Exercise 10–30

Requirement 1

According to U.S. GAAP, the following costs would be expensed as R&D:

Requirement 2

10–42 Intermediate Accounting, 8/e

Exercise 10–31

Requirement 1

NXS should expense only the research expenditures:

Requirement 2

Exercise 10–32

List A List B

f 1. Depreciation a. Exclusive right to display a word, a symbol,

or an emblem.

Exercise 10–33

Requirement 1

Requirement 2

(1) Percentage-of-revenue method:

Exercise 10–34

Requirement 1

2016:

Requirement 2

(1) Percentage-of-revenue method:

(2) Straight-line method:

10–46 Intermediate Accounting, 8/e

Exercise 10–35

Requirement 1

Requirement 2

CPA / CMA REVIEW QUESTIONS

CPA Exam Questions

1. d. Simons Company should value the land at $170,500. All expenditures

3. d. There are eight payments due, the first one due immediately, and the

remaining seven due each year on December 31. Therefore, the correct

4. b. The recorded cost of the new asset is equal to the fair value of the asset

5. c. Dahl Corporation should capitalize the materials, engineering fees, and labor

10–48 Intermediate Accounting, 8/e

CPA Exam Questions (concluded)

6. b. The interest cost capitalized is the lesser of the formula amount based on

7. a. Amortization of capitalized software is the greater of the amount calculated

using the percentage–of-revenue method and the straight-line method. In

8. d. All of the expenditures are considered research and development.

CMA Exam Questions

1. a. The costs of fixed assets (plant and equipment) are all costs necessary to

acquire these assets and to bring them to the condition and location required

2. d. GAAP states that the basic principle to be followed in these exchanges is to

value the asset received at fair value and to recognize gain or loss (the

3. c. The answer is the same as question 2.

