Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

ASSIGNMENT OF ACCOUNTS RECEIVABLE

(continued)

In Santa Teresa’s December 31, 2016, balance sheet, the receivables and

note payable would be reported together as follows:

T7-13 (continued)

7-22 Intermediate Accounting, 8/e

ACCOUNTS RECEIVABLE FACTORED WITHOUT RECOURSE

The buyer assumes the risk of uncollectibility when accounts

receivable are factored without recourse. The seller accounts

for the transaction as a sale.

In December 2016, the Santa Teresa Glass Company factored accounts

receivable that had a book value of $600,000 to Factor Bank. The transfer

was made without recourse. Under this arrangement, Santa Teresa

transfers the $600,000 of receivables to Factor, and Factor immediately

remits to Santa Teresa cash equal to 90% of the factored amount (90% x

$600,000 = $540,000). Factor retains the remaining 10% to cover its

Illustration 7-17

T7-14

ACCOUNTS RECEIVABLE FACTORED WITH RECOURSE —

SALE CONDITIONS MET

If certain conditions are met, factoring with recourse is

accounted for as a sale of the receivables; otherwise, it is

accounted for as a borrowing.

If accounted for as a sale, the only difference in accounting

In Illustration 7-17, assuming that the fair value of the recourse

obligation is estimated to be $5,000, the transfer is accounted for as

follows:

Illustration 7-18

T7-15

7-24 Intermediate Accounting, 8/e

DISCOUNTING A NOTE RECEIVABLE

The transfer of a note receivable to a financial institution is

called discounting. Similar to accounts receivable, if certain

conditions are met, the transfer is accounted for as a sale;

otherwise as a borrowing.

On December 31, 2016, the Stridewell Wholesale Shoe Company sold

land in exchange for a nine-month, 10% note. The note requires the

payment of $200,000 plus interest on September 30, 2017. The

company’s fiscal year-end is December 31. The 10% rate properly

reflects the time value of money for this type of note. On March 31,

2017, Stridewell discounted the note at the Bank of the East. The Bank’s

discount rate is 12%.

Because the note has been outstanding for three months before being

discounted at the bank, Stridewell first records the interest that has

accrued prior to being discounted:

Illustration 7-19

T7-16

DISCOUNTING A NOTE RECEIVABLE

(continued)

Discounted Note Treated as a Sale

Cash (proceeds determined above) ......................... 202,100

T7-16 (continued)

