Exercise 8–6

Inventory balance before additional transactions $165,000

Add:

2. Goods shipped to Kwok f.o.b. shipping point on Dec. 28 17,000

Exercise 8–7

Inventory balance before additional transactions $210,000

Add:

4. Merchandise on consignment with Joclyn Corp. 15,000

Exercise 8–8

1. Excluded

3. Included

5. Included

7. Included

Exercise 8–9

Requirement 1

Purchase price = 1,000 units x $50 = $50,000

July 15, 2016

July 23, 2016

Requirement 2

August 15, 2016

Requirement 3

Exercise 8–10

Requirement 1

July 15, 2016

July 23, 2016

Requirement 2

August 15, 2016

Requirement 3

8–24 Intermediate Accounting, 8/e

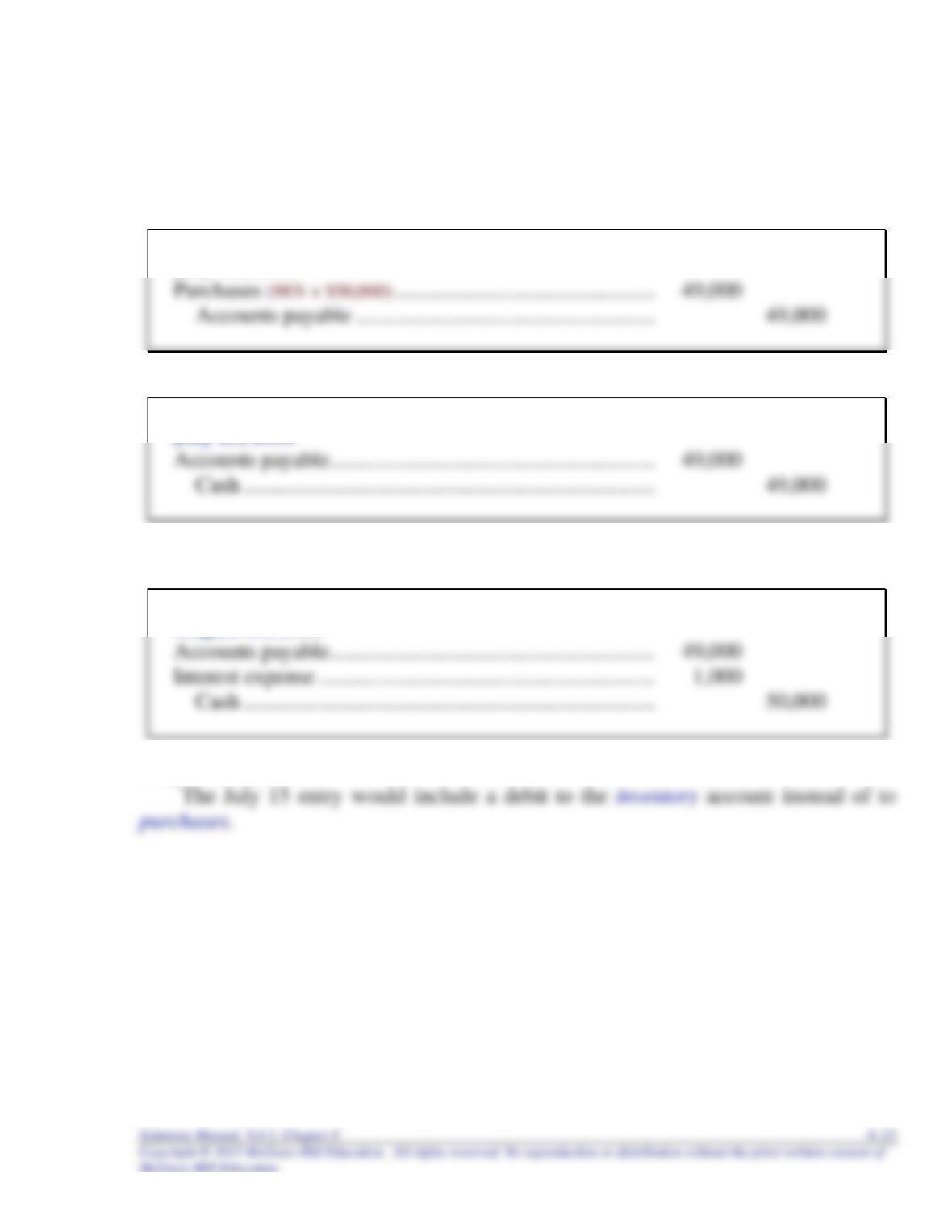

Exercise 8–11

Requirement 1

Purchases: $500 x 70% = $350 per unit.