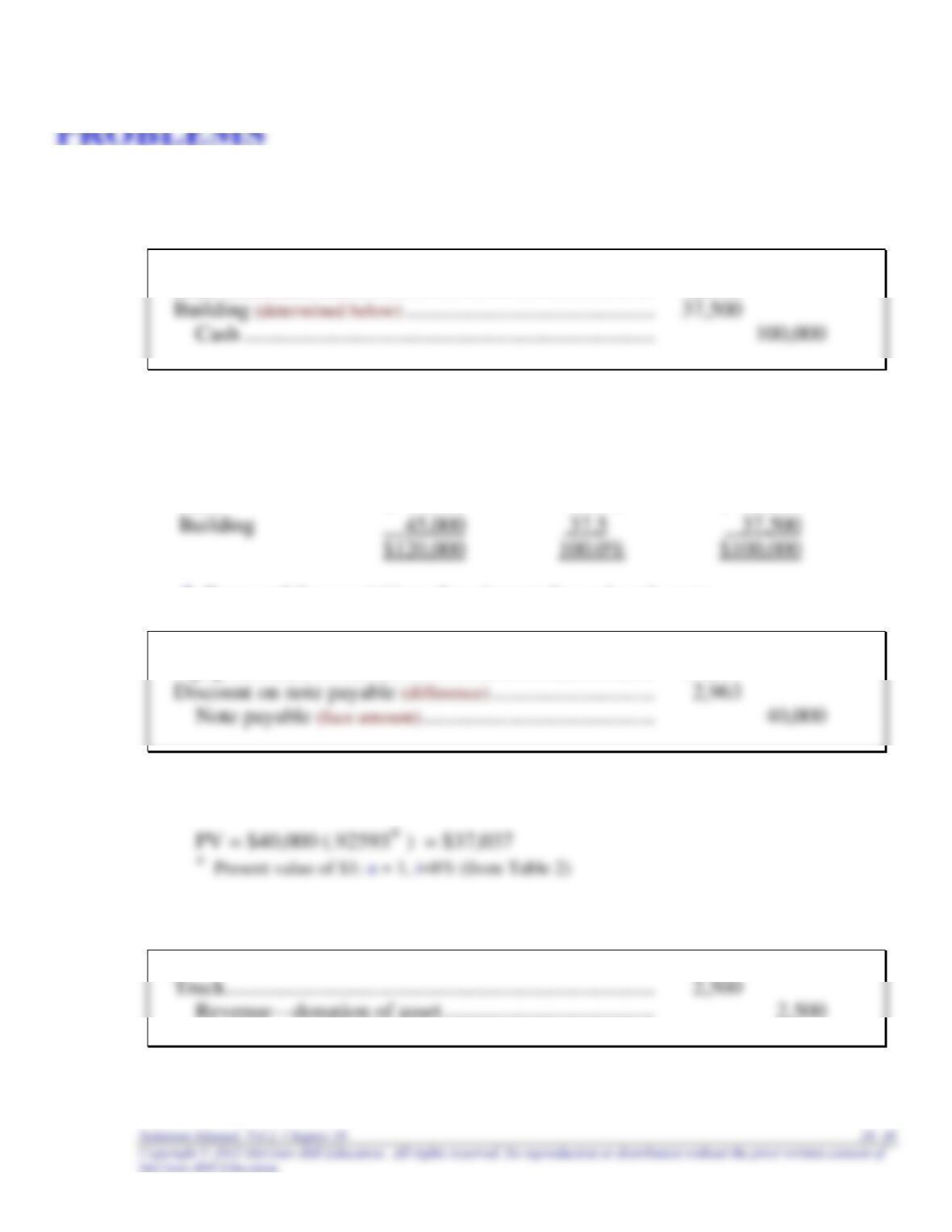

Problem 10–1

1. To record the acquisition of land and building.

Land (determined below) ……………………………………………………………… 62,500

Asset

Fair Value

Percent of Total

Fair Value

Initial

Valuation

(Percent x

$100,000)

Land

$ 75,000

62.5%

$ 62,500

Building

37.5

$120,000

100.0%

$100,000

2. To record the acquisition of equipment for cash and a note.

Equipment (determined below) ……………………………………. 37,037

Present value of note payments:

3. To record the acquisition of a truck by donation.

10–50 Intermediate Accounting, 8/e

Problem 10–1 (concluded)

