Problem 16–1 (continued)

Requirement 2

($ in thousands)

Current Future

Year Taxable

2017 Amount

Pretax accounting income 220

Temporary difference:

Deferred Tax Liability

Deferred Tax Liability:

16–62 Intermediate Accounting, 8/e

Problem 16–1 (concluded)

Requirement 3

($ in thousands)

Current Future

Year Taxable

2018 Amount

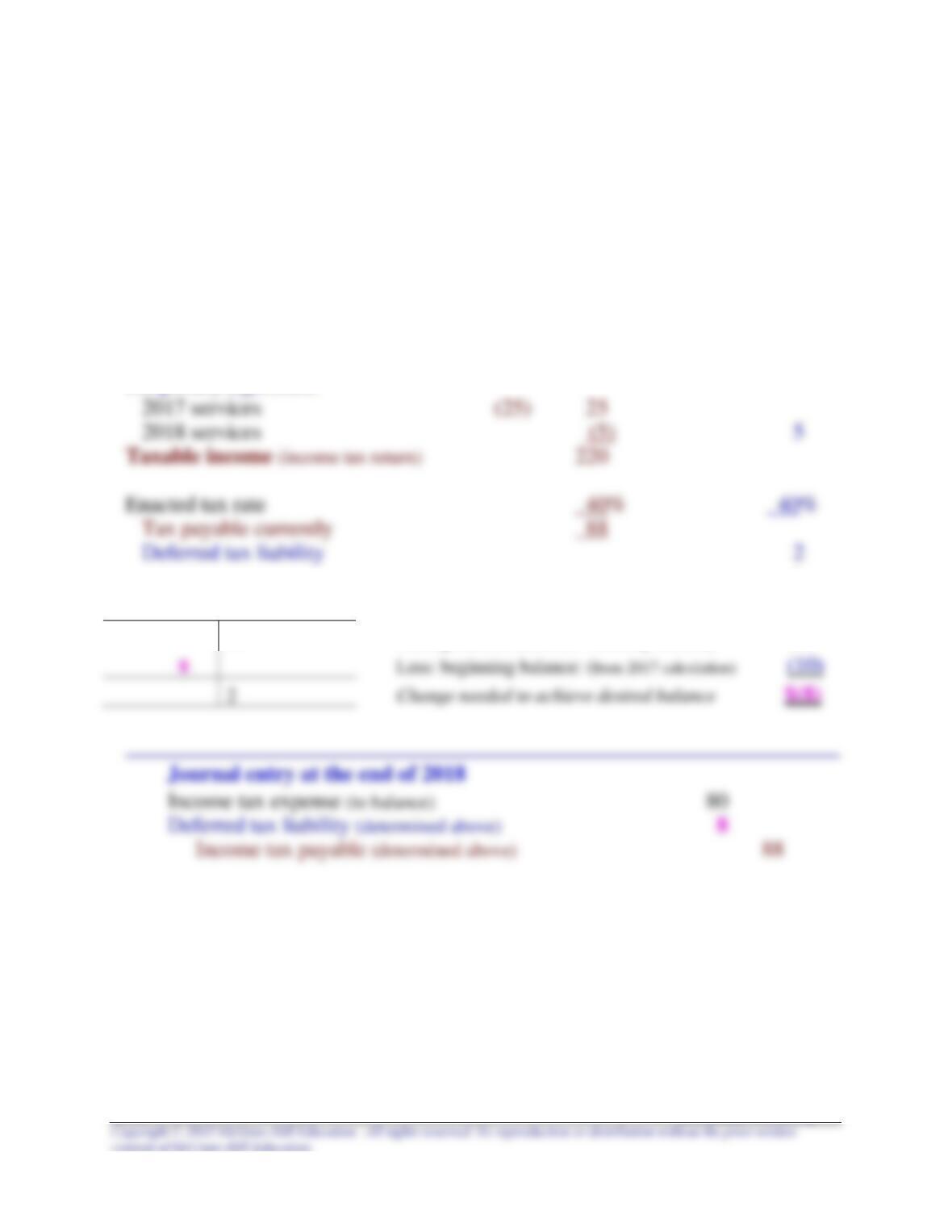

Pretax accounting income 200

Temporary difference:

Deferred Tax Liability

Deferred Tax Liability:

10

Ending balance (balance currently needed)

$ 2

Less: beginning balance: (from 2017 calculation)

2

Problem 16–2

Requirement 1

A liability for unearned subscription revenue is created when subscriptions are

Requirement 2

($ in millions)

December 31

2016 2017 2018

Liability—Subscriptions:

$ 0 $ 40 $ 20

Requirement 3

Requirement 4

16–64 Intermediate Accounting, 8/e

Problem 16–3

Requirement 1

($ in millions)

Current Future Future

Year Taxable Taxable

2016 Amounts Amounts

2017 2018 2019 [total]

Pretax accounting income 16

Deferred Tax Liability

Deferred Tax Liability:

0

Ending balance (balance currently needed)

$ 4.8

Less: beginning balance

4.8

Journal entry at the end of 2016

16–66 Intermediate Accounting, 8/e

Problem 16–3 (continued)

Requirement 2

($ in millions)

Current Future Future

Year Taxable Taxable

2017 Amounts Amounts

2018 2019 [total]

Pretax accounting income 15

Deferred Tax Liability

Deferred Tax Liability:

4.8

Ending balance (balance currently needed)

$ 2.8

Less: beginning balance

2.8

Journal entry at the end of 2017

Problem 16–3 (concluded)

Requirement 3

The balance in the deferred tax liability account at the end of 2017 would have

been $3.2 million if the new tax rate had not been enacted:

16–68 Intermediate Accounting, 8/e

Problem 16–4

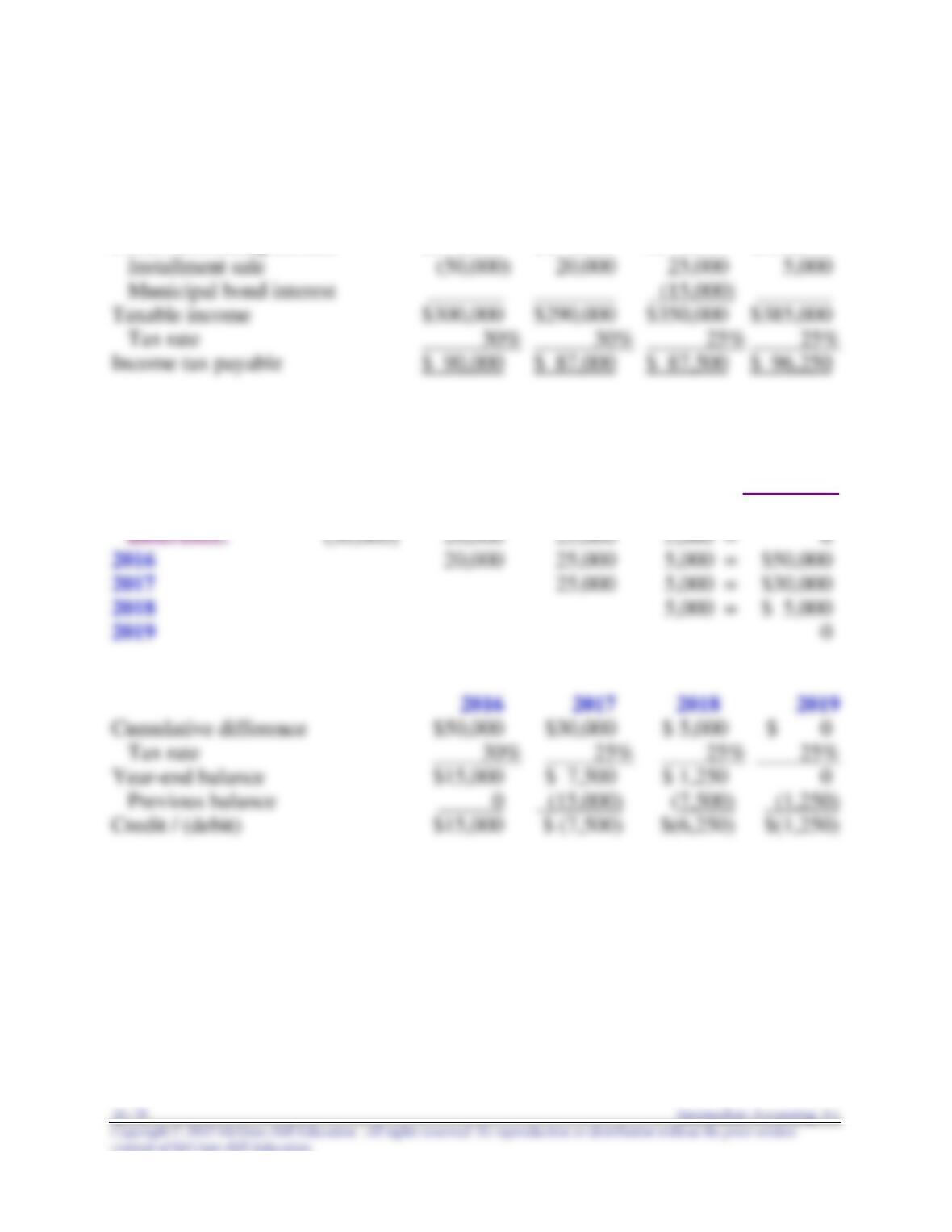

2016 2017 2018 2019

Pretax accounting income $60,000 $80,000 $70,000 $70,000

Depreciation for tax (39,600) (52,800) (18,000) ( 9,600)

Cumulative

Temporary

2016 2017 2018 2019 Difference

Straight-line 30,000 30,000 30,000 30,000

2016 2017 2018 2019

Cumulative difference $ 9,600 $32,400 $20,400 $ 0

Problem 16–4 (concluded)

Journal entry at the end of 2016

Income tax expense (to balance) 9,000

Journal entry at the end of 2017

Problem 16–5

2016 2017 2018 2019

Pretax accounting income $350,000 $270,000 $340,000 $380,000

Cumulative

Temporary

2016 2017 2018 2019 Difference

Temporary

Problem 16–5 (concluded)

Journal entry at the end of 2016

Income tax expense (to balance) 105,000

16–72 Intermediate Accounting, 8/e

Problem 16–6

Requirement 1

($ in millions)