7-26 Intermediate Accounting, 8/e

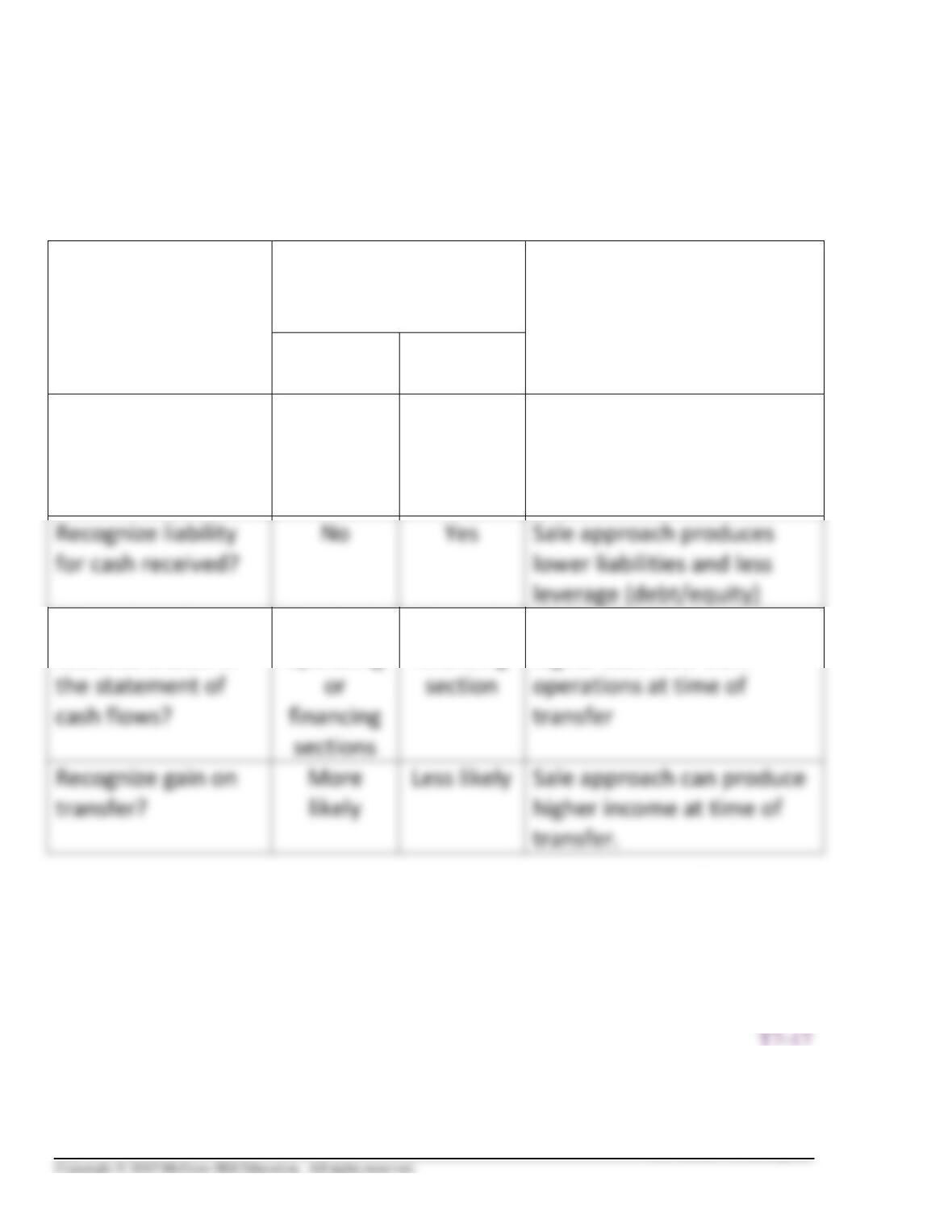

Do Transferors Typically Prefer Sales or

Secured-Borrowing Treatment? Sales!

Does the

Accounting

Approach:

Transfer of

Receivables

Accounted for as a:

Why Sales Approach is

Preferred by the

Transferor:

Sale

Secured

Borrowing

Derecognize A/R,

reducing assets?

Yes

No

Sale approach produces

lower total assets and

higher return on assets

(ROA)

Where is cash

received shown in

May be in

operating

Always in

financing

Sale approach can produce

higher cash flow from

Illustration 7-21

When Can a Transfer be Treated as a Sale?

Key – the transferor must have surrendered control of the

receivables, which occurs if and only if:

A.

The transferred assets have been isolated from the

transferor—beyond the reach of the transferor and its

creditors.

T7-18

7-28 Intermediate Accounting, 8/e

FINANCING WITH RECEIVABLES – A SUMMARY

Financing with Receivables

Is the arrangement a transfer

of specific receivables or

Transfer

Pledging

Does the transfer meet the three

conditions for treatment as a sale?

Yes

No

Record as a Sale:

Record as a secured borrowing:

Disclose arrangement in debt

Illustration 7-23

INTERNATIONAL FINANCIAL REPORTING STANDARDS

Transfers of Receivables. The international and U.S. guidance often lead to

similar accounting. Both seek to determine whether an arrangement should be treated

as a secured borrowing or a sale, and, having concluded which approach is

appropriate, both account for the approaches in a similar fashion. Also, the recent

change in U.S. GAAP that eliminated the concept of QSPEs is a step towards

convergence with IFRS, and is likely to reduce the proportion of U.S. securitizations

that qualify for sale accounting.

Where IFRS and U.S. GAAP most differ is in the conceptual basis for their choice

of accounting approaches and in the decision process they require to determine which

approach to use. Under IFRS:

1. If the company transfers substantially all of the risks and rewards of

ownership, the transfer is treated as a sale.

T 7-20

7-30 Intermediate Accounting, 8/e

DECISION MAKERS’ PERSPECTIVE

➢ A company's investment in receivables is influenced by

several variables, including the level of sales, the nature of the

product or service sold, and credit and collection policies.

➢ Management must evaluate the costs and benefits of any

change in credit and collection policies.

➢ The two ratios designed to monitor receivables are:

the receivables turnover ratio, and

Receivables turnover ratio = Net sales

Average accounts receivable (net)

Average collection period = 365

Receivables turnover ratio

T7-21

BANK RECONCILIATION —

RECONCILING ITEMS

Step 1: Adjustments to Bank Balance:

1. Add deposits outstanding. These represent cash received by the company and

debited to cash that have not been deposited in the bank by the bank statement

Step 2: Adjustments to Book Balance:

1. Add collections made by the bank on the company’s behalf and other increases

in cash that the company is unaware of until the bank statement is received.

