Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Alternate Exercises and Problems 15–1

Chapter 15 Leases

EXERCISES

Exercise 15-1

(a) Gothic Corporation (Lessee)

June 30, 2016

Rent expense ................................... 40,000

(b) HardWhere (Lessor)

June 30, 2016

15–2 Intermediate Accounting, 8/e

Exercise 15-2

Present Value of Minimum Lease Payments:

($10,000 x 10.78685*) = $107,866

lease present

Lease Amortization Schedule

Lease Effective Decrease Outstanding

Payments Interest in Balance Balance

2% x Outstanding Balance

107,866

1 10,000 10,000 97,886

2 10,000 .02 (97,886) = 1,957 8,043 89,823

3 10,000 .02 (89,823) = 1,796 8,204 81,619

Alternate Exercises and Problems 15–3

Exercise 15-2 (concluded)

January 1, 2016

Leased equipment (calculated above) ..................... 107,866

Lease payable (calculated above) ....................... 107,866

April 1, 2016

Interest expense (2% x [$107,866 – 10,000]) ............. 1,957

Exercise 15-3

Lease Amortization Schedule

Lease Effective Decrease Outstanding

Payments Interest in Balance Balance

2% x Outstanding Balance

107,866

1 10,000 10,000 97,886

2 10,000 .02 (97,886) = 1,957 8,043 89,823

Alternate Exercises and Problems 15–5

Exercise 15-3 (concluded)

January 1, 2016

Lease receivable (present value of lease payments) .. 107,866

Inventory of equipment (lessor’s cost) .............. 107,866

April 1, 2016

Cash (lease payment).............................................. 10,000

15–6 Intermediate Accounting, 8/e

Exercise 15-4

Requirement 1

Lessor’s Calculation of Lease Payments

Amount to be recovered (fair value) $107,866

Requirement 2

January 1, 2016

Lease receivable (fair value) ................................. 107,866

April 1, 2016

Cash (lease payment) .............................................. 10,000

Alternate Exercises and Problems 15–7

Exercise 15-5

Present value of periodic lease payments*

($205,542 x 7.49236**) $1,540,000

January 1, 2016

Cash (given) ..................................................................... 1,540,000

Helicopter (book value) ................................................. 1,240,000

December 31, 2016

Interest expense (11% x [$1,540,000 – 205,542]) .................... 146,790

Interest payable .......................................................... 146,790

PROBLEMS

Problem 15-1

Requirement 1

Capital lease to lessee; Direct financing lease to lessor.

Since the present value of minimum lease payments (same for both the

lessor and the lessee) is equal to (>90%) the fair value of the asset, the

90% recovery criterion is met.

Calculation of the Present Value of Minimum Lease Payments

Requirement 2

Pal Learning Systems (Lessee)

January 1, 2016

Leased equipment (calculated above) ................................. 500,000

April 1, 2016

Interest expense (3% x [$500,000 – 32,629]) ........................... 14,021

Alternate Exercises and Problems 15–9

Problem 15-1 (concluded)

Star Leasing (Lessor)

January 1, 2016

Lease receivable (present value) ........................................ 652,580

Inventory of equipment (lessor’s cost) .......................... 500,000

Requirement 3

Star Leasing (Lessor)

January 1, 2016

Lease receivable (present value) ........................................ 500,000

15–10 Intermediate Accounting, 8/e

Problem 15-2

Requirement 1

Lessor’s Calculation of Lease Payments

Amount to be recovered (fair value) $1,097,280

Less: Present value of the guaranteed

Requirement 2

The lessee’s incremental borrowing rate (12%) is more than the lessor’s

Alternate Exercises and Problems 15–11

Problem 15-2 (continued)

Application of Classification Criteria

1 Does the agreement specify that

ownership of the asset transfers

to the lessee? NO

Present Value of Minimum Lease Payments

Present value of periodic lease payments

($300,000 x 3.48685**) $1,046,055

Problem 15-2 (continued)

(a) By Blair Co. (the lessee)

Since at least one criterion is met, this is a capital lease to the lessee.

