Exercise 11–24

Requirement 1

IFRS requires an impairment loss to be recognized when an asset’s book value

exceeds the higher of the asset’s value–in-use (present value of estimated future cash

flows) and fair value less costs to sell. In this case, value–in-use and fair value less

Requirement 2

An impairment loss also is indicated because book value ($6.5 million) exceeds

fair value less costs to sell/value-in-use ($5 million). The amount of impairment loss

is $1.5 million.

11–42 Intermediate Accounting, 8/e

Exercise 11–25

Requirement 1

IFRS requires an impairment loss to be recognized when an asset’s book value

exceeds the higher of the asset’s value–in-use (present value of estimated future cash

Requirement 2

U.S. GAAP requires an impairment loss to be recognized when an asset’s book

Exercise 11–26

Requirement 1

An impairment loss is indicated because the estimated undiscounted sum of

Requirement 2

Requirement 3

Requirement 4

An impairment loss is indicated because the estimated undiscounted sum of

future cash flows of $12 million is less than the book value of $18.3 million.

Exercise 11–27

Requirement 1

Determination of implied fair value of goodwill:

Fair value of Centerpoint, Inc. $220 million

Exercise 11–28

Under IFRS, the impairment loss is the difference between book value and the

Exercise 11–29

Requirement 1

Calculation of goodwill:

Consideration exchanged $420 million

Less fair value of net assets:

Requirement 2

Because the book value of the net assets ($410 million) exceeds fair value ($400

million), an impairment loss is indicated.

Determination of implied fair value of goodwill:

Requirement 3

Entry to record the impairment loss:

11–46 Intermediate Accounting, 8/e

Exercise 11–30

Requirement 1

The Codification topic number that provides guidance on accounting for the

impairment of long-lived assets is FASB ASC 360: “Property, Plant, and Equipment.”

Requirement 2

Requirement 3

All of the following information shall be disclosed in the notes to financial

statements that include the period in which an impairment loss is recognized:

Exercise 11–31

The FASB Accounting Standards Codification® represents the single source

of authoritative U.S. generally accepted accounting principles. The specific

citation for each of the following items is:

1. Depreciation involves a systematic and rational allocation of cost

rather than a process of valuation:

FASB ASC 360–10–35–4: “Property, Plant, and Equipment–Overall–

Subsequent Measurement–Depreciation.”

2. The calculation of an impairment loss for property, plant, and

equipment:

FASB ASC 360–10–35–17: “Property, Plant, and Equipment–Overall–

Subsequent Measurement.”

11–48 Intermediate Accounting, 8/e

3. Accounting for a change in depreciation method:

FASB ASC 250–10–45–18: “Accounting Changes and Error

Correction–Overall–Other Presentation Matters.”