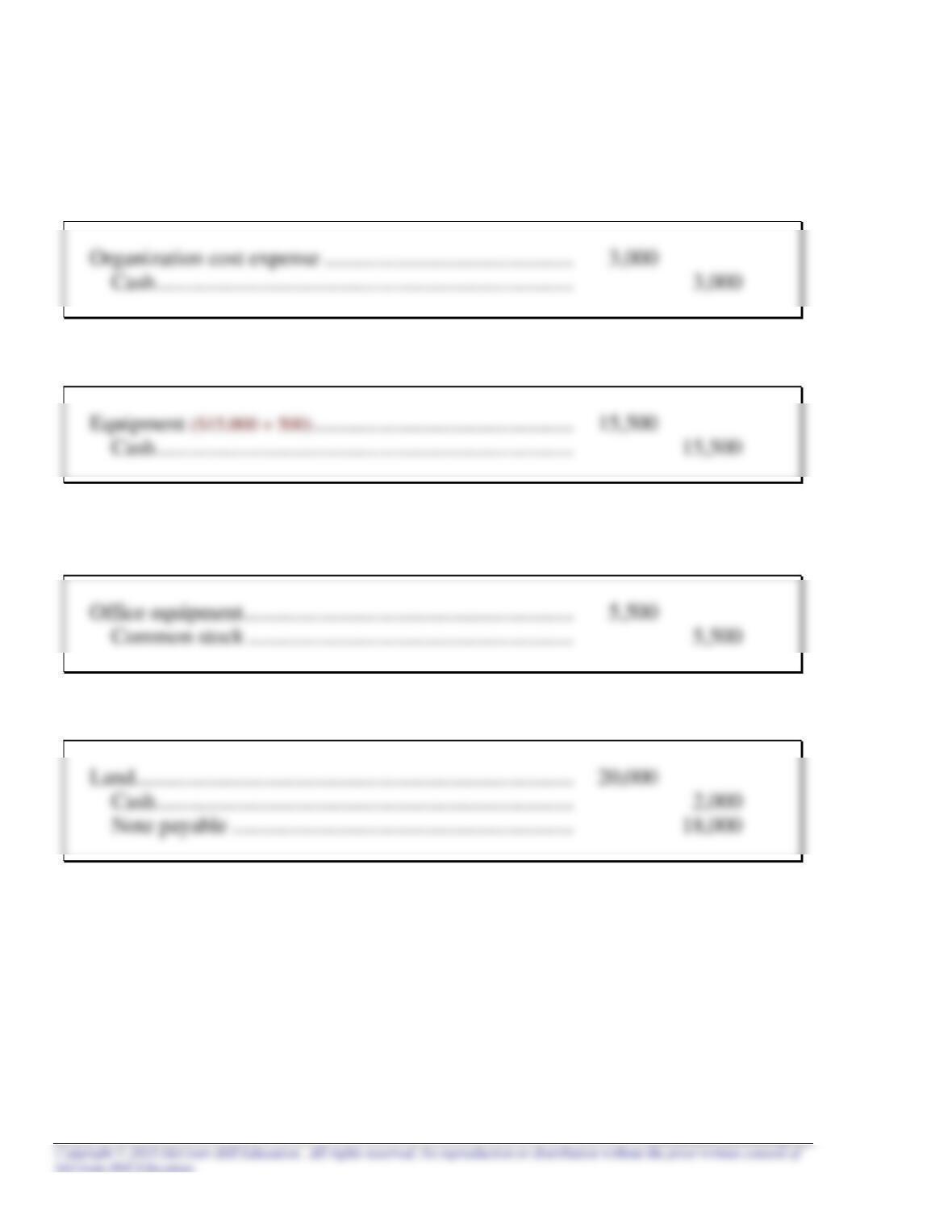

4. To capitalize organization costs.

5. To record the purchase of equipment.

6. To record the acquisition of office equipment by the issuance of common

stock.

7. To record the acquisition of land in exchange for cash and a note.

Problem 10–2

Requirement 1

BLACKSTONE CORPORATION

Land Account (Site Number 11)

