Exercise 17–4

Requirement 1

($ in millions)

Pension expense (total) …………………………………………… 14

Requirement 2

($ in millions)

Pension expense (total) …………………………………………… 10

Requirement 3

($ in millions)

Pension expense (total) …………………………………………… 17

17–22 Intermediate Accounting, 8/e

Exercise 17–5

($ in millions)

Plan assets

Beginning of the year $600

Exercise 17–6

($ in millions)

PBO:

Beginning of the year $360

Service cost ?

Exercise 17–7

($ in millions)

Plan assets

Beginning of the year $700

Exercise 17–8

($ in 000s)

Service cost $112

Exercise 17–9

Under IFRS the various components of pension expense are not reported

as a single net amount. Instead, Sterling Properties would separately

report service cost (including past service cost), net interest cost/income,

and remeasurement gains and losses:

($ in 000s)

17–24 Intermediate Accounting, 8/e

Exercise 17–10

Requirement 1

($ in millions)

Service cost $20

Requirement 2

Pension expense (calculated above) 24

Exercise 17–11

Requirement 1

($ in 000s)

Service cost $310

Interest cost (7% x $2,300) 161

Requirement 2

Pension expense (calculated above) 250

Plan assets (expected return on assets) 240

17–26 Intermediate Accounting, 8/e

Exercise 17–12

Requirement 1

1.2% x service years x final year’s salary =

Requirement 2

The present value of the retirement annuity at the end of 2041 is

Requirement 3

The PBO is the present value of the retirement benefits at the end of 2016:

Requirement 4

1.2% x 20 x $80,000 = $19,200

Requirement 5

1.2% x 21 x $270,000 = $68,040

Exercise 17–12 (concluded)

Requirement 6

PBO at the end of 2017 $122,174

The change due to service cost can be verified as follows ($1 difference due to rounding):

(1.2% x 1 yr. x $270,000) x 9.10791 x .19715 = $5,818

17–28 Intermediate Accounting, 8/e

Exercise 17–13

Requirement 1

($ in 000s) Case 1 Case 2 Case 3

Net loss or gain $320 $330 $260

Requirement 2

($ in 000s) Case 1 Case 2 Case 3

January 1, 2016 net loss or (gain) $320 ($330) $260

Exercise 17–14

In the balance sheet,

Liabilities increase by $274 million:

➢ The PBO increases by $374 (service cost and interest cost); plan

Shareholders’ equity decreases by $274 million:

Retained earnings:

Journal entries (not required):

To record expense ($ in 000s)

Pension expense (given) 294

To record gain on assets ……………………….

Plan assets ………………………………………… 10

17–30 Intermediate Accounting, 8/e

Exercise 17–15

PBO

Plan

Assets

Prior

Service

Cost

–AOCI

Net Gain

–AOCI

Pension

Expense

Cash

Net

Pension

(Liability

) / Asset

cost

Expected

assets

Adjust for:

Loss on

assets

(6)

6

(6)

0

Prior

cost

Amortization:

Prior

Exercise 17–16

Requirement 1

($ in millions)

Pension expense (calculated below) 88*

Plan assets (expected return on assets) 40

Requirement 2

($ in millions)

Loss—OCI ($32 actual return on assets – $40 expected return) 8

Plan assets 8

Exercise 17–16 (concluded)

Requirement 3

($ in millions)

Plan assets 90

Exercise 17–17

List A List B

d_ 1. Future compensation levels estimated. a. Actual return exceeds expected

17–34 Intermediate Accounting, 8/e

Exercise 17–18

Requirement 1

A decrease in the discount rate from 7% to 6% increases the projected benefit

Requirement 2

($ in millions)

Loss—OCI (from change in discount rate) 13

PBO 13

Requirement 3

Reporting actuarial gains and losses among OCI items in the statement of

comprehensive income also is required under IAS No. 19, referred to as

Exercise 17–19

Requirement 1

($ in millions)

Pension expense (calculated below) 67*

Plan assets (expected return on assets) 45

Computation of net gain amortization:

Net gain—AOCI (previous gains exceeded previous losses) $ 80

Requirement 2

Journal entries to record gains and losses

($ in millions)

PBO (given) ……………………………………….. 10

17–36 Intermediate Accounting, 8/e

Exercise 17–19 (continued)

Requirement 3

($ in millions)

Plan assets 70

Requirement 4

PBO

480 Jan. 1 balance

82 Service cost

Plan Assets

Jan. 1 balance 500

Expected return 45

Exercise 17–19 (concluded)

SHAREHOLDERS’ EQUITY: ACCUMULATED

OTHER COMPREHENSIVE INCOME

Net Gain—AOCI

80 Jan. 1 balance

Prior Service Cost—AOCI

Requirement 5

The pension plan is overfunded. Beale will report a net pension asset of $34 million

in its 2016 balance sheet:

