Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Problem 15-15 (continued)

Not required in the problem, but helpful to see that the present value calculation

is precisely the reverse of the lessor’s calculation of quarterly payments:

Amount to be recovered (fair value) $26,427

Requirement 2

September 30, 2016

Anything Grows (Lessee)

Leased equipment .......................................................... 26,427

Lease payable (present value of minimum lease payments) 26,427

15–122 Intermediate Accounting, 8/e

Problem 15-15 (continued)

Requirement 3

Since both use the same discount rate, the amortization schedule for the lessee and

lessor is the same:

Lease Amortization Schedule

Effective Decrease Outstanding

Date Payments Interest in Balance Balance

3% x Outstanding Balance

9/30/16 26,427

9/30/16 3,000 3,000 23,427

Problem 15-15 (concluded)

Requirement 4

December 31, 2016

Anything Grows (Lessee)

Depreciation expense ([$26,427 ÷ 4 years*] x 1/4 year) .......... 1,652

Requirement 5

September 29, 2018

Anything Grows (Lessee)

Depreciation expense ([$26,427 ÷ 4 years*] x 3/4 year) ......... 4,955

Accumulated depreciation .......................................... 4,955

15–124 Intermediate Accounting, 8/e

Problem 15-16

Requirement 1

Since at least one (exactly one in this case) criterion is met, this is a capital lease

to the lessee:

Lessee’s Application of Classification Criteria

1 Does the agreement specify that

ownership of the asset transfers

to the lessee? NO

Problem 15-16 (continued)

Schedule 1: Lessee’s Calculation of the

Present Value of Minimum Lease Payments

Present value of periodic lease payments

Requirement 2

Present value of lessee’s minimum lease payments, calculated in Schedule 1

Requirement 3

15–126 Intermediate Accounting, 8/e

Problem 15-16 (continued)

Application of Classification Criteria

1 Does the agreement specify that

ownership of the asset transfers

to the lessee? NO

Schedule 2: Lessor’s Calculation of the Present Value of Minimum Lease

Payments

Present value of periodic lease payments ($10,000 x 3.48685**) $34,869

Plus: Present value of the guaranteed

Problem 15-16 (continued)

Since the fair value exceeds the lessor’s book value, the asset is being “sold” at a

profit, making this a sales-type lease:

Fair value $45,114

minus

Requirement 4

Lessor’s Calculation of Lease Payments

Amount to be recovered (fair value) $45,114

Problem 15-16 (continued)

Requirement 5

Present value of lessor’s minimum lease payments, calculated in Schedule 2

above: $42,382

Requirement 6

December 31, 2016

Yard Art Landscaping (Lessee)

Leased equipment (calculated in requirement 1) ................... 39,564

Branch Motors (Lessor)

Lease receivable (to balance) ............................................. 45,114

Problem 15-16 (continued)