Income tax expense (to balance) 16.4

Requirement 2

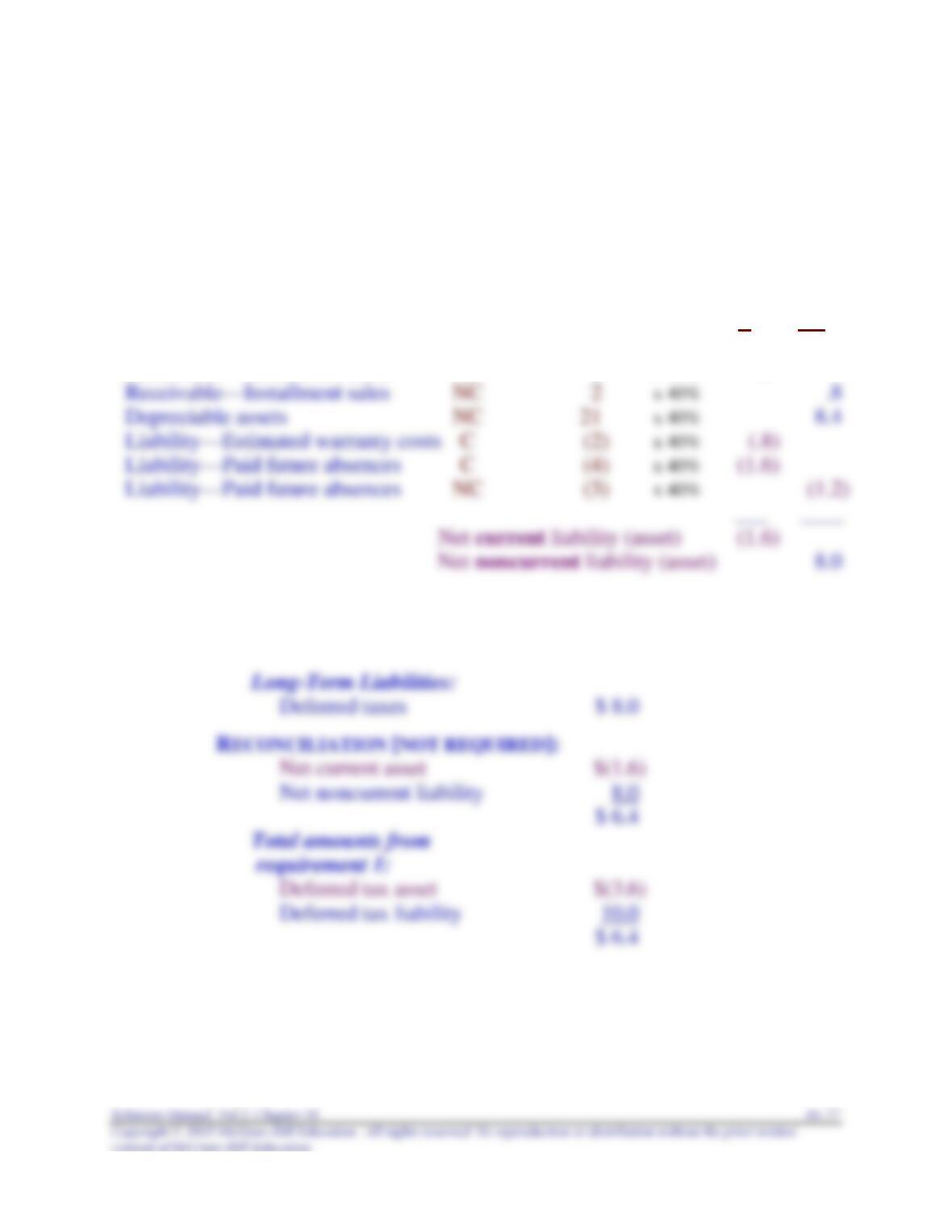

In a classified balance sheet, deferred tax assets and deferred tax liabilities

are classified as either current or noncurrent according to how the related

assets or liabilities are classified for financial reporting. The deferred tax

liabilities and deferred tax assets are offset to get the net current and the net

noncurrent amounts:

($ in millions)

Future Deferred

Classification Taxable Tax (Asset)

Related Balance current-C (Deductible) Tax Liability

Sheet Account noncurrent-NC Amounts Rate C NC

Problem 16–6 (continued)

Requirement 3

($ in millions) Current Future Taxable Deferred

Year (Deductible) Tax

2016 Amounts Liab. Asset

2017 2018 2019

Pretax accounting income 41

Temporary differences:

Depreciation (30) 30*

Deferred

Tax

Liab. Asset

Ending balances (balances currently needed) $14.1 $2.1

16–74 Intermediate Accounting, 8/e

Problem 16–6 (concluded)

* When a portion of a temporary difference has yet to originate, as in the

case of depreciation here, only the reversals of the temporary difference

at the balance sheet date ($30) can be scheduled. Future originations

Problem 16–7

Requirement 1

($ in millions)

Future

Current Taxable Future Future

Year (Deductible) Taxable Deductible

2016 Amounts Amounts Amounts

2017 2018 [total] [total]

Pretax accounting income 76

Permanent difference:

Fine paid 2

Deferred Tax Asset

Deferred Tax Liability

1.2

2.8

10.0

Deferred

Tax

Liab. Asset

Ending balances (balances currently needed) $10.0 $3.6

16–76 Intermediate Accounting, 8/e

Problem 16–7 (continued)

Journal entry at the end of 2016

Income tax expense (to balance) 31.2

Problem 16–7 (concluded)

Requirement 3

($ in millions)

Future Deferred

Classification Taxable Tax (Asset)

Related Balance current-C (Deductible) Tax Liability

Sheet Account noncurrent-NC Amounts Rate C NC

Receivable—Installment sales C 2 x 40% .8

Current Assets:

Deferred taxes $ 1.6

16–78 Intermediate Accounting, 8/e

Problem 16–8

Requirement 1

The expense for life insurance premiums is a permanent difference each year

Problem 16–8 (continued)

Requirement 2

Current Future Future

($ in millions) Year Taxable Deductible

2016 Amounts Amounts

[2017] [2017]

Pretax accounting income 128

Permanent difference:

Life insurance premiums 2

Deferred Tax Asset

Deferred Tax Liability

6

0

12

16–80 Intermediate Accounting, 8/e

Problem 16–8 (continued)

Journal entry at the end of 2016

Income tax expense (to balance) 52

* Temporary difference for subscriptions:

2015 2016 2017

Earned in current yr. (reported on income statement) $25 $33

Requirement 3

Because all accounts related to the temporary differences (prepaid