Illustration 7–A1

T7-22

7-32 Intermediate Accounting, 8/e

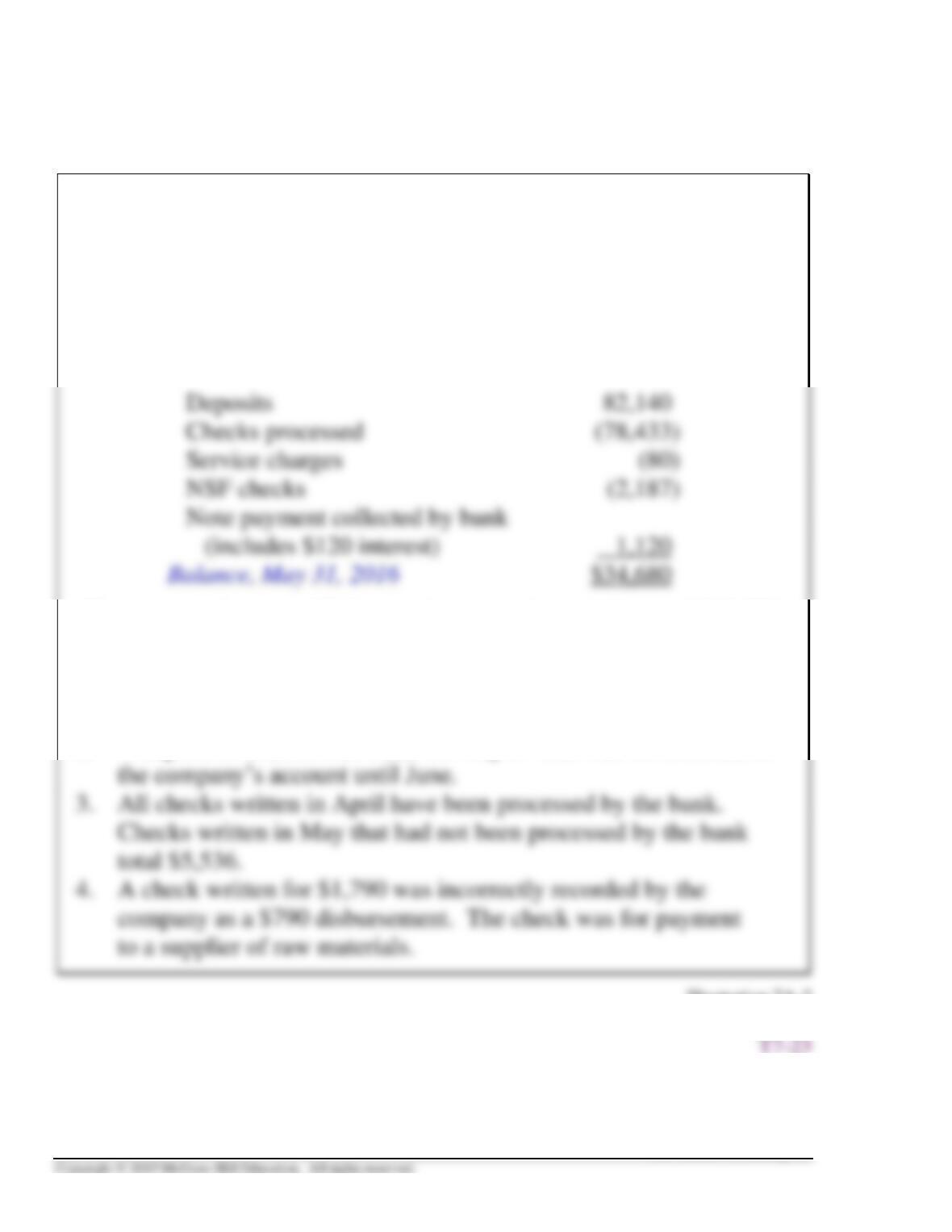

BANK RECONCILIATION

The Hawthorne Manufacturing Company maintains a general checking

account at the First Pacific Bank. First Pacific provides a bank statement

and canceled checks once a month. The cutoff date is the last day of the

month. The bank statement for the month of May is summarized as

follows:

Balance, May 1, 2016 $32,120

The company’s general ledger cash account has a balance of $35,276 at

the end of May. A review of the company records and the bank statement

reveals the following:

1. Cash receipts not yet deposited totaled $2,965.

2. A deposit of $1,020 was made on May 31 that was not credited to

Illustration 7A-2

BANK RECONCILIATION

(continued)

Step 1: Bank Balance to Corrected Balance

Balance per bank statement $34,680

Add: Deposits outstanding 3,985 *

Step 2: Book Balance to Corrected Balance

Balance per books $35,276

Add: Note collected by bank 1,120

Deduct:

Cash ........................................................................ 1,120

Miscellaneous expense (bank service charges) ........... 80

T7-23 (continued)

7-34 Intermediate Accounting, 8/e

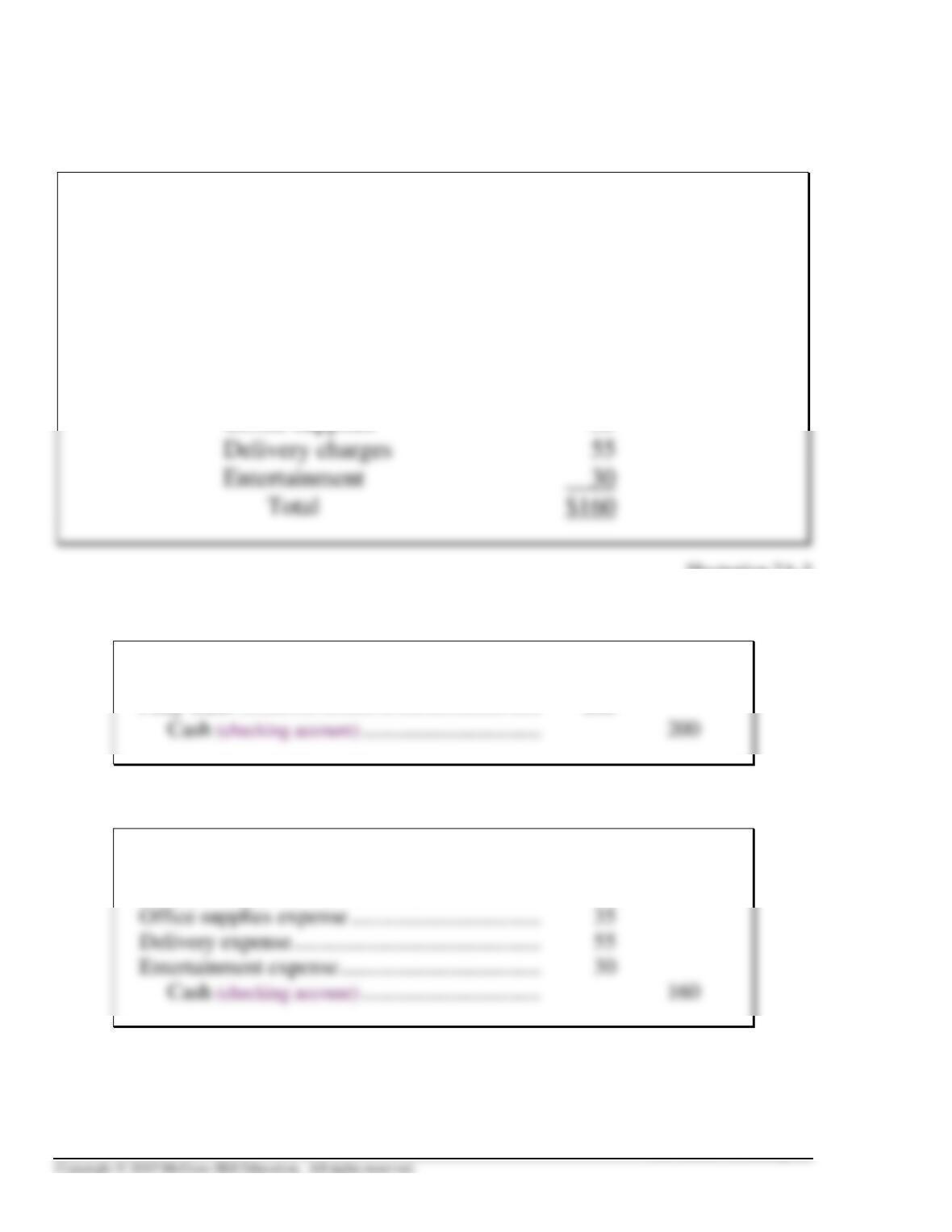

PETTY CASH

On May 1, 2016, the Hawthorne Manufacturing Company established a

$200 petty cash fund. John Ringo is designated as the petty cash

custodian. The fund will be replenished at the end of each month. On

May 1, 2016, a check is written for $200 made out to John Ringo, petty

cash custodian. During the month of May, John paid bills totaling $160

summarized as follows:

Postage $ 40

Office supplies 35

Illustration 7A-3

When the petty cash fund is established

May 1, 2016

Petty Cash ........................................................ 200

When the petty cash fund is reimbursed

May 31, 2016

Postage expense ............................................... 40

T7-24