Distinguishing between a change in an accounting principle and a change

4. Goodwill should not be amortized:

FASB ASC 350–20–35–1: “Intangibles-Goodwill and Other–Goodwill–

Exercise 11–32

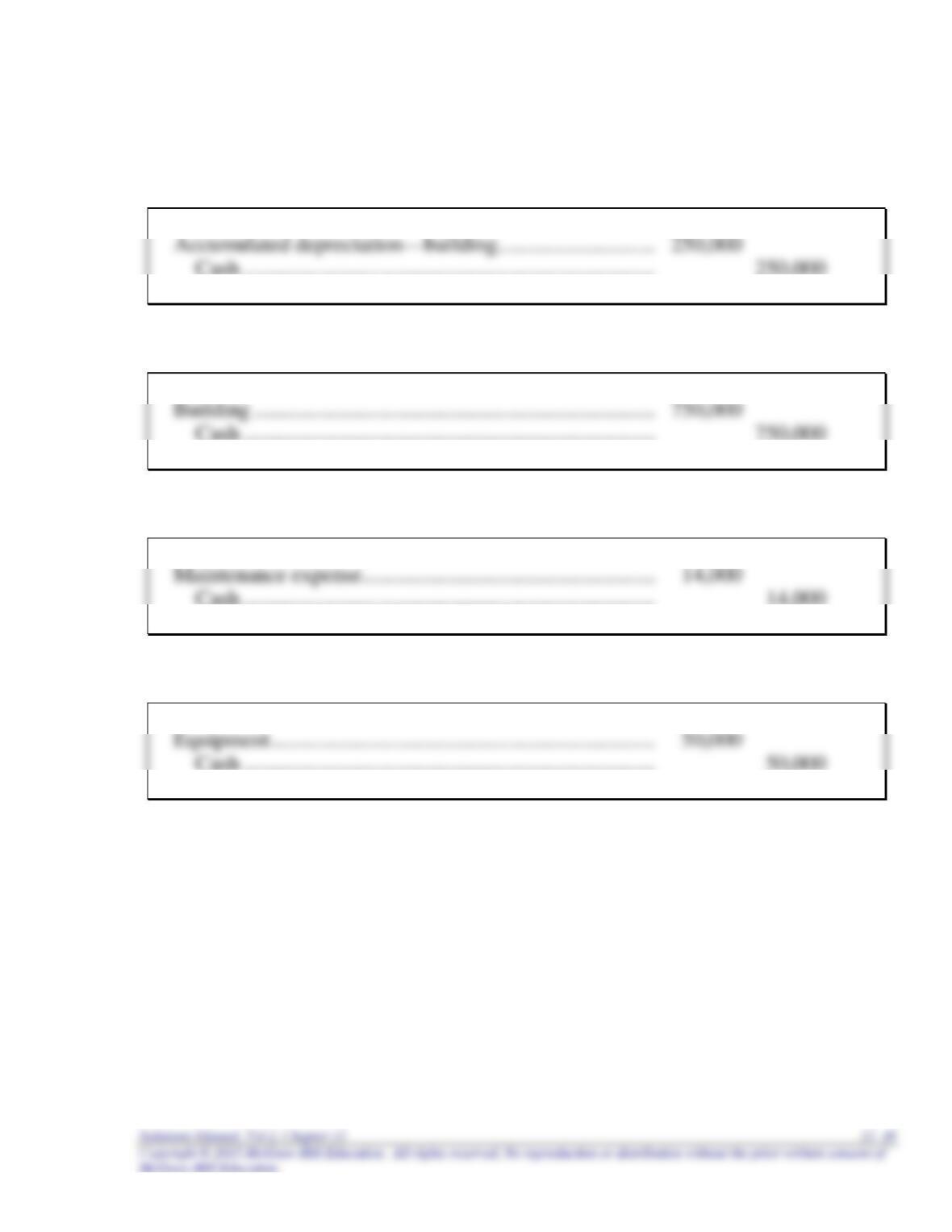

1. To record the replacement of the heating system.

2. To record the addition to the building.

3. To expense annual maintenance costs.

4. To capitalize rearrangement costs.

11–50 Intermediate Accounting, 8/e

Exercise 11–33

Requirement 1

Requirement 2

Requirement 3

Calculation of revised annual amortization:

$6,000,000 Cost

Requirement 4

Requirement 2:

