C

CH

HA

AP

PT

TE

ER

R

1

16

6

A

Ac

cc

co

ou

un

nt

ti

in

ng

g

f

fo

or

r

I

In

nc

co

om

me

e

T

Ta

ax

xe

es

s

Overview

In this chapter we explore the financial accounting and reporting standards for the effects of

income taxes. The discussion defines and illustrates “temporary differences,” which are the basis for

recognizing deferred tax assets and deferred tax liabilities, as well as “permanent differences,” which

have no deferred tax consequences. You also will learn how to adjust deferred tax assets and

deferred tax liabilities when tax laws or rates change. We also discuss accounting for operating loss

carrybacks and carryforwards and intraperiod tax allocation.

Learning Objectives

After studying this chapter, you should be able to:

LO16-1 Describe the types of temporary differences that cause deferred tax liabilities and determine

the amounts needed to record periodic income taxes.

LO16-2 Identify and describe the types of temporary differences that cause deferred tax assets.

LO16-3 Describe when and how a valuation allowance is recorded for deferred tax assets.

LO16-4 Explain why non-temporary differences have no deferred tax consequences.

LO16-5 Explain how a change in tax rates affects the measurement of deferred tax amounts.

LO16-6 Determine income tax amounts when multiple temporary differences exist.

LO16-7 Describe when and how an operating loss carryforward and an operating loss carryback are

recognized in the financial statements.

LO16-8 Explain how deferred tax assets and deferred tax liabilities are classified and reported in a

classified balance sheet and describe related disclosures.

LO16-9 Demonstrate how to account for uncertainty in income tax decisions.

LO16-10 Explain intraperiod tax allocation.

LO16-11 Discuss the primary differences between U.S. GAAP and IFRS with respect to accounting

for income taxes.

L

Le

ec

ct

tu

ur

re

e

O

Ou

ut

tl

li

in

ne

e

Part A: Deferred Tax Assets and Deferred Tax Liabilities

I. Temporary Differences

A. Revenues and expenses included on a company’s income tax return usually are the same

as those reported on the company’s income statement for the same period.

1-2 Intermediate Accounting, 8/e

D. Income tax expense includes both the current and deferred tax consequences of the

activities of the reporting period.

II. Deferred Tax Liabilities

A. A temporary difference causes a future taxable amount if the taxable income will be

increased relative to accounting income in the year(s) when the difference reverses.

B. Such differences create deferred tax liabilities for the taxes to be paid on the future

taxable amounts.

2. Expenses or losses reported on the tax return before the income statement. (T16-5

through T16-11).

III. Deferred Tax Assets

A. A temporary difference causes a future deductible amount if the taxable income will be

decreased relative to accounting income in the year(s) when the difference reverses.

B. Such differences create deferred tax assets for the taxes to be paid on the future taxable

amounts.

1. Expenses or losses reported on the tax return after the income statement. (T16-12

through T16-14)

2. Revenue or gains reported on the tax return before the income statement.

IV. Balance Sheet and Income Statement Perspectives

A. Another perspective starts with the balance sheet effect. (T16-4,

1. An assumption underlying a balance sheet is that assets will be recovered (used or

2. Before that occurs, there is a temporary difference between the book value (also

3. The tax basis of an asset or liability is its original value for tax purposes reduced by

any amounts included to date on tax returns.

B. We can calculate the related deferred tax asset or liability balance by multiplying the

temporary book-tax difference by the applicable tax rate.

V. Valuation Allowance

A. Deferred tax assets are recognized for all deductible temporary differences.

VI. Permanent Differences

A. Permanent differences, are those caused by transactions and events that under existing tax

Part B: Other Tax Accounting Issues

I. Change in Tax Rates

A. A deferred tax liability or asset is calculated using currently enacted tax rates and laws

rather than anticipated tax rates. If a phased-in change in rates is scheduled to occur, the

II. Multiple Temporary Differences

A. A company usually has several temporary differences, both originating and reversing, in

any particular year.

III. Net Operating Losses (NOLs)

A. A net operating loss (NOL) can be used to reduce taxable income in other, profitable

years by either: (T16-24)

2. A carryforward of the NOL to later years (up to 20). (T16-26)

B. The income tax benefit of both an NOL carryback and an NOL carryforward are

recognized for accounting purposes in the year the NOL occurs.