Plan assets – PBO = Net pension asset

17–38 Intermediate Accounting, 8/e

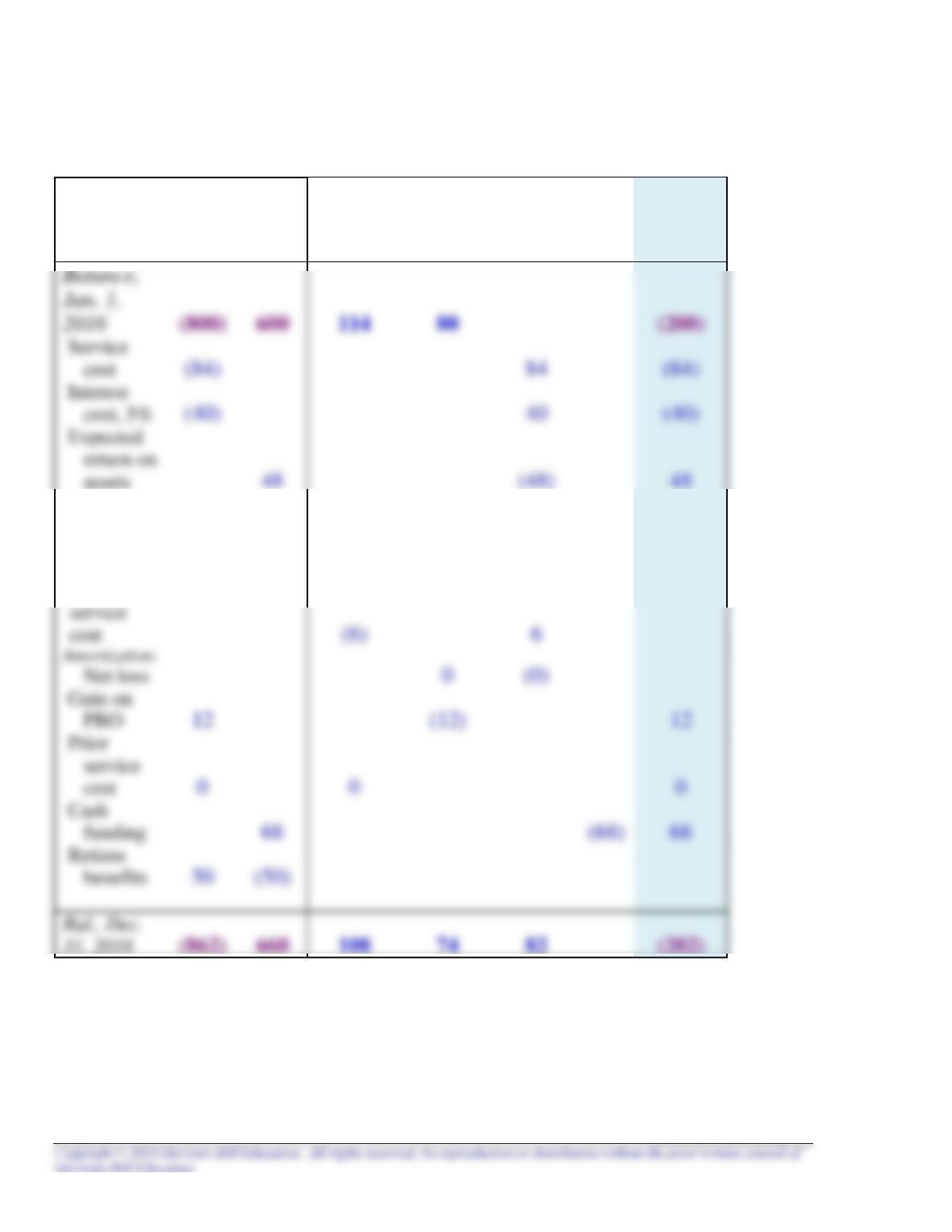

Exercise 17–20

PBO

Plan

Assets

Prior

Service

Cost

–AOCI

Net

Gain

–AOCI

Pension

Expense

Cash

Net

Pension

(Liability)

/ Asset

Balance,

Jan. 1, 2016

(480)

500

48

(80)

20

assets

Adjust for:

Loss on

assets

(5)

5

(5)

Amortization

of:

(536)

570

40

(83)

34

Prior

service

Exercise 17–21

Requirement 1

($ in millions)

Service cost $ 60

Requirement 2

($ in millions)

Pension expense (calculated above) 63

17–40 Intermediate Accounting, 8/e

Exercise 17–22

Under U.S. GAAP, prior service cost is included among other comprehensive

income items in the statement of comprehensive income and thus subsequently

becomes part of accumulated other comprehensive income where it is amortized

over the average remaining service period.

Under IAS No. 19, past service cost (called prior service cost under U.S. GAAP) is

expensed immediately as part of the service cost for the year.

Requirement 1

Income statement: ($ in millions)