Exercise 11–34

Requirement 1

Cash …………………………………………………………………….. 17,000

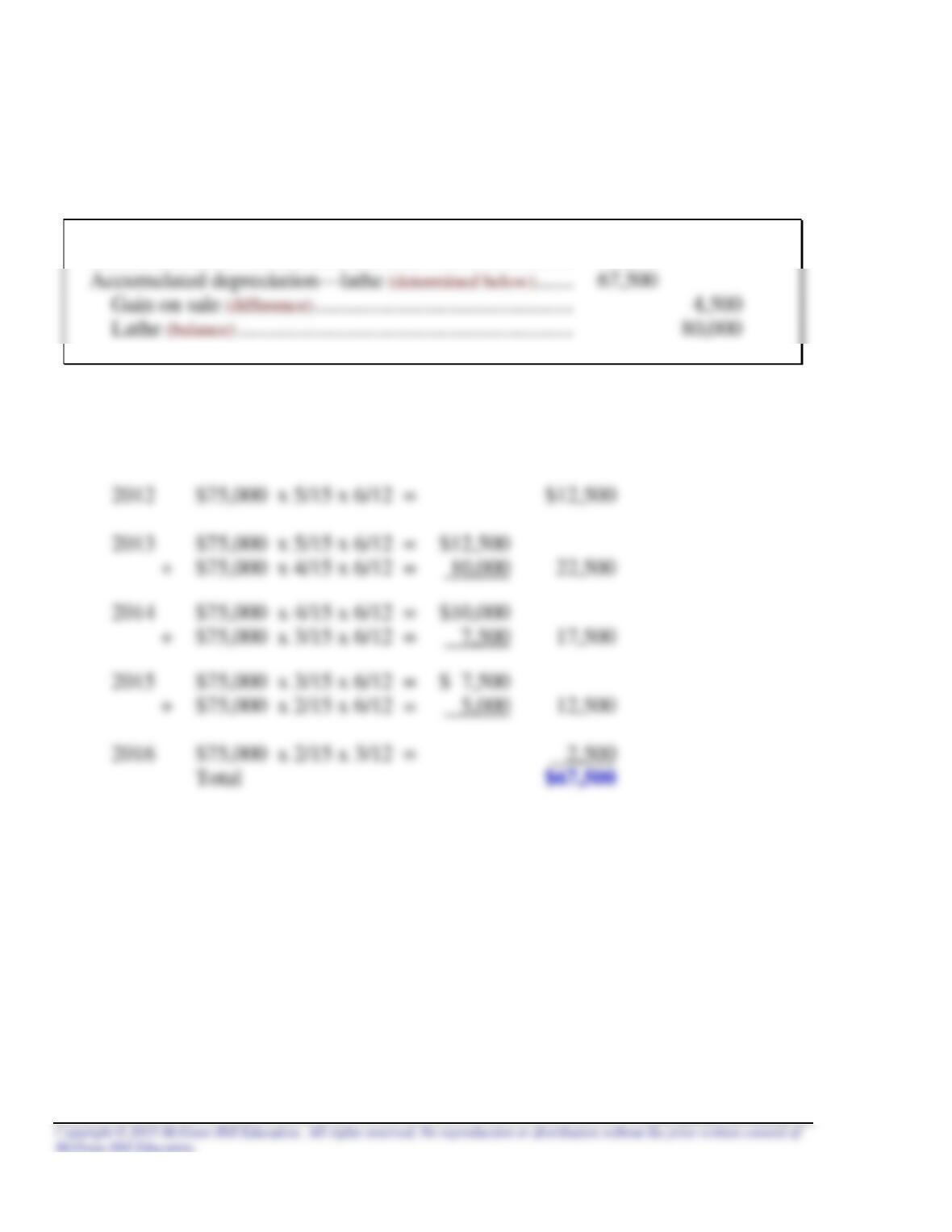

Accumulated depreciation—lathe (determined below) …… 56,250

11–52 Intermediate Accounting, 8/e

Exercise 11–34 (concluded)

Requirement 2

Cash ……………………………………………………………………… 17,000

Accumulated depreciation:

Sum-of-the-digits is ([5 (5 + 1)]/2) = 15

Exercise 11–35

List A List B

g 1. Depreciation a. Cost allocation for natural resource.

d 2. Service life b. Accounted for prospectively.

11–54 Intermediate Accounting, 8/e

Exercise 11–36

Requirement 1

To record the acquisition of small tools.

2014

Small tools ……………………………………………………………. 8,000

Exercise 11–36 (concluded)

Requirement 2

To record the acquisition of small tools.

2014

Small tools …………………………………………………………… 8,000

11–56 Intermediate Accounting, 8/e

CPA / CMA REVIEW QUESTIONS

CPA Exam Questions

1. a. Double-declining-balance depreciation rate = 2 x 1/8 = ¼ or 25%

CPA Exam Questions (concluded)

9. c. $12,000.

$80,000 10 years = $ 8,000

10. a. When as asset is revalued, the entire class of property, plant, and equipment

CMA Exam Questions

1. d. Because 50% of the original estimate of quality ore was recovered during

the years 2008 through 2015, recorded depletion of $250,000 [50% x

2. a. Given that the company paid $6,000,000 for net assets acquired with a fair

3. a. The cost should be amortized over the remaining legal life or useful life,

whichever is shorter. In addition to the initial costs of obtaining a patent,

Problem 11–1

Requirement 1

Determine useful life:

$200,000 depreciable base

= 20-year useful life

Requirement 2

Depreciation expense (below) …………………. 20,000

Accumulated depreciation ……………….. 20,000

PROBLEMS

11–60 Intermediate Accounting, 8/e

Problem 11–2

Requirement 1

CORD COMPANY

Analysis of Changes in Plant Assets

For the Year Ending December 31, 2016

Balance Balance

12/31/15 Increase Decrease 12/31/16

Land $ 175,000 $ 312,500 [1] $ — $ 487,500

Explanations of Amounts:

[1] Plant facility acquired from King 1/6/16—allocation to Land and Building:

Allocation in proportion to appraised values at date of exchange:

% of

Amount Total

Land $187,500 25