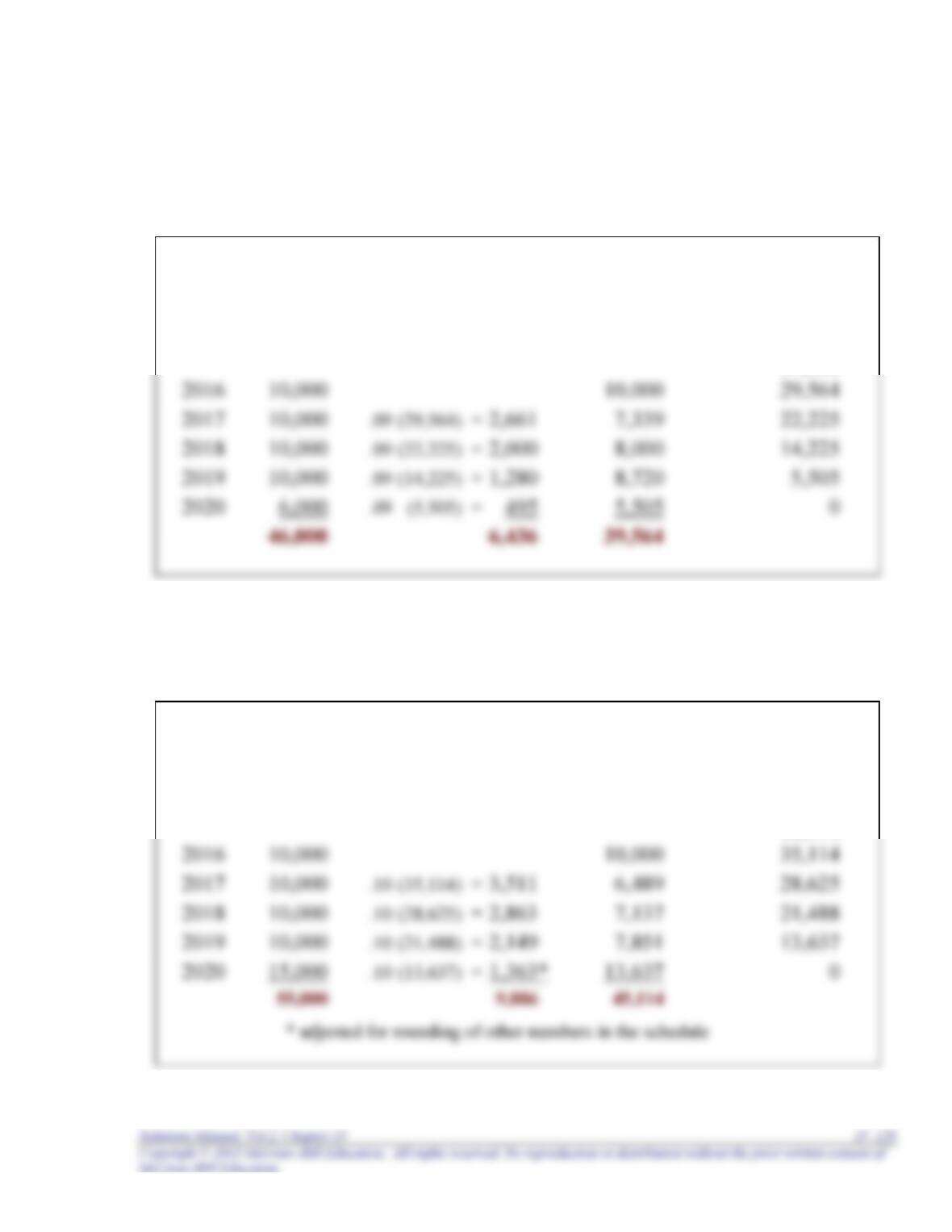

Requirement 7

Lessee’s Amortization Schedule

Effective Decrease Outstanding

Dec. Payments Interest in Balance Balance

31 9% x Outstanding Balance

39,564

Requirement 8

Lessor’s Amortization Schedule

Effective Decrease Outstanding

Dec. Payments Interest in Balance Balance

31 10% x Outstanding Balance

45,114

15–130 Intermediate Accounting, 8/e

Problem 15-16 (continued)

Requirement 9

December 31, 2017

Yard Art Landscaping (Lessee)

Maintenance expense (2017 fee) ............................................. 1,000

Prepaid maintenance expense (paid in 2016) ................... 1,000

Problem 15-16 (continued)

Requirement 10

December 31, 2019

Yard Art Landscaping (Lessee)

Maintenance expense (2019 fee) ............................................. 1,000

Prepaid maintenance expense (paid in 2018) ................... 1,000

Interest expense (9% x $14,225: from schedule) ...................... 1,280

15–132 Intermediate Accounting, 8/e

Problem 15-16 (concluded)

Requirement 11

December 31, 2020

Yard Art Landscaping (Lessee)

Maintenance expense (2020 fee) ............................................. 1,000

Prepaid maintenance expense (paid in 2019) ................... 1,000

Branch Motors (Lessor)

Inventory of equipment (actual residual value) ................... 4,000

Cash ($11,000 – 4,000) ....................................................... 7,000*

Problem 15-17

Calculation of interest expense for the year ended December 31, 2016

Bonds payable $91,384 [1]

Notes payable 49,500 [2]

[1] $1,827,681 x 10% x ½ = $91,384

Interest $90,000¥ x 17.15909 * = $1,543,581

[2] June 30: $500,000 x 10% x ½ = $25,000

Relevant journal entries:

December 31, 2015 (adjusting entry)

June 30, 2016

Interest expense ($500,000 x 10% x ½) 25,000

December 31, 2016

15–134 Intermediate Accounting, 8/e

Problem 15-17 (concluded)

[3] 10% x $99,474 ($139,474* – 40,000) = $9,947

Problem 15-18

Requirement 1

Application of Classification Criteria

1 Does the agreement specify that

ownership of the asset transfers

to the lessee? NO

The lessee’s incremental borrowing rate (11%) is more than the lessor’s implicit

rate (10%). So, both parties’ calculations should be made using a 10% discount rate:

Present value of minimum lease

Problem 15-18 (continued)

(a) Since at least one (two in this case) classification criterion and both additional

Requirement 2

January 1, 2016

Red Baron Flying Club (Lessee)

Leased equipment (calculated above) ................................. 645,526

Problem 15-18 (continued)

Requirement 3

Lease Amortization Schedule

Effective Decrease Outstanding

Payments Interest in Balance Balance

10% x Outstanding Balance

645,526

1/1/16 110,000 110,000 535,526

15–138 Intermediate Accounting, 8/e

Requirement 4

With the initial direct costs, the lease payments are the same, but the net

investment is higher: $645,526 + 18,099 = $663,625. The new effective rate

is the discount rate that equates the net investment and the future lease

payments:

$663,625 ÷ ?** = $110,000

Problem 15-18 (continued)

Requirement 5

Lease Amortization Schedule

Effective Decrease Outstanding

Payments Interest in Balance Balance

9% x Outstanding Balance

663,625

1/1/16 110,000 110,000 553,625

15–140 Intermediate Accounting, 8/e

Problem 15-18 (concluded)

Requirement 6

December 31, 2016

Red Baron Flying Club (Lessee)

Interest expense (10% x [$645,526 – 110,000]) ....................... 53,553

Requirement 7

December 31, 2022

Red Baron Flying Club (Lessee)

Interest expense (10% x $100,000: from schedule) .................. 10,000