100 units x $350 = $35,000

November 17, 2016

November 26, 2016

Accounts payable ………………………………………………….. 35,000

Requirement 2

December 15, 2016

Exercise 8–11 (concluded)

Requirement 3

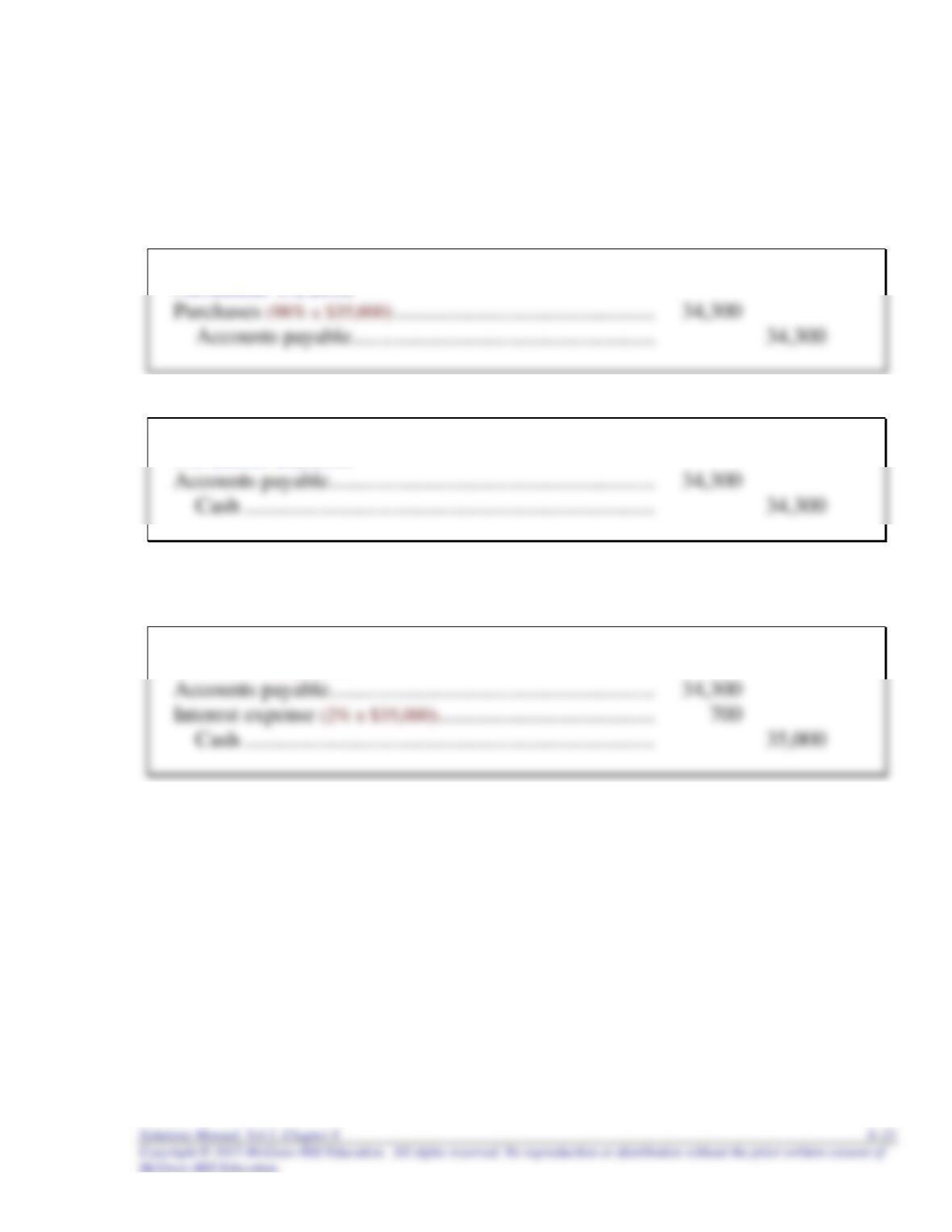

Requirement 1:

November 17, 2016

November 26, 2016

Requirement 2:

December 15, 2016

Exercise 8–12

The FASB Accounting Standards Codification® represents the single source

of authoritative U.S. generally accepted accounting principles. The specific

citation for each of the following items is:

1. Define the meaning of cost as it applies to the initial measurement of

inventory.