As of September 30, 2017

Acquisition cost $600,000

Requirement 2

BLACKSTONE CORPORATION

Capitalized Cost of Office Building

As of September 30, 2017

Contract cost $3,000,000

Plans, specifications, and blueprints 12,000

10–52 Intermediate Accounting, 8/e

Problem 10–3

Requirement 1

PELL CORPORATION

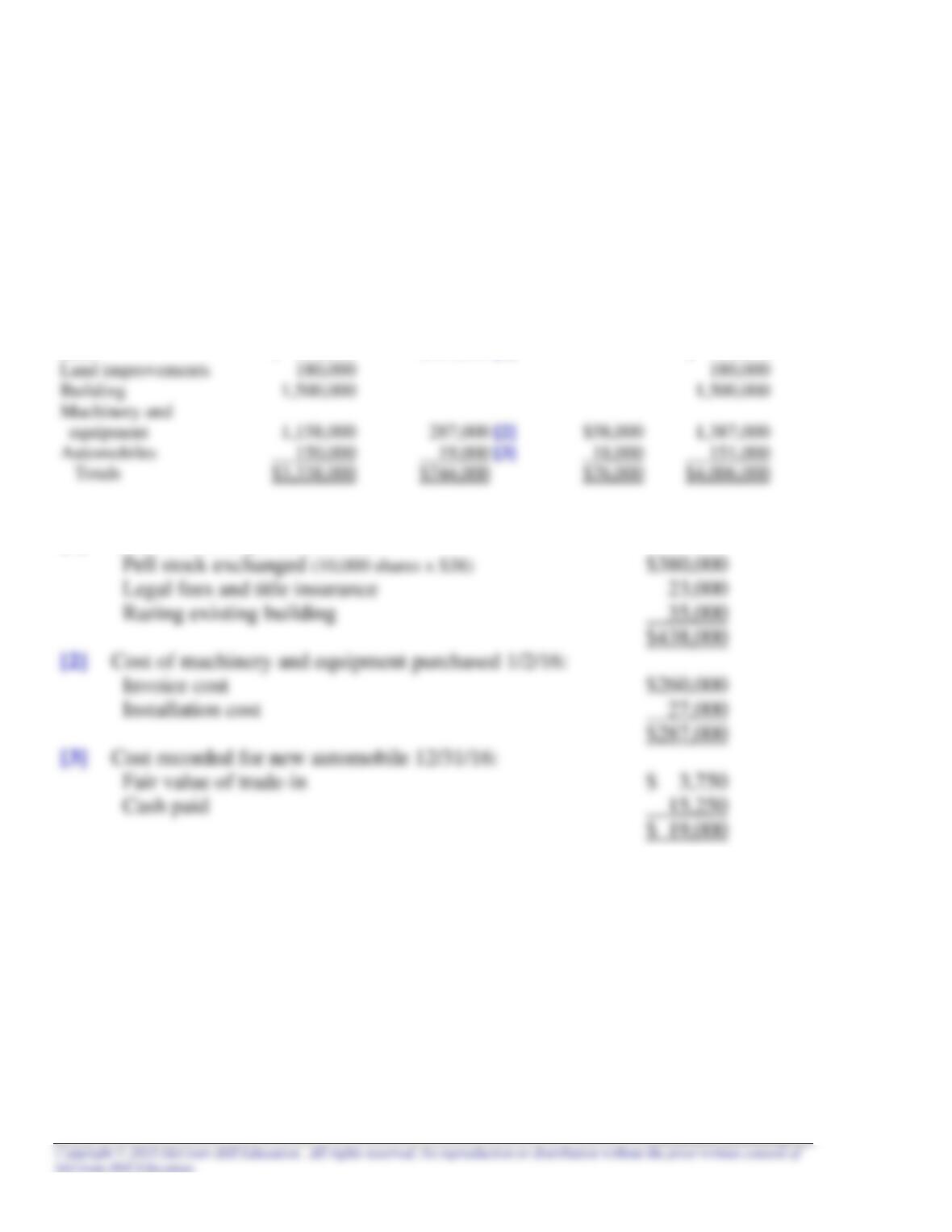

Analysis of Changes in Plant Assets

For the Year Ended December 31, 2016

Balance Balance

12/31/15 Increase Decrease 12/31/16

Land $ 350,000 $438,000 [1] $ 788,000

Explanation of Amounts:

[1] Cost of land acquired 11/1/16:

Problem 10–3 (concluded)

Requirement 2

Pell Corporation

Gain or Loss from Plant Asset Disposals

For the Year Ended December 31, 2016

Sale of machine on 3/31/16:

Selling price $36,500

10–54 Intermediate Accounting, 8/e

Problem 10–4

To reclassify various expenditures incorrectly charged to the intangible asset

account.

Organization cost expense ………………………………………. 7,000

Prepaid insurance …………………………………………………… 6,000

Problem 10–5

1. To expense R&D costs.

Research and development expense …………………………. 12,000

Cash …………………………………………………………………. 12,000

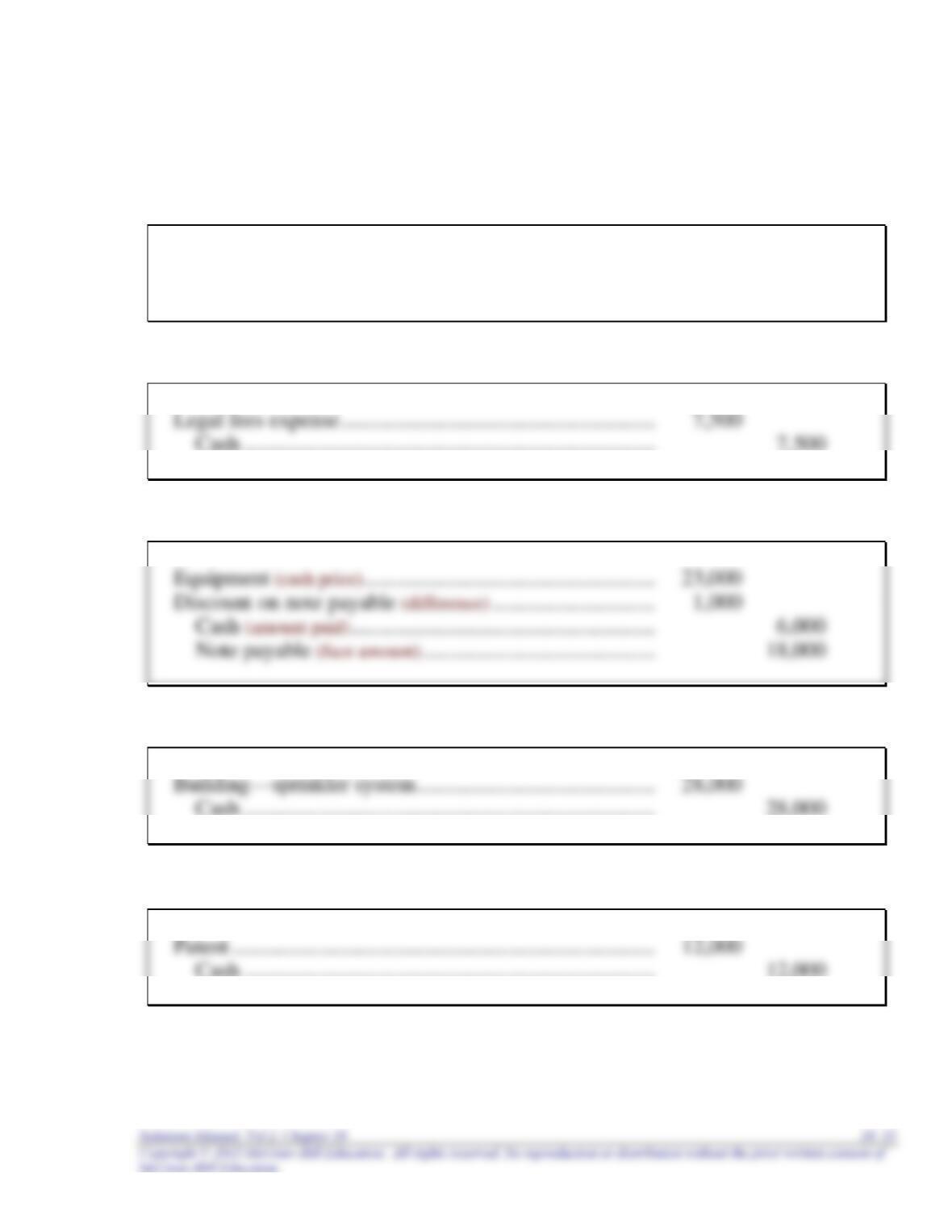

2. To expense legal fees for unsuccessful defense of patent.

3. To capitalize the cost of equipment.

4. To capitalize cost of the sprinkler system.

5. To capitalize legal fees for successful defense of patent.

10–56 Intermediate Accounting, 8/e

Problem 10–5 (concluded)

6. To record the trade-in of an old machine for a new machine.

Machine—new ($2,000* + 8,000) ……………………………….. 10,000

Problem 10–6

Southern Company:

Cash …………………………………………………………………….. 140,000

Eastern Company:

The fair value of Eastern’s building is $1,260,000 ($1,400,000 fair value of

Southern’s building less $140,000 cash given).

