized in income over the periods necessary to

10–6 Intermediate Accounting, 8/e

Answers to Questions (concluded)

Question 10–21

Other than software development costs incurred after technological feasibility has

Question 10–22

The periodic amortization percentage for capitalized computer software

Question 10–23

Brief Exercise 10–1

Capitalized cost of the machine:

Purchase price $35,000

Brief Exercise 10–2

Capitalized cost of land:

Purchase price $600,000

BRIEF EXERCISES

10–8 Intermediate Accounting, 8/e

Brief Exercise 10–3

Cost of land and building:

Purchase price $600,000

The total must be allocated to the land and building based on their relative fair

values:

Asset

Fair Value

Percent of Total

Fair Value

Initial

Valuation

(Percent x

$639,000)

Land

$420,000

60%

$383,400

Building

40

$700,000

100%

Brief Exercise 10–4

Cost of silver mine:

Acquisition, exploration, and development $5,600,000

Brief Exercise 10–5

After one year, the liability will increase to $455,456.

Brief Exercise 10–6

Calculation of goodwill:

Consideration exchanged $14,000,000

Brief Exercise 10–7

The initial value of equipment and note will be the present value of the note

payment:

PV = $60,000 (.85734* ) = $51,440

10–10 Intermediate Accounting, 8/e

Brief Exercise 10–8

Brief Exercise 10–9

Average PP&E for 2016 = ($740,000 + 940,000) ÷ 2 = $840,000

Brief Exercise 10–10

Proceeds $16,000

Less book value: Cost $80,000

Brief Exercise 10–11

Pickup trucks = Fair value of equipment plus cash paid

Brief Exercise 10–12

Pickup trucks = Fair value of equipment plus cash paid

10–12 Intermediate Accounting, 8/e

Brief Exercise 10–13

Brief Exercise 10–14

Average accumulated expenditures:

Interest capitalized:

* Weighted-average rate of all other debt:

10–14 Intermediate Accounting, 8/e

Brief Exercise 10–15

Average accumulated expenditures:

January 1, 2016 $500,000 x 12/12 = $ 500,000

Interest capitalized:

* Weighted-average rate of all other debt:

$ 700,000 x 7% = $ 49,000

Brief Exercise 10–16

Research and development:

Salaries $220,000

Exercise 10–1

Capitalized cost of land:

Purchase price $60,000

Capitalized cost of building:

Construction costs $500,000

Exercise 10–2

To record the purchase of equipment.

To record prepaid insurance for the equipment.

EXERCISES

10–16 Intermediate Accounting, 8/e

Exercise 10–3

Requirement 1

Cost of land and building:

Purchase price $4,000,000

Title search and insurance 16,000

Exercise 10–3 (concluded)

Requirement 2

Cost of land:

Purchase price $4,000,000

10–18 Intermediate Accounting, 8/e

Exercise 10–4

Requirement 1

Cost of copper mine:

Requirement 2

Copper mine (determined above) ………………………………. 1,903,939

Exercise 10–5

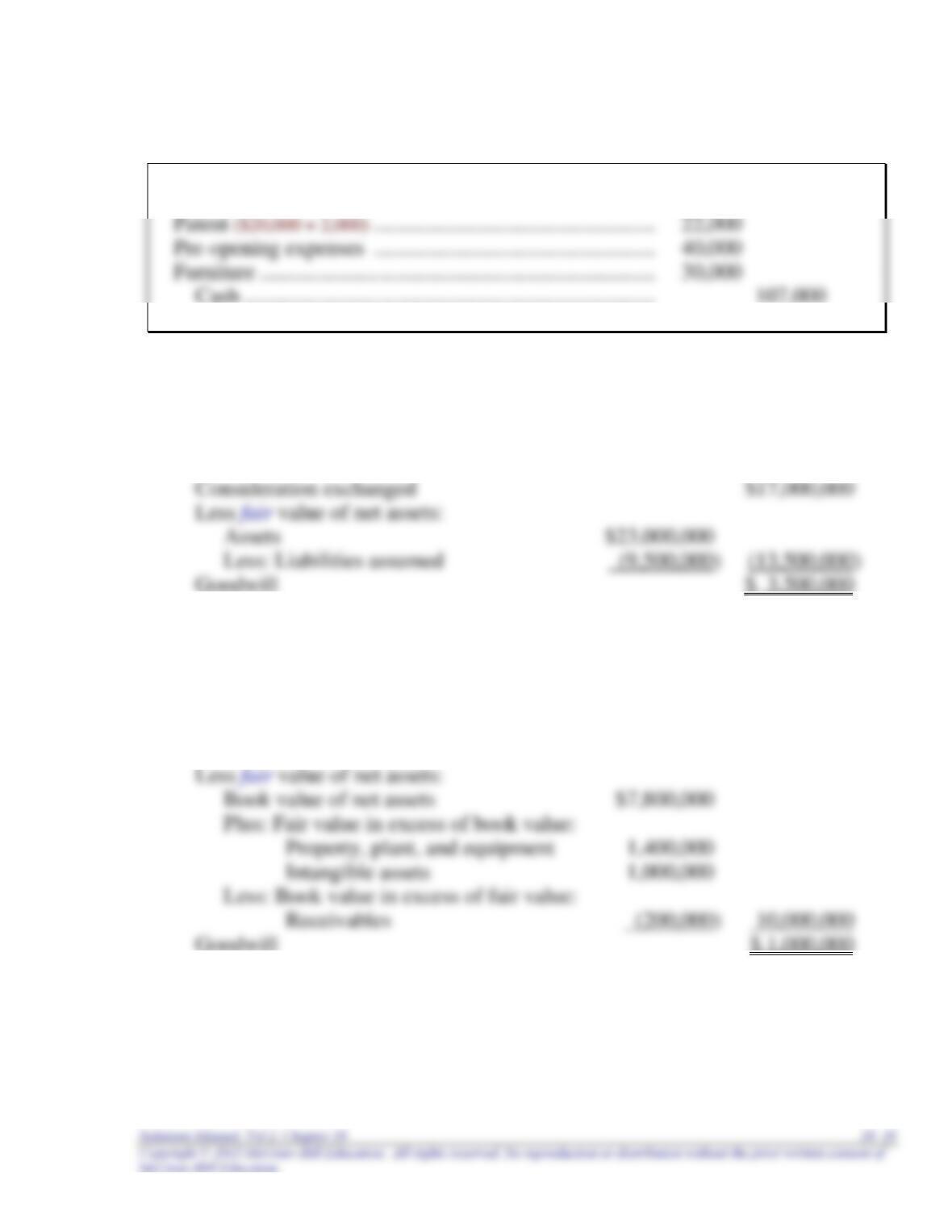

Organization cost expense ($12,000 + 3,000) ……………….. 15,000

Exercise 10–6

Calculation of goodwill:

Exercise 10–7

Calculation of goodwill:

Consideration exchanged $11,000,000

Exercise 10–8

Land ……………..

Building B …….

Percent of Total

Fair Value

Initial

Valuation

(Percent x

$900,000)