FASB ASC 330–10–30–1: “Inventory–Overall–Initial Measurement.”

The primary basis of accounting for inventories is cost, which has been

2. Indicate the circumstances when it is appropriate to initially measure

agricultural inventory at fair value.

FASB ASC 905–330–30–1: “Agriculture–Inventory–Initial

Measurement.”

Exceptional cases exist in which it is not practicable to determine an

appropriate cost basis for products. A market basis is acceptable if the

products meet all of the following criteria:

Exercise 8–12 (concluded)

3. What is a major objective of accounting for inventory?

4. Are abnormal freight charges included in the cost of inventory?

8–28 Intermediate Accounting, 8/e

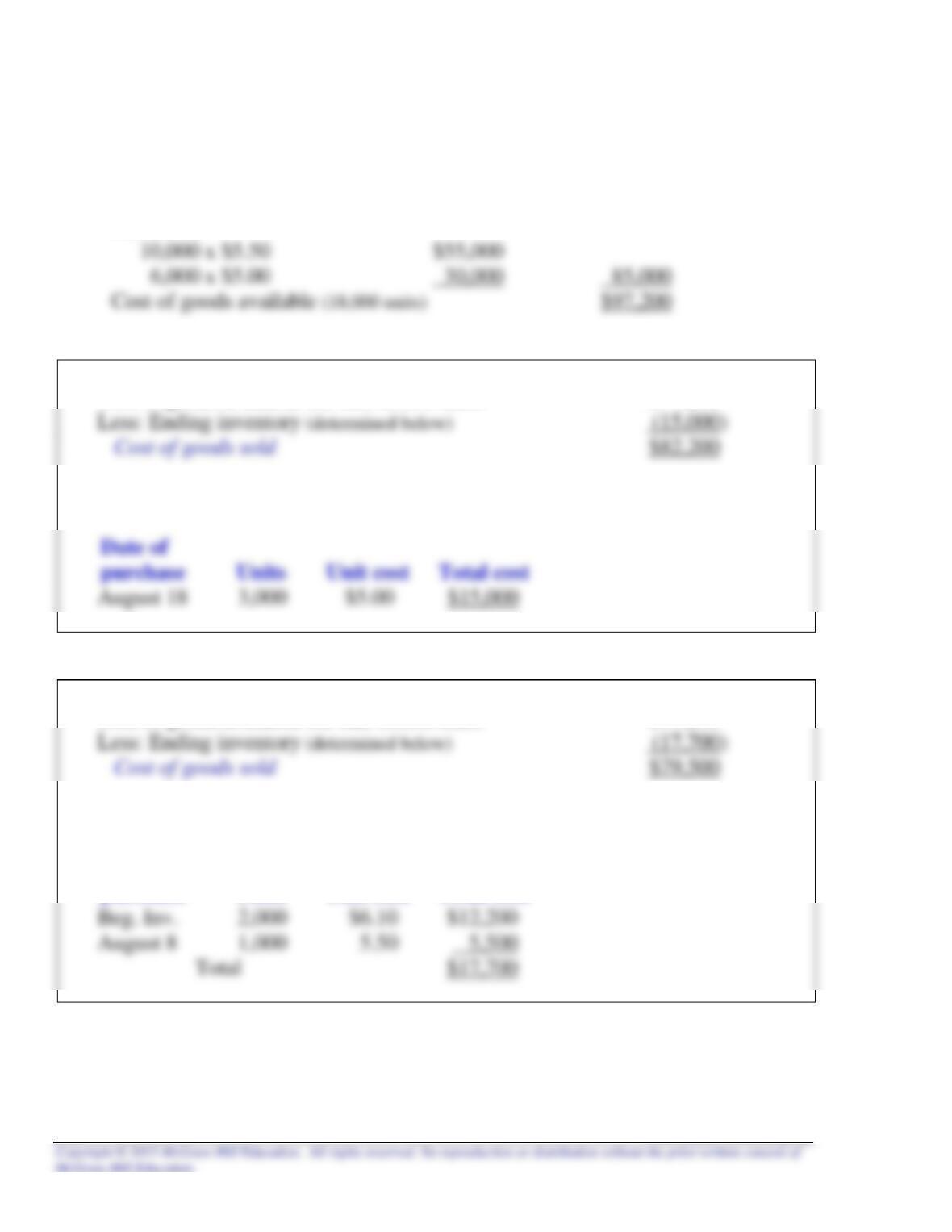

Exercise 8–13

Cost of goods available for sale:

Beginning inventory (2,000 x $6.10) $12,200

Purchases:

First-in, first-out (FIFO)

Cost of goods available for sale (18,000 units) $97,200

Cost of ending inventory:

Last-in, first-out (LIFO)

Cost of goods available for sale (18,000 units) $97,200

Cost of ending inventory:

Date of

purchase Units Unit cost Total cost

Exercise 8–13 (concluded)

Average cost

Cost of goods available for sale (18,000 units) $97,200

Less: Ending inventory (determined below) (16,200)

Cost of goods sold $81,000 *

8–30 Intermediate Accounting, 8/e

Exercise 8–14

First-in, first-out (FIFO)

Cost of goods sold:

Date of Cost of

Sale Units Sold Units Sold Total Cost

Aug. 14 2,000 (from Beg. Inv.) $6.10 $12,200

Last-in, first-out (LIFO)

Date

Purchased

Sold

Balance

Beginning

inventory

2,000 @ $6.10 = $12,200

2,000 @ $6.10 $12,200

Exercise 8–14 (concluded)

(Note: the perpetual inventory LIFO results in this exercise are the same as

periodic LIFO results, due to the timing of sales and purchases. The same LIFO

layers are on hand at the end of the period under each method. This is unusual. LIFO

perpetual and LIFO periodic normally produce different results for ending inventory

and cost of goods sold.)

Average cost

Date

Purchased

Sold

Balance

Beginning

inventory

2,000 @ $6.10 = $12,200

2,000 @ $6.10 $12,200

August 14

4,000 @ $5.60 $22,400

8–32 Intermediate Accounting, 8/e

Exercise 8–15

Requirement 1

LIFO will result in the highest cost of goods sold figure because both the cost of

merchandise and the quantity of merchandise rose during the period. FIFO will result

in the highest ending inventory balance for the same reasons.

Requirement 2

Cost of goods available for sale:

Beginning inventory (600 x $80) $ 48,000

Purchases:

First-in, first-out (FIFO)

Cost of goods available for sale (2,400 units) $223,000

Less: Ending inventory (below) (80,000)

Cost of goods sold $143,000

Cost of ending inventory:

Last-in, first-out (LIFO)

Cost of goods available for sale (2,400 units) $223,000

Cost of ending inventory:

Date of

purchase Units Unit cost Total cost

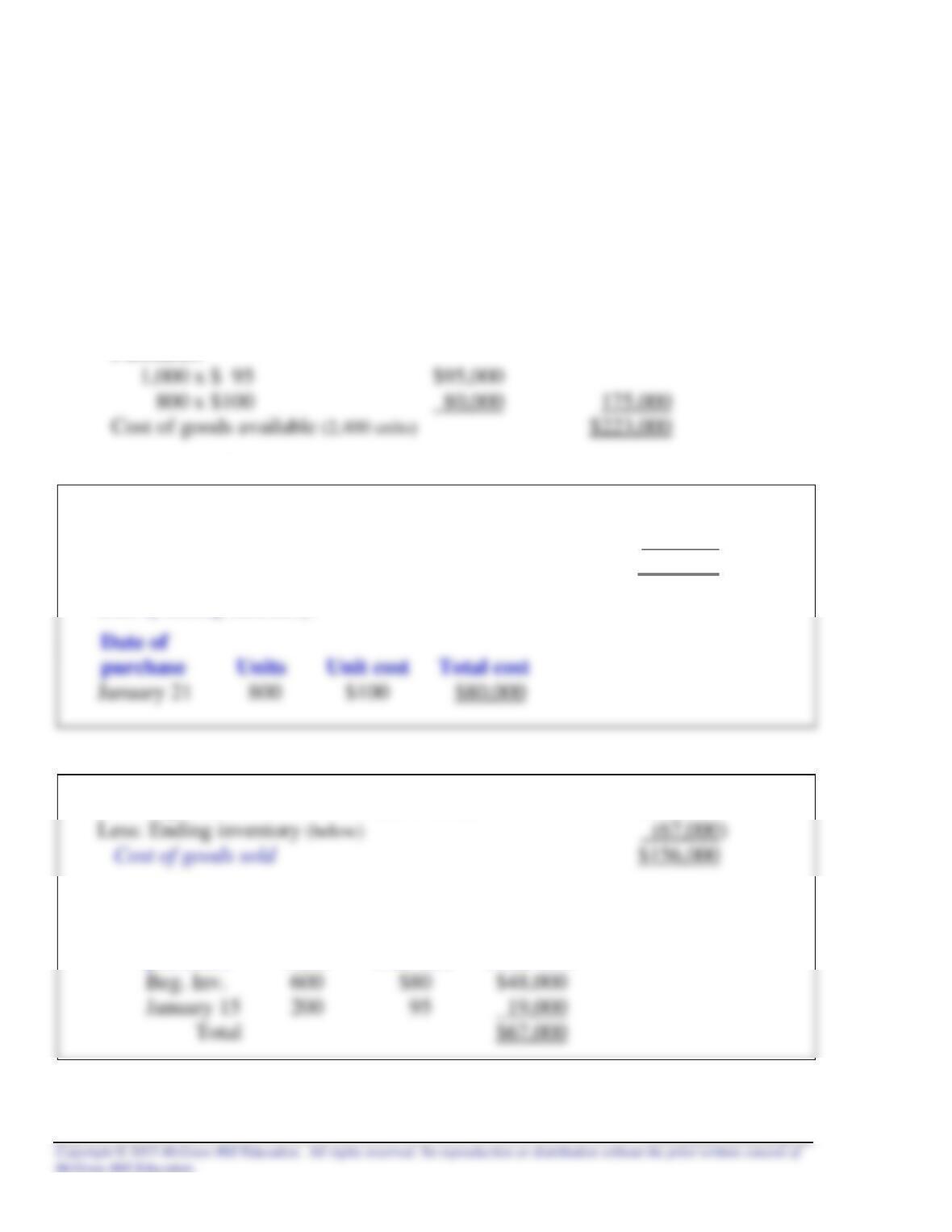

Exercise 8–16

Requirement 1

Cost of goods available for sale:

Beginning inventory (5,000 x $10.00) $ 50,000

Purchases:

Cost of goods available for sale (16,000 units) $167,200

Cost of ending inventory:

8–34 Intermediate Accounting, 8/e

Exercise 8–16 (concluded)

Requirement 2

Date

Purchased

Sold

Balance

Beginning

inventory

5,000 @ $10.00 = $50,000

5,000 @ $10.00 $50,000

September 10

4,000 @ $10.15 = $40,600

4,000 @ $10.15 $40,600

September 25

8,000 @ $10.75 = $86,000

Exercise 8–17

Requirement 1

FIFO cost of goods sold:

Requirement 2

LIFO cost of goods sold:

Calculations to determine cost per unit of year 2016 purchases:

Cost of goods sold

= Weighted-average cost per unit

Number of units sold

Cost of goods available for sale:

Beginning inventory (10,000 x $5.00) $ 50,000

Purchases (30,000 x $6.00) 180,000

Cost of goods available (40,000 units) $230,000

Exercise 8–18

Requirement 1

January 31, 2014 ($ in thousands)

Requirement 2

Exercise 8–19

Requirement 1

Cost of goods sold:

50,000 units x $8.50 = $425,000

Requirement 2

When inventory quantity declines during a reporting period, liquidation of LIFO

inventory layers carried at different costs prevailing in prior year’s results in

8–38 Intermediate Accounting, 8/e

Exercise 8–20

Units liquidated 10,000

Units liquidated multiplied by the difference between

their current cost and acquisition cost:

8,000 x ($12 – 9) = $24,000

Exercise 8–21

Requirement 2

Requirement 3

When a company using LIFO liquidates a substantial portion of its LIFO

inventory and as a result includes a material amount of income in its income statement

Exercise 8–22

($ in millions)

HOME DEPOT LOWE’S

Gross profit ratio = 27,390 = 34.8% 18,476 = 34.6%

78,812 53,417

Exercise 8–23

Ending

Ending Inventory Inventory Layers Inventory Layers Inventory

Date at Base Year Cost at Base Year Cost Converted to Cost DVL Cost

1/1/16 $660,000

= $660,000 $660,000 (base) $660,000 x 1.00 = $660,000 $660,000

1.00

8–40 Intermediate Accounting, 8/e

Exercise 8–24

Ending

Ending Inventory Inventory Layers Inventory Layers Inventory

Date at Base Year Cost at Base Year Cost Converted to Cost DVL Cost

12/31/16 $200,000

= $200,000 $200,000 (base) $200,000 x 1.00 = $200,000 $200,000

1.00