10–58 Intermediate Accounting, 8/e

Problem 10–7

Robers:

Cash ……………………………………………………………………… 5,000

Phifer:

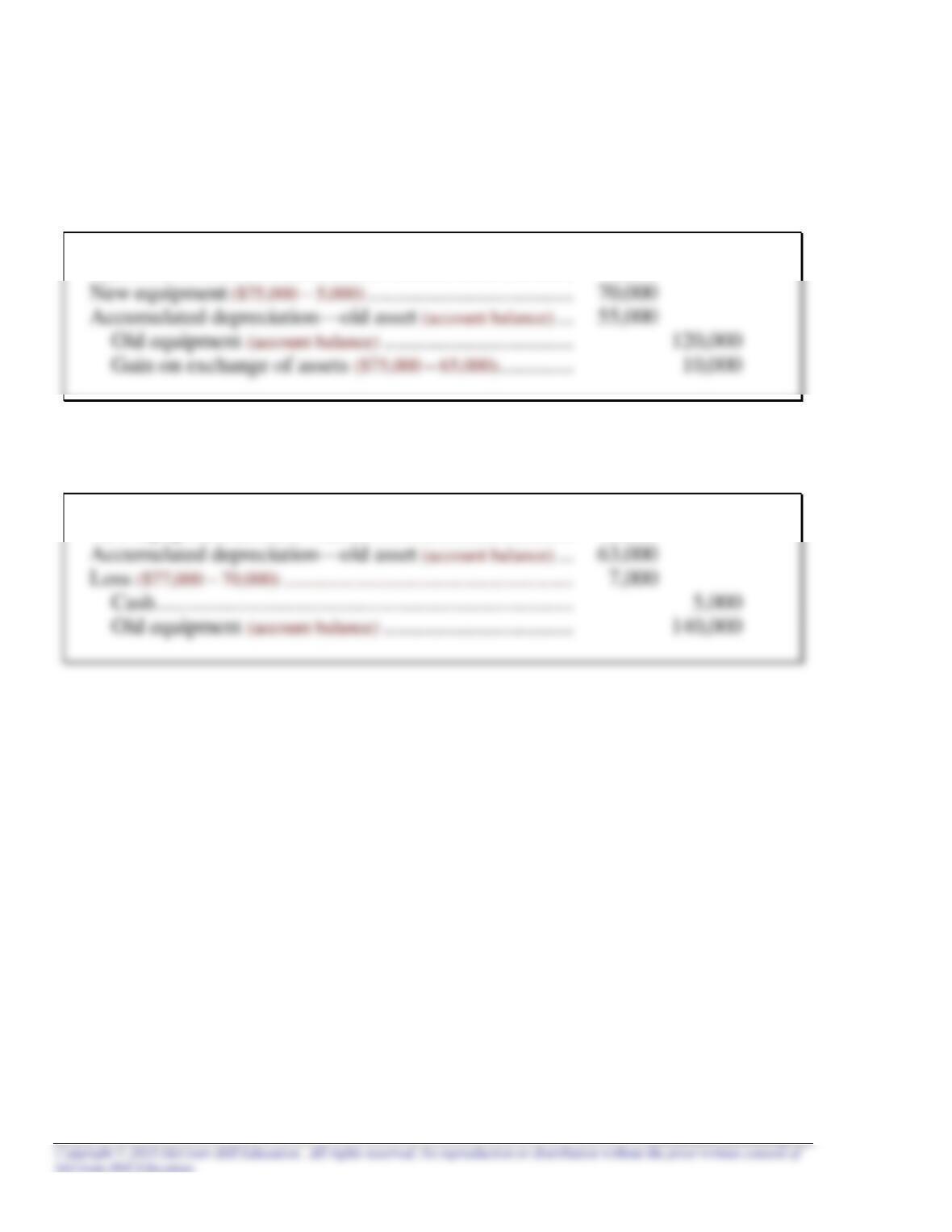

New equipment ($70,000 + 5,000) ………………………………. 75,000

Problem 10–8

Case A.

Requirement 1

Book value less fair value = loss on exchange

Requirement 2

Fair value less book value = gain on exchange

10–60 Intermediate Accounting, 8/e

Problem 10–8 (continued)

Case B.

Requirement 1

Fair value less book value = gain on exchange

Requirement 2