12-40 Intermediate Accounting, 8/e

REPORTING AN EQUITY-METHOD INVESTMENT

ON THE BALANCE SHEET

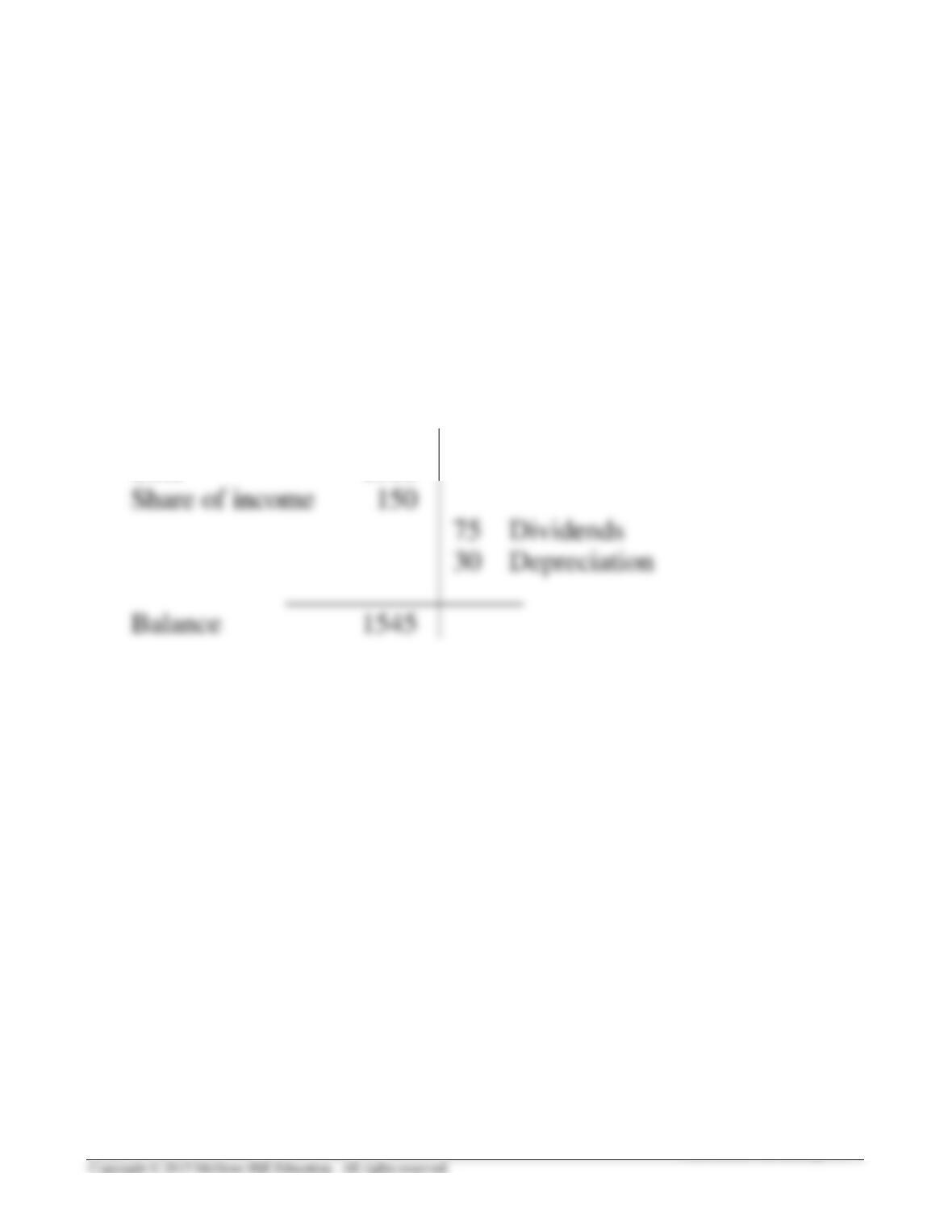

The investment account represents the investor’s share of the

investee’s net assets initially acquired, adjusted for the investor’s

share of the subsequent increase in the investee’s net assets (net

assets earned and not yet distributed as dividends).

Investment in Equity Securities

_____________________________________________

($ in millions)

Cost 1500

T12-24

A CHANGE FROM THE EQUITY METHOD

TO ANOTHER METHOD

A CHANGE FROM ANOTHER METHOD

TO THE EQUITY METHOD

T12-25

12-42 Intermediate Accounting, 8/e

Comparison of Fair Value and Equity Methods

Fair Value Method

Equity Method

Purchase equity

investment

Investment asset 1,500,000

Cash 1,500,000

Same as TS

Recognize

Adjust

investment to

Net unreal.

Recognize gain or loss:

Cash 1,446,000

Loss (to balance) 54,000

Cash 1,446,000

Loss (to balance) 99,000

Illustration 12-17

T12-26

Fair Value Option

Established by SFAS No. 159.

A choice is made when security acquired or becomes eligible for the fair

value option. The choice is made on an instrument-by-instrument basis,

T12-27

12-44 Intermediate Accounting, 8/e

INTERNATIONAL FINANCIAL REPORTING STANDARDS

Fair Value Option

IFRS are more restrictive than U.S. standards for determining when firms are allowed to

elect the fair value option. Companies can elect the fair value option only in specific

circumstances. For example:

• A company could elect the fair value option for an asset or liability in order to

T12-28

Variation in Earnings by Method

Used to Account for Investments

Situation: Investor Company owns 20% of Investee Company. Investee’s net

income is $1 million. Investee distributes one-half its earnings as

Which accounting method causes reported income to be highest?

Accounting Method Used:

Trading Security available- Equity

security for-sale method

T12-29

12-46 Intermediate Accounting, 8/e

CASH SURRENDER VALUE

Several years ago, American Capital acquired a $1 million insurance policy

on the life of its Chief Executive Officer, naming American Capital as

To record insurance expense and the increase in the investment:

Insurance expense (difference) ……………………………………………. 16,000

T12-30

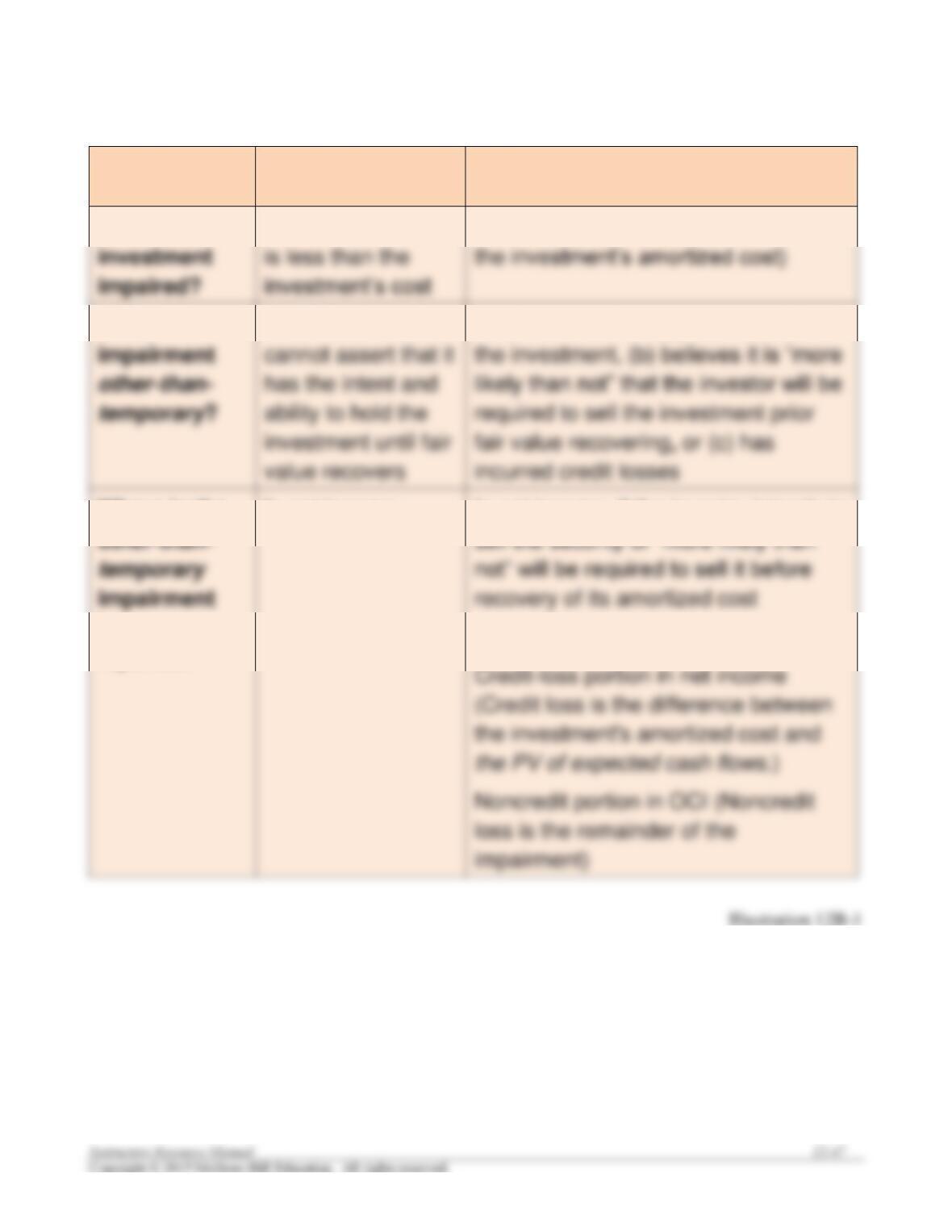

OTT IMPAIRMENTS

Investment in

Equity Security

Investment in

Debt Security

is less than the

the investment’s amortized cost)

Is the

Yes, if the fair value

Same (yes, if the fair value is less than

investment until fair

fair value recovering, or (c) has

Is the

Yes, if the investor

Yes, if the investor (a) intends to sell

loss is the remainder of the

Where is the

loss

reported?

In net income

In net income, if the investor intends to

Otherwise:

T12-31

12-48 Intermediate Accounting, 8/e

INTERNATIONAL FINANCIAL REPORTING STANDARDS

Other-Than-Temporary Impairments

• Under IAS No. 39:

o Companies recognize OTT impairments if there exists objective evidence

of impairment. Objective evidence must relate to one or more events

occurring after initial recognition of the asset that affect the future cash

• Under IFRS No. 9:

o Impairment of debt investments is calculated using the expected credit

loss (ECL) model. Under that approach,

▪ If the credit risk of a debt investment has not increased, the estimate

o OTT impairments of equity investments are not recognized.

▪ If the investment is classified as FVPL, unrealized losses are

S

SU

UG

GG

GE

ES

ST

TI

IO

ON

NS

S

F

FO

OR

R

C

CL

LA

AS

SS

S

A

AC

CT

TI

IV

VI

IT

TI

IE

ES

S

1. Real World Scenario

EchoStar Communications operates through two business units, the DISH Network and EchoStar

January 10, 2002

ITEM 5. OTHER EVENTS

Effective September 27, 2001, EchoStar Communications Corporation (“EchoStar” or “the Company”)

invested an additional $50 million in StarBand Communications, Inc. (“StarBand”), increasing its

Suggestions:

Have the class discuss the manner in which EchoStar would have accounted for the change it

described.

Points to note:

2. Real World Scenario

Media General, Inc. is an independent, publicly owned communications company with interests in

metropolitan newspapers, broadcast television, cable television, newsprint production, and diversified

information services located primarily in the Southeast United States. Its 1998 annual report reported

the following as a portion of its disclosure note related to investments:

Note 3: Investments in Unconsolidated Affiliates

—————————————-——————–——————–

Summarized financial information for these investments accounted for by the equity method

follows:

Southeast Paper Manufacturing Company:

(In thousands) 1998 1997

Suggestions:

Without access to other information reported by Media General in the annual report, have the class

estimate Media General’s percentage ownership interest in Southeast Paper Manufacturing Company.

Assuming Southeast Paper Manufacturing Company declared no cash dividends during 1998, what

was the change in Media General’s investment account related to Southeast Paper Manufacturing

Company?

Points to note:

3. Professional Skills Development Activities

The following are suggested assignments from the end-of-chapter material that will help your

students develop their communication, research, analysis, and judgment skills.

Communication Skills. Research Case 12-5, Real World Cases 12-6 and 12-7, and Problem 12-13

are suitable for student presentation(s). Real World Case 12-1 does well as group assignments.

Questions 12-7, 12-9 and 12-10 create good class discussions.

Research Skills. In their careers, our graduates will be required to locate and extract relevant

information from available resource material to determine the correct accounting practice or to

Analysis Skills. Accountants routinely are required to gather, assemble, organize, process, or

interpret data to provide options for making business and investment decisions. Real World Case

12-1, and International Case 12-3, and Trueblood Case 12-8 provide opportunities to develop

analysis skills.

12-52 Intermediate Accounting, 8/e

4. Internet Activities

I. Cisco Systems is the world’s leading supplier of internetworking solutions targeted at corporate

enterprise intranets and the internet. Have students, individually or in groups:

A. Go to Cisco’s web site at: www.cisco.com/. Ask them to:

1. Access the company’s corporate profile.

2. Determine its primary products and activities.

B. Access Cisco’s most recent annual report from EDGAR on the web.

1. Identify any amounts that Cisco reports as short-term investments; as long-term investments.

What changes have occurred in investments during the most recent year?

2. From disclosure notes determine the types of securities held in each category.

3. Does the statement of cash flows offer any useful information about Cisco’s investing

activities?

II. SFAS 115 requires companies to report fair values for trading securities and securities available–

for-sale. The internet greatly facilitates that process.

Suggestion:

Give students the names of three or four nationally traded public companies. Ask students to

A

As

ss

si

ig

gn

nm

me

en

nt

t

C

Ch

ha

ar

rt

t

Learning Est. time

Questions Objective(s) Topic (min.)

12-1

12-01

Classification categories

5

12-2

12-01

Price changes for a held-to-maturity security

5

12-3

12-02, 12–03

Determining fair value

5

12-4

12-02, 12–03

Why fair value?

5

12-5

12-02, 12–03

Unrealized holding gains and losses

5

12-6

12-03

Comprehensive income

5

12-7

12-02, 12–03

Unrealized holding gains and losses

5

12-8

12-01, 12–02,

12-03

Reclassification of an investment

5

12-9

12-01, 12–02,

12-03

Investment disclosures

5

12–10

12-01, 12-02,

12-03, 12-08

12-11

12-02, 12-03,

IFRS, cost method

5

12-08

12-12

12-01, 12–03,

12-07

Fair value option

5

12-13

12-01, 12–03,

12-07, 12–08

IFRS, fair value option

5

12-14

12-04

Criteria for the equity method

5

12-15

12-04

Equity method, concepts

5

12-16

12-05

Equity method, dividends

5

12-17

12-06

Equity method, depreciation

5

12-18

12-05

Equity method, dividends

5

12-19

12-06

Change from the equity method to another method

5

12–20

12-04, 12-05,

12-08

IFRS, equity method

5

12-21

12-04, 12–07

Fair value option (equity method)

5

12-22

12-01

Define a financial instrument. [based on appendix]

5

12-23

12-01

Derivatives [based on appendix]

5

12-24

App 12A

Special purpose fund [based on appendix]

5

12-25

App 12A

Life insurance policies [based on appendix]

5

12-26

App 12B

OTT impairment, debt investments [based on appendix]

5

12-27

App 12B, 12-03

OTT impairment, AFS investments [based on appendix]

5

12-28

App 12B, 12-03

OTT impairment, AFS investments [based on appendix]

5

12-29

App 12B, 12-08

IFRS, OTT impairment, [based on appendix]

5

Brief Learning Est. time

Exercises Objective(s) Topic (min.)

12-54 Intermediate Accounting, 8/e

12-1

12–01

Securities held–to-maturity; bond investment;

effective interest

5

12-2

12–02

Trading securities

5

12-3

12–03

Available-for-sale securities

5

12-4

12–03

Securities available-for-sale; adjusting entries

5

12-5

12–03

Classification of securities; reporting

5

12-6

12–07

Fair value option; available-for-sale securities

5

12-7

12-02, 12-03

Trading securities, securities available-for-sale and

dividends

5

12-8

12-2, 12-8

Accounting for fair value changes in debt investments

10

12-9

12-1, 12-8

Accounting for fair value changes in debt investments

10

12–10

12–05

Equity method and dividends

5

12–11

12-06, 12-07

Equity method

5

12–12

12-06, 12-08

Equity method investments

10

12–13

12–05

Change in principle; change to the equity method

10

12–14

12–07

Fair value option; equity method investments

5

12–15

12–03

Available-for-sale securities and impairment

(Appendix 12B)

10

12–16

12–03

Available-for-sale securities and impairment

(Appendix 12B)

10

12–17

12–03

(Appendix 12B)

10

Available for sale securities and impairment

12–18

12-03, 12-08

Recovery of impairment under IFRS (Appendix 12B)

10

Learning Est. time

Exercises Objective(s) Topic (min.)

12-1

12–01

Securities held–to-maturity; bond investment;

effective interest

15

12-2

12–01

Securities held–to-maturity

15

12-3

12–01

FASB codification research

15

12-4

12-02, 12-03

Purchase and sale of investment securities

15

12-5

12–02

Various transactions related to trading securities

15

12-6

12-02, 12-03,

12–05

FASB codification research

15

12-7

12–03

Securities available-for-sale; adjusting entries

15

12-8

12–03

Classification of securities; adjusting entries

20

12-9

12–03

for-sale

20

Various transactions related to securities available-

12–10

12–03

Securities available-for-sale; journal entries

15

12–11

12-01, 12-02,

12–03

Various investment securities

10

12–12

12–03

Investment securities and equity method investments

compared

20

12–13

12–03

Securities available-for-sale; fair value adjustment

15

12–14

12-01, 12-08

Accounting for debt investments

12–15

12-02, 12-08

Accounting for debt investments

12–16

12-03, 12-04,

Investment securities and equity method investments

12–05

compared

15

12–17

12-04, 12-05

Equity method; purchase; investee income; dividends

20

12–18

12–05

Change in principle; change to the equity method

25

12–19

12-01, 12-02,

12–03

Error corrections; investment

25

12–20

12-05, 12-06

Equity method; adjustment for depreciation

25

12–21

12-05, 12-06

Equity method

25

12–23

12-01, 12-02,

12–07

Fair value option; held-to-maturity investments

25

12–24

12-02, 12-03,

12–07

Fair value option; held-to-maturity investments

10

12–25

12-02, 12-05,

12–07

Fair value option; held-to-maturity investments

10

12–26

App 12A

Life insurance policy

25

12–27

App 12A

Life insurance policy

25

12–28

12-01, App 12B

Held-to-maturity securities; impairments

25

12–29

12-03, App 12B

Available-for-sale debt securities; impairments

25

12–30

12-03, App 12B

Available-for-sale debt securities; impairments

25

12–31

12-01, 12-03,

12-08, App 12B

Accounting for impairments under IFRS

25

CPA Learning Est. time

Review Questions Objective(s) Topic (min.)

12-1

12-02

Trading securities

5

12-2

12-03

Available-for-sale securities

5

12-3

12-03

Available-for-sale securities

5

12-4

12-03

Available-for-sale securities

3

12-5

12-05

Equity method

3

12-6

12-05

Equity method

5

12-7

12-06

Equity method

3

12-8

12-04, 12-05

Equity method

5

12-9

12-08

Debt investment categories under IFRS

5

12–10

12-08

Equity investment categories under IFRS

5

12–11

12-08

Transfers between investment categories under

IFRS

5

12–12

12-08

Equity method under IFRS

5

12–13

12-08

OTT impairments under IFRS

5

CMA

Review Questions

Learning

Objective(s)

Topic

Est. time

(min.)

12-1

12-03

Available-for-sale securities

3

12-2

12-03

Available-for-sale securities

5

12-3

12-01

Held-to-maturity investments

5

Learning Est. time

Problems Objective(s) Topic (min.)

12-1

12-01

Various transactions related to securities held–to-maturity

30

12-2

12-02

Various transactions relating to trading securities

35

12-56 Intermediate Accounting, 8/e

12-3

12-03

Various transactions related to securities available-for-

sale; bonds

30

12-4

12-01, 12–02,

Various transactions related to securities held–to-maturity;

30

12-03, 12-07

fair value option

12-5

12-03

Various transactions related to securities available-for-sale

35

12-6

12-02

Various transactions relating to trading securities

35

12-7

12-01, 12–02,

12-03

Securities held–to-maturity, securities available-for-sale,

and trading securities

30

12-8

12-03

Securities available-for-sale; fair value adjustment;

reclassification adjustment

35

12-9

12-01, 12–02,

12-04, 12–05,

12-06

Investment securities and equity method investments

compared

35

12–10

12-02, 12-04,

Equity method, fair value option

12-07

12–11

12-02, 12-04,

12-05, 12-07

Equity method, fair value option

35

12–12

12-05, 12–06

Equity method

35

12–13

12-05, 12–06

Equity method

25

12-14

12-01, 12–02,

12-03, 12–04,

12-05

Classifying investments

15

12–15

12-01, 12-07

Held-to-maturity investments, fair value option

30

12–16

12-01, 12-02,

12–08

Accounting for debt and equity investments

30

12-17

App 12B, 12–

02, 12-03

OTT impairments, HTM and AFS investments [based on

appendix12–B]

30

12-18

App 12B, 12–

02, 12-03, 12–

08

IFRS, OTT impairments, HTM and AFS investments

[based on appendix12-B]

30

Star Problems

Learning Est. time

Cases Objective(s) Topic (min.)

Real World Case 12-1

12-03

Securities available-for-sale; Intel

20

Research Case 12-2

12-02

Reporting securities available-for-sale; obtain and

critically evaluate an annual report

45

International Case 12-3

12-04, 12-05,

12-06, 12–08

IFRS comparison of equity method with U.S. GAAP;

Renault

20

International Case 12-4

20

12-06, 12-08

Research Case 12-5

12-01, 12-02,

12-03

Researching the way investments are reported; retrieving

information from the Internet

20

Real World Case 12-6

12-02

Researching the way investments are reported; retrieving

information from the Internet; Merck

45

Real World Case 12-7

12-02

Researching the way comprehensive income reported;

retrieving information from the Internet; Microsoft

20

Real World Case 12-8

App 12B

OTT impairments

20

Real World Case 12-9

App 12B

Researching rationale for approach used to account for

OTT impairments [based on appendix12-B]

20

Air France-KLM Case

12-08

IFRS; Air France-KLM, FVTPL, AFS, equity method

30

CPA Simulation 12-1 Held-to-maturity securities, trading securities, and