IV. Financial Statement Presentation

A. In the balance sheet, deferred tax assets and deferred tax liabilities are classified as either

current or noncurrent depending on how the related assets or liabilities are classified for

V. Dealing with Uncertainty

A. The means of dealing with uncertainty in tax decisions is prescribed by FASB ASC 740–:

Income Taxes–Overall (previously “Accounting for Uncertainty in Income Taxes, an

1-4 Intermediate Accounting, 8/e

VI. Intraperiod Tax Allocation

A. Intraperiod tax allocation means the total income tax expense for a reporting period is

allocated among the financial statement items that gave rise to it.

Decision-Makers’ Perspective

A. One of the most important aspects of most business decisions is the tax effect.

B. Income tax is one of the largest expenditures many firms incur.

D. Deferred tax assets represent future tax savings.

1. An operating loss carryforward is a deferred tax asset that often reflects sizable

future tax deductions.

P

Po

ow

we

er

rP

Po

oi

in

nt

t

S

Sl

li

id

de

es

s

A PowerPoint presentation of the chapter is available in the Connect library.

T

Te

ea

ac

ch

hi

in

ng

g

T

Tr

ra

an

ns

sp

pa

ar

re

en

nc

cy

y

M

Ma

as

st

te

er

rs

s

TEMPORARY DIFFERENCES

Kent Land Management reported pretax accounting income in

2016, 2017, and 2018 of $100 million, plus additional 2016

income of $40 million from installment sales of property.

T16-1

1-6 Intermediate Accounting, 8/e

DEFERRED TAX LIABILITY

Because tax laws permit the company to delay reporting this

profit as part of taxable income, the company is able to defer

T16-2

RECORDING INCOME TAXES

➢ Each year, income tax expense comprises both the current

and the deferred tax consequences of events and transactions

already recognized. This means we:

($ in millions)

Current Future Future

Year Taxable Taxable

2016 Amounts Amounts

2017 2018 [total]

Pretax accounting income 140

T16-3

1-8 Intermediate Accounting, 8/e

TEMPORARY BOOK–TAX DIFFERENCE

The deferred tax liability each year is the tax rate times the

temporary difference between the financial statement

carrying amount of the receivable and its tax basis.

($ in millions)

December 31

2016 2017 2018

Receivable from

TYPES OF TEMPORARY DIFFERENCES

Revenues (or gains)

Expenses (or losses)

Return Later

recording investments at

Estimated expenses and

recording investments at

fair value or inventory at

Return Now,

but in

the Income

advance

in the income statement

T16-5

1-10 Intermediate Accounting, 8/e

EXPENSE REPORTED ON THE TAX RETURN

BEFORE THE INCOME STATEMENT

To determine taxable income, we add back to accounting

income the actual depreciation taken in the income statement

and then subtract the depreciation deduction allowed on the

tax return.

Woods Temporary Services reported pretax income in 2016, 2017, 2018, and

($ in millions) Temporary Difference:

originates reverses

2016 2017 2018 2019

Total

ACCOUNTING INCOME $100 $100 $100 $100 $400

T16-6

DETERMINING AND RECORDING INCOME TAXES – 2016

Taxable income is $8 million less than accounting income

because that much more depreciation is deducted on the 2016

($ in millions) Current Future Future

Year Taxable Taxable

2016 Amounts Amounts

2017 2018 2019 [total]

Pretax accounting income 100

Temporary difference:

Deferred tax liability:

Journal entry at the end of 2016

Income tax expense (to balance) 40

T16-7

1-12 Intermediate Accounting, 8/e

2017 INCOME TAXES

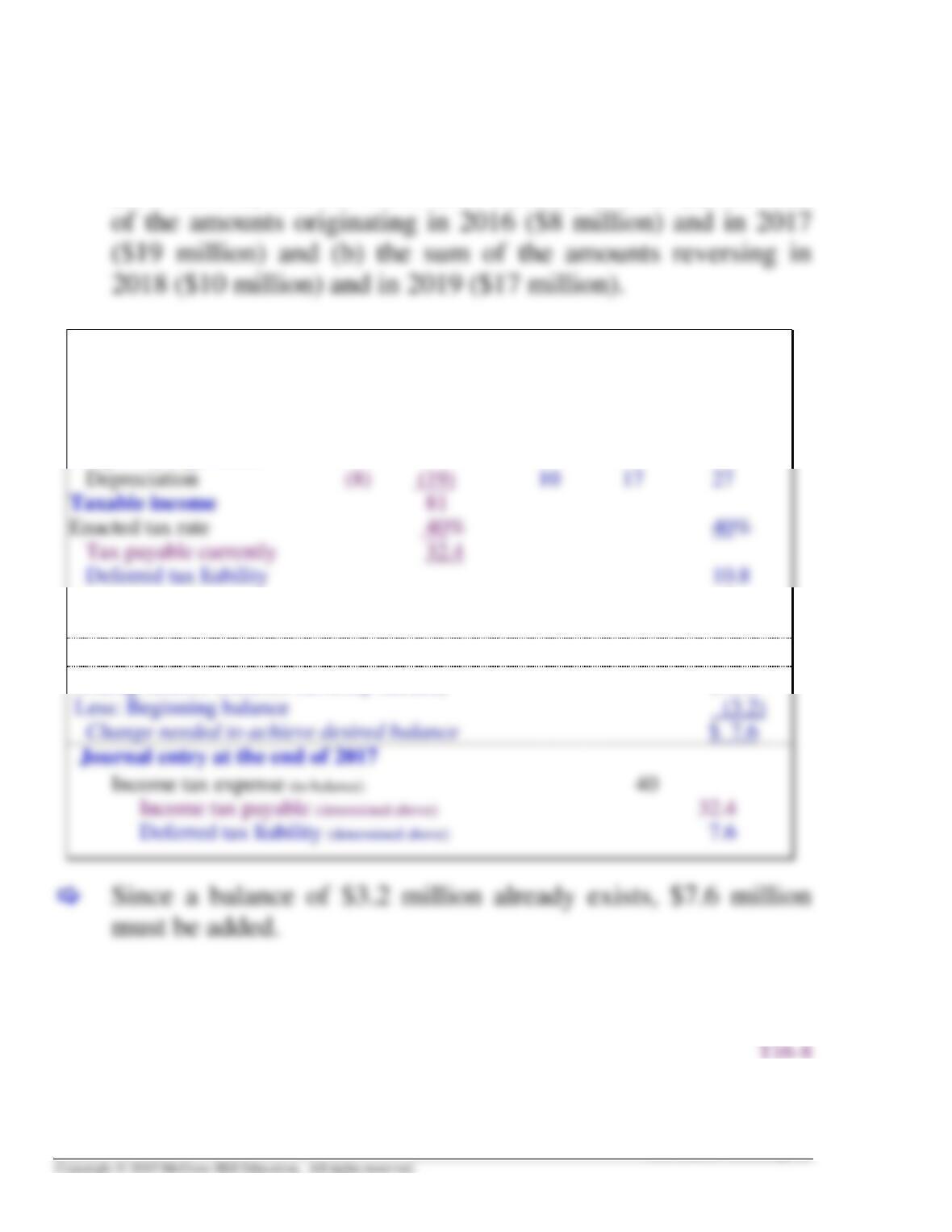

The cumulative temporary difference between the book basis

($50 million) and tax basis ($23 million) is both (a) the sum

($ in millions) Future Future

Current Taxable Taxable

Year Amounts Amounts

2016 2017 2018 2019 [total]

Pretax accounting income 100

Temporary difference:

Deferred tax liability:

Ending balance (balance currently needed) $10.8

2018 INCOME TAXES

A portion of the tax deferred from 2016 and 2017 is now

being paid in 2018.

($ in millions) Future Future

Current Taxable Taxable

Year Amount Amount

2016 2017 2018 2019 [total]

Pretax accounting income 100

Temporary difference:

T16-9

1-14 Intermediate Accounting, 8/e

2019 INCOME TAXES

Because the entire temporary difference has now reversed,

there is a zero cumulative temporary difference, and the

balance in the deferred tax liability should be zero.

($ in millions) Current Future

Year Taxable

2016 2017 2018 2019 Amount

[total]

Pretax accounting income 100

Temporary difference:

Deferred tax liability:

T16-10

DEFERRED TAX LIABILITY

The deferred tax liability increases the first two years and is

paid over the next two years.

Deferred Tax Liability ($ in millions)

7.6 2017 ($19 x 40%)

T16-11

1-16 Intermediate Accounting, 8/e

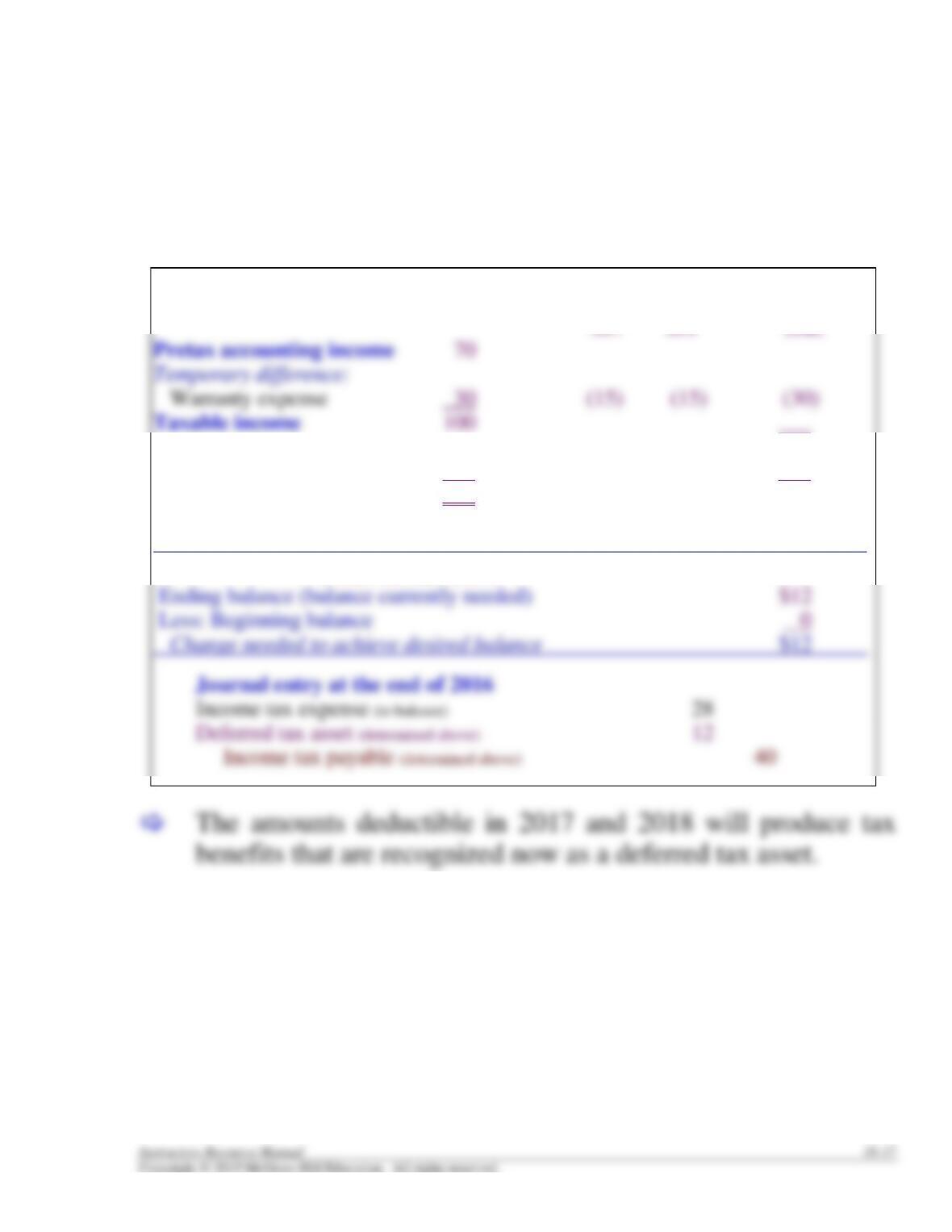

DEFERRED TAX ASSETS

Deferred tax assets are recognized for the future tax benefits

of temporary differences that create future deductible

amounts.

($ in millions) Temporary Difference:

originates reverses

2016 2017 2018

T16-12

RECORDING INCOME TAXES

Because the warranty expense was subtracted on the 2016

income statement, but isn’t deductible on the 2016 tax return,

it is added back to accounting income to find taxable income.

($ in millions) Current Future Future

Year Deductible Deductible

2016 Amounts Amounts

(30)

Enacted tax rate 40% 40%

Tax payable currently 40

Deferred tax asset (12)

Deferred tax asset:

T16-13

1-18 Intermediate Accounting, 8/e

DEFERRED TAX ASSET

At the end of 2016 and 2017, the company reports a deferred

tax asset for future income tax benefits.

Deferred Tax Asset

2016 ($30 million x 40%) 12

If we continue the assumption of $85 million taxable income

in each of 2017 and 2018, income tax those years would be

recorded this way:

2017

Income tax expense (plug) ………. ……………………… 40

VALUATION ALLOWANCE

Deferred tax assets are recognized for all deductible

temporary differences. However, a deferred tax asset is then

T16-15

1-20 Intermediate Accounting, 8/e

PERMANENT DIFFERENCES

Provisions of the tax laws, in some instances, dictate that the

amount of a revenue that is taxable or expense that is

deductible permanently differs from the amount reported on

the income statement.

Interest received from investments in bonds issued by state

and municipal governments (not taxable)

Investment expenses incurred to obtain tax-exempt income

(not tax deductible)

T16-16