Blair records the present value of minimum lease payments as a leased

Requirement 3

December 31, 2016

Blair Co. (Lessee)

Leased equipment (calculated above) ................................. 1,097,280

Lease payable (calculated above) ................................... 1,097,280

Alternate Exercises and Problems 15–13

Problem 15-2 (continued)

Requirement 4

Since both use the same discount rate and since the residual value is

lessee-guaranteed, the same amortization schedule applies to both the lessee

and lessor:

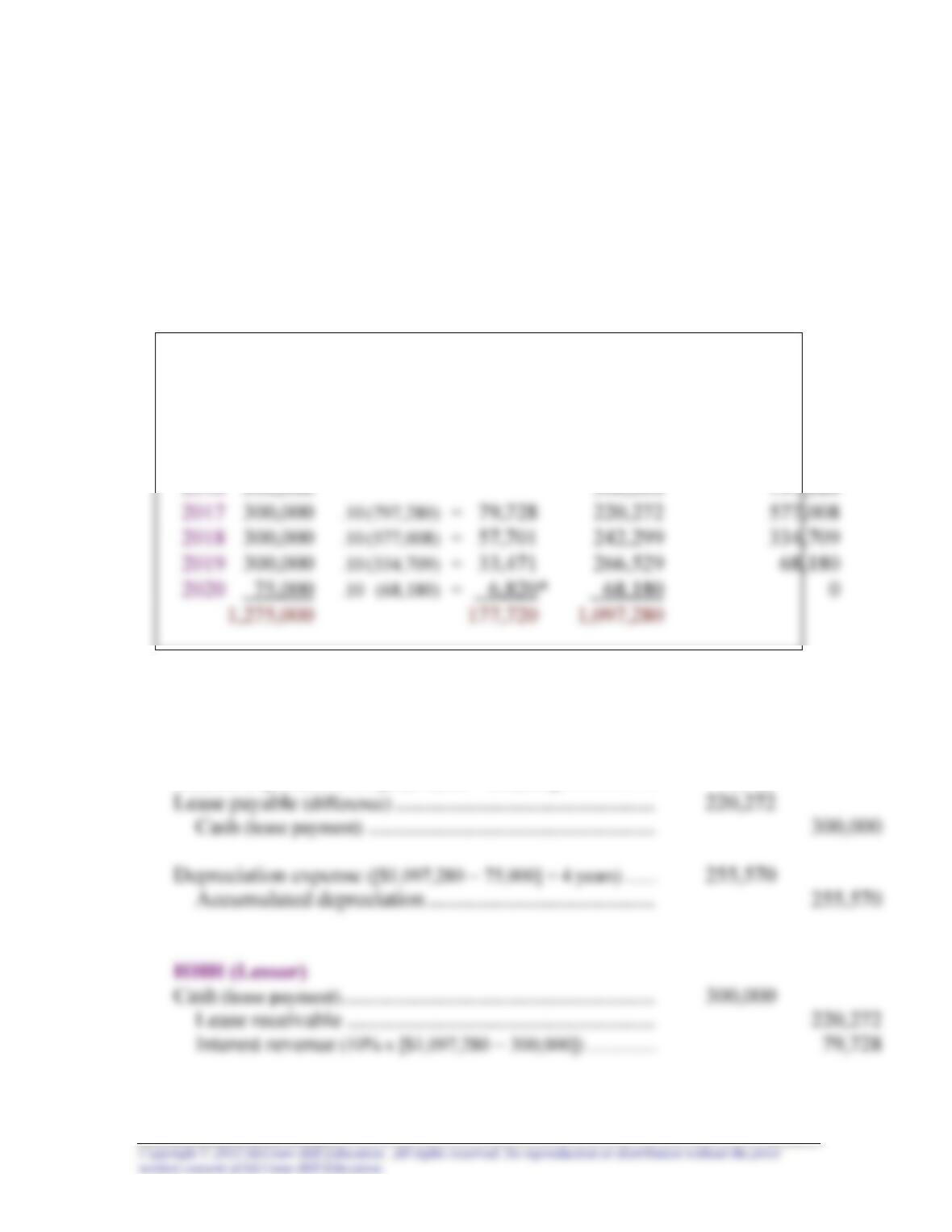

Lease Amortization Schedule

Effective Decrease Outstanding

Dec. Payments Interest in Balance Balance

31 10% x Outstanding Balance

2016 1,097,280

Requirement 5

December 31, 2020

Blair Co. (Lessee)

Interest expense (10% x [$1,097,280 – 300,000]) .................... 79,728

15–14 Intermediate Accounting, 8/e

Problem 15-2 (concluded)

Requirement 6

December 31, 2018

Blair Co. (Lessee)

Depreciation expense ([$1,097,280 – 75,000] ÷ 4 years) ....... 255,570

Accumulated depreciation